EXTEND & PRETEND: Uncle Sam, You Sly Devil!

Interest-Rates / Credit Crisis 2010 Apr 30, 2010 - 10:20 AM GMTBy: Gordon_T_Long

The modus operandi (MO) of deviant behavior aids investigators in doing criminal profiling. Forensic accounting takes a similar approach and leads us to some unnerving conclusions about Uncle Sam. As Tax Payers we place our sacred trust in our elected officials and government. Is that trust being handled similarly to how Goldman Sachs apparently has been handling its fiduciary responsibilities?

The modus operandi (MO) of deviant behavior aids investigators in doing criminal profiling. Forensic accounting takes a similar approach and leads us to some unnerving conclusions about Uncle Sam. As Tax Payers we place our sacred trust in our elected officials and government. Is that trust being handled similarly to how Goldman Sachs apparently has been handling its fiduciary responsibilities?

Has our government been playing accounting games like European tax payers discovered in Greece and like many angry tax payers are now discovering in local, city, state and sovereign governments across Europe and the US? All are now learning how the use of off balance sheet accounting and cleverly structured Interest Rates Swaps have been applied to obscure visibility to toxic debt levels from the very tax payers who will be responsible for the debt obligations.

Has our government been playing accounting games like European tax payers discovered in Greece and like many angry tax payers are now discovering in local, city, state and sovereign governments across Europe and the US? All are now learning how the use of off balance sheet accounting and cleverly structured Interest Rates Swaps have been applied to obscure visibility to toxic debt levels from the very tax payers who will be responsible for the debt obligations.

Is our government playing the role of Jack Nicholson in “A Few Good Men” when he condescendingly justified his behavior, yelling in the courtroom: “You can’t handle the truth!”

If you can handle the truth then let me explain some very suspicious behavior of our trusted Uncle Sam.

WHALES MAKE WAVES

In two recent articles in the Extend & Pretend Series, I laid out eight suspicious anomalies that few professionals can presently explain.

Though there are more suspicious anomalies than the above list reflects, I want to add a ninth before we proceed with attempting to make sense of them.

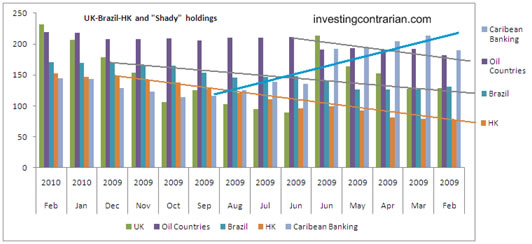

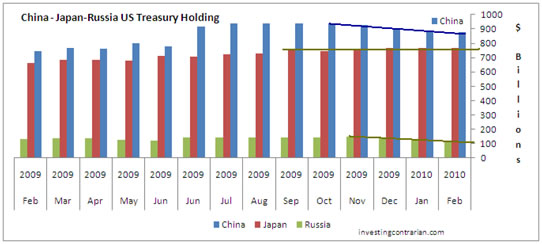

SUSPICIOUS CLUE #9 – US TREASURY PURCHASES ARE SUDDENLY COMING FROM THE CARRIBEAN & UK (Channel Islands)

The “tooth fairy” which I described as part of Suspicious Clue #2 in Extend & Pretend – Gaming the US Tax Payer appears to reside in the Caribbean and UK Channel Islands. The ‘tooth fairy’ was the name I gave to the mysterious direct bidder that has emerged in the US Treasury Auction to stop the bond auction from being a failure. A failure would scare the market and would result in a sudden and dramatic increase in US Treasury interest rates.

The ‘Tooth Fairy’ Residence

THE BALANCING ACT

To understand the shorter term actions we are seeing in our table of suspicious clues above, it is important to place them in the following context:

1- Uncle Sam as represented by the US Treasury, with a $14 TRILLION debt load, must do everything in its power to keep Interest rates as low as possible for as long as possible.

1- Uncle Sam as represented by the US Treasury, with a $14 TRILLION debt load, must do everything in its power to keep Interest rates as low as possible for as long as possible.

2- Placing too much supply on the US Treasury Auction which doesn’t match buying demand will drive interest rates up and possibly spook the market. This would elevate rates to even higher levels. Indirect Bids are already steadily falling.

3- The US Treasury must balance monthly revenue receipts with monthly outlays to ensure sufficient funds are available. This means the rate of change in tax receipts is critically important. Tax receipts are already below reduced budget estimates. ‘Over the first six months of the fiscal year, personal income tax receipts net of refunds are actually down significantly – 8.4%. Reflecting last year’s sharp drop in personal income, final tax settlements on 2009 returns are running about 11% below year-earlier levels, and refunds (as reported in the Daily Treasury Statement) have been up about 5%.’ (2)

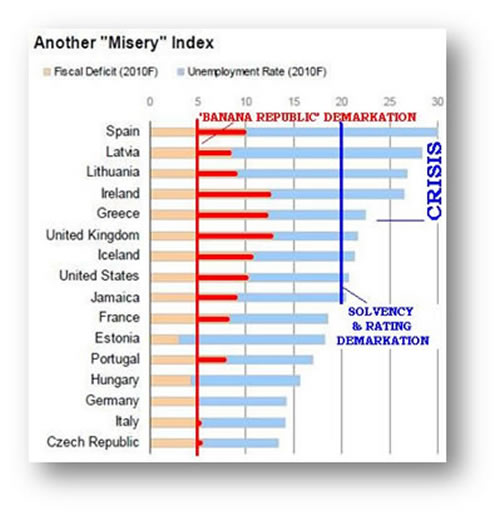

4- Historically sovereign countries faced currency crisis and debt funding problems when fiscal deficits rose above 5%. The IMF’s harsh restrictions were imposed when these levels were approached. The EMU Maastricht Treaty rules restricted debt to 3% of GDP. The 2010 US Government Budget estimates presently reflect a 10.7% deficit.

5- When unemployment rises on top of heavy fiscal deficits, serious problems become even more critical. Tax revenues plummet when unemployment is high and consumer purchases fall. US unemployment as reflected by U3 is presently reported at 9.8%. The broader U6 measure reflects approximately 17%. According to Government Shadow Statistics the actual unemployment is closer to 22%. This is why the public is so skeptical with what the government tells them. It doesn’t match what they see in their neighborhood and hear from friends and family.

6- The actual size of total sovereign debt is also important versus the annual fiscal deficit financing needs. It isn’t just the percentage of budget that interest payments are consuming (US interest payments are presently net 14% of budget) but also the supply of the rollover of existing debt financing requirements. Once again the US faces major difficulties in this matter because the US Treasury has been steadily reducing maturity duration over the last few years.

6- The actual size of total sovereign debt is also important versus the annual fiscal deficit financing needs. It isn’t just the percentage of budget that interest payments are consuming (US interest payments are presently net 14% of budget) but also the supply of the rollover of existing debt financing requirements. Once again the US faces major difficulties in this matter because the US Treasury has been steadily reducing maturity duration over the last few years.

7- The US is facing the strong possibility of a future credit downgrade. This would also raise funding costs significantly which are not planned for in the already massive deficit budgets. “The Aaa rating of the U.S. is not guaranteed" - Moody's!

With all these interconnected elements playing out simultaneously, it is an incredibly difficult job to orchestrate them in a controlled and managed fashion. It is not credible to believe everything could be working this well by simply matching monthly receipts with outlays and issuing bonds at the monthly treasury auctions to make up the difference. For anyone that has actually managed cash flows you know you require more tools than these. The public is being very naïve to the complexities involved. This is why cash flow management receives so little scrutiny. Those few doing any analysis have no exposure to the management realities.

PRIMA FACIA - WHERE IS UNCLE SAM?

I have written extensively about the unregulated, non-exchange traded, offshore, off balance sheet (OTC) $605 Trillion derivatives market and specifically about the $437 Trillion Interest rate swap market. In Sultans of Swap: the Getaway I laid out some of the court actions taking place throughout Europe and the US at all levels of government. Below is a summary of those findings along with governments where the use of Interest rate Swaps is publicly documented.

This list includes only those Interest Rate Swap deals that have become problematic or which I have written about. The Service Employees Union (SEIU) has additionally documented an extensive list that was published by the Wall Street Journal: This study by the Service Employees International Union, was commissioned to demonstrate the broad based seriousness of the problem.

The question is: Where is Uncle Sam?

Surely the largest debtor in the world, with the biggest financing challenges in the world, where the whole structured finance industry was born, where the banking industry has near monopolistic control over congressional legislation through its $1 Million/day army of lobbyists succumbed to the ‘forbidden fruit’. Surely Uncle Sam did not take the high road for fear of hurting the tax payer when almost every local, city, state and sovereign country appears to have. Not to have defies common sense, yet that is precisely what we are led to believe. Similarly we were told by Alan Greenspan that no one could see a bubble before it burst and by Goldman that they never saw the housing bubble collapse coming. Sorry gentlemen, you long ago lost my confidence in believing almost anything you tell me.

What makes it even more suspicious is there is absolutely no mention of interest rate swaps anywhere in the hundreds of government accounting reports I have read over the years. Surely you would think Uncle Sam might have occasionally tried the ‘forbidden fruit’ in at least some minor ways. No – nothing! Like a cat burglar – clean as a whistle – a professional job.

What makes it even more suspicious is there is absolutely no mention of interest rate swaps anywhere in the hundreds of government accounting reports I have read over the years. Surely you would think Uncle Sam might have occasionally tried the ‘forbidden fruit’ in at least some minor ways. No – nothing! Like a cat burglar – clean as a whistle – a professional job.

The closest you find that Uncle Sam even knew Swaps existed is that at almost the instant the financial crisis hit in 2008 Uncle Sam immediately executed a massive and highly complex Currency Swap with the EU to attempt to put liquidity into the system. Uncle Sam clearly understood the instruments in minute detail to make this happen on such a grand scale and so fast. Yet we are to believe the $605 Trillion Derivative market has nothing to do with our trusted Uncle Sam. I am sorry, I am from Missouri. Show me this is true!

MY ASSUMPTIONS

Renowned physicists Albert Einstein and Stephen Hawking have suggested that to solve the big problems, big leaps of faith must be made in your assumptions. They allow you to get outside of the box and see what has been obvious all along. This is what I propose to do.

I am therefore going to work on the premise Uncle Sam is a MASSIVE player in the Interest Rate and Currency Swap Market.

I am also going to assume that with discovery a significant percentage of the exponential growth of the $605 Trillion derivatives market could be traced in some manner to Uncle Sam.

Having adopted this perspective, our suspicious clues suddenly become obvious effects of such participation.

I have intentionally not previously speculated in any of my Sultans of Swap series and Extend & Pretend series articles. For the remainder of this article I am going to lay out my personal speculation based on these assumptions. Your e-mails have overwhelmingly requested this.

MAKING SENSE OF THE SHORT TERM SUSPICIOUS CLUES

HOW COULD THIS BE DONE

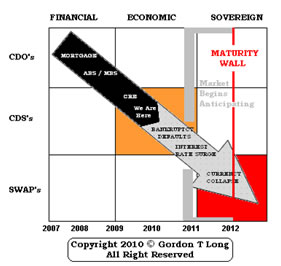

I have taken the uncovered Greek Kitlos PLC structure that exposed the magnitude of the Greek accounting ‘games’ and which has now placed Greece on the verge of financial collapse and used it has a guiding model. It is very clear that a similar structure could be used in the US. Goldman Sachs clearly had a ‘cookie cutter’ solution which it took to Greece.

Where the recipe was origianlly developed we likely will find out during the next financial crisis.

THE FOLLOWING GRAPHIC IS AN EXAMPLE ONLY. IT DOES NOT REPRESENT THIS IS ACTUALLY OCCURRING NOR DOES IT REPRESENT THAT THE PLAYERS LABELLED IN THE DIAGRAM ARE OR EVER HAVE PARTICIPATED IN SUCH A MANNER. THE FLOWCHART DOES NOT REPRESENT THAT THIS IS THE ONLY WAY SWAPS COULD BE USED

IT IS A REPRESENTATIVE EXAMPLE ONLY AND IS FOR ILLUSTRATIONAL PURPOSES ONLY.

For further explanation: See Kitlos PLC Structure & Sultans of Swap: Understanding %605 Trillion in Derivatives.

RELATING OUR SUSPICIOUS CLUES (SC) – SC# 1-9

If demand was not sufficient to meet supply because it was falling off (SC#1 and SC#3), then the proposed structure would provide funds to purchase US Treasuries at the Treasury Auction as Direct Bidders (SC#2). The Direct Bidders would have to come from offshore havens (SC#9) so it wouldn’t be readily apparent that there was a US Treasury funding arrangement. If it was widely understood then its purpose would not be successful.

Collateral from PPP/PFI assets would need to be posted and it would likely require further direct deposited funds at the US Treasury to achieve full collateral coverage (SC#6).

Presently US banks are being recapitalized by the use of an extraordinary steep yield curve, this along with major accounting changes was the most expedient political solution to the insolvency of the US banking industry instead of being nationalized as was debated at the onset of the financial crisis. The spread between the 10 Year US Treasury and the Fed Discount / Primary credit rate is over 3%. This is a high that has only been seen a few times in the last 30 years. In the few other times, inflation was also never this low. Is it any wonder that bank profits just released are eye popping?

Borrowing short and lending long is the basis of banking, but seldom have we ever made it this profitable or easy for the banks. All of these actions are at the tax payers’ expense. With 30 Year Treasury Bond yields minus the 6 month CD at a high only seen twice before since 1986, it discourages private savers. As Adrian Ash points out in “How the Banks Print their Money”:

"In effect," gasps one commentator, "American taxpayers are now subsidizing the profits of Wall Street." He puts the profit at "200 basis points and up."

"The easiest and most profitable risk-adjusted trade for the banks," swoons another, "is to borrow billions from the Fed...and then to lend the money back to the US Treasury. The imbedded profit – of some 2.5 percentage points – is an outright and ongoing gift from American taxpayers to Wall Street."

But where's the shock? American and British taxpayers have long subsidized Wall Street and the City. Progressively more so over the last 25 years, sure. Without any payback since 1981, in fact. And spectacularly so during the last 3 recessions, too. Just check out those peaks above!

But 'twas ever so, at least since "Big Bang" in the mid-1980s. Nothing much in this scam is new. Banks print money, quite literally and despite the monopoly that the Fed and Bank of England apparently hold. Only the pace of production has picked up as the number of forgers has shrunk, leaving a small but swollen cartel of banks running the racket. And to keep the cops off their back, they've got tax-payers hostage, and will keep them tied up, for as long as "saving the banks" – instead of just letting them fail – remains the approved political fix.

I was tempted to include as SC#10 - the fact that the Federal Reserve hurriedly added paying interest on bank reserves deposited at the Fed during the financial crisis. Bank reserves required by law and any additional funds above the minimal requirements now earn interest. This has never been done in the history of the Federal Reserve. I raise it now because it seems strange to pay banks to hold reserves above minimal requirements when the major concern is that banks are not lending. Why would you reward this behavior? Is it possible we are rewarding the banks for buying US Treasuries which would then be held on deposit at the Federal Reserve? Think of the profit on this arrangement. The banks borrow unlimited funds from the Federal Reserve at nearly zero interest rates, and then buy US Treasuries at close to 3.5%. The banks then put the notes on deposit at the Federal Reserve and are paid interest on the face value of the Treasuries. Of course the fool in all this is “we the tax payer”.

If alternative financing was being used then sudden lending spikes at commercial banks (SC#4) would likely be seen when urgent cash management funds were needed or a monthly Treasury Auction was going to be possibly uncovered. You would also see inflows into government outlays (SC#8) when receipts were too light and had the potential to be a shock and possible contagion catalyst to the Treasury Auction.

You would also expect to see Interest Rate Swap Spreads between the 10 Year US Treasury notes to also plummet and possibly go negative (SC#5).

To keep this whole gig going with low perceived low inflation you would require an extraordinary complacent Gold and Precious Metals market (SC#7).

Of course this is just one person’s view.

CONCLUSION

What I have attempted to do with my speculation is to create a ‘straw man’. It is intended as a starting point from which to begin the discovery process for the truth. I am likely wrong in a number of areas. That is part of discovery. Someone has to put themselves out there to begin the dialogue. I look forward to hearing from readers who can add to the discovery of the real truth.

GOVERNMENT SACHS TELL US THE TRUTH

"You want the truth? You can't handle the truth. Son, we live in a country with an investment gap. And that gap needs to be filled by men with money. Who's gonna do it? You? You, Middle Class Consumer? Goldman Sachs has a greater responsibility than you can possibly fathom. You weep for Lehman and you curse derivatives. You have that luxury. You have the luxury of not knowing what we know: that Lehman's death, while tragic, probably saved the financial system. And that Goldman's existence, while grotesque and incomprehensible to you, saves pension funds. You don't want the truth. Because deep down, in places you don't talk about at parties, you want us to fill that investment gap. You need us to fill that gap. "We use words like credit default swaps, collateralized debt obligation, and securitization? We use these words as the backbone of a life spent investing in something. You use 'em as a punchline. We have neither the time nor the inclination to explain ourselves to a commoner who rises and sleeps under the blanket of the very credit we provide, and then questions the manner in which we provide it! We'd rather you just said thank you and paid your taxes on time. Otherwise, we suggest you get an account and start trading. Either way, we don't give a damn what you think you're entitled to!"

As Posted on Calculated Risk

SOURCES:

(1) 03-25-10 - SULTANS OF SWAP: The Get Away! Gordon T Long

(2) 04-26-10 - Goldman Sees A $10.8T Budget Deficit In Next Decade, Focuses On Subpar Tax Receipts ZeroHedge

For the complete unabridged version of this article see: EXTEND & PRETEND

For the complete Extend & Pretend series: Commentary

Gordon T Long gtlong@comcast.net Web: Tipping Points

Mr. Long is a former executive with IBM & Motorola, a principle in a high tech start-up and founder of a private Venture Capital fund. He is presently involved in Private Equity Placements Internationally in addition to proprietary trading that involves the development & application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. While he believes his statements to be true, they always depend on the reliability of his own credible sources. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments.

© Copyright 2010 Gordon T Long. The information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. Please note that Mr. Long may already have invested or may from time to time invest in securities that are recommended or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.