Welcome to Financial Slaughterhouse

Stock-Markets / Credit Crisis 2011 Apr 25, 2011 - 02:42 AM GMT

"There are no characters in this story and almost no dramatic confrontations, because most of the people in it are so sick and so much the listless playthings of enormous forces."– Kurt Vonnegut, Slaughterhouse-Five

"There are no characters in this story and almost no dramatic confrontations, because most of the people in it are so sick and so much the listless playthings of enormous forces."– Kurt Vonnegut, Slaughterhouse-Five

Hardly a day goes by without an excellent analysis of hard facts and data being followed by a surprisingly disconnected conclusion. Over the weekend, it appeared to be Zero Hedge's analysis of a video report by Eric deCarbonnel of Market Skeptics, which concluded that the Federal Reserve, U.S. Treasury market, and U.S. dollar may all be on the verge of imminent implosion due to the Fed's AIG-esque policy of selling large amounts of protection against an increase in Treasury bond rates. A rebuttal to this view was provided the next day on The Automatic Earth, in a piece entitled Bailing Out The Thimble With The Titanic.

In this piece, it was essentially argued that the U.S. dollar and Treasury market are symbolic of the Fed and the financial elite class, as partly confirmed by deCarbonnel's report, and these elite institutions have been engineering a successful bailout of those markets over the last few years, in tandem with natural financial dynamics and at the expense of everyone else. The bailout was "successful" in the sense that those markets will most likely remain stable in value for at least the next 2-3 years. On April 19 we were provided an excellent report by Chris Martenson, entitled The Breakdown Draws Near, but, as usual, all roads lead to financial chaos in Washington, D.C.

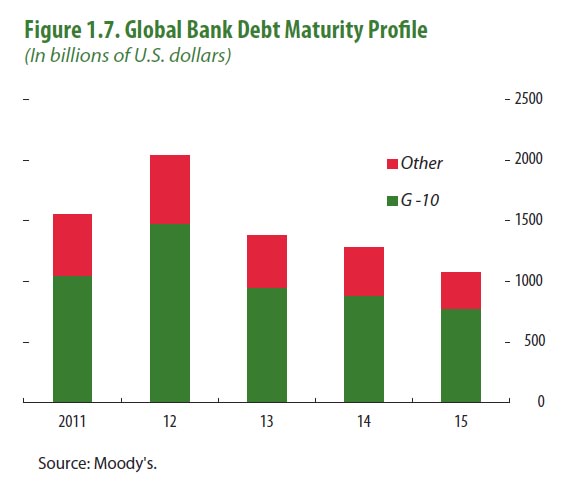

The "excellent" part of the report comes from the thorough data it provides regarding global liabilities that are maturing for banks and governments over the next few years. First, we are given a reference to the IMF's conclusions regarding global bank liabilities maturing in the near-term, with a stern eye locked on Europe [1]:

The world's banks face a $3.6 trillion "wall of maturing debt" in the next two years and must compete with debt-laden governments to secure financing. Many European banks need bigger capital cushions to restore market confidence and assure they can borrow, and some weak players will need to be closed, the International Monetary Fund said in its Global Financial Stability Report.

The debt rollover requirements are most acute for Irish and German banks, with as much as half of their outstanding debt coming due over the next two years, the fund said.

The IMF basically tells us what has become painfully obvious by now - European banks and governments are both struggling to acquire the capital necessary to service their existing and/or refinance maturing debts, and there isn't nearly enough to satisfy them both. The latter fact is especially true when factoring in the maturing liabilities of banks and governments in other parts of the world, which is something that Martenson focuses on in the remainder of his analysis.

It is important, however, to note the added twist in the IMF's statement, in which it says that "some weak players will need to be closed". While it is specifically referring to European banks, the logic can be applied just as well to banks and governments all around the world, but we will return to that point later. In the rest of Martenson's report, we find out that Spain is actually pinning a significant portion of its private financing hopes on China, which, in turn, is facing its own imminent financial crisis due to an imploding real estate bubble.

But it is Spain that is first in the firing line and its 10-year bond premium in the secondary market widened 14 basis points to 194 bps. Madrid is hoping for support from China for its efforts to recapitalise a struggling banking sector... [2]

Prices of new homes in China's capital plunged 26.7% month-on-month in March, the Beijing News reported Tuesday, citing data from the city's Housing and Urban-Rural Development Commission. [3].

We can also expect that housing bubbles in countries such as Australia and Canada will start to implode in lockstep with China, as their economies are both highly dependent on Chinese import demand for natural resources. A renewed round of real estate busts, combined with the ongoing slump in Europe and the U.S. and less aggressive monetary policy (-temporary- winding down of QE), will also feed off of and into a collapse in global equity and commodity values. That collapse will wipe out large swaths of imaginary capital existing on the books of major institutions. All of that leads us to Martenson's seminal question, "Who Will Buy All of the Bonds?", specifically meaning the public bonds of Europe and the U.S.

Martenson refers to the Treasury International Capital (TIC) Report in his piece, which indicated that there was a "lower-than-trend" net inflow of foreign capital ($26.9B) into long-term securities for the month of February, which includes those going into long-term Treasury bonds. When including short-term securities, we see that there was a healthy net inflow of $97.7B into U.S. bond markets from foreign investors. [4]. What this data indicates is that, during the month of February, there was significant foreign investment in U.S. bonds, but 72% of that was into short-term securities (which do not include 10 or 30-year Treasury bonds).

He goes on to conclude that this inflow dynamic will get worse as Japanese purchases drop off in the next few months, and that the proposed "spending cuts" for a few federal programs will hardly do anything to reduce the supply of Treasury bonds over this same time period. I agree that there is a strong possibility of reduced purchases by the Japanese government in the short-term, as well as the governments of China and the UK. In addition, the minuscule spending cuts will indeed be irrelevant to the overall size of the 2011-12 federal budget deficits.

To go from there to the conclusion that the U.S. Treasury faces an imminent funding crisis, however, requires a few major and unlikely assumptions; the classic hallmark of those fretting over hyperinflation of the dollar in the short-term. As briefly discussed above, a slowdown in foreign government purchases of U.S. Treasury bonds could be significantly offset by an increase of inflows from private foreign investors fleeing the equity, commodity, government agency and mortgage-related investments of other regions, as well as domestic investors fleeing those same risky investments.

And that's where we return to the IMF's little "hint" in its report from last week. The financial elites do not need anyone to buy ALL of the bonds, only those that are most important to maintaining their wealth extraction operations. The weak players? Well, they can all fight over the scraps and devour themselves in the financial marketplace. The truly significant capital will be transported towards a few central locations by natural forces and by human design, like lambs to the inevitable slaughter. Of these locations, the most critical are surely the U.S. Treasury market, which can be used to support major U.S. banks, and the U.S. currency market.

What are the chances that the majority of people who find themselves invested in U.S. government bonds and the dollar will get anything close to a return on their investment over 10, 20 or 30 years? The answer to that is probably a massively negative percentage, because the psychological pain of holding on for that long will be even worse than the total wipe out itself. However, the herd typically doesn't figure out how close they were to the edge of the cliff until after they are tumbling down the other side.

Stoneleigh at The Automatic Earth has repeatedly pointed out that people in such fearful environments tend to discount the future by an increasing rate, which means they care less and less about what will happen several decades, years or even months from the present time. The discount situation of financial elites is similar because they know how precarious the dollar-based financial markets are, so their concern is over whether they can corral all of the lambs into one or two places over a relatively short time period. So far, most of the evidence says that not only is it possible, but the process is already well under way.

Another unlikely assumption contained in Martenson’s report is the following [emphasis mine]:

With the Fed potentially backing away from the quantitative easing (QE) programs in June, the US government will need someone to buy roughly $130 billion of new bonds each month for the next year. So the question is, "Who will buy them all?"

I say the above question is an unlikely assumption because it seems to imply that the Fed may stop QE for another whole year after the QE-lite and QE2 programs wind down. If recent history has taught us anything, it's that a fearful deflationary environment is the perfect justification for the Fed to resume QE, and perhaps at an even larger scale than it has "monetized" in the past. Will the American people be up in arms about monetization of the federal debt or an indirect link to sociopolitical unrest, when their own finances, homes and careers are once again being beaten down by the unrelenting force of debt deflation? I really doubt they will be.

In the next section of his article, Martenson himself refers to how significant QE has been when talking about proposed budget cuts [emphasis mine]:

For the record, these 'cuts' work out to ~$3 billion less in spending each month, or less than the amount the Fed has been pouring into the Treasury market each business day for the past five months.

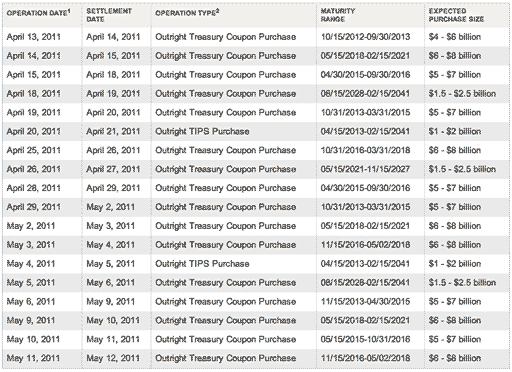

In addition, as discussed in Bailing Out The Thimble With The Titanic, the Fed may also be using Treasury put options to help them exert more control over long-term rates that cannot be reached as easily by QE programs. With regards to the latter, the following table is the Fed's "liquidity injection" schedule for the next month, which is certainly winding down, but still towers over any notional amount that has been "negotiated" by the politicians on Capitol Hill in their budget talks [5]:

The other major assumption involved here is that interest rates will start to rise along the curve, and this will make sovereign default much more likely, since a significant portion of Treasury debt is in notes with relatively short-term maturities. This logic is circular at best, since it relies on the fact that sovereign default and/or inflation concerns will drive short-term interest rates up in order to posit the argument that increased short-term interest burdens will lead investors to be more concerned about sovereign default or inflation (from printing). There is certainly a positive feedback involved in such dynamics, but the feedback must be rooted in some initial economic or political trigger.

As mentioned earlier in this piece, and many other times on The Automatic Earth, the dominant and natural economic trend is debt deflation, while the dominant (and natural) political trend is aggressive fiscal and monetary policies that are crafted to funnel money into major banks, rather than the productive economy. There are very few reasons to think that either of these trends will reverse in the short-term, either by design of the financial elite class or by the inadvertent consequences of their actions. They have no doubt painted themselves into a corner, but their corner is significantly larger than the concentration camps built to imprison a large majority of the global population. The latter fact is clearly evidenced by the perpetual taxpayer subsidies given to financial institutions in the sullied names of "economic recovery" and "austerity".

The cities of Greece continue to erupt in violence as its citizens are forced to bail out European banks, and, meanwhile, Americans continue to mistake their own reflections in the global mirror. Earlier this year, Standard & Poor's rating agency downgraded the outlook for the triple-A rated status of Treasury bonds (from "stable" to "negative"), in what was nothing less than an act of aiding and abetting the politicians, bankers and major corporate executives who strive for the imposition of austerity on everyone but themselves. The only difference between Greece and the U.S. is that the latter is not a "weak player" in the eyes of elite institutions, such as the IMF. Which means that, while the Greek taxpayers may soon be put out of their misery, we will die a much slower death, choking on our own debt for years to come.

"He kept silent until the lights went out at night, and then, when there had been a long silence containing nothing to echo, he said to Rumfoord, "I was in Dresden when it was bombed. I was a prisoner of war."

- Kurt Vonnegut Slaughterhouse-Five

Ashvin Pandurangi, third year law student at George Mason University

Website: "Simple Planet" - http://theautomaticearth.blogspot.com (provides unique analysis of economics, finance, politics and social dynamics in the context of Complexity Theory)

© 2011 Copyright Ashvin Pandurangi to - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.