Yen's Hidden Global QE Signal and Gold Breakout

Commodities / Gold and Silver 2011 Jul 14, 2011 - 02:12 PM GMTBy: Jim_Willie_CB

Take a short break from all the hubbub in the United States over the faltering USEconomy, the reckless politicians pretending to come to a USGovt budget agreement (small or large), and the tacit admission by USFed Chairman Bernanke that indeed QE3 is very likely. The June Jobs Report confirmed my forecast of a moribund economy in deterioration. The Republicans will not budge on their refusal to approve tax increases. The Democrats will not budge on their refusal to approve entitlement cuts. The Pentagon through hidden pressures has managed to keep the sacred war off the table for discussion, even though it stands as the largest factor in the federal deficits. But the queer item is that President Obama spent most of his time in the last six weeks raising $86 million for his re-election campaign. His taking the high road in the budget discussion reeks of hypocrisy.

Take a short break from all the hubbub in the United States over the faltering USEconomy, the reckless politicians pretending to come to a USGovt budget agreement (small or large), and the tacit admission by USFed Chairman Bernanke that indeed QE3 is very likely. The June Jobs Report confirmed my forecast of a moribund economy in deterioration. The Republicans will not budge on their refusal to approve tax increases. The Democrats will not budge on their refusal to approve entitlement cuts. The Pentagon through hidden pressures has managed to keep the sacred war off the table for discussion, even though it stands as the largest factor in the federal deficits. But the queer item is that President Obama spent most of his time in the last six weeks raising $86 million for his re-election campaign. His taking the high road in the budget discussion reeks of hypocrisy.

The absence of leadership in the executive branch is matched by an equal absence in the Congress. The leadership at the US Federal Reserve is clear, but the incompetence and lost credibility has rendered the bumbling professor chairman a mere Wall Street tool whose ample tools dole out capital destruction. Bernanke must react to the USTreasury Bond market pressures as much as his own long string of steadily wrong forecasts. My forecast was for QE3 to come by summer. The blueprints are on the table. The head fake and diversion drivel spouted by Helicopter Ben were ignored by the Jackass, just like the Green Shoots and Exit Strategy and No QE2 distractions in the last two years. Quantitative Easing will go viral next, enough to call it Global QE. Gold & Silver will react, gold first with solid gains, then silver with massive gains to follow. The common theme is the ruin of money. Watch Italy for an extremely robust toxic powerful addition to the entire dangerous mix. Its nation is very large, whose debts are huge.

In March the earthquakes and tsunami struck with a vengeance. Amidst the rubble came a financial response of obscure variety, reminiscent of the Kobe earthquake of 1995. The response was an emergency G-7 Meeting of finance ministers to soak up all the USTreasury Bonds dumped en masse by the Japanese collectively. Not just the Bank of Japan, but the many insurance companies and financial firms were into the act, raising huge sums of money. Reconstruction claims, stock market swoons, and corporate relocation costs mounted. They all sold from the hoard of USTBonds accumulated over the decades from the Yen Carry Trade. Twenty years of near 0% rates in Japan, contrasted to semi-normal rates in the United States made for a grand carry trade for speculators, the Japanese financial entities being the expert. The coordinated sponge effect of the Western nations to take what Japan sold, to do so off the grid of the FOREX markets. That enabled the Japanese Yen to fall from the flashing signal at 128 down to a tame 117. All was fixed, all cured, crisis averted. Not so fast!! The reconstruction in Japan, along with a wide array of related costs, would not go away so easily. It is back!!

GLOBAL QE

In a Jackass piece entitled "Currency Deadend Paradoxes" from late April, warning was given in the form of a forecast. The Yen currency would rise, contrary to conventional thinking. It has done precisely that, a correct call, but the best part of the move has yet to come. The rationale for the forecast was sale of foreign assets to finance reconstruction, to cover the newly arriving trade deficit, and to alleviate political pressures against further wreckage of the government budget. Two decades of stimulus failed to achieve much economic rebound and recovery from the 0% dead end on the monetary road, a lesson the Americans never learned. Their heads are too steeped in arrogance to bother to learn basic economics and finance. In April, the Jackass harsh words were "The dull blades posing as economists in the United States fail to observe the Japanese lesson that a nation never emerges from the 0% corner. To admit this is to admit a failure of the monetary system and central bank franchise control tower." The words still apply. Revisionist history prevailed, just like with Professor Bernanke and his aberrant revisionist account of the Great Depression. We are learning that mass deployment of the electronic money printing machine has indeed a wicked cost, hardly free, in the form of a rising global cost structure and powerful profit squeeze. The result is an economy in permanent recession. My description of the G-7 Accord to sell down the Japanese Yen via backroom purchase of USTBonds was GLOBAL QE. With the mushroom of European sovereign debt ruin, the contagion to Italy and soon Greece, the declaration of junk status for Portugal and Ireland in addition to the toxic paper blowing from Mt Olympus, the new dawn of Global Financial Crisis part II has hit.

THE JAPANESE YEN BREAKOUT

My eye never stopped watching the J-Yen currency exchange rate since May. A couple of feints were cut off at the pass. But here in July, at the supposed ordered end of QE2, the game is on again. The 125 resistance level has been shattered on the third attempt since April. This time, another Global QE will be needed to stop the Yen from rising more. The reconstruction is underway. Insurance firms are cashing in to raise funds urgently needed. The financial firms are recognizing yet another important liquidation phase in the Yen Carry Trade. Those who delay in liquidation will face huge losses. This is an important unrecognized short cover squeeze on the Yen currency. It is the hidden signal. Look for rising price inflation on imports to the USEconomy. Add Japan to China as the source of rising prices to US retail shelves on finished electronic products.

The April analysis included many important points in my view, enough to warrant this article as followup. The most salient points are worth repeating. They apply in spades here and now. The recent action in the Japanese flagship Nikkei stock index below 10,000 has sparked a torrent of USTBond sales for rescue funds outside the Japanese walls. A weak stock market has conspired with reconstruction costs due. Foreign asset sales finally hit critical mass. The article from the spring made these points. The paradox finally has hit the billboards in plain view. Domestic disruption to the vast industrial and car supply sector can next combine with a slower USEconomic demand to bring the trade deficit into view.

The after effects in Japan will work in numerous hidden ways to lift their Yen currency. Its steady stubborn rise will confuse the constantly wrong-footed economists. The next phase inside Japan will include an unspoken emphasis of foreign asset sales in order to fund the staggering costs and to avert price inflation. Additional debt with Yen markings risks a surge in domestic price inflation. In the next year, the Japanese trade balance will turn into an outright deficit. The trade deficit will not keep down the Yen exchange rate down. The deficit will send into reverse the process of suppressing the Yen currency for 20 to 30 years. No longer will the Japanese financial institutions, led by the BOJ, purchase the USTBonds.

The critical point was reached three weeks ago when an emergency G-7 Meeting was convened. Its purpose was coordination to buy USTBonds and keep the Yen down, ergo Global QE. The Yen Sale Pact was never called Global QE but that is the proper interpretation, since all major central banks became USTBond buyers of last resort. The Gold & Silver market properly interpreted the event, and surged to breakout levels. The effect of the G-7 desperate clumsy pact was temporary. The trade deficit will not keep down the Yen exchange rate down. Contrary to standard economic theory, their trade gap will push up the Yen currency. Such a Jackass forecast goes directly contrary to their broken standard theoretical concepts, few if any have shown to contain much validity or sinew to hold together the broken planks of their financial theory. The Japanese Yen currency will continue to rise even though a trade deficit comes. Their trade surplus used to enable vast funds to suppress the Yen, now gone. The Japanese will sell foreign assets to cover the deficits. They will have to avoid price inflation by selling available foreign assets, in particular the plentiful US$-based assets. Banks will lead the final phase of the Yen Carry Trade unwinding process. Insurance companies will unload US$-based assets in order to finance claims. The financial firms will unload US$-based assets so as to protect Japanese stock values.

A SOUR EURO: THE NEW FACTOR

A new factor has joined in the push to breakout. Emerging market nations are storing reserves more and more in the Japanese Yen. Either a rising Euro or the toxic Euro-based sovereign debt has deterred investment of reserves. No longer do the emerging market nations regard the Euro currency as a fine upstanding alternative to the increasingly suspect USDollar. The USDollar is sliding in the role at asset held in FOREX reserves. Its reserve currency status is widely questioned. In a single decade, the USDollar share of reserve assets fell by over 11%, a huge amount. In the last twelve months, the share fell by another 1%. In the meantime, the Japanese Yen, Aussie Dollar, and Canadian Dollar are relied upon more. One can understand the movement to the other dollars with their strong resource and mineral riches. The rising commodity price trend has given strong support to the Aussie and Loonie. The revolt continues, as confidence is eroding. The USDollar share of global reserves continues to decline, and its reserve status has been called into question. An Intl Monetary Fund report was released in late June. The Composition of Official Foreign Exchange Reserves (COMFER) lists reserves held at central banks in 33 developed economies and 105 emerging and developing economies. Further confirmation came that the USDollar is gradually losing its reserve status. The USDollar slipped. The Euro slipped. But the Japanese Yen, the Aussie Dollar, and the Canadian Dollar gained. Gradual diversification is happening. Gaping USGovt deficits, debt limit roadblocks, profound bond fraud, protection of big US insolvent banks, and outright hyper monetary inflation by the USFed to cover the deficits have contributed to the USDollar decline. China was not part of the sample, curiously or intentionally.

The US share of allocated reserves fell by the end of 1Q2011 to 60.69%% from 61.53% in Q4 2010. Central Bank reserves would have been steeper if China was included in the sample. The decline has been signicant over the last decade, a full 10% less. One year ago, the greenback share stood at 61.64%, almost one percent less. In 1Q2001, ten years ago, it stood at 72.3%, over 11% less. No longer is the greenback dominant. Nations are scurrying to diversify, in an act of self-preservation and bank system survival. In local discussions and at conferences such as the G-20, talks are held about a move toward a multi-currency system, which the US and UK leaders attempt to stall and sidetrack. The USDollar remains first among peers, but times are changing. Deflationist morons fail to notice, surely not its effect on costs. The global financial crisis has altered banking practices in a profound manner. Emerging and developing nations accumulated foreign reserves in high volume during the first quarter. Capital flows from the older economies has been huge. The data is shocking. Richer older nations added $65.5 billion in reserves, of those $1.6 billion in US$ terms. The data is staggering. Emerging markets added $366.3 billion in reserves, of those $65.8 billion in US$ terms. The Japanese Yen was a primary beneficiary of emerging market diversification. Their central banks accumulated $6.6 billion in new JPY reserves in the first quarter, lifting the allocation to 2.9%. The Canadian and Australian Dollars were other beneficiaries, whose share climbed to 5.8% from 5.1% in 4Q2010.

Emerging markets spot the European crisis unfolding in full glory. They have moved out a little from the Euro currency, where its share fell to 28.2%. But globally the Euro share rose to 26.6%, up a tiny amount. Nomura analysts reason that central banks reacted to the Euro strength as an opportunity to move into the Yen and other currencies. One can infer that the Yen is seen as a mature currency (yet it yields nothing on bonds), and the two other Dollars are resource currencies with strong national commodity supply. Expect the data in July to show less affection for the Euro, given the contagion has spread to Italy, and given the downgrade of Greece, Portugal, and Ireland to junk status. The COMFER report produced by the IMF continues to support the thesis that the USDollar is losing its reserve status. In a very gradual process of erosion, central banks rely upon stable allocations but they clearly are depending less and less on the greenback.

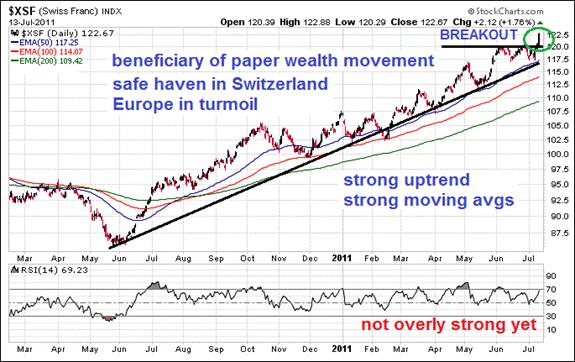

SNAPSHOT OF SWISSY

Gold bullion (along with Silver bullion) is the latest key reserve asset being vigorously pursued by central banks. Within the European continent, great distress is generated by the entire sovereign debt crisis. The government bonds from the Southern nations in Europe are equally toxic as the mortgage bonds of the United States. The other common thread is woven from the hand of Goldman Sachs, caught red-handed in corrupted currency swap contracts to conceal the Greek debt volume. Given the differentiation of Euro Notes from strong nation to weak nation, where bond yields vary wildly among the entire group of sovereign entities, the Euro currency has been able to trade on interest rate alone. The Euro Central Bank last week hiked rates by 25 basis points to 1.50% which gave more support to the common Euro currency. The entire sovereign debt crisis and strain on European banks, if not the EU economy, has opened the door for a paper wealth exodus to Switzerland. The small nation of 7 million people remains a haven for storing funds safely. The same cannot be said for gold bullion in private allocated accounts. Regardless of raids to allocated accounts, and massive footdragging on delivery upon demand, complicated by numerous multi-$million lawsuits, the move to Switzerland for storing funds in safe haven has been vast. While the Aussie Dollar and Canadian Dollar might be the resource plays in the currency market, the Swissie is the big fiat paper play in the FOREX. The Swissie has broken out above the 120 level. It is up 20% to 25% since the 2009 and 2010. The range for 2009 was SWF from 84 to 100. The range for 2010 was 86 to 106. The Swissie is the fiat paper story, while Gold is the metal story.

GOLD BREAKOUT IN MAJOR CURRENCIES

The gold breakout slams the Western bankers with all their chicanery in naked shorts of Gold & Silver, chicanery in dumping crude oil from reserves, chicanery in debt monetization of USTBonds, and chicanery in doctored economic reports. The crumbling monetary system continues. The sovereign debt contagion is in the process of jumping from Greece to Italy, a major escalation of bank risk and regional crisis. Spain is next. For context, consider that Italy is three times larger than Greece, Portugal, and Ireland combined. Italy has the largest debt burden and highest debt ratio in all of Europe. Italy has almost 60 million in population, six times larger than Greece. The grand daddy of all risk is the United States. Apart from the baseline risk of exceeding a rigidly enforced debt limit, the US looks remarkably like Greece in debt ratios. To be more accurate, the US is Greece times one hundred. Just as insolvent as a nation like Greece, just as absent in a fundamental industrial base. The second half recovery mantra nonsense in the USEconomy has been blatant propaganda for five years running. The second half will feature a powerful Gold & Silver breakout rally that will blow the socks off the public and investment community, and blow brown particulate matter with excretory chunks on banker faces. The keys are debt virus hitting Italy and Spain in Europe, and the recession accelerating in the United States. The US housing market is stuck in terminal decline, dragging down the big US banks which have toxic homes on their balance sheets. The kicker is the debt limit debate, and gross incompetence and lack of leadership exhibited within the USGovt.

Gold has broken out in US$ terms. The Gold price has extended gains to $1594 today. It is a CH away from $1600. Notice the wonderful W-shaped bullish reversal pattern. The double bottom has been established and retested. With a boxed low of 1475 and high of 1565, look for a target of 1655 in gold. Discount all talk from Wall Street on the Gold price. They are defending attacks on their own bunkers loaded still with toxic paper, together with court attacks to win restitution on mortgage bond fraud, even raiding their Loan Loss Reserves to augment profit stories. The clownish Bernanke actually told the USCongressional committee this week that gold was not money, contrary to a Greenspan position. Bernanke is an utter dolt, a hack financial engineer, a mad paper merchant, an ink salesman, a journeyman paper shuffler, a destroyer of capital. Gold is banking system ballast, absent since 1971, when the cost of the Vietnam War forced the Nixon Admin to abandon the Gold Standard and to defy foreign claims. The offshore exodus of Intel and other tech firms to the Pacific Rim produced a trade gap that forced the issue. The US is officially isolated. The Euro Central Bank is focused on price inflation, hiking rates. The USFed is focused on growth, stuck at the 0% rate. A great monetary schism is in progress. The rating agencies have decided reluctantly to do their job. To have USGovt debt at AAA is like calling a hurricane a bright sunny day, like giving the stupidest kid in class straight A grades, like having Ugly Betty win as the prom queen, like naming the Pittsburgh Pirates as baseball's best.

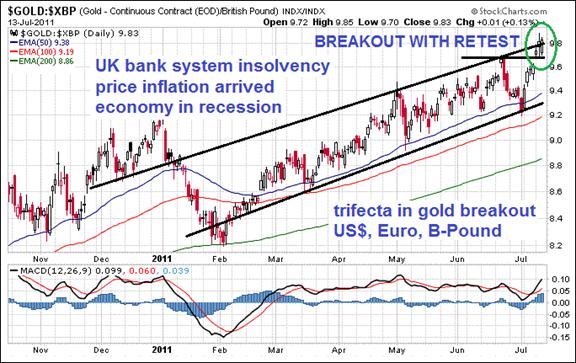

Gold has broken out in Euro currency terms. It is powerful and convincing, not too surprising since the sovereign debt crisis has its center stage in Europe. Notice the gigantic bullish triangle that has formed over the last several months. An impulse low of 9.65 and resistance of 10.85 yields a target of 1200 for Gold in Euro terms. A gap exists between 10.85 and 11.0, which should fill, maybe not, but probably yes. That is the European final entry opportunity for Gold investors. The Gold breakout in US$ terms and Euro terms makes for a strong confirmation. A potential wild card ugly might lie on the money market horizon in Europe, based in USDollars. It is on the verge of blowing up.

Gold has broken out in British Pound currency terms. That completes the trifecta in gold breakout in three major currencies. The UK banking system is in ruins. The UKEconomy is in deadly decline. Price inflation has arrived. Rupert Murdoch has provided a nice distraction in London, much bigger than Manchester United. The Gold price is flirting with a breakout in Canadian Dollar terms. There is no semblance of Gold breakout in either Swissie terms or Aussie Dollar terms, where the currencies are too strong. Prepare for a massive bull rally in both Gold & Silver from July through January. The yellow metal as usual will fight the political and banker battles and clear the path for the white horse metal to sprint. The Silver price gains in US$ terms will continue to triple the Gold price gains, but Silver must be given a little time to overcome the spiked springtime top near $50. All in time. The Commitment of Traders report on commercial positions indicates that Silver is ready to rock & roll once again. A very hot autumn is coming from precious metals, their annual strong season. Fireworks a plenty are in store. The global monetary system is crumbling, whose sovereign debt foundation is collapsing. It is that simple. Money is in ruins. Greece and Italy serve as detonation.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

At least 30 recently on correct forecasts regarding the bailout parade, numerous nationalization deals such as for Fannie Mae and the grand Mortgage Rescue.

"When I initially read your writings, they provoked a wide range of emotions in me from fear and anger to outright laughter. Initially some of your predictions ranged from the ridiculous to impossible. Yet time and again, over the past five years, I have watched with incredulity as they came true. Your analysis contains cogent analysis that benefits from a solid network of private contacts coupled with your scouring of the internet for information."

(PaulM in Missouri)

"Your analysis is absolutely superior to anything available out there. Like no other publication, yours places a premium on telling the truth and provides a true macro perspective with forecasts that are uncannily accurate. I eagerly await each month's issues and spend hours reading and studying them. Many times I go back and re-read the most current issue just make sure I did not miss anything the first time!"

(DevM from Virginia)

"I think that your newsletter is brilliant. It will also be an excellent chronicle of these times for future researchers."

(PeterC in England)

by Jim Willie CB

Editor of the “HAT TRICK LETTER”

Home: Golden Jackass website

Subscribe: Hat Trick Letter

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by compromised central bankers and inept economic advisors, whose interference has irreversibly altered and damaged the world financial system, urgently pushed after the removed anchor of money to gold. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy.

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 25 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.