The Eurozone Stimulus Package and Economic Fundamentals

Economics / Global Debt Crisis May 21, 2010 - 02:19 AM GMTBy: Frank_Shostak

On Monday, May 10, eurozone officials presented a stimulus plan involving $1 trillion. The main reason for the package, as stated by officials, is to prevent European economies from falling into an economic black hole on account of the economic crisis in Greece.

On Monday, May 10, eurozone officials presented a stimulus plan involving $1 trillion. The main reason for the package, as stated by officials, is to prevent European economies from falling into an economic black hole on account of the economic crisis in Greece.

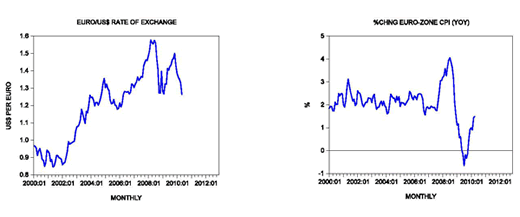

Another factor that prompted the European leaders to come up with the massive stimulus package is the desire to arrest the slide of the euro. After climbing to $1.51 in November 2009 the price of the euro in US dollar terms plunged to around $1.26 in early May — a fall of 16%.

Another factor that prompted the European leaders to come up with the massive stimulus package is the desire to arrest the slide of the euro. After climbing to $1.51 in November 2009 the price of the euro in US dollar terms plunged to around $1.26 in early May — a fall of 16%.

There is a concern that an uncontrolled fall in the euro could accelerate the rate of increase in price inflation. Note that after falling to −0.3% in September last year, the yearly rate of growth of the consumer price index (CPI) jumped to 1.5% in April.

The stated intent of eurozone leaders to defend the euro at any price seems to be contradictory given that the European Central Bank (ECB) on May 10 started pumping money into the economy by buying government bonds on the secondary market. Observe that the growth momentum of the ECB balance sheet has been trending up since January this year. The yearly rate of growth climbed from −6.8% in January to 11.5% in the first week of May.

Eurozone policy makers were quick to suggest that the ECB monetary pumping via the purchase of government bonds of weak economies such as Greece, Portugal, and Spain is meant to stabilize financial markets.

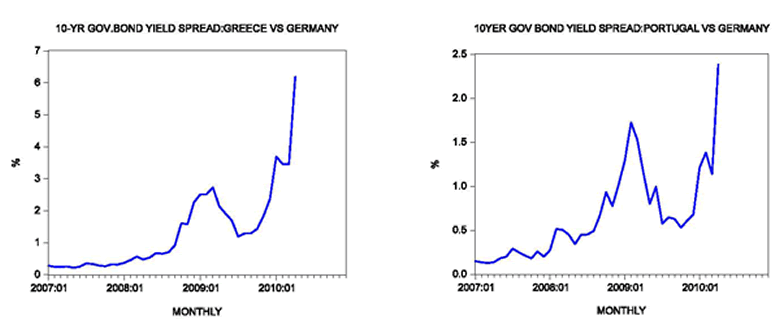

What they mean by stabilizing the markets is to suppress the widening of the yield spread of the Greek, Spanish, and Portuguese government debt against the German government debt. For instance, in April the spread on the 10-year Greek government bond stood at 6.2% against 3.7% in January while the Portuguese spread stood at 2.4% against 1.2% in January.

Trying to suppress the symptoms without addressing the causes behind the widening in the spread can only make things much worse. Clearly, investors are now assigning a much greater risk to Greek versus German government bonds given the fact that the Greek economy is in much worse shape.

Eurozone policy makers have also suggested that this pumping is not inflationary because it will be neutralized by an appropriate monetary policy of the ECB — the monetary pumping by the ECB is not going to lift the money-supply rate of growth, it is held.

Irrespective of these statements, what matters is what the ECB balance sheet is doing — as we have seen, it has been on a rising growth path since January this year.

Some other experts are of the view that the role of the central bank is to accommodate the demand for money. In this sense an increase in the supply of money in response to the increase in the demand for money is not inflationary, so it is held.

Given the widening yield spread, clearly — it is held — we have a strong increase in the demand for money. Failing to accommodate this demand, it is argued, can seriously damage the monetary system.

Regardless of demand, any monetary pumping sooner or later will lead to an exchange of nothing for something, which will weaken the real-wealth-generation process.

Now, can the $1-trillion package fix the underlying problems of Greece and other eurozone economies? I.e., can it improve the ability of some European governments to service their debt?

This ability is dependent on the wealth-generating process of the private sector of the economy and not a reshuffling of nominal debt ratios. The stimulus package, which really amounts to income redistribution, will only weaken further the wealth-generating process.

Another important factor that undermines this process is the reckless monetary policy of the ECB.

What we currently observe in Greece and other European economies is an economic bust brought about by a visible decline in the growth momentum of the money supply.

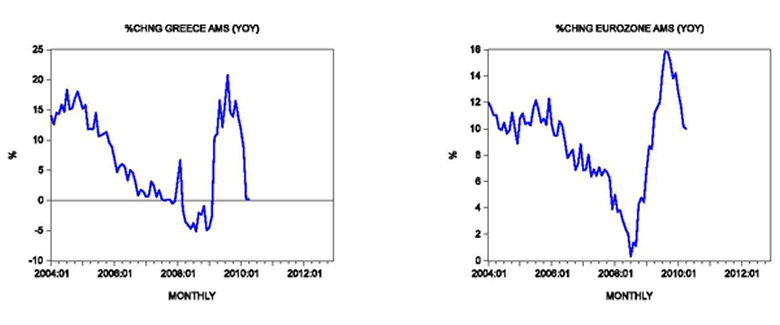

After rising to 20.8% in August last year, the yearly rate of growth of Greece's AMS fell to 0.2% by April this year.[1] The yearly rate of growth of the eurozone's AMS fell from 15.8% in August last year to 10% by April.

The sharp fall in the money-supply rate of growth is currently putting pressure on various nonproductive — i.e., bubble — activities that emerged on the back of the previous strong increase in money-supply rate of growth.

Note that increases in the growth momentum of money out of "thin air" divert real savings to bubble activities. A fall in the growth momentum weakens the diversion and thus weakens bubble activities.

While a fall in the growth momentum of money is good news for the wealth-generating process, ever-growing government activities have continued to undermine this process.

In 2009, Greek government outlays rose by 104% from 1999. Also in Spain, government outlays have continued to push ahead, rising by 119% in 2009 from 1999, while in Ireland the rate of increase stood at 157%.

The relentless increases in government outlays implies a persistent diversion of real savings from wealth-generating activities to nonproductive activities, i.e., consumption of real capital. Obviously, this undermines the process of real-wealth generation.

So, rather than curtailing government outlays and eliminating various nonproductive activities, the rescue package coupled with a loose ECB is actually going to further reinforce nonproductive activities. Obviously, this cannot be good news for the eurozone.

Conclusion

On Monday, May 10, eurozone officials presented a $1-trillion stimulus plan to prevent the eurozone economies falling into an economic black hole. To reinforce the plan, the European Central Bank (ECB) was forced by eurozone officials to step in with monetary pumping to provide a quick fix to financial markets. Such policies can only make things much worse — it is not possible to create something by printing money and redistributing real wealth. All that such policies produce is a further economic impoverishment.

Frank Shostak is an adjunct scholar of the Mises Institute and a frequent contributor to Mises.org. He is chief economist of M.F. Global. Send him mail. See Frank Shostak's article archives. Comment on the blog.![]()

© 2010 Copyright Ludwig von Mises - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.