The Age of Debt Deleveraging Deflation, Decade of Slow Economic Growth

Economics / Deflation Nov 16, 2010 - 06:35 AM GMTBy: John_Mauldin

Before we get into this week’s outstanding Outside the Box, I want to comment on QE2 and the efforts by some Republican economists to urge legislators to get involved to stop it (see the front page of Monday’s Wall Street Journal). That pushes my comfort zone a little too much.

Before we get into this week’s outstanding Outside the Box, I want to comment on QE2 and the efforts by some Republican economists to urge legislators to get involved to stop it (see the front page of Monday’s Wall Street Journal). That pushes my comfort zone a little too much.

First, I am not a fan of QE2. Never have been. If it had been my call, I would have punted and told the guys in the Capital that the ball was in their court to get their fiscal house in order, because that is the main source of the problem. But Bernanke and the Fed felt they had to “do something,” to demonstrate they got the seriousness of the situation. If the only policy tool you have left is the hammer of printing money, then the world looks like a nail.

Second, I doubt it works. It might be interesting to see what would happen (theoretically) if they decided to print $3-4 trillion. Now that would have a (probably very negative) impact. But it would show up on the radar screen. I think $600 billion just gets soaked up in bank balance sheets, sloughed off to world emerging markets (that don’t want it) and other hot spots, with some drifting into the stock market. But does it increase real final demand, which is what the Keynesians are so seemingly desperate for? I doubt it. And I just don’t see the transmission mechanism for QE2 to produce new employment of any statistical significance.

Third, targeting the middle of the yield curve is about as benign a way as you can do it, as far as QE goes. It certainly is not bringing down mortgage rates (so far). This is not exactly shock and awe QE.

Now, if the real plan, which no one can mention in polite circles at G-20 meetings, is to weaken the dollar, then QE2 just might work at doing that. But do we want it to? Do we want our input prices to go higher? A weaker dollar cuts both ways. And Germany seems to be able to work with either a strong or a weak euro. Are they that much better than us? Really? I sincerely hope we can take Bernanke at his word that this policy is not meant to weaken the dollar. Currency manipulation is not what we need from the world’s reserve currency, nor will we hold that status much longer if we embark down that path.

Back to the Republican sortie against QE2. As long as it stays on a debate level, or even as a resolution, then fine. There is considerable room for debate, and some very serious economists on both sides of the issue. This is new territory and deserves to be debated vigorously. This is, after all, affecting the public. Fed policy is too important to be talked about only inside a conference room with a few appointed governors and economists.

But I do not want to see anything that would reduce the independence of the Fed from the political process (any more than it already has been reduced). I don’t want Republicans dictating Fed policy. Or Democrats. Or the President, beyond his power to appoint. That is the path to becoming a banana republic.

If We the People want to change Fed policy, then we need to realize it is important who we elect as president, because he appoints the chairman and the governors. Ideas matter and have consequences. How many times do presidential candidates get asked about their views on monetary policy in national debates? Are you a proponent of Keynes? Or Friedman? Fisher? von Mises? Which of these four dead white guys have you read and studied? These elections of ours are more than taxes and health care. The Senators who sit on the committees have the right to review appointees, though few understand the real issues regarding the Fed, I am afraid. (Wouldn’t it be fun to have Rand Paul on that committee? He could tag team with his dad in the House. Just a thought.)

Final thought. Maybe the reason for a less than shock and awe QE is that the Fed can get to the end of it and say, “Look, we tried. But the money just went back onto our balance sheet. Printing more doesn’t seem to be advisable.” (Especially if the public pushback gives them some cover.) Then they can back off and let Congress know that they have no intention of monetizing their fiscal profligacy and that Congress must get its house in order before the bond markets react negatively.

And then again I may be wrong. Maybe QE2 does do something. No one really knows because this is truly uncharted territory. We’ll find out in the coming months. And this Friday, in my weekly letter, we’ll look at the prospects for the economy going forward. I get back home tonight and will be home for two weeks. I am looking forward to catching up on my reading.

Now, for this week’s OTB I offer a review of Gary Shilling’s brand new book, The Age of Deleveraging: Investment strategies for a decade of slow growth and deflation.

Gary has long been a proponent of the idea that we are in for a period of deflation, and was writing as far back as the ’90s about the coming deflation. I am already into the book and am enjoying his wonderful prose, but must admit I skipped ahead to see his predictions, some of which are in the review below. You can buy the book at http://www.amazon.com/deleveraging.

Have a great week. And think about a few more fun things than QE2 every now and then.

Your loving the La Jolla weather analyst,

John Mauldin, Editor

Outside the Box

The Age of Deleveraging

In his new book, The Age of Deleveraging: Investment strategies for a decade of slow growth and deflation, published by John Wiley & Sons, Dr. A. Gary Shilling makes the case for slow economic growth and deflation for many years ahead as well as lays out the investment strategies that flow from this forecast—12 sectors to sell or avoid and 10 to buy.

This new age of deleveraging was sired by the back-to-back collapses of the housing and financial bubbles in 2007 and 2008, both of which he had been forecasting since early in the 2000s. He begins his new book with a look at how both of those bubbles were created, how they grew and how he was lucky enough to have spotted them in their infancies. Gary loves to be among the few to spot them and predict their demises. He also reviews the five other Great Calls he's made in his 40-year forecasting career, including the 19691970 recession, the early 1970s inventory bubble and 1973-1975 recession, disinflation starting in the early 1980s, the demise of Japan’s 1980s bubble and the dot com blowoff in 2000.

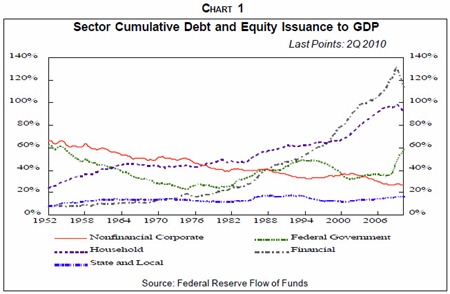

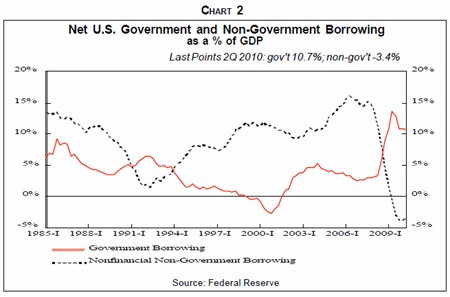

After four decades of leveraging up by the global financial sector and a three-decade borrowing-and-spending binge by U.S. consumers, deleveraging is underway. The good life and rapid growth that started in the early 1980s was fueled by massive financial leveraging and excessive debt, first in the global financial sector, starting in the 1970s, and later among U.S. consumers (Chart 1). That leverage propelled the dot-com stock bubble in the late 1990s and then the housing bubble. But now those two sectors are being forced to delever and, in the process, are transferring their debts to governments and central banks. The federal budget deficit leaped from $187 billion in the 12 months ending December 2007 to $1.3 trillion in the 12 months ending August 2010, but it had little net effect on the economy as private sector retrenchment more than offset the deficit jump (Chart 2 ). Federal borrowing relative to GDP leaped from 3.0% in the third quarter of 2007 to 10.7% in the second quarter of 2010, a 7.7-percentage point climb, but private borrowing fell from 15.2% to a negative 3.4%, a drop of 18.6 percentage points, or more than twice as much.

This deleveraging will probably take a decade or more to complete—and that’s the good news. The ground to cover is so great that if it were traversed in a year or two, major economies would experience depressions worse than in the 1930s. This deleveraging and other forces will result in slow economic growth and probably deflation for many years. And as Japan has shown, these are difficult conditions to offset with monetary and fiscal policies.

Insidious

The insidious reality is that this deleveraging doesn’t occur in a straight line, but is highlighted by a series of seemingly isolated events. After each, the feeling is that it’s over, all may be well, but then follows the next crisis. When the subprime residential mortgage market started to collapse in February 2007, most thought it was a small, isolated sector. After all, new subprime mortgages were only about 20% of total residential mortgages issued even at their peak in 2006, and those subprime loans were made to people that, luckily, we never have to meet. And at its top in fourth quarter of 2005, total residential construction was a mere 6.3% of GDP.

But then the “subprime slime,” as he dubbed it, spread to Wall Street in June of that year with the implosion of two big Bear Stearns subprime-laden hedge funds. Most hoped the Fed actions that August had ended the crisis and, indeed, stocks reached their all-time highs in October 2007. But as the financial woes spread, Bear Stearns was forced to sell for next to nothing to JP Morgan Chase bank, Merrill Lynch suffered a shotgun wedding with Bank of America, major banks like Citigroup and Bank of America itself were on government life support, and Lehman Bros. went bankrupt in September 2008.

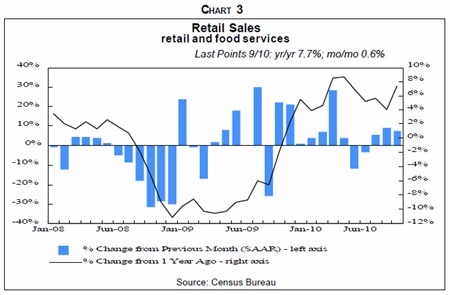

Then the third phase struck as U.S. consumers stopped buying in the fall of 2008 (Chart 3 ) and the fourth, the global recession, coincided. Falling house prices and earlier home equity withdrawal wiped out the home equity that many had used to finance oversized consumer spending and the availability of loans in general became as scarce as hens teeth amidst the financial panic.

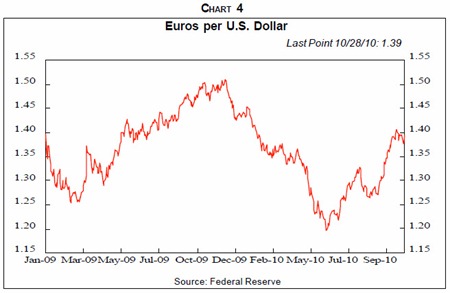

The optimists hoped the $862 billion fiscal stimulus package in the U.S. and similar fiscal bailouts abroad would take care of all those problems, but were surprised by the eurozone crisis in late 2009 and early 2010 and the drop it sired in the euro against the greenback (Chart 4). Nevertheless, that’s just the fifth step in global deleveraging. The combination of the Teutonic north and the Club Med south under the common euro currency only worked with strong global growth driven by the debt explosion—but now that’s over.

More Traumas Ahead

Further traumas on this deleveraging side of the long cycle lie ahead. Another sovereign debt crisis in Europe may be in the cards with Ireland replacing Greece as the focus. A further 20% drop in U.S. house prices due to huge excess inventories of over 2 million and foreclosure delays may push underwater homeowners from 23% of mortgagors to 40% and precipitate a self-feeding spiral of walkaway homeowners and nosedive in consumer spending.

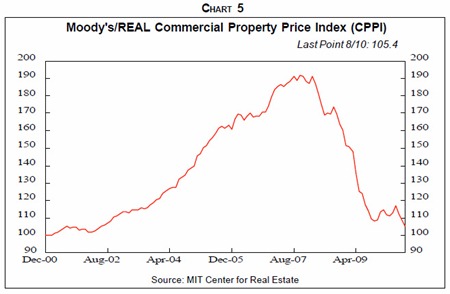

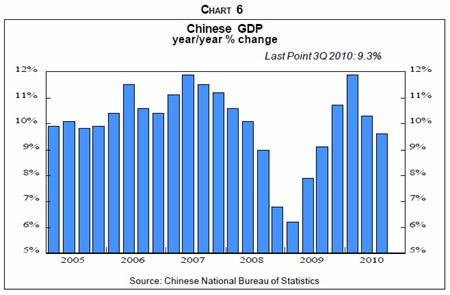

Other roadblocks on the deleveraging highway may include a crisis in U.S. commercial real estate (Chart 5) that could exceed the earlier one in housing. Then there’s a possible hard landing in China that exceeds the 2008 weakness (Chart 6) as the government’s measures to cool the red hot property market and economy in general take hold. A slow-motion train wreck in Japan will probably occur sooner or later as her all-important exports fall along with weakening U.S. consumer willingness to buy them, and as her already subdued domestic sector suffers from her rapidly aging population.

Nine Causes of Global Slow Growth

In The Age of Deleveraging, Gary notes that with deleveraging comes slow economic growth, and he details nine reasons why real GDP will rise only about 2% annually in the years ahead— far below the 3.3% growth it takes just to keep the unemployment rate stable. Those nine reasons include:

1. U.S. consumers will shift from a 25year borrowing-and-spending binge to a saving spree. This will spread abroad as American consumers curtail the imports of the goods and services many foreign nations depend on for economic growth.

2. Financial deleveraging will reverse the trend that financed much global growth in recent years.

3. Increased government regulation and involvement in major economies will stifle innovation and reduce efficiency.

4. Low commodity prices will limit spending by commodity-producing lands.

5. Developed countries are moving toward fiscal restraint.

6. Rising protectionism will slow, even eliminate global growth.

7. The housing market will be weak due to excess inventories and loss of investment appeal.

8. Deflation will curtail spending as buyers anticipate lower prices.

9. State and local governments will contract.

2.0% Growth May Be High

Please note that these nine economic growth-slowing forces make 2.0% annual advances in real GDP in coming years reasonable, maybe even optimistic. The switch from a quarter-century-long consumer borrowing-and-spending binge to a saving spree will cut 1.5 percentage points off the 3.7% GDP growth rate of the lush 1982–2000 years. That alone brings growth down to 2.2%, and the eight other forces can easily reduce growth by another 0.2 percentage points.

Deflationary Expectations

And the deflationary environment Dr. Shilling foresees will feature both good deflation of excess supply resulting from rising globalization and the increasing economic dominance of productivity-soaked new technologies as well as the weak economic growth-inspired bad deflation of deficient demand. Good deflation will amount to about 1% to 2% while the bad deflation will run about 1%, making for annual deflation rates of 2%-3% per year.

Deflation is self-feeding and a key, but by no means the only, self-perpetuating mechanism is the anticipation of lower prices. But how much deflation does it take for consumers and businesses to wait for lower prices before buying? There is no simple answer, but it depends on at least four factors:

1. The breadth of deflation. Declining prices have to spread across a wide spectrum of goods and services to be convincing. The declines in energy prices in 2009 were too narrow to be convincing.

2. The chronic nature of deflation.The consumer price index (CPI) and producer price index (PPI) dropped year over year in 2009, but only for a few months due to declining energy prices. Furthermore, against the background of nonstop inflation since World War II, that experience was not long-standing enough to convince people that it would persist.

3. Decelerating prices, at least in the short run. Few Americans expect deflation, and most regard a return to significant inflation as inevitable. This probably means that it will take a pattern of smaller and smaller rates of inflation turning into bigger and bigger rates of deflation to be convincing. Inflation rates have fallen from double digits to essentially zero in the past 25 years. If deflation sets in, but at a steady rate of, say, 1% per year, it will probably take a number of years before people believe in its permanence. More immediately convincing would be 1% deflation followed by a 2% decline in general prices the next year and 3% the following year.

4. The amount of deflation. Of course, the deeper the deflation, the more convincing it becomes. Deep deflation would be a big persuader as it promotes big drops in interest rates and tangible asset and commodity prices, and unbelievable consumer bargains, but also job losses in firms that don’t cut their costs and prices. Those living on fixed incomes would feel like kings as their purchasing power grows while highly leveraged individuals and corporations would fail.

Furthermore, deflation must be significant enough to spur action. Even if you are convinced that a decline in shoe prices is in the offing, it may not be big enough to make you wait to buy. Waiting could entail another trip to the shoe store to check prices, and besides, if you buy a pair now, you get the use of them in the meanwhile.

In addition, the cost and discretionary nature of a good or service influences the sensitivity to deflation. An expected 5% decline in car prices next year may make you wait. If you’re spending $30,000, that’s a cool $1,500 in your pocket, and you can probably nurse your old bus along for another year anyway. Recall how rebate programs have pushed vehicle sales up and down like ping-pong balls. But a guaranteed 10% drop in toothpaste prices next month may not make you get out the pliers so you can, by vigorous squeezing, make the old tube last until the lower price is in effect—or to brush your teeth with Ajax while waiting for that price drop.

Trigger Point For Deflationary Expectations

Taking these four factors into account, what would it take to trigger deflationary expectations? Probably not as big a decline in prices as the 3% inflation rate level that seemed to touch off inflationary expectations in the 1970s. Even before that decade, folks had gained familiarity with rising prices throughout the postwar era and were relatively insensitive to the inflationary beast. Been there, done that.

Deflation, however, is a different animal, not seen since the 1930s, and few of us today have had first-hand experience with it. Widespread and chronic falling prices would be such a shock to most that it would probably take less deflation today than it took inflation earlier to get people’s attention. Our judgment is that declines in the prices of most goods and a fair number of services, averaging 1% to 2% and lasting for several years, would do the job. Then, anticipation of lower prices by buyers and all of the other self-feeding aspects of deflation would kick in. As noted earlier, Gary believes that annual declines in general price indexes of 2% to 3% are likely. If he's right, the world will be quite different than with the 2% to 3% annual inflation rates that most investors currently expect.

My Investment Themes

In The Age of Deleveraging, Gary discusses 12 investment areas to sell or avoid in the long run. Included are expensive consumer discretionary purchases like motor vehicles, appliances, airline trips and ocean cruises. These will be hurt by consumers' zeal to save and by the self-feeding downward spiral of deflationary expectations. The latter has locked automakers into profit-killing rebates. Similarly, credit card and other consumer lenders will suffer from the household shift from borrowing to debt retirement. Conventional homebuilders and their suppliers will be pressured as more than 2 million excess house inventories drive prices down another 20%.

The 10 investment sectors he favors include Treasury bonds. Back in the early 1980s, when the 30-year Treasury yielded 15.25%, he said we were entering "the bond rally of a lifetime.” He believes that rally is still intact as 30-year yields head for 3% and 10-year yields for 2% amidst slow economic growth, deflation and Treasurys’ global appeal as safe havens. Dr. Shilling also likes securities with high, reliable and growing cash returns such as stocks that pay significant dividends.

As households increasingly separate their abodes from their investments, they’ll favor small single-family houses, especially the cost-effective homes built in factories. Rental apartments will also be attractive as younger couples stay in them until their children are old enough to need single-family houses, and empty-nesters will prefer rentals to condos when they sell their suburban money pits. Our nation has decided to reduce its dependence on unreliable foreign energy sources, so he likes conventional North American energy suppliers such as coal, nuclear, natural gas, oil sands and related industries, but no government subsidy-dependent renewal energy such as ethanol, wind, solar and geothermal.

The Age of Deleveraging

Dr. Shilling believes the deleveraging process has years to go and that economic and financial markets have not returned to business as usual, at least not to the world of rapid growth supported by oversized and growing debt.

During the last fascinating decade, he played three roles. First, as an eyewitness to history, watching speculation survive the Internet bubble collapse in the early 2000s due to massive monetary and fiscal stimuli, and then spreading to commodities, foreign currencies, emerging market stocks and bonds, hedge funds and private equity, and especially housing. Gary saw the housing and financial bubbles expand and then explode. He watched the fears of financial meltdown spur gigantic monetary and fiscal bailouts. He experienced the witch hunts that followed, the inevitable result of widespread losses and high unemployment.

Second, he's been a participant in this drama, not only chronicling it in his monthly Insight newsletter, but also continually warning of the impending collapses in the housing and financial bubbles. And he was involved through a very profitable year in 2008 for the portfolios his firm manages when all 13 of his investment strategies worked—most gratifying in contrast to those who never acknowledged that those bubbles existed, much less could burst.

Third, Gary participated as a forecaster in successfully foreseeing the expansion and then collapse of the housing and financial bubbles. More recently, his forecasts have focused on the continuing deleveraging that the bursting of those two bubbles commenced, and the resulting investment strategies for the next decade.

The Age of Deleveraging describes all three of these roles, and I hope you find it enlightening, provocative, instructive, and at times amusing. It's available via amazon.com and barnesandnoble.com as well as at your local bookseller.

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.