Vintage Wine Turns Sour for Financiers

Stock-Markets / Investing 2010 Feb 05, 2010 - 12:24 PM GMTBy: Doug_Horning

Alex Daley and Doug Hornig, Casey Research write: When the folks at a private equity firm gather at the holiday party refreshment table to talk about “vintage,” they aren’t commenting on the Château Pétrus.

Alex Daley and Doug Hornig, Casey Research write: When the folks at a private equity firm gather at the holiday party refreshment table to talk about “vintage,” they aren’t commenting on the Château Pétrus.

The world of private equity financing doesn’t have high visibility, but it is big business behind the scenes. Unlike venture capital outfits – which provide startup money to very early-stage companies – those who play this game grab existing private companies, often through leveraged buyouts (LBOs). Each year’s investments are referred to as vintages, with some being more highly drinkable than others.

Now, some of the recent vintages look like they’ll turn out to be little more than vinegar.

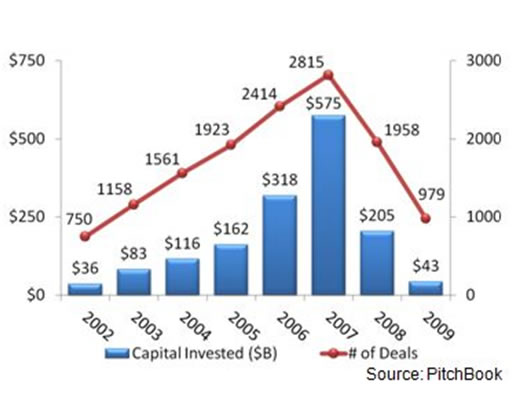

Private equity investing has never been for the faint of heart. But investors continue to engage in it, because the payoff can be substantial. And for the first few years of the new millennium, it was a go-go place to be. With so much easy money sloshing around, the number of PE deals exploded, totaling over half a trillion dollars at the manic peak in ’07.

Then came the crash:

It’s important to remember that credit was not a single bubble. It was a bubble machine. It created the housing bubble, which fueled the personal debt bubble (which in turn popped the housing bubble, but that’s another story). The mortgage market gave birth to a whole new range of derivatives, things like collateralized debt obligations (CDOs), mortgage-backed securities (MBSs), and the rest of the acronyms we’ve all become familiar with, even if we don’t quite understand what they do. (Don’t be embarrassed, neither did the financial geniuses who swapped them like baseball cards.)

Frantic trading in these newly printed scraps of paper created its own bubble, manufacturing an incredible amount of seeming liquidity in a very compressed time frame. We know the ultimate consequences to the balance sheets of our banks, and our government, by now. But there was more to it than that. The capital these transactions threw off had to go somewhere, and suddenly well-capitalized investors were pouring their phantom profits into something perceived as more solid: private equity firms. Presto, yet another bubble.

In a mania, all investments are at the mercy of the greater fool. As in: if you can’t find one, you’re it. Doesn’t matter if we’re talking housing, stocks, commodities, or whole companies. The last man standing is left staring into an abyss in which there are no buyers.

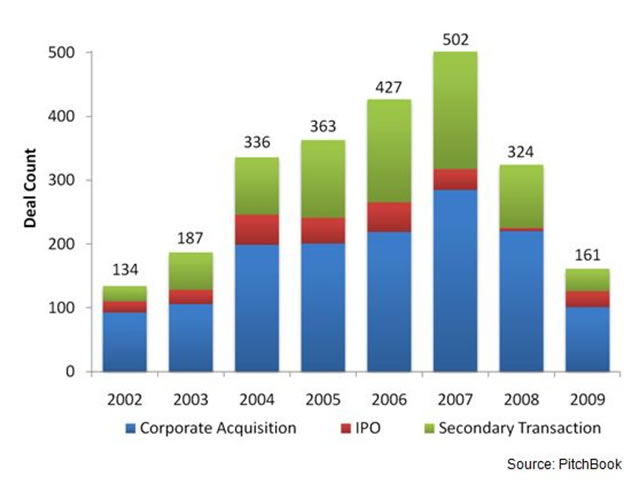

With PE deals, investors don’t acquire companies because they want to own them. They buy in because they expect to sell to a higher bidder. Here are their three exit strategies:

- wait until the company goes IPO and clean up when you sell your stock into the liquid public markets;

- arrange for a takeover by a corporate entity; or,

- pawn it off on another PE firm in a secondary transaction.

And this is what’s happened in those areas over the past eight years:

Compare the two graphs, and it’s immediately apparent that PE firms are sitting on a lot of properties that’ll be difficult to move. They invested an unprecedented amount right at the same time as the bottom was falling out of an overheated exit market, returning back to normal levels of deal flow in just two short years.

Furthermore, while it looks like IPOs in general recovered a bit in 2009, they still totaled just 25 from the ranks of PE-backed companies. And even that number may be misleading. According to PitchBook, a respected industry analyst, “a number of these IPOs did not represent full exits but were used as a means of raising capital to pay down debt and provide investors with partial returns.”

It Only Gets Worse

At the same time, much of the huge money stack they piled up through ’07 is still there. It doesn’t move because, in the current environment, there’s no point in adding more companies when they can’t profitably dispose of the pile they already have. And that’s led to a boatload of uninvested capital – a massive cash overhang estimated at some $400 billion:

Excess Funding + a Bloated Portfolio = ??

Well, that is the question. First of all, you can save the pity you might slop onto these firms. They are, after all, making some kind of return on the money they hold. Beyond that, though, we’re looking at the potential for some pretty vinegary vintages.

Generally, the wait time for a vintage to mature – i.e., for the investment to show a profit – is about five years. So the more than $1 trillion thrown into PE firms between 2005 and 2007 will be expected to yield fine wines from now through 2012.

Whether, instead, we’ll hear only whines, no one can say for sure. But for comparison purposes, we can look at PE’s sister market, venture capital. In a recent analysis of VCs, investment advisor Cambridge Associates reported that returns were off steeply from their heyday in the early ’00s, falling from 36% to 14% just following a similar flood of increased inflows during the early part of last decade. A similar decline in returns from private equity investments – with lower risk and lower expectations than VCs – could take them down into the single digits, if not close to or below zero. You might as well be in T-Notes.

The takeaway is this: Private equity fuels the IPO market, as well as the growth pipeline for big companies that can't grow only organically.

But PE firms are sitting on the equivalent of a bunch of drunken Vegas marriages, having pledged “till death do us part” at the top of the frothy debt market. All those unwanted spouses in the portfolio mean lower gains.

Add in the excess capital, much of which may end up being recalled by investors tired of waiting for it to be invested, and the big firms – which grew cocky playing with billions in this once-lucrative market – are likely in for some lean years.

What does all this mean to you as an investor?

Well, you need to be wary of IPOs; many of the dogs will be trotted out, with tails wagging and mouths closed to hide the rotting teeth.

Also on the way are diminished returns for the banks and insurance companies that back the PE guys. And if equity prices remain at recent highs, there will probably be a shakeout in the industry, as increasing numbers of companies look to global public markets to raise money, instead of turning to private equity. A trend that’s already apparent with the incredible number of secondary offerings over the past few months (in just two days this past September, nine were filed or priced on U.S. markets), and the thawing global IPO market.

But remember that every crisis holds danger as well as opportunity. That’s the specialty of the editors of The Casey Report: to analyze emerging mega-trends and find the best opportunities to profit from them. And if you go along for the ride, you will be able to do the same. To learn more about how to make money in a roller-coaster economy, click here.

© 2010 Copyright Casey Research - All Rights ReservedDisclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.