The Unintended Consequences of the Federal Reserve's Low Interest Rate Policy

Interest-Rates / US Interest Rates Nov 21, 2009 - 09:06 AM GMTBy: John_Mauldin

Where the Wild Things Are

Where the Wild Things Are

It Is Not Just Japan

The Euro-Yen Cross and the Dollar Carry Trade

Where the Wild Things Are is a beloved children's book and now a beautiful movie. But in the investment world there are really scary wild things lurking about in the hidden recesses of the economic landscape. Today we look at one of the unintended consequences of the Federal Reserve's low interest rate policy.

For quite some time, I have been arguing that we are faced with no good choices, not just in the US but in the entire "developed" world. I see a low-growth, Muddle Through world over the next years (with a double-dip recession just to liven things up). However, that does not mean that we will lack for volatility. Things could get volatile rather quickly. Let's quickly set the background.

It Is Not Just Japan

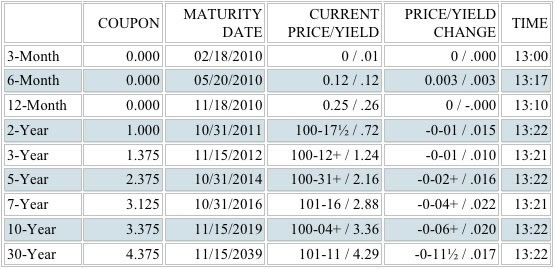

Let's look at today's interest rate picture. Yesterday, we had the bizarre occurrence of banks actually paying the government to hold their cash. Three-month treasuries yield a miniscule 0.01% in interest. If you opt to buy a one-year bill you get all of 0.26%. You can see the entire spectrum below.

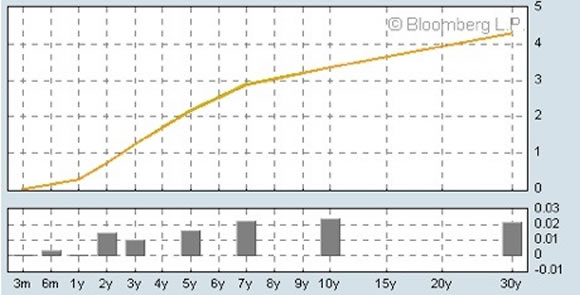

Look at the graph of the yield curve below. It is as steep as we have seen it in a long time. But that is almost the point. Banks are essentially getting free money. If you are a banker and can't make money in this environment, you need to quit and find meaningful employment.

And that is part of the rationale that the Fed espouses with its low interest rate regime. Not only does it allow banks to repair their balance sheets, it also encourages investors to put money into riskier assets in order to get some return on their investments. Over $260 billion has gone into bond funds this year, and just $2.6 billion into stock funds. However, you have to balance that with the fact that some $400 billion has left money market funds paying less than 0.2%. So there is some movement to capture yield.

But is it just banks that are getting cheap money? And is encouraging investors to find riskier assets a sound policy? Maybe not.

The Euro-Yen Cross and the Dollar Carry Trade

I wrote a great deal in the past few years about the strong correlation of the euro-yen cross to stock markets all over the world in general. (The euro-yen cross is the exchange rate of the euro and the Japanese yen.) This was a proxy for the Japanese carry trade. The stock markets of the world rose and fell in synchronization with the yen versus the euro.

A currency carry trade is a strategy in which an investor sells a certain currency with a relatively low interest rate and uses the funds to purchase a different currency yielding a higher interest rate. A trader using this strategy attempts to capture the difference between the rates, which can often be substantial, depending on the amount of leverage used.

The Japanese drove their rates down to essentially zero in the 1990s. By early 2007, it was estimated that the yen carry trade was over $1 trillion. But when the world credit crisis hit, the world wanted dollars. They paid back the yen and bought dollars, driving the yen higher and killing the yen carry trade. Who wants to borrow in a currency that continues to rise, even if the costs are low? And often, large leverage was used, so small movements in the currency could destroy outsized amounts of capital.

But now, there are some who are beginning to ask whether there is a dollar carry trade. In the last nine months, the correlation between the dollar and the stock market has gone to about 90%. If the dollar rises, the stock markets and other risk assets tend to fall, and vice-versa. It would appear that investors and funds are borrowing cheap dollars on a short-term basis and investing in all sorts of risk assets. Not only have stock markets risen, but so have high-yield bonds, commodities, and so on.

We have seen the steepest rise in US stock markets coming out of a recession since the end of the last world war. The market is "discounting" a 5% GDP next year and a profit rebound beyond anything in past experience. Depending on the quarter, operating earnings are expected to rise by anywhere from 30-40%. P/E ratios are back at 23, well above the 17 we saw in the summer of 2007 (I am using 4th quarter 2009 estimates so as to not have to take into account the disastrous 4th quarter of last year.)

Worrying about a dollar carry trade is not just a preoccupation of my friends Nouriel Roubini or David Rosenberg or Frank Veneroso. Look as this story from Bloomberg:

"China's Liu Says U.S. Rates Cause Dollar Speculation

"Nov. 15 (Bloomberg) -- The decline of the dollar and decisions in the U.S. not to raise interest rates have caused "huge" speculation in foreign exchange trading and seriously affected global asset prices, said Liu Mingkang, chairman of the China Banking Regulatory Commission."

"The continuous depreciation in the dollar, and the U.S. government's indication, that in order to resume growth and maintain public confidence, it basically won't raise interest rates for the coming 12 to 18 months, has led to massive dollar arbitrage speculation," he told reporters in Beijing today at the International Finance Forum.

"Liu said this has 'seriously affected global asset prices, fuelled speculation in stock and property markets, and created new, real and insurmountable risks to the recovery of the global economy, especially emerging-market economies.'

"His view echoes that of Donald Tsang, the chief executive of Hong Kong, who said the Federal Reserve's policy of keeping interest rates near zero is fueling a wave of speculative capital that may cause the next global crisis."

"'I'm scared and leaders should look out,' Tsang said in Singapore Nov. 13. 'America is doing exactly what Japan did last time,' he said, adding that Japan's zero interest rate policy contributed to the 1997 Asian financial crisis and U.S. mortgage meltdown."

It is not just China. Brazil has moved to impose a tax (or tariff) on investment money coming into the country on a shorter-term basis, as they are worried about both a bubble in their markets and in their currency. Russia is openly considering similar policies.

I have been doing a lot of speaking in the last month. In almost every speech, I warn of the significant imbalance in the dollar. I walk to the very end of the stage to help illustrate that the world now has on a massive ABD trade. By that I mean Anything But Dollars. Everyone is now on the same side of the boat. They have borrowed dollars to buy other risk assets, assuming that the dollar, like the yen in the glory days of the yen carry trade, will continue to fall. Dollar bears are everywhere.

Explanations abound for why the dollar is a trash currency. It is Fed policy, or the Obama administration's willingness to run massive deficits, or the trade deficit or our health-care policy or (pick any number of issues). But I wonder.

Global trade collapsed last year and well into this year. Global trade was essentially done in dollars. If global trade is down 20% or more, then there is less need for companies in various countries to hold dollars and more need for local currency because of the crisis. Thus, after a rush to safety in the credit crisis, there is a rational selling of dollars by business.

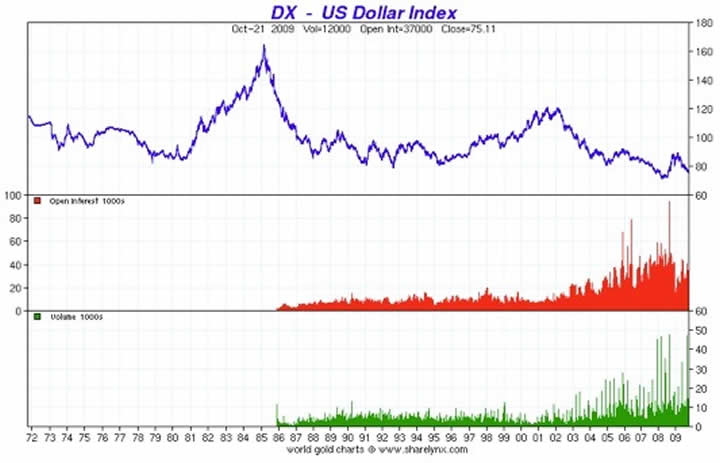

Look at the above chart. Notice that the dollar is roughly where it was 20 years ago. And notice the recent jump during the credit crisis. We are not even back to where we were before the crisis.

What happens if world trade picks back up, as it appears to be doing? Admittedly, it is not a robust recovery as yet, but it is rising. That means more need for dollars. And dollars which are being borrowed (and probably leveraged!) on the assumption the dollar will continue to fall.

And I agree that, over time, the case for the dollar is not as good as I would like. But in the meantime, we could have one very vicious dollar rally, which would take equity markets down worldwide, along with other risk assets. Why? Because it would be a major short squeeze.

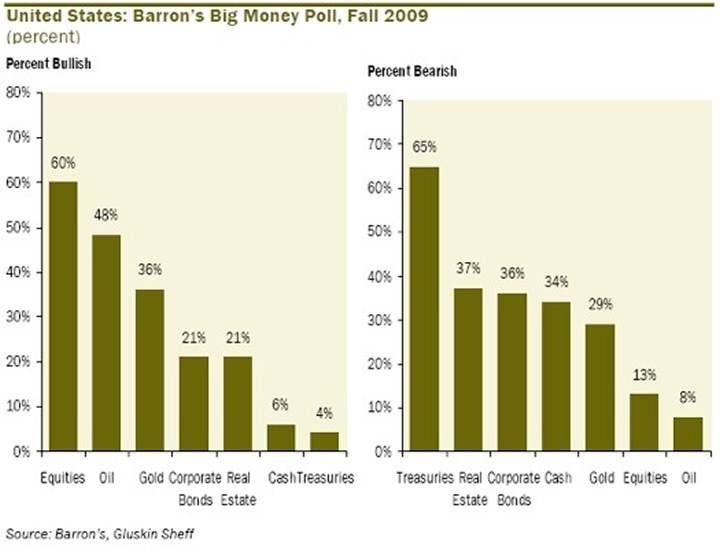

Barron's just did a survey. It revealed that the bullish sentiment on stocks is quite high and almost everyone hates US treasuries (graph courtesy of David Rosenberg of Gluskin, Sheff)

Whenever sentiment gets too strong in one way or the other, it is usually setting up the markets for a rally in the despised asset. Mr. Market like to do whatever he can to cause the most pain to the largest number of people.

I am not predicting a near-term crash or imminent precipitous bear, although in this environment anything can happen. I am merely noting that there is an imbalance in the system. The longer this imbalance goes on, the more likely it is that it will end in tears. And the irony is that a recovering world economy could be the catalyst.

The Wild Things? They may be hiding in a portfolio near you. Just food for thought. Stay nimble.

New York, London, and Switzerland

I am going to hit the send button on what may be the shortest e-letter I have ever done. The travel is catching up with me and I need some rest.

I am looking forward to Thanksgiving next week. It may be my favorite holiday. Family, friends, food, and football. My usual pattern is to get up very early Thursday and start the prime slow-cooking, and then turn to the side dishes. It will be no different this year. My brother will bring the smoked turkeys, which he has down to an art form. And then there are the over-the-top wines I was so graciously given this past birthday by so many friends. I will bring a few of those bottles out.

The next weekend I am in New York for Festivus with the crowd from Minyanville, and then I am home for over a month before I go to London and Switzerland in late January. Then not much is currently scheduled until April, although it always does seem to change. After the recent hectic schedule (15 cities and even more speeches in just a little over three weeks), I look forward to some home time.

I wish those of you in the US the best of Thanksgivings, and the rest of you a great week. And thanks for all the very kind words of late about Tiffani. She seems to be doing better. She is due in a month, so she is still moving slowly, but you can sense the excitement in her and Ryan. I find it all very pleasant.

Your "there's no place like home" analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.