Financial Fraud and the Global Derivatives Casino, Mechanisms of the Scam

Politics / Credit Crisis 2010 Sep 29, 2010 - 12:35 PM GMTBy: Matthias_Chang

Basel Accords III is another crude endeavour by BIS and Global Too Big To Fail Banks to cover up their scams and shore up the global derivative casino.

Basel Accords III is another crude endeavour by BIS and Global Too Big To Fail Banks to cover up their scams and shore up the global derivative casino.

Part 1 - The Mechanics of the Derivative Scam

The fact that common folks in the US and other developed countries have not come out in arms to lynch the central bankers and their accomplices in Wall Street and other banking centres is an indication how effective the financial elites have been able to hoodwink and confuse the masses.

$Trillions have been wiped out but hardly anyone of substance has demanded criminal prosecutions. Fraud, massive frauds have been committed by top bankers, lawyers, accountants, regulators and politicians of all hues but none had to pay for their crimes.

$Trillions have been wiped out but hardly anyone of substance has demanded criminal prosecutions. Fraud, massive frauds have been committed by top bankers, lawyers, accountants, regulators and politicians of all hues but none had to pay for their crimes.But, the guy who robs the corner shop down the road for a couple of bucks is incarcerated for five years or more, buggered and abused in prison. There is no pity for such a scumbag, no matter what are the circumstances that drove him to commit the crime.

The Bernankes, the Geithners, the Paulsons, the Larry Summers and their pals in Goldman Sachs, JP Morgan, Citigroup, Merrill Lynch, Bear Sterns, Lehman Brothers, Fannie Mae, Freddie Mac and their European counterparts are given blanket immunity and allowed to continue the rape and plunder of the global economy. I believe that unless progressive financial analysts and commentators simplify their analysis and commentaries so that more people will understand how the frauds have been committed, the status quo would remain and the plunder would continue.

This article is an attempt on my part to explain the massive banking fraud in simple terms and I hope that I have succeeded in doing so.

SOME BASIC CONCEPTS

Banking business is a very lucrative business and the manager of your local bank works hard to provide a service and earn decent profits for his employers. I have spent over 20 years in my 34 years as a lawyer training bankers in their day-to-day operations and found them to be professional and trustworthy. Very rarely does a branch suffer losses. I would put it as high as 98% of branches deliver a steady stream of profits to Headquarters. The network of branches provides an effective payment system for commerce and for our daily needs. I have no quarrels with the main street banks, notwithstanding that it is based on fractional reserve banking.

The purpose of this article is to expose the fraud committed by financial elites at Headquarters and the Too Big To Fail Banks abusing the loopholes in the system with the connivance of central bankers and regulators.

So, to understand the loopholes in the system, you must understand how the banking system works, specifically the fractional reserve banking system practice by all banks throughout the world.

This is best done by understanding some key terminology. Please be patient.

1.0 Banks Capital

1.01 A bank is required by law to maintain a minimum amount of capital. In laymans term, there must be sufficient assets to offset liabilities.

1.02 You will note that the word asset is in inverted commas i.e. Assets because in the banking business, what constitutes assets differs from your ordinary business.

1.03 The financial health and strength of a bank depends on the Capital / asset ratio and is referenced as a percentage.

1.04 In 1988, the Bank of International Settlements (BIS) in Basel, Switzerland established a universal standard (Basel I) for the capital /asset ratio. It was stipulated that total capital must be at least 8% of total risk-weighted assets.

Please fix this in your mind, that way, way back in 1988 the ratio was fixed at 8%, as you would not be able to appreciate how the fraud was perpetrated.

2.0 Risk-Weighted Assets

2.01 Please recall that in the preceding paragraph I referred to assets because in banking terms, assets are treated not in accordance with the laymans understanding of the term.

2.02 This is one of the reasons for the public and so many analysts confusion and misunderstanding about fractional reserve banking. This is also how banksters commit the fraud. More of this later.

2.03 So how are banks assets treated and or classified?

To understand, you must bear in mind that the purpose of the classification of the banks assets is for the purpose of determining the capital ratio (How Basel I and the subsequent Basel Accord II and III arrived at the ratio).

2.04 Not all assets of a bank are treated the same.

Why?

2.05 The bankers came up with the clever idea of classifying assets by the concept of risks. Hence, the term Risk-weighted assets!

In the result, if the asset has less risk, less capital reserves will be required.

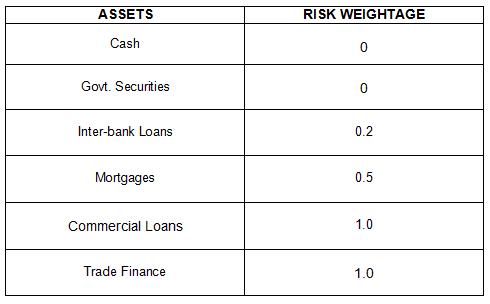

2.06 Let me explain. Please see table 1 below as an example.

2.07 You will notice straight away that loans are classified as assets for bank accounting purposes and this is never understood by the layman who considers assets as comprising cash, savings, properties (houses, factories), shares and or govt. securities. This is another reason for the confusion when reference is made to a banks assets.

2.08 It follows from the table that O risks will not require capital reserves and that assets which has high risks will attract higher capital reserves. Under the Basel Accords, common equity constitutes the highest / best form of loss absorbing capital.

2.09 Further confusion is created for the layman when Basel Accords have two categories of capital.

3.0 Tier 1 and Tier 2 Capital

3.01 Tier 1 capital refers to the book value of the banks stock and retained earnings. Tier 1 capital must be at least 4% of total risk-weighted assets. Tier 2 capital is loan-loss reserves (money set aside in the event of loans defaulting and the bank suffers a loss) and subordinated debts. [1]

3.02 Therefore, total capital is the sum total of Tier 1 and Tier 2 capital as defined by the Basel Accords. Total capital must be at least 8% of total risk-weighted assets. Please see sub-paragraph 1.04 above and keep this in mind at all times.

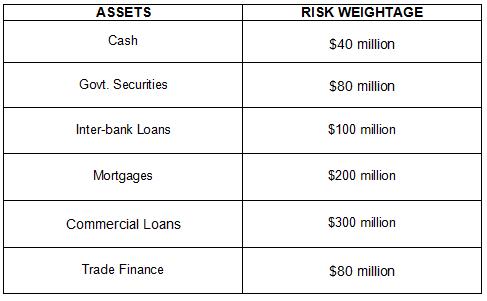

The table 2 below is a simple illustration [2]

From the table above we can calculate the capital reserves that are required to be maintained by the bank.

3.03 0 x $40 million plus 0 x $80 million plus 0.2 x $100 million plus 0.5 x $200 million plus 1.0 x $300 million plus 1.0 x $80 million = $500 million

The risk-weighted assets value is $500 million because we only took into account the last four categories of assets as they have been assigned a risk factor greater than zero (0).

Therefore, the bank must have Tier 1 capital of at least 4% of $500 million = $20 million (see sub-paragraph 3.01).

Therefore, the bank must have total capital of at least 8% of $500 million = $40 million (see sub-paragraph 3.02).

3.04 I want you to take a closer look at Table 1 again. What conclusions can you draw from the risks assigned to the assets? It is so obvious, it is staring at your face.

a) Government securities are as good as cash and treated as 0 Risk, meaning that there can be no risk of sovereign defaults zero risk. I did not say it. Basel Accord I assigned zero risk. It is not even a black swan event. But, we have seen in the last few months, the threat of sovereign risks from PIIGS countries (Portugal, Ireland, Italy, Greece & Spain) and of course the UK and the mighty USA. In fact in 1971, the US was in default and that was why Nixon took the US off the gold standard under the Bretton Woods system.

And of course, loans to fellow bankers are hardly any risk at all, but under the Basel Accord I, the assigned risk factor is a mere 0.5. The banks would not want to be perceived as bias.

b) Commercial loans are more risky than mortgages (housing loans secured by the value of the property).

4.0 Ratings by Rating Agencies - Moodys, S & P, Fitch etc.

4.01 The rating agencies also assign risks to all sorts of financial products, institutions etc. The ratings range from AAA (the very best) to Junk status! Government securities are rated AAA which denotes zero risk as in the Basel Accord I.

4.02 I am sure most of you can anticipate the con perpetrated by the banks, the rating agencies, the regulators and the central bankers. The starting point of the derivative scams is here, especially credit derivatives. Why?

4.03 The declared purpose of ratings is to enable investors to determine the price of their investments which they are willing to pay the more risky the investment, the higher would be the returns demanded and vice-versa. And bearing in mind that government securities are rated AAA, any entity or product that has been rated AAA is deemed to carry zero risks. This must be so, as the Basel Accord I assigned government securities with Zero risks and the rating agencies triple A rating for government securities carry the same connotation. Therefore, any entity or product that carries an AAA rating is held out to be as good as government securities.

4.04 From the standpoint of the bankers and their accomplices in the regulatory agencies, the central banks etc. assets that can be rated AAA (zero risk) will be exempted from the need to have any capital reserve. Even, if a minimum risk factor is imposed on such AAA rated securities etc. the banksters still benefit in that they will only need to set aside minimum capital reserves. Herein lies the seed of the bankers devious schemes.

Before we proceed further, it must be obvious to all of you that the whole system of fractional reserve banking is an inverted pyramid scheme with a small capital base supporting a huge asset base as illustrated in Table 1 and 2.

Part 2 - THE BANKERS DEVIOUS MIND

You must now put on your thinking cap and begin to think like a Goldman Sachs or JP Morgan banking executive if you want to understand how the con has been played.

Just pause and think about this issue. Table 2 is an illustration in the $millions. Extrapolate Table 2 in the $trillions and you will immediately see why banksters are working overtime to come up with schemes that will reduce their need to set aside capital reserves. To the banksters, what is important is not the need to protect their customers and depositors the people who place their hard-earned monies in their banks, but how to minimise the need to set aside capital reserves, for each dollar set aside is a dollar not earning compound interest / profits.

If loan assets are in the trillions, capital reserves will be in the billions, money idling and not earning interests and generating profits!

I have stated earlier, banking is a lucrative business. And one of the most lucrative aspects of banking is mortgage finance loans to buy a house. These loans invariably cover a period of 20 to 30 years. This means that a bank has literally a lifetime of a steady stream of profits, as a result of compound interests charged for these loans. Additionally, these loans are monies / debts created out of thin air. This issue will be addressed in my next article. But you get my drift.

But in the last two decades, the banks got greedy, very greedy and reckless. The investment bankers are the worst of the lot - financial rapists, who only look out for themselves, getting multi-billion dollar bonuses!

Recap: From Table 1 above, loans are treated as assets and they carry risks. Such risks are rated from 0 to 1. If there are risks, capital must be set aside to meet potential losses.

Lets assume that you are the CEO of Goldman Sachs or JP Morgan, and you have a bunch of whiz kids and rocket scientists. What would you ask them to do in such a situation?

I want you to step back and think deeply for a while and experience the ecstasy of the Eureka Moment, the self realization of how the scam was invented.

5.0 BISTRO

5.01 Not many people know that BISTRO is the name of the scheme created by the whiz kids of JP Morgan in the 1990s to circumvent the capital/asset ratio of Basel I.

5.02 When a borrower defaults in paying a loan, the loan is categorised as a Non-performing loan. There is always a risk of a borrower not paying his loan. In banking terminology, this is called the Default Risk.

5.03 Bearing in mind that loans generate a stream of interest payments as well as default risks, how would you as a banker come up with a neat solution of having the cake and eat it as well if I may be allowed to borrow the expression i.e. have the revenue stream and profit, but without the risk of default? This was the $trillion question and challenge faced by greedy bankers in the 1990s.

5.04 Put it in another way the challenge was to earn substantial income and profits and unload the risks!

5.05 Can the risks be distributed and dissipated thereby circumventing the need to comply with Basel I capital/asset ratio? How?

5.06 The answer was to package the default risk and trade them as securities. The scheme to implement this audacious financial engineering was named BISTRO by the devious minds in JP Morgan headed by Peter Hancock. Though Hancocks team was not the first to come up with the idea, it has been conceded by the industry that they were the first to do it in a big way, turning credit derivatives into the global casino as we know it today.

5.07 The essence of the scheme was to find an entity that was willing to assume the risk for a fee form of insurance. If there is no default, the entity would earn a stream of premiums or fees for assuming the risk of default. The bank (originator of the loan) would be protected and its profits would be the stream of interest payments less the fee paid for the protection. The bank was the protection buyer and the entity the protection seller.

Recall the infamous hanky panky between A.I.G and Goldman Sachs.

5.08 The first major deal was between JP Morgan and the European Bank for Reconstruction and Development covering a $4.8 billion credit line given to Exxon by the bank. JP Morgan was in cloud nine. A default risk was successfully sold, and the risk was dispersed.

5.09 The name given to this specific transaction was Credit Default Swap (CDS)!

5.10 The regulators were also impressed by the logic of the scheme and by 1996, the Fed was sufficiently confident of the scheme that it issued a statement that banks be allowed to reduce capital reserves by using credit derivatives.

5.11 Please note that the CDS was just one of several credit derivative products that were being promoted in the 1990s. You will notice that the products are not called debt derivatives but credit derivatives. But this simple terminology has pulled the wool over the eyes of so many. A loan is a debt due from a borrower, and is also a credit extended by the lender.

5.12 Think about it. Why not a debt derivative? Why not call the swap Debt Default Swap (DDS) instead of CDS? It is sound marketing strategy and or propaganda to promote a name which has a positive connotation. Debt has a negative connotation, even though it conveys more accurately the nature of the transaction. It is obvious that the terminology is a way of shielding the fact that the banker has not much faith in the borrower that it requires a insurance against a default by the borrower of the credit facility, notwithstanding that the borrower would have provided collateral to secure the loan / credit facility. In this case it was the mighty Exxon!

5.13 Thinking through logically. Exxon is rated AAA, yet JP Morgan was insecure and needed protection against default. Should not the rating agencies, given the circumstances downgraded Exxon from AAA (zero risk or minimum risk)? Calling it a credit derivative camouflages the inherent heightened risks of default for such a credit facility. No one is complaining as everyone in the overall scheme of things gets to retain their respective AAA ratings!

5.14 Before proceeding further, I just like to give a short explanation about the term derivative. Let us examine the transaction referred in sub-paragraph 5.08.

The principal transaction is the credit facility extended by JP Morgan to Exxon. The need for protection against a default gave rise to another transaction which is derived from the principal transaction. Therefore, any financial transaction which is derived from another principal transaction will be a derivative.

It follows that credit derivatives such as CDS are credit transactions which is derived from or dependent on another principal credit transaction such as a loan.

6.0 Packaging & Securitisation of Loans

6.01 In the beginning of the development of credit derivatives, you will notice that while the risk was transferred / distributed to a protection seller such as the European Bank for Reconstruction and Development, the loan or credit facility still remained on the banks balance sheet. Having a CDS may reduce the risk factor assigned to a particular loan asset but, the bank has still to comply with the Basel Accord I capital / asset ratio.

6.02 The logical deduction from the above is that if the loans are no longer on the banks balance sheet, there would be no need to maintain the requisite capital / asset ratio. This means that the banks will have less exposure to defaults either because the risk has been transferred to a protection seller and or the loan asset was disposed to investors.

6.03 Selling individually loan assets would be cumbersome, time consuming and would not be market friendly. The logical progression would be to sell the loan assets in bundles, which would provide a larger stream of revenue by way of interest payments. But, there is an inherent problem in bundling loan assets, as different types of loans have different risk-factors as well as borrowers have different credit ratings as to their ability to repay the loans. The bankers came up with the idea to bundle low risk loans with some high risk loans so that even if some of the high risk loans were to default, the profit from the low risk loans would be sufficient to cover the defaults. The idea took off.

6.04 There was another variation. When banks issue securities such as bonds, they could latch the bundle of loan assets to the security such that the mortgage payments (cash flow) would go to pay the bondholders (the purchasers of the bonds). In market terminology, such securities were referred to as Mortgage-backed securities. This idea made the trading of such securities more acceptable and profitable.

6.05 From the banks point of view, there is never ever enough of money to be made. Financial engineering must be employed to churn out more revenue and profits and of course more bonuses. The financial engineers came up with the idea of slicing the aforesaid securities into tranches.

6.06 Each tranche would have different levels of risk and returns there were three tranches. The junior tranche consists of the highest risks and pays out the highest returns. The mezzanine tranche consists of moderate risks and moderate returns. The senior tranche has the lowest risks and lowest returns. This gave investors the option to take up whichever tranche that they fancy. The speculative-minded would go for the junior tranche while the conservative investor would opt for the senior tranche preferring safety to high returns. In this way, loan assets were removed from the banks balance sheet. To attract investors, the rating agencies (for enormous fees) colluded and connived in giving top ratings for these financial products. And as they say, the rest is history.

7.0 Special Purpose Vehicles (SPVs)

7.01 When the global derivative casino took off, the Too Big To Fail Banks became more greedy. The protection sellers (sellers of CDS) were making too much easy money for insuring default risks. So these banks decided to insure themselves. They created Special Purpose Vehicles (SPVs) that would sell CDS to cover the banks loan assets. It was like taking money from the left pocket and putting into the right pocket and getting away with it and more importantly effectively circumventing Basel I capital / asset ratio. The SPVs soon realise they could make additional profits by selling the CDS to investors, hedge funds and pension funds chasing for higher returns. In the result, the ultimate protection sellers were the global investors.

But no one ever queried whether in the event of a major default this last line of protection sellers from all over the world have the means to cover the defaults. If AIG did not have the requisite financial means to cover the CDS of Goldman Sachs and the other Too Big To Fail Banks, how in the world can these investors pay up? It was a Ponzi scheme pure and simple!

7.02 Eventually, the CDS became meaningless. They were no longer used for insuring defaults but became an instrument for gambling, with Goldman Sachs leading the way. This was done when Goldman Sachs having unloaded the mortgage-backed securities as well as through their own SPVs, their own CDS, they would then buy CDS from some other protection sellers betting that these so-called investments would turn bad. In simple terms, these fraudulent bankers created toxic loan assets, bundled them, insured them and off-loaded to greedy investors and then kicked them when they were down by betting against them.

7.03 Can the FED, the US treasury, the central bankers or anyone really tell with confidence that this banking / derivative cesspool can be cleaned up and that the $trillions of toxic waste can be de-leveraged? I will bet my bottom dollar that the FEDs second round of quantitative easing (the purchase of the toxic assets from the global banks) can erase the problem. There is just too much of this mess to be resolved through QEII.

That is why I can say with confidence in all my articles that the Too Big To Fail Global Banks are all insolvent.

THE CENTRAL BANKS COVER UP

The Bank of International Settlements (BIS) is often referred to as the Central Bank of all the Central Banks, and is up to its eyeballs in covering up the financial crime of the century.

I want you to recap on Basel I, specifically Table 1 above and the Tier 1 capital of 4% and total capital of 8% of the risk-weighted loan-assets in sub-paragraphs 2.06 and 3.01 above. This was stipulated way back in 1988.

Then BIS issued Basel II.

Now fast-forward to Basel III which was announced recently.

Please read the following passages from the Press Statement of the BIS introducing Basel III. We quote:

At its 12 September 2010 meeting, the Group of Governors and Heads of Supervision, the oversight body of the Basel Committee on Banking Supervision, announced a substantial strengthening of existing capital requirements and fully endorsed the agreements it reached on 26 July 2010

My $Trillion dollar query is this Why is there a need now for SUBSTANTIAL STRENGTHENING of existing capital requirements?

I have shown in the above analysis how the Big Banks used devious means to reduce SUBSTANTIALLY the capital requirements, and all of these devious means were condoned and approved by the BIS and other central banks.

Tier 1 capital was fixed at 4% and total capital fixed at 8% of total risk-weighted assets in 1988.

In the same Press Statement, the BIS stipulated that:

The Committees package of reforms will increase the minimum common equity requirement from 2% to 4.5%. In addition, banks will be required to hold a capital conservation buffer of 2.5% to withstand future periods of stress bringing the total common equity requirement to 7%.

BIS went on to state that by January 1, 2013 banks will be required to meet the following new minimum requirements in relation to risk-weighted assets (RWA):

- 3.5% Common equity/RWA

- 4.5% Tier 1 capital/RWA, and

- 8.0% total capital/RWA

After 22 years, we are back to square one again. Back to Basel I requirements. Not that even this requirement (Basel III) will be sufficient. In any event, its implementation will be delayed. Final compliance would not take place until 2019.

$Trillions have been spent to bail out these corrupt bankers. But hardly any monies have been spent to resolve the massive unemployment in the USA. It has been reported that over 45 million Americans are on food stamps and one in seven are unemployed.

But not one banker, regulator or central banker has been prosecuted.

In the past two years, you may be excused for your ignorance. After reading this article, there can be no more excuses for not taking actions against these financial rapists. And if you dont, you deserve to be raped and plundered! I offer no apologies for my bluntness!

End Notes

[1] A Subordinated debt is a debt which ranks (stand in line) in a case of insolvency/liquidation after payment to depositors and other creditors.

[2] Source: William F. Hummel, Money - What It Is, How It Works

Matthias Chang is a frequent contributor to Global Research. Global Research Articles by Matthias Chang

© Copyright Matthias Chang , Global Research, 2010

Disclaimer: The views expressed in this article are the sole responsibility of the author and do not necessarily reflect those of the Centre for Research on Globalization. The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible or liable for any inaccurate or incorrect statements contained in this article.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.