Stocks Somersault Into the Red But European Debt Crisis Won't Derail U.S. Economy

Stock-Markets / Stock Markets 2010 May 03, 2010 - 05:48 AM GMTBy: Money_Morning

Jon D. Markman writes: Stocks somersaulted into the red early last week in the wake of European debt downgrades, rising revulsion over the prospect of a bailout of Athens and a broad re-pricing of risk. Breadth was negative, the number of new highs shrank and number of new lows swelled. Financials tumbled and retailers stumbled. Caution flags are rising.

Jon D. Markman writes: Stocks somersaulted into the red early last week in the wake of European debt downgrades, rising revulsion over the prospect of a bailout of Athens and a broad re-pricing of risk. Breadth was negative, the number of new highs shrank and number of new lows swelled. Financials tumbled and retailers stumbled. Caution flags are rising.

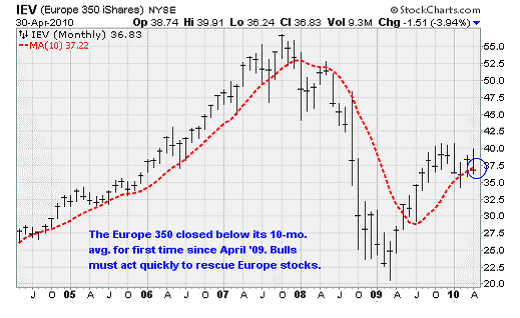

The news that's unnerving world markets was a downgrade of Greek and Portuguese debt. The move pushed Greece's two-year note yield to 17% and shot down the euro, both of which are highly destabilizing. The broadest measure of large-cap European stocks, the Europe 350 (IEV) closed below its 10-month average for the first time in a year.

Long-time subscribers know we treat this level very seriously, as it tends to distinguish well between bull and bear cycles. The $36.83 close on April 30 is ominous for European equities; another month this weak would likely lead straight to a new bear cycle for the Continent.

In the United States, the NYSE suffered two intense days of downside with a two mild days of recovery in the middle. This cluster of selling intensification boosts the probability of the start of a more extensive market correction than anything seen in the past two months.

However, 90% downside days are typically followed by two to seven rally days, at minimum. This is because these broad, heavy declines usually exhaust the energy of individuals wishing to sell. That's exactly what transpired after the last 90% downside day: It's been seven days of advances until the Tuesday splat.

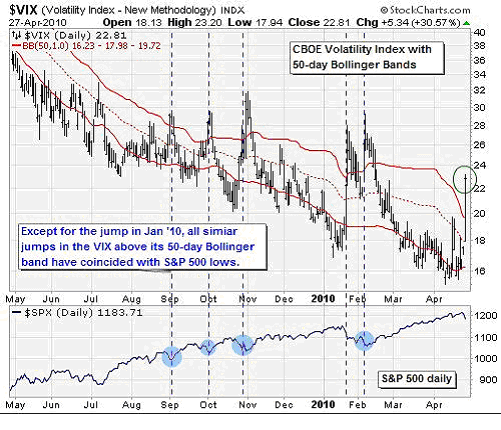

But breadth is not destiny, and there is more to the story. From a technical point of view, the Tuesday decline took the S&P 500 down to support established during the reaction low of April 19, around 1,183 for the benchmark index. That may very well satisfy technicians. If it doesn't, then the next support is around 1,152 near the April 8 reaction low. Also, as you can see in the chart above, all similar spikes in the CBOE Volatility Index (VIX) in the past year have coincided with local lows, except the one in late January, when the low came a week later after only moderate additional losses.

So from a technical point of view we are left with the picture of an intense desire to dump shares and avoid buying near a top. It's easy to see how the desire to sell could become contagious as bears try to press their bets. The VIX rose 30% this week, its biggest one-day move since October 22, 2008, a measure of just how extreme the price change was.

There is more at stake here than just technical patterns. The news was unsettling and since we have seen this movie before -- just two years ago, around the Lehman Brothers bankruptcy -- we kind of know what can happen next.

But is it really all bad? Well if you step back from the fray a moment you can see that outside of Greece the economy in Europe has been getting a lot better lately. Sure, borrowing costs are higher in Greece and Portugal now, but costs are now actually lower for the rest of the continent since there has been a rush to buy the stronger European countries' sovereign debt; German two-year bund yields plunged this week. And of course a lower euro is helpful to European exporters.

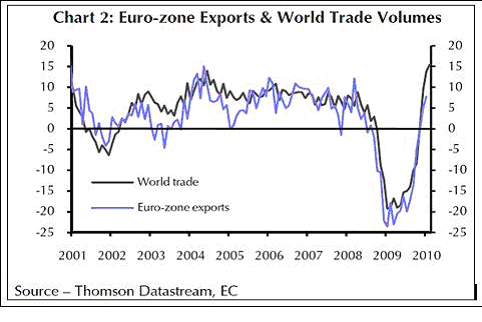

Another possible positive impact could be the scare effect that this situation is having on the rest of Europe. Other governments, from London to Bonn, are showing greater restraint in their budgeting process, and plans for tax cuts in Germany, in particular, were shelved this week. And all this is happening at a time when Euro-zone exports are improving dramatically, as shown in the chart above. So optimists might say that the dark cloud overhanging Europe could have a silver lining, while pessimists say that the cloud itself is growing darker.

Let's not forget that just last week, the economic strength overseas was very impressive. ISI Group reported on improved industrial strength in Germany and Poland, rising retail sales in Canada, rising exports in Mexico and Japan, including machine tool orders, as well as Taiwan employment and exports and even Indonesian auto sales.

ISI's global economic diffusion index -- which is a measure that adds up all pluses in the world economy and subtracts the negatives -- hit a record high by a wide margin last week. A main driver is the decline in interest rates (outside of Greece, of course) and narrower corporate bond spreads. Add it up all up, and global growth is on track to hit +5.1% year-over-year in the second half.

But what does this all mean for U.S. stocks? If there's a contagion similar to the winter of 2008, it means a lot. Yet there's no guarantee that it will play out that way, especially since central banks and governments developed a new set of countermeasures back then, and the overall economy is on a much sounder footing.

Back in 2008 the U.S. economy was in the middle of its worst recession since the early 1980s. Right now we're in the middle of our strongest recovery since the mid-1980s. Corporate earnings and revenue are growing rapidly, and the quality of those earnings are good. We have seen countless times in the past that weak economies can be crushed by shocks, while strong economies are more bulletproof. It's the difference in being exposed to a cold virus when you've run down from lack of sleep and travel vs. being exposed when you are healthy.

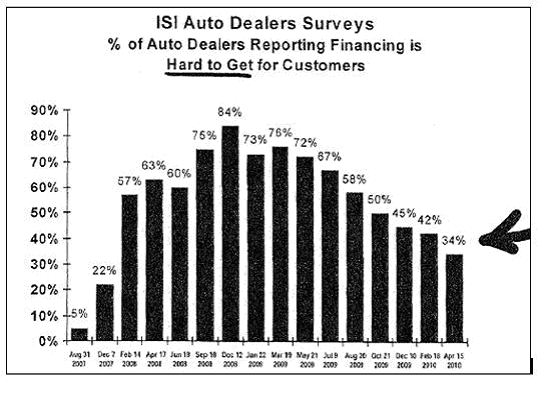

The 13-month rally off the March 2009 lows has restored $21 trillion to equity markets that had evaporated during a two-year bear market. Just in the past week, we've seen exceptionally positive reports and boosted guidance by U.S. powerhouses Apple (NASDAQ: AAPL), E. I. duPont de Nemours & Co. (NYSE: DD), United Parcel Service Inc. (NYSE: UPS), Ford Motor Co. (NYSE: F) and Family Dollar Stores Inc. (NYSE: FDO). Much of this is driven by the wider availability of consumer credit than you may have thought given negative media coverage. The chart above shows that the percentage of auto dealers reporting that financing is 'hard to get" for consumers has been dropping sharply in the past year and now rests right around 2007 levels.

More companies beat expectations in Q1 this year than in any quarter in the past two decades, and the momentum is actually expected to be higher in the second quarter. Cyclical economic strength and investment sentiment favoring these companies is not going to change on a dime no matter how troublesome the debt fiasco in Europe becomes. S&P 500 earnings are on track for a 54.2% increase this year at almost $88, and that's on a 19.2% surge in sales.

Let me point out that these are not small matters or isolated to certain areas of the economy that are helped by government spending (though some are). As ISI points out, there's been a 14.7% annualized increase in existing house sales, and home prices are up 3.6% annualized in the past three months. And housing affordability -- driven by higher wages and lower rates -- is now the highest on record. Moreover apartment rents continue to improve, and are up briskly in the past seven months straight. Vehicle sales are rising at a 25% annualized rate.

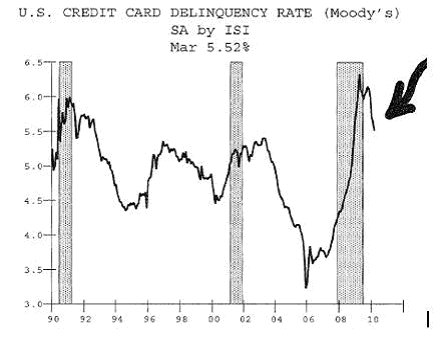

And just to show how consumers' health is improving, note in the chart above that the U.S. credit card delinquency rate has fallen sharply this year from the 2009 peak in the same way that it fell out of prior recession highs. Wells Fargo & Co. (NYSE: WFC) last week reported that delinquencies declined across all of their major consumer loan portfolios -- not just cards. That goes for companies too. Low-rated corporations that wish to issue "junk" bonds can do so at a new low rate of 8.02%, vs. the peak of 22.5% a year ago.

In summary, although the trouble in Europe is non-trivial, it comes at a time when the global and U.S. economy is much more capable of withstanding a hit. That doesn't mean U.S. earnings and share prices won't suffer from exposure to Europe's woes, but it does mean they're much less likely to be completely derailed.

Week in Review

Monday: Caterpillar Inc. (NYSE: CAT) and Whirlpool Corp. (NYSE: WHR) both reported better-than-expected earnings. CAT earned 50 cents per share against the 39 cents analysts were expecting and the year-ago result of 29 cents. WHR earned $2.13 per share against a $1.33 consensus estimate and the 91 cents earned in the year ago period.

Tuesday: Ford Motor Co. (NYSE: F) reported better-than-expected quarterly earnings of 46 cents per share against the 31 cents analysts were expecting and the 75 cents per share loss reported in 2009. The Case-Shiller Home Price Index recorded its first year-over-year increase in nearly four years in February, but posted a 0.9% month-over-month decline. The price action suggests the recovery in housing remains tepid.

Wednesday: The Federal Reserve concluded with two-day policy meeting with no change to its interest rate policy target of zero to 0.25%. The Fed noted that while the economic continues to strength and the labor market is beginning to improve, low interest rates are still appropriate for an extended period.

Thursday: Exxon Mobil Corp. (NYSE: XOM) reported a slight miss, with earnings of $1.37 per share against the $1.41 analysts were expecting. Initial weekly jobless claims dropped slightly, to 448k, but remains troublingly high. Jobs creation is the last piece of the economic recovery puzzle.

Friday: First quarter GDP growth came in at 3.2% versus the 3.4% consensus estimate. Although down from the 5.6% growth seen in the fourth quarter of 2009, there were important improvements seen in consumer spending. Also, the University of Michigan's consumer sentiment index jumped to 72.2 compared to a consensus estimate of 71. The improvement was led by a 4 point increase in the expectations sub-index.

The Week Ahead

Monday: An update on personal income and the manufacturing sector via the ISM Manufacturing Index. Analysts expect the ISM index to move further into expansionary territory with a reading of 61 compared to March's 59.6 as factories across the country come back online.

Tuesday: Motor vehicle sales for April should remain at the 8.8 million seasonally adjusted annual rate reported in March.

Wednesday: The ISM Non-Manufacturing Index will provide an update on activity in the larger services sector. Analysts expect the index to increase to 56.4 for April from March's 55.4 result. Remember that any reading over 50 indicates expansion.

Thursday: Chain store sales and initial weekly jobless claims.

Friday: The all important employment situation report for April will provide an update on the unemployment rate and the change to payrolls. Analysts are looking for +200,000 jobs on the payroll side and a slight improvement in the unemployment rate to 9.6%. Early indications of jobs strength, such as an increase in temporary employment and a longer average work week, suggest robust job creation is on the way.

[Editor's Note: As this market analysis demonstrates, Money Morning Contributing Writer Jon D. Markman has a unique view of both the world economy and the global financial markets. With uncertainty the watchword and volatility the norm in today's markets, low-risk/high-profit investments will be tougher than ever to find.

It will take a seasoned guide to uncover those opportunities.

Markman is that guide.

In the face of what's been the toughest market for investors since the Great Depression, it's time to sweep away the uncertainty and eradicate the worry. That's why investors subscribe to Markman's Strategic Advantage newsletter every week: He can see opportunity when other investors are blinded by worry.

Subscribe to Strategic Advantage and hire Markman to be your guide. For more information, please click here.]

Source : http://moneymorning.com/2010/05/03/european-debt/

Money Morning/The Money Map Report

©2010 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or 72 hours after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.