World Economic Forum Endorses Fraud, "Need to Double Credit in 10 Years"

Economics / Credit Crisis 2011 Jan 24, 2011 - 06:28 AM GMTBy: Mike_Shedlock

A few days ago I received an email from the World Economic Forum regarding a need to double credit over the next 10 years. Here is that email.

A few days ago I received an email from the World Economic Forum regarding a need to double credit over the next 10 years. Here is that email.

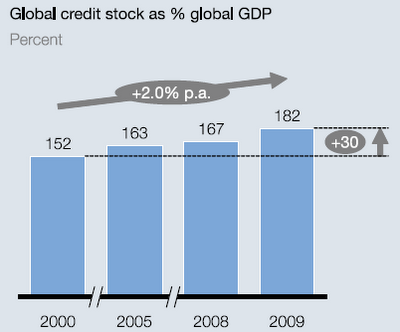

New York, USA, 18 January 2011 – Credit levels will need to double over the next 10 years, growing by US$ 103 trillion, to support consensus-projected economic growth. This doubling of credit could be achieved without increasing the risk of major crisis, finds More Credit with Fewer Crises: Responsibly Meeting the World’s Growing Demand for Credit, a report released by the World Economic Forum in collaboration with McKinsey & Company. The study develops a detailed global credit model using historical credit volumes and forecasting potential credit demand to 2020 across 79 countries, representing 99% of world credit volume. The study applies a sustainability methodology to the projected credit demand, using newly developed metrics to answer the following two questions: Will credit growth be sufficient to meet demand? Is there a risk of future credit crises and, if so, where?

The accompanying PDF entitled More Credit with Fewer Crises is 84 pages of economic claptrap. The main mission of the World Economic Forum appears to cram more credit down the throats of a world so stuffed with credit it cannot possibly be paid back.

Australian economist Steve Keen found three major flaws in the report. There are many others. Inquiring minds will certainly want to read Keen's WEF-mocking analysis entitled How I learnt to stop worrying and love The Bank.

The three flaws Keen spotted are:

- Poor starting year for the report

- Report ignores financial sector debt

- Report ignores Ponzi schemes

A Not-So Robust Study

The WEF brags "To create a robust fact base for the study, a detailed global credit model was constructed to map credit volumes between 2000 and 2009, and to project potential credit demand to 2020. The model spans 79 countries representing 99% of world credit volume."

I would specifically like to point out the absurdity of calling a study "robust" that only encompasses only the last 10 years, ignoring the great depression, WWI, WWII, the Great Society, the rise and fall of unions, the effects of baby boomers moving through the economy, and the move from one to two wage earners in a family.

Debt Slaves and the Expansion of Credit

I also point out the study does not mention Bretton-Woods, Nixon closing the gold window, or how wealth has become increasingly concentrated in the hands of fewer and fewer people, while those in debt have become debt slaves for life.

It's important to understand that rampant credit expansion is in and of itself inflation. My precise definition is "Inflation is a net expansion of money and credit, with credit marked-to-market.

The primary beneficiaries of "inflation" are those with first access to credit: banks, government, and the wealthy. By the time credit filters down to those lowest on the totem pole, those who take credit are screwed. The housing bubble is proof enough.

Credit bubbles pop, they always do. Thus, the idea that the WEF can put in place procedures to identify bubbles while openly promoting the doubling of credit is simply preposterous.

First let's discuss the proper starting point for analysis.

Fractional Reserve Lending Is Fraud

Here are two easy to read, free online books that make the case.

Here are hardcopy versions you can order.

- The Case Against The Fed by Murray Rothbard

- What Has Government Done To Our Money by Murray Rothbard

- End The Fed by Ron Paul

If you haven't read them, read them. If you have read them, read them again. Then meet with your legislative representatives and get them to read the books. Better yet, buy them a hardcopy so you can be sure of it.

Fraud aside, let's move on to a discussion of blatant errors in the report.

Sustainable Credit Growth

The WEF says "Between 2000 and 2009, the world economy was growing at a healthy rate – at 5.3% annually in nominal terms, or 2.2% in real terms. The rate of GDP growth between 2000 and 2008 was 6.2% nominal and 2.8% real. This means that the world’s stock of credit outpaced GDP growth by less than 2 percentage points a year – not a wide margin. In theory, there is nothing unsustainable about this picture: as long as credit grows broadly in line with economic growth, the credit is put to good use and borrowers can meet interest obligations and repay principal."

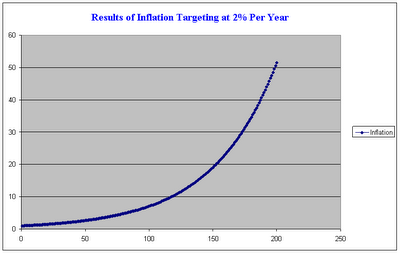

Have you ever seen a chart of what 2% compounded looks like?

Here is a chart of Bernanke's 2% inflation targeting. Note that 2% can represent 2% excess credit growth or anything else.

Inflation Targeting at 2% a Year

Many bad things can happen with Bernanke's 2% inflation target.

- Wages do not keep up.

- Asset bubbles build

- Rising asset prices make it appear debt is sustainable

- Wage growth is disproportionate to debt

- Wealth concentration

- By the time bubbles are spotted it is already too late

- Recessions happen

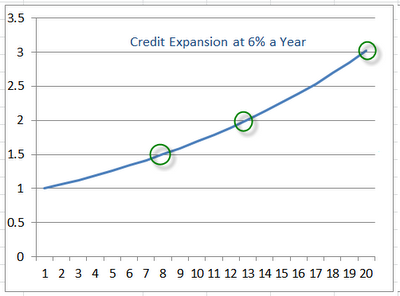

Credit Expansion at 6% Per Year

Wages vs. Credit Expansion

At 6% per year credit expansion, credit is up 50% in 8 years, 100% in 13 years, and 200% in 20 years.

Did after-tax wages go up by 50% in the last 8 years? Did after-tax wages go up 100% in the last 13 years? We all know the answer to those questions.

We also know that although incomes did not increase that fast, property taxes are most assuredly up 100% in the last 13 years (except in capped states) and real wages are negative.

Real wages are hugely negative for the bottom 80% of the population.

Yet the WEF thinks that credit expansion of 6% is sustainable and it does not fully understand what even happened.

WEF Ignores the Wealth Effect and the Price of Credit

It's pretty easy to explain what happened: People "felt" wealthy by rising asset prices (homes and the stock market). Credit was granted on the basis of rising asset prices and an asinine belief that home prices will rise forever into the future.

Credit expanded but wages did not.

Property bubbles resulted from credit priced too cheaply. Failure to discuss the price of credit is of course yet another flaw in the report.

Equity and Commodity Prices Already Back in Bubble Territory

Amazingly the WEF cannot figure out what happened or that asset prices with the exception of the US housing market are already back in bubble territory.

Bear in mind we still have not gotten to Steve Keen's objections to the report. Here we go.

Poor Starting Year for the Report

Steve Keen mocks the starting year of the report with a nice series of graphs.

Keen quips:

How could I ever have thought that the growth of credit could have caused the Great Recession, when in fact the growth rate of debt has been negative?Credit a "Human Right"?!

I am also chastened to realise that credit is only used for good purposes. As the report notes: In the long run, the scale and distribution of credit is only economically sustainable if it also meets society’s broader social objectives. Muhammad Yunus, founder of Grameen Bank, goes so far as to say that credit is a human right, and adds: "If we are looking for one single action which will enable the poor to overcome their poverty, I would focus on credit."

Foolish me: here was I, thinking that credit might also be used to fund Ponzi Schemes.

Yunas seriously has holes in his head. Credit is not a right.

The global housing bubbles are proof enough of what happens when credit is extended to those who are not credit-worthy.

Certainly there are countries where there is little or no credit. It might behoove Yunas to figure out why.

It's easy to figure out if you think in reverse. What do countries have in common where credit is generally available? Here's your answer.

- property rights

- rule of law

- civil rights

Fix problems in those areas and credit will likely be available.

This next section is in regards to financial sector debt, the second fundamental flaw Keen spots in the report.

Why omit financial sector debt?

The report omits borrowing by within the financial sector from its record of total debt, when this has been a major component of the growth of debt (certainly in the USA) in the last 60 years. I include financial sector debt in my analysis for two reasons:

- The initial borrowing by the shadow banking sector from the banks creates both money and debt;

- The money lent by the shadow banking sector to other sectors of the economy creates debt to the shadow banking sector, but not money

I frequently get the argument that debt within the financial sector can be netted out to zero, but I think this ignores those two factors above: the creation of additional debt-backed money by the initial loan, and the creation of further debt to the financial sector—most of which has been used to fund asset bubbles rather than productive investment.A focus on total private sector debt during and after the Great Depression also conveys a somewhat different perspective.

Did you catch that subtle reference to fractional reserve lending?

"I frequently get the argument that debt within the financial sector can be netted out to zero, but I think this ignores those two factors above: the creation of additional debt-backed money by the initial loan, and the creation of further debt to the financial sector—most of which has been used to fund asset bubbles rather than productive investment. "

I am waiting for Keen to come flat out and explicitly state that Fractional Reserve Lending is fraudulent. He sure hints at it, without saying the words.

Indeed, it is fractional reserve lending that is the root of most of the huge credit Ponzi schemes. Speaking of Ponzi schemes, Keen discusses his third objection to the report.

Why ignore Ponzi Schemes—and Minsky?Sustainable Credit: A Challenge of Definition (from the report)

The report’s listing of the uses to which credit is put is so innocent as to make me wonder whether one of the author’s primary school children wrote the relevant paragraph: "In early stages of development, credit is used to support family-owned businesses; next, it supports small and large corporations; and finally it is used to smooth consumption."

But maybe I’m being harsh: it could, after all, have been written by a neoclassical economist.

Please, let’s get real: yes credit can do all of those things, but it can also fund asset bubbles and Ponzi Schemes, and that has been by far the dominant aspect of credit growth since the report’s base year of 2000, and arguably since the 1987 Stock Market Crash. To ignore this aspect of credit after the biggest financial crisis since the Great Depression is simply puerile.

Prior to 2008, such ignorance was excusable simply because it was so widespread, as the dominant neoclassical school simply ignored dissidents like Minksy. After the crisis, he is receiving long overdue respect for focusing on the importance of credit in a capitalist economy while neoclassical economists effectively ignored it.

This study recognized it would be no easy task to come up with a definition of sustainable credit that was both specific enough to be meaningful and broadly accepted by public and private decision-makers. Before attempting a definition, therefore, the study canvassed the question – “What is a sustainable level of credit?” – in interviews with more than 50 industry CEOs, rating agency executives, central bankers, regulators and academics.Interview Bias

Although there was a breadth of perspectives among these experts, there was also significant convergence. In particular, while a minority of interviewees believed current absolute levels of borrowing were unsustainable and would require substantial deleveraging, the general view was that the current global credit stock is at sustainable levels but should be rebalanced towards economically beneficial uses. In this view, the recent financial crisis was driven by ineffective monitoring and managing of information asymmetries, which drove misallocation of credit and excess contagion risk.

Note that McKinsey interviewed all the people who benefited from the bubble. CEOs, rating agency executives, central bankers, and regulators all were beneficiaries of the credit expansion. Of course they are going to agree on the need for more of it even if they cannot come up with a precise definition.

Report Bias

Report bias is even more basic than interview bias. The study's mission seems to be to determine how much credit is needed to achieve desired GDP growth. What if the desired GDP growth is flawed?

No Challenge At All

I can easily define "sustainable credit" conditions. All it takes is a 100% gold-back dollar and no fractional reserve lending. Heck, abolishing fractional reserve lending alone would do it.

Will Credit Growth Meet Demand?

I have to laugh at the ridiculous question the report asks: Will Credit Growth Be Sufficient to Meet Demand? In short, there will be significant challenges in channelling credit to where it is needed.

In a fractional reserve lending system with credit priced too cheaply and central bankers willing to act as lenders of last resort, the last worry anyone should have is whether credit growth will be sufficient to meet demand.

By the way, did you catch the flaw in the question itself? There is unlimited demand for credit if credit is cheap enough. As I pointed out before, the article forgot to address "the price of credit" and that silly question highlights the flaw.

Bear in mind that in a deflationary environment the price of credit might have to drop to zero, perhaps even negative, before any credit worthy borrowers want it, but priced right, there will unlimited demand for credit.

Report's Absurd Conclusion

The financial crisis not only shook the foundations of the world economy, it also suggested to many observers that overall credit levels were unsustainably high and would need to be scaled back. The analysis in this report provides a different perspective: credit demand will grow strongly in the decade ahead, and meeting this demand is not only sustainable in principle, but also essential if the world is to meet its economic development goals.

Report Confuses Inflation and Government Spending with Growth

Flaws after flaws after flaws mount up. The paragraph above shows the authors do not know the difference between real growth (production and output), vs. "economic development goals" as measured by arbitrary measures of GDP and government spending.

Government spending, no matter how ridiculous, adds to GDP by definition. Note that it has taken fed balance sheet expansion by $2 trillion and deficit spending of $1.5 trillion just to get a GDP rising at a 3% clip.

Also note that taxpayers bailed out the banks but still hold the debt. That situation holds true in the US, Ireland, and Spain (places where the housing bubble popped). The housing bubble is bursting in Australia right now and will burst in Canada, the UK, and China at some point.

Every one of those bubbles was caused by credit expansion yet the report's conclusion is we need more credit. The report's major worry is credit expansion will be insufficient.

Summary of Flaws

I have never seen such a collectively pathetic group effort of 50 people since I started this blog six years ago. It appears to have been written in Bizarro-World or some alternate universe where economic laws and common sense run in reverse.

- Failure to understand the role of Fractional Reserve Lending

- Failure to consider the price of credit

- Failure to discuss the beneficiaries of inflation and credit expansion

- Interview bias

- Report bias

- Failure to encompass sufficient economic history

- No consideration of credit expansion as a cause of the Great Depression

- No discussion of the role of Bretton Woods or central bankers on credit bubbles

- Participants do not understand inflation

- Report did not properly factor in wage growth or taxes

- Report did not consider global wage arbitrage as a limiting factor in Western economies

- Report did not consider income inequality

- Report does not understand the infeasibility of perpetual compounding at 6% annualized

- Report has no concept of valid human rights

- Report fails to consider wealth effect

- Poor starting year for the report

- Report ignores financial sector debt

- Report ignores Ponzi schemes

Click Here To Scroll Thru My Recent Post List

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.comMike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .© 2011 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.