Gold Outlook 2011: Irreversible Upward Pressures and the China Effect

Commodities / Gold and Silver 2011 Jan 11, 2011 - 03:31 AM GMTBy: Nick_Barisheff

Good afternoon. It is a pleasure to return to the Empire Club to discuss the outlook for gold and precious metals in 2011. I know this may appear to some to be an enviable job—getting to speak about the one asset class that seems to continually out-perform all others year after year—but it is a double edged sword.

Good afternoon. It is a pleasure to return to the Empire Club to discuss the outlook for gold and precious metals in 2011. I know this may appear to some to be an enviable job—getting to speak about the one asset class that seems to continually out-perform all others year after year—but it is a double edged sword.

I’ve struggled to find an appropriate simile. The best I can come up with is that speaking about gold is like one of those good news bad news jokes, you know the ones—your doctor phoned with some good news and some bad news. The good news is they will be naming a new incurable disease after you.

The good news is that gold is rising in value; the bad news is—well nearly everything else about the economy.

This year we travelled to the Middle East, the Far East and South and Central America to discuss gold. The different mindsets about gold we encountered there surprised all of us. Most people in these countries see gold as the protector of wealth. In the West, we view gold as a commodity for speculation.

Western economists treat the act of buying gold as an admission of defeat and their attempts at disparaging gold’s steady rise became even more tenuous than ever this past year. Some of these disparaging opinions include:

- “Financial tightening will cause commodity prices to fall.”

- “Gold is in a bubble.”

- “The gold stocks haven’t confirmed the gold bull.”

- Perhaps most desperate of all—“The economy is on the road to recovery.”

Despite these protests, gold had another remarkable year. It was up 25 percent in 2010, which marked its tenth straight annual gain.

Although we are speaking about gold today, I would be remiss in ignoring silver’s performance. Silver is up 78 percent in 2010 as it is, like gold, beginning to assume its role as a monetary metal. Platinum was also up 17 percent.

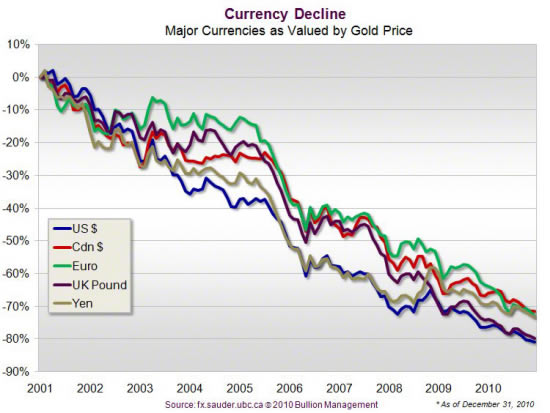

When we look at a ten year chart of the US and Canadian dollars, the Euro, the British Pound and the Yuan, we see that these five major currencies have lost between 70 to 80 percent of their purchasing power against gold over this 10 year period. In truth, gold is not rising, currencies are falling in value and gold can therefore rise as far as currencies can fall.

Three Short to Mid-Term Trends

I’d like to pick up where we left off last year with a review of three dominant medium term trends that put upward pressure on the price of gold in 2010 and will likely continue to in 2011. Then I’d like to look briefly at three longer term, irreversible trends that will put downward pressure on currencies resulting in upward pressure on gold for decades.

First, the three dominant mid-term trends we discussed last year.

These are:

- Central bank buying

- Movement away from the US dollar

- China

Central Bank Buying

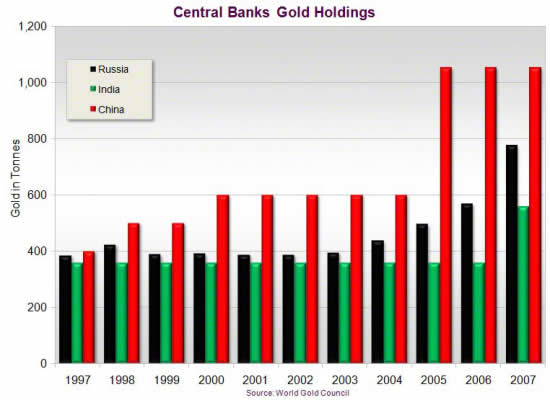

In 2009, for the first time in 20 years, monetary gold, or central bank and investment buying, outpaced gold buying for industrial or jewellery purposes. In 2010 China, Iran, Russia and India’s central banks were all significant buyers as they moved cash reserves to gold.

In Q3 of 2010, Russian central bank gold holdings rose seven percent to 756 tonnes. In 2010, the Russian Central Bank bought two thirds of its own gold production.

In December we learned that China had imported 209.7 metric tonnes of gold in the first 10 months of the year. This was a 500 percent increase over the same period of 2009 and on top of their world leading domestic gold production.

By the third quarter, India’s gold imports, both commercial and private, for the year were 624 tonnes, putting them 100 tonnes above the previous year’s total of 595 tonnes. Fourth quarter purchases could put India’s annual total over 750 tonnes.

China and Russia need to acquire gold to bring their gold reserve ratio to outstanding currency closer to Western central banks. Russia needs to acquire at least 1000 tonnes and China at least 3000 tonnes to remain on parity with the US. Chinese officials have stated publicly that China would like to acquire at least 6000 tonnes. Unofficially they have stated targets as high as 10,000 tonnes.

Movement Away from US Dollar

Last year we quoted a November 2009 story written by veteran journalist Robert Fisk claiming Russia and China along with France, were working on an agreement to trade oil with Arab states using currencies other than the US dollar. As expected, central bankers fervently denied these rumours. The US dollar has since 1973 been the only currency that oil could be traded in. This is the only reason the US has been able to amass nearly $14 trillion in debt. Loss of the petrodollar’s hegemony would have a devastating effect on the US as this is essentially the only reason foreign countries in the past needed to hold US dollars.

On November 24, 2010, China and Russia officially ``quit the dollar`` and agreed to use each other’s currencies for bilateral trade—including oil. Official trading on Moscow’s MICEX Index began December 15th, 2010.

In 2009, Robert B. Zoellick, made his well-publicized comment that, the US would be "... mistaken to take for granted the dollar's place as the world's predominant reserve currency.” And that, “... looking forward, there will increasingly be other options to the dollar." In 2010 he continued hinting at a new reserve currency made up of five currencies with gold as the “reference point.” He also called for a new Bretton Woods agreement this year. Mr. Zoellick is no lunatic goldbug. He’s the President of the World Bank.

China

Last month, I was a speaker and panellist at the China Gold and Precious Metals Summit in Shanghai. I can confirm that Chinese buying, both official and public, is a major trend that is not only well in place, but may be the single most important influence on the price of gold in 2011. As I said, the Chinese see gold quite differently from the way we see it. If we are to understand gold’s price direction in 2011 and beyond I believe it is essential to understand the “mindset” the Chinese have built around gold.

Economic Mindsets and Gold

Although the forming of economic mindsets is a complex topic, I’d like to simplify how major financial mindsets are created in one sentence. What our government, our banks and financial media tell us about money is what most of us will accept as our financial mindset or financial reality. If anyone doubts the power of government economic policy to shape mass economic reality, just look at how we have changed our attitudes towards debt, saving and economic value over the past 40 years. Our current debt based mindset began to form the day the US dollar, the worlds reserve currency, was removed from its final international peg with gold in 1971.

Different Attitudes about Gold

Although the West shares many common economic principles with the East, as the capitalist banking systems are similar, there is one area where there is a clear distinction—this is how Easterners view the role of gold as money.

Western governments fear gold. It restricts their ability to create currency.

In the West, governments borrow and encourage their constituents to follow their example. Banks encourage us to borrow for everything from vacations to widescreen televisions made in China. They tell us we are “stimulating” the economy through consumption. Generally speaking, the investing public in the West sees gold as a wealth gaining asset to be traded like stocks and bonds. This is why Westerners are constantly fretting about the price of gold in currency terms.

The Chinese government, on the other hand, respects gold. This is evident by the laws they have passed to facilitate mining and private gold ownership. China currently leads the world in gold production.

The government encourages the public to put five percent of their savings—yes they encourage savings—into gold. This is significant because the Chinese can save up to 40 percent of their annual salary. In the West, most middle class families are lucky to break even. The Chinese see gold as a wealth preserving asset that will weather all seasons. This is the difference that I believe anyone who wishes to fully understand gold’s rising price must comprehend. Inhabitants of older countries, who have lived through the destruction of an inflation fuelled currency crisis, do not need to be reminded that gold is the most effective hedge against inflation and a currency crisis.

Former CEO of Newmont Mining, Pierre Lassonde also feels that it will be buying by the Chinese public that will eventually propel gold prices into the stratosphere.

Three Irreversible Trends

Clearly, the three medium term trends we noted last year are still firmly in place. Now I’d like to look at three longer irreversible trends that I believe will affect the price of gold and currencies for decades. These are:

- The aging population

- Outsourcing

- Peak oil

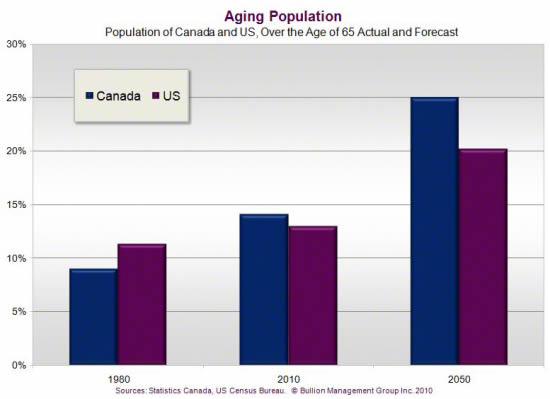

The Aging Population

The aging population is a combination of a population that is living longer and the “pig in the python” effect of a huge tidal wave of “baby boomers” born between 1946 and 1963 who are just starting to enter retirement age. As people age, they spend less and downsize. GDP and tax revenues are reduced and a much smaller workforce follows the baby boomers so this is a triple whammy. This problem is universal. In China, it is further exacerbated by their one child per couple policy. Governments will have no choice but to create more currency and further debase it.

Outsourcing

Outsourcing has almost entirely destroyed the manufacturing sectors of many first world countries like the US and Canada and much of Europe. The Chinese worker who built your IPhone made $287 a month; this was after a well-publicized raise. The West simply can no longer compete with these labour costs. The United States was the world’s largest manufacturer after WWII and has driven the world’s economy ever since. However, the US consumer can no longer buy things as they lose their jobs. As factories move off shore the high unemployment becomes systemic. Without jobs, the GDP and the tax revenues of the US fall. The mountain of federal, state and municipal debt will become even harder to service and the government will be forced to go even deeper in debt and to further debase its currency.

Peak Oil

Peak oil is the point at which the maximum rate of global petroleum extraction is reached, after which the rate of production enters terminal decline. This has already happened in the US, Alaska and the North Sea. In the next few years Mexico will become an importer of oil and the US will lose its third largest supplier. Our fragile, highly indebted economy relies on this land based cheap oil to continue and it cannot withstand the shock of transitioning to more expensive alternatives. In September of 2010 a

German military think tank reported that the German government is taking the threat of peak oil seriously and preparing accordingly. Numerous studies around the world have concluded that we are very close to peak oil production, which will be accelerated due to gulf drilling bans.

This will lead to higher price inflation for most goods. This will be another blow to the fragile US economy, which currently pays less for oil and gas than any of the first world countries. When added to the effects of the waning strength of the petrodollar the results will be devastating.

May I remind you that if China, which currently has one tenth the number of cars per capita as Americans, was to reach par with the US, we would need, by one estimate, seven more Saudi Arabia’s to meet their needs.

These three mega trends will continue to lower the GDP, lower the tax revenue, create higher trade deficits, create higher unemployment, resulting in the need for further currency creation. This will cause inflation to rise as currencies depreciate in value and create higher universal debt. All of this means the gold price will continue to rise.

Competition for the World’s Gold

Finally, as a direct result of world-wide debt and currency debasement, more people will be competing for the world’s available gold. We discussed peak oil, but gold is also reaching a peak as fewer and fewer new deposits are being found. Smaller, lower grade deposits with none of the “economy of scale” benefits of larger deposits are being put into production out of desperation. Mine supply has been in a decline since 2000.

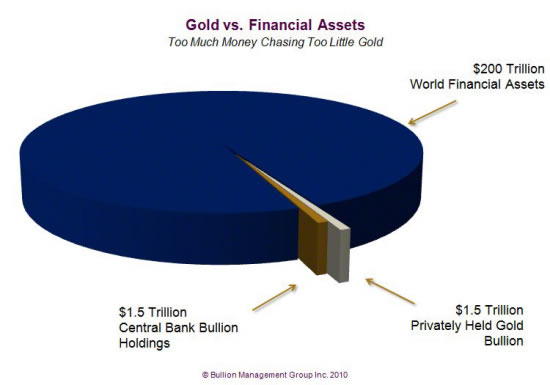

As safe haven demand accelerates, there will be a transition from the $200 trillion of financial assets to about the $3 trillion of above ground gold bullion. Of the $3 trillion of above ground gold bullion about half is owned by central banks and half is privately held. The privately held gold is largely held by the world’s richest families and is not for sale at any price. The central banks are now net buyers. If the world’s pension funds and hedge funds moved only five percent of their assets into gold, which these days seems quite conservative, gold would trade above $5,000.

So in conclusion, I will say that without any new financial crisis, both mid-term and long term trends are in place to ensure gold and silver will continue rising through 2011 and well beyond. For those of you who are looking for a prediction...last year at the Empire Club, I forecasted that the price of gold to be between $1300 and $1500 at the end of 2010. We ended up right in the middle at $1405. For 2011, I recently forecasted it may climb to $1,700 to $2000 per ounce based on the last five years performance and the factors I have presented today.

I encourage you to follow the example of those who know how devastating a currency crisis can be and buy gold to protect wealth and not treat it as speculation. I’d like to close with a quotation that seems to put all of this into perspective. It comes from Norm Franz’s appropriately titled book, Money and Wealth in the New Millennium. He said, "Gold is the money of kings; silver is the money of gentlemen; barter is the money of peasants; but debt is the money of slaves."

Thank you.

The speech was also presented by Nick in Montreal and Vancouver on January 7th and 10th respectively as part of the Investment Outlook 2011 Series.

By Nick Barisheff

Nick Barisheff is President and CEO of Bullion Management Group Inc., a bullion investment company that provides investors with a cost-effective, convenient way to purchase and store physical bullion. Widely recognized in North America as a bullion expert, Barisheff is an author, speaker and financial commentator on bullion and current market trends. He is interviewed monthly on Financial Sense Newshour, an investment radio program in USA. For more information on Bullion Management Group Inc. or BMG BullionFund, visit: www.bmginc.ca .

© 2011 Copyright Nick Barisheff - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.