Housing Market Impact on the US Economy, Should the Fed Cut Interest Rates?

Interest-Rates / US Interest Rates Sep 09, 2007 - 01:05 AM GMTBy: John_Mauldin

In this issue:

The Shocker in the Employment Numbers

The Shocker in the Employment Numbers

Should the Federal Reserve Cut Interest Rates?

Will A Cut Make Any Difference?

How Housing Woes Hurt the Rest of the Economy

Home Again, Home Again

The unemployment numbers came in today, and if you look under the hood of the data, it is worse than the headline loss of 4,000 jobs. Should the Fed cut the interest rates in two weeks? Will it make a difference? Are we headed into recession (as predicted here in my January 2007 forecast issue)? When do we see a bottom in the housing market? Are we there yet? We look at all this and more. It should make for an interesting letter, if I can get my jet-lagged body to cooperate.

But first (and quickly) let me mention that I will be at the venerable New Orleans Investment Conference October 21-25. This is the grand-daddie of all investment conferences and features some of the top investment analyst and minds in the country. Among the many speakers are James Grant, Ann Coulter, Lawrence Lindsey, and good friends Marc Faber, Dennis Gartman, Doug Casey. Click on the link and then click on faculty to see what is one of the highest quality gatherings of top-notch speakers at any conference anywhere. You should check it out, especially if you have an interest in gold and natural resources, as some of the top investment analysts in that area are always there. If you are there make sure and look me up.

And quickly, speaking of gold, it is soaring. It closed at over $700 today, in partial reaction to the awful employment numbers, which was not good for the dollar. But there is another interesting story going on in the background, pointed out to me earlier this week by that South African gold maven Prieur du Plessis. He points out there is a massive build-up of call options in the October and December Comex gold contracts, similar to a period in November 2005 prior to the gold price surging by more than 50%. Smart money? Maybe. But the recent 6% move or so may not be all there is in the "barbarous relic."

The Shocker in the Employment Numbers

Economists surveyed by Bloomberg expected that payrolls would increase by 100,000. Instead they dropped by 4,000. That is the first drop since August of 2003. The weakness was broad based and payrolls for both June and July were revised down, from 92,000 to 68,000 in July and from 126,000 to 69,000 in June. That is an average of less than 46,000 a month for the last three months. The economy needs to create 150,000 jobs a month in order for employment not to rise.

Technically, there was a drop of 35,000 in September of 2005, but it was later revised upward to 105,000, a rather large swing. But that brings up a point. The employment numbers are subject to large revisions, especially at major turning points in the economy. The employment data is based on a survey of businesses called the establishment survey. It tends to miss jobs created at small businesses at the economy expands. Thus, the jobless recovery of 2002-2005 was not really jobless at all when the revisions came in over the next few years. The Bureau of Labor Statistics (BLS) makes the survey and then based on past data trends, heavily influenced by recent trends, makes an estimate as to the number of new jobs.

A large part of the unemployment figure is from the so called "birth/death ratio." They estimate the numbers of new jobs created or destroyed each month based on past history. This is the main source of the "under" during the recovery phase, but the converse is also true. It will almost always overestimate the number of new jobs as the economy slows, and especially before a recession.

This month the BLS estimated 120,000 new jobs in the birth/death column. These jobs may not in fact be there if the economy is slowing as it seems to be. There are good reasons to suspect that the August number will be revised down at a later date, as were June and July.

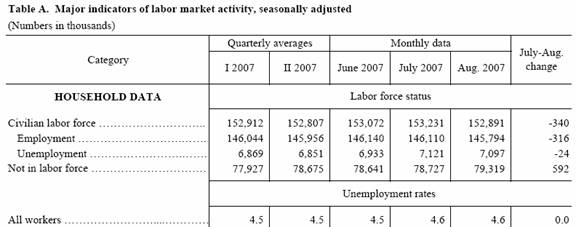

But it may be worse. The BLS conducts two surveys. One is the "establishment survey" mentioned above. The second is the "household survey" where they phone households and ask how many people in the household are employed, are seeking employment or are not in the market for a job.

I reprint the table from their website below ( www.bls.gov ). The number of unemployed people in this survey actually fell slightly, but notice that it also shows a drop of 316,000 jobs last month. Further, they show a rise of 592,000 people who are no longer considered to be in the work force! That is a total swing of over 900,000 workers, or about 0.5% of the labor force. That is a rather large swing in this series.

Finally, and in the "it's probably just a coincidence category," all the research that shows that employment for low wage jobs, especially among teenagers, actually decreases, especially initially, as the minimum wage rises. The new minimum wage kicked in starting July 24, with the rate rising from $5.15 to $5.85. And teenage unemployment rose by almost 6% from July to August. Got to be coincidence. Congress wouldn't do anything to hurt teenage employment, would they?

Should the Federal Reserve Cut Interest Rates?

Looking at the chart below, notice that 2 year rates on US government is at 3.9%. The rate on the ten year bond is at 4.38%. The spread on TIPS (the markets best guess on inflation) is hovering just above 2%. And Fed funds are at 5.25%. The market is screaming for a rate cut.

As I have noted in previous letters, getting an inflation number lower than 2% in the next few months is going to be hard because of the rather low year over year comparison numbers of the latter part of 2006. And the various Fed governors have been telling us that inflation is their primary concern in speech after speech. Cutting rates before we see a lower inflation number is something they have clearly indicated that they are not interested in.

Bernanke and others have made it clear that they do not see it as their job to bail out borrowers who took out home loans they could not pay, or lenders who made risky loans or investors who bought the loans. The fact that the Fed helped create the low interest rate environment which fostered such excessive risk taking is not something they have yet acknowledged.

After today's unemployment number, the futures market is pricing in a rate cut for the September FOMC meeting. If they do not get it, their will be lynch mobs forming. You do not want to be long the S&P of there is no rate cut. It will be ugly. The arguments I have heard and read (not necessarily mine) go like this:

The economy is slowing down. We may even be looking at the possibility of a recession. Recessions are by definition deflationary, so whatever concerns you have about inflation will go away. If the Fed waits until the backward looking inflation data comes in, it almost guarantees a recession.

Further, the credits markets are in the worst crisis in decades. Financial institutions do not trust each other, as there is not transparency. The commercial paper market is in the process of imploding. Mortgages, except for government back agency paper, are not being written or is being done is at very high rates. Want a jumbo loan today? It could cost you 9%, if you can find it, even with good credit. Please, Chairman Bernanke, could we have at least 50 basis points to make the problem go away?

Finally, the housing market is on the verge of a collapse. Foreclosures are high and rising. We need lower rates to help homeowners and jump start the housing market so it can recover.

Will A Cut Make Any Difference?

Now, for what it's worth, here's my view. I think the Fed should cut rates in September. The economy is indeed in the process of slowing down and I think, for the reasons I outline below, is on the verge of a recession. The Fed policy is now clearly quite tight. A 50 basis point cut will still leave real rates at around 2.75%, which is not exactly an easy monetary policy.

But let's be clear. A fed cut is not going to solve, or even help much, the current credit crisis. The problem, as I have repeatedly said, is not a liquidity problem but a credibility problem. There is plenty of cash, and central banks around the world are adding to it daily.

The problem is that no one wants to buy debt that they do not completely understand. If you are a bond buyer for an institution, it is a career ending decision to buy an asset backed investment grade bond even rated AAA if it goes bad. You might be able to explain buying such assets last spring. Buying a problem bond today and it is now your fault, not to mention your job.

And commercial paper from another financial institution? How much subprime debt do they have hidden on off-balance sheet vehicles? Why loan anyone money for just a few extra basis points when you can't be 100% sure? Especially if you are looking at your own exposure and you see how easy it might be to hide a few problems here or there.

These problems are going to be worked through. I have personally talked to more than a few managers who are raising money to create distressed debt funds to buy this paper at discounts, as there are going to be lots of funds and institutions that will be forced to sell asset backed paper. For instance, if you are a pension fund, bank or insurance company that by law can only hold rated paper, and when the ratings agencies mark the subprime paper that you own down below investment grade, you will be forced to sell.

But the question is who will buy? Those who own these bonds and are forced to sell are going to take large losses. The hedge funds that buy them will have the potential for some very good profits. That helps the markets in general, as it helps "clear" the market and allows things to get back to normal more quickly. But the losses for those who are forced to sell will be larger than for those who can sit it out. (It might help for regulators to relax the holding period for those assets as long as they are properly priced in the portfolio.)

A lower Fed funds rate might make the bonds slightly more valuable. But if your A-rated subprime paper is selling for 50 cents on the dollar (and some are), the extra value that even a 150 basis point Fed funds cut would make is only a few points in value. Small consolation.

On a side note, the higher rated asset backed paper is bouncing back rather significantly from the lows of mid-August, although still at steep discounts. The lower rated (BBB and below) is still near their lows. The market is starting to make the distinction between various types of debt, and that is good. The first part of the process, which is to establish some realistic pricing, is at least starting.

Second, a lower fed funds rate is not going to bail out the housing market. It will of course help some, but again, it is not the interest rates that are the problem. The problem is that we are talking about the 20% plus of the home buyers in the last two years that were able to buy homes because of poor lending practices on the part of mortgage companies. Those home buyers are not going to be there to support the market.

Further, let's say that we could wave a magic wand and allow the millions of home buyers who bought homes on adjustable rate and teaser rate mortgages to somehow refinance their homes at reasonable rates, even though their homes are going down in value. For those who qualified on 2% teaser rates, even if they could get a 7% mortgage, the payment might be too much.

Goldman Sachs suggests home values could drop as much as 20%. Gary Shilling has been saying 25%. We don't have time and space this week to go into housing prices, but many of the mortgages sold in the past two years only made sense in a housing market that was rising by 10-15% a year. A market that is dropping 10-15% a year, as it may do in the next 12 months, is only marginally be helped by a Fed funds cut.

But that does not mean they should not cut. They should, simply because the economy is clearly slowing, and the risks are now to the downside.

How Housing Woes Hurt the Rest of the Economy

I have maintained for a long time that the bursting of the housing bubble would cause a serious slowdown or a recession in the economy. My critics would counter that housing is only 5-7% of the economy and a housing recession would not be enough to drag the whole economy down.

They are wrong for the following reasons. First, rising home values have allowed homeowners to use their homes as an ATM through mortgage equity withdrawals, which have added almost 2% to GDP annually over the last five years. That is now evaporating.

Secondly, falling home construction and lower home sales means fewer jobs not just in the direct home building market, but in the parts of the economy related to the home building markets, like mortgage brokers, real estate agents, hardware and furniture, etc. As an example, Countrywide announced a planned 10-12,000 person lay-off, when just a few weeks ago they were thinking of expansion, as they now think new mortgages may drop 25% in 2008. Fewer jobs mean lower consumer spending.

Consumers are not going to spend as much due to the wealth effect. If you feel your house was going to be a major part of your retirement, and now the value is going down, you are going to be more cautious and actually think about saving. This has been a dangerous prediction for 50 years, but I think consumer spending, some 71% of the US economy, is due to slow down. Year over year growth could drop below inflation later this year.

Further, with all the additional homes coming onto the market due to foreclosures, hone values are going to drop even more, and new home construction, which peaked at an annual run rate of 2,000,000 homes per year, is likely to fall to less than 1,000,000. We are currently at a level of 1,400,000, so we are not yet close to the bottom.

Rising unemployment. A housing market looking at the deepest recession in values since the Great Depression. A consumer under siege. A visibly slowing economy.

The Fed should cut rates. It will not be enough, but it will be something.

The Bush administration needs to augment those cuts with programs to help those who could make their mortgage payments if they could get a reasonable rate to be able to do so. Not a bailout of lenders, but help to those caught in the whiplash of a mortgage market that is rapidly freezing up for many.

Further, the rating agencies need to quickly move to increase transparency on the ratings of structured vehicles, investment banks need to figure out how to create credible structured products, etc.

But that is another story for another letter. For now, the Fed needs to cut. And at least 50 basis points, please.

Home Again, Home Again

I rather enjoyed my vacation, but now I need to rest up. As usual for me, I tried to do too much in too little time, but it was fun. I want to thank Tom Fischer at Jyske Bank in Denmark for being such a perfect host in Denmark. Rarely have I been treated so well. Warsaw was interesting. I loved Krakow, and Prague is beautiful. I met so many new friends.

I had dinner in London Wednesday night with old friend Bill Bonner of Daily Reckoning fame, but he and I met almost 25 years ago as (then young and struggling) publishers of investment newsletters. He went on to build one of the largest investment publishing businesses in the world, and I left the business five years later for the investment management side of the business, but we have stayed close all these years. We have seen a lot of changes over that time, and I trust we will see a few more over the decades.

He brought me his new book, Mobs, Messiahs and Markets , which will go to the top of my reading list. I love the way Bill writes. Interestingly, I looked at this book on Amazon, and noted that they have his book paired with Alan Greenspan's new book.

I am not certain what it says about the world, but I note that Bill's book is at #10 on Amazon and Greenspan's is at 265. I intend to review the book in the near future, but you can get it at Amazon.com .

It is good to be home. I look forward to being here for awhile. And while I have had major writer's block on the book I am supposed to be writing, I think I worked my way through my problems these past two weeks. Trying to convey the nature of the changes we will be facing in the next 20 years has been a much more daunting task than I had first supposed. But then most things that are worthwhile, it seems, end up taking more effort than we first thought. It is good to be somewhat overly-optimistic, at least for me, for if I was a realist, I would start way fewer projects and end up accomplishing less.

We celebrate my oldest son Henry's birthday tomorrow. It was actually last week while I was on vacation, but nearly everyone, including me, was gone. The twins are down from Tulsa and Henry wants sushi, although that may be tough for me as I did have some bad sushi at the Park Plaza in London on Tuesday and have been sick since then, although I am getting better.

Here's to old and new friends and family. Have a great week.

Your thinking a lot about life analyst,

By John Mauldin

http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here: http://www.frontlinethoughts.com/subscribe.asp

Copyright 2007 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Note: The generic Accredited Investor E-letters are not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for accredited investors who have registered with Millennium Wave Investments and Altegris Investments at www.accreditedinvestor.ws or directly related websites and have been so registered for no less than 30 days. The Accredited Investor E-Letter is provided on a confidential basis, and subscribers to the Accredited Investor E-Letter are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an NASD registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Pro-Hedge Funds; EFG Capital International Corp.; and EFG Bank. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.