European Commission Fires Big Guns, Euro TARP!

Interest-Rates / Credit Crisis 2010 Jun 01, 2010 - 02:25 AM GMTBy: HRA_Advisory

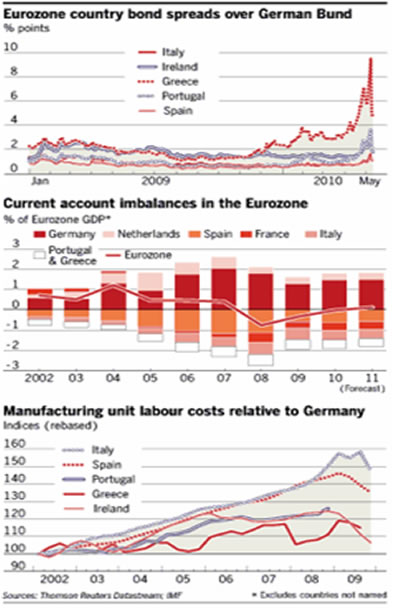

The European Commission brought out the big guns. In a move intentionally reminiscent of the US TARP program, leaders of the continent’s major economies promised to keep throwing money at the problem in bulk until some of it stuck. The set of charts below (courtesy of the Financial Times of London) gives a good graphical representation of the crisis to date.

The European Commission brought out the big guns. In a move intentionally reminiscent of the US TARP program, leaders of the continent’s major economies promised to keep throwing money at the problem in bulk until some of it stuck. The set of charts below (courtesy of the Financial Times of London) gives a good graphical representation of the crisis to date.

The “good news” can be seen in the top chart that depicts sovereign bond spreads against German bunds (their equivalent of Treasury bonds), It’s not a pretty picture overall, but the drop in yields in the past two weeks points to at least grudging acceptance of EuroTARP by bond vigilantes. Like the reaction to the US program 18 months ago this might simply reflect a belief that it doesn’t pay to bet against a trader that can print its own money.

The “good news” can be seen in the top chart that depicts sovereign bond spreads against German bunds (their equivalent of Treasury bonds), It’s not a pretty picture overall, but the drop in yields in the past two weeks points to at least grudging acceptance of EuroTARP by bond vigilantes. Like the reaction to the US program 18 months ago this might simply reflect a belief that it doesn’t pay to bet against a trader that can print its own money.

That is pretty much the mindset EuroTARP was created to instill. Stripping away the dogma on both sides of the trade, bond yields are really about trust. Traders either believe a government, or a committee of governments in this case, is willing and able to support the market or they don’t. The 750 billion Euro package had enough shock and awe to calm the bond markets a bit but yields are still high and unlikely to be back to “normal” for the foreseeable future. Rising LIBOR rates and large drop in the amount of bank and commercial credit issuance in Europe is also worrisome if it continues.

It will take months for the market to know if the plan is working. Until then, markets will be more risk averse and will discount lower growth in the Euro region as austerity programs start to bite. This is turn is leading to fears of knock on effects in other markets, particularly the BRICs. That is especially apparent in the base metal space and the Shanghai stock exchange which has dropped about 20% in the past month or so. Longer term wagers will continue to be made on the survival of the Euro itself. Anyone who has looked at a Euro/Dollar chart lately knows which way those bets have been running.

The Euro is getting pummeled, having been knocked down 20% in the past six months and there is no sign the selling is about to end. The lower chart helps explain the skepticism. It compares unit manufacturing costs in several countries to Germany. All of the southern Eurozone countries have become significantly less competitive against Germany through the past decade. This is not due to pay rates, which are much higher in Germany but to productivity. Most of the southern, weaker, economies simply took the upgrade in incomes when they joined the Euro as a bonus rather than a competitive loss that has to be corrected. Germany is famous for productivity growth and cost control. Its one reason it’s the world’s most successful exporter.

Some of the PIIGS have a long way to go to get competitive and generate growth in incomes. It’s easy to make a case that some of these countries may be forced to leave the Euro and that; really, it would be the best thing for them. That, however, is not the same as saying the Euro as a currency would “fall apart”. The collective debts of Greece, Ireland and Portugal would not exceed the damage the Lehman Brothers bankruptcy created even in the case of a 100% write-off. If the contagion effects can be addressed the fund for buying Club Med debts now being set up should be adequate. At that level the market is over-reacting but it won’t calm down unless traders decide larger economies won’t be sucked into the same black hole. Given how much slower growth in Euroland could be the haircut markets and the Euro itself are getting make sense. The jury is definitely still out on the survival of the currency itself however and the core Eurozone countries remain committed to it.

All this uncertainty has been working in gold’s favor. Gold has made a number of important new highs and is still firmly above $1200 US per ounce. Relative to equity markets gold has been a pillar of strength for the past few weeks, rising to all time nominal highs in virtually every major currency. Gene Arensberg, who created the Got Gold Report which focuses on the precious metals markets and activities of the large Comex traders, noted over the weekend (May 16-17) that the pattern seen in the latest price rise is different from the action in late 2009. Some categories of “commercial” traders have been decreasing their short positions as the price rose, a very different reaction from the last run up. For those that want to get Gene’s insights into the esoteric world of gold market “commitment of traders” reporting we highly recommend the free blog he recently created which you can access at http://www.gotgoldreport.com.

In our view, gold is trading more and more as an independent currency. We would expect currency based trading to be more stable than fear buying, which is also going on. The list of countries starting up the printing presses continues to grow. The ECB is now planning to embark on a campaign of quantitative easing; something it insisted would never happen only a few days ago. As more people view the fiat currency race to the bottom as back on, more funds have moved into gold. Fear buying will reverse if things calm in Europe but the currency view seems like its here to stay. How much running room that could give gold would depend on what currency it’s traded against. It’s worth remembering that gold’s leverage in the currency arena is high. The entire gold market is barely a rounding error compared to the foreign exchange market.

Silver has followed gold but remains more volatile. Silver, platinum and palladium have all been quicker to show weakness as equity markets fell. This is a reflection of the mainly industrial demand for PGE metals and that silver still has some industrial drag holding back its currency cachet. Silver made a one year high and while is has yet to exceed its 2008 peak near USD$21, that target is within reach if gold has another surge.

The big moves in recent sessions have come on the base metal side. After a couple of weeks of downtrend, copper and other base metals experienced one day losses of about 6% today (May 17). That is the largest downward move in the past 18 months. We have of course been expecting this sort of weakness and it’s no surprise given recent growth concerns. As always, China will be the driver for this market.

There are concerns that China’s amazing growth will finally falter under a renewed debt crunch. Statistics that bear this out have yet to appear but most traders view this as only a matter of time. We are not quite that pessimistic ourselves. Rumours of China’s economic decline have been premature and exaggerated so far so we are waiting to see new economic stats before we assume too much. What we can say at this point is that base metal prices are getting closer to our comfort level and that western inventories continue to decline along with prices. We view this as evidence that most of these stockpiles are probably held by end users and not just speculators ready to flood the market at the first sign of weakness. That is good news but metals will still need to find a bottom before base metal producer and exploration stocks get any traction. We’re not there yet but are getting closer.

If there is any silver lining this month it’s that the rush to safety has bailed out the US Treasury yet again. The flood of safe haven seekers has made it easy for the US to keep selling bonds. The turmoil also means that interest rate increases in either the US or Europe are not likely in the near term. Zero interest rate policies have been a major (some would say only) boon for equity markets. The correction we are in will have to run its course but continued loose money policies should help support markets.

Market weakness also means Beijing is likely to stall an upward revision of the Yuan Dollar exchange rate. We don’t think this is the best move and it does open the door for more friction later in the year. Given how strong the US$ has been China can at least fall back on the argument that the Yuan is rising against most other currencies. The euro on the other hand is at least giving exporters in Europe some blessed relief. That is hardly enough to save the day but it should mean continued good earnings for exporters. More market weakness is possible, even likely given the mess the sovereign bond markets are in, but the real economy still seems to be on the mend.

Ω

To view Eric Coffin’s latest video interview on Industry Watch with Al Korelin, please go to: http://www.youtube.com/.. [April 12, 2010]

Gain access to potential gains of hundreds or even thousands of percent! HRA initiated coverage on 8 new companies in 2009. So far, the average gain on those companies is over 250%! For more information about HRA Advisories, please visit: www.hraadvisories.com

By David Coffin and Eric Coffin

http://www.hraadvisory.com

David Coffin and Eric Coffin are the editors of the HRA Journal, HRA Dispatch and HRA Special Delivery; a family of publications that are focused on metals exploration, development and production companies. Combined mining industry and market experience of over 50 years has made them among the most trusted independent analysts in the sector since they began publication of The Hard Rock Analyst in 1995. They were among the first to draw attention to the current commodities super cycle and the disastrous effects of massive forward gold hedging backed up by low grade mining in the 1990's. They have generated one of the best track records in the business thanks to decades of experience and contacts throughout the industry that help them get the story to their readers first. Please visit their website at www.hraadvisory.com for more information.

© 2010 Copyright HRA Advisory - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

HRA Advisory Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.