The Split Personality of Gasoline and Diesel

Commodities / Gas - Petrol Sep 26, 2011 - 05:59 AM GMTBy: EconMatters

Crude oil tanked to its lowest in more than six weeks, amid a broad selloff in other commodities and equities with investors increasing fear of another global recession after the U.S. Federal Reserve warned of "significant downside risks" to the U.S. economy on Thursday, Sept. 22. Oil prices plunged $5.00 a barrel on that day, and as of Friday, Sept. 23, WTI sank to $79.96 a barrel, while the ever relentless Brent also retreated to $103.97.

Crude oil tanked to its lowest in more than six weeks, amid a broad selloff in other commodities and equities with investors increasing fear of another global recession after the U.S. Federal Reserve warned of "significant downside risks" to the U.S. economy on Thursday, Sept. 22. Oil prices plunged $5.00 a barrel on that day, and as of Friday, Sept. 23, WTI sank to $79.96 a barrel, while the ever relentless Brent also retreated to $103.97.

Market expectation is that crude oil prices are expected to continue to fall in the coming week on concern economic growth will slow in the U.S. and China, according to a Bloomberg survey. However, Financial Times noted a diverging expectation between the financial and physical traders:

“The crude oil market is witnessing a titanic battle: some macroeconomic hedge funds are betting on a drop in prices yet most physical traders are placing wagers that prices will rise.”

Reuters also reported in mid September that lower production and disruptions to North Sea, plus the loss of Libyan crude exports have “combined to produce an extraordinary backwardation across European crude markets.” Backwardation refers to the market condition where the price of a futures contract is trading lower than the spot price, which typically reflects a tight supply market for immediate purchases and deliveries.

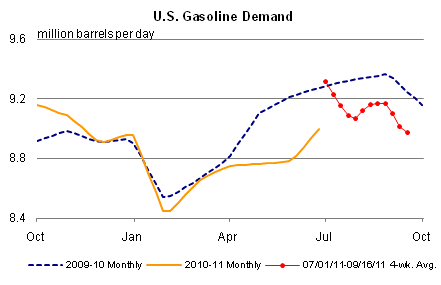

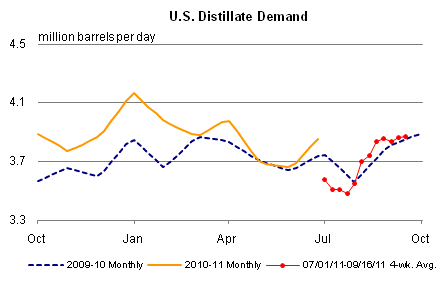

A similar split is also observed in the gasoline and diesel product markets. Bloomberg cited a report from API (American Petroleum Institute) that distillate fuel deliveries, which include diesel and heating oil, hit record highs, rising 11% year-over-year to 4.15 million b/d for the August month, while motor gasoline deliveries fell to a 10-year low. (See Charts Below). Overall, year-to-date product consumption averaged 19.1 million a day, down 0.3% from a year ago.

|

| Chart Source: EIA |

|

| Chart Source: EIA |

|

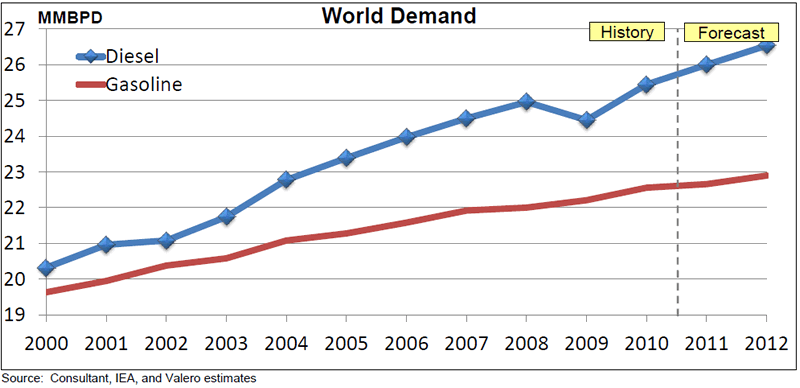

| Chart Source: Valero Presentation Sep. 2011 |

Older refineries in Europe and on the U.S. East Coast (since WTI is landlocked at Cushing, OK) that are not upgraded to handle heavy sour crudes generally prefer West African crudes due to their lower sulfer content (about half of the average Brent) and higher (up to twice more) distillate yield.

Rising diesel demand, increasing regulatory requirements to remove all sulfur, and the loss of Libyan crude all contributed to form a perfect storm making African crudes the hottest grade among global refiners including the energy-starved China.

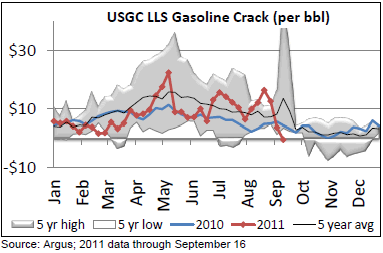

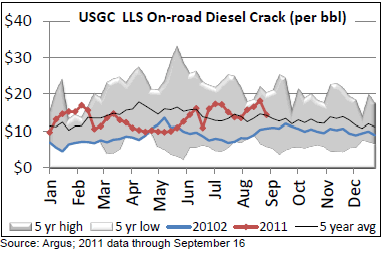

Meanwhile, the Great Recession and high oil prices have basically knocked the highly consumer dependent gasoline (demand as well as margins) into playing second fiddle to the industrial diesel (See 2 Crack Charts).

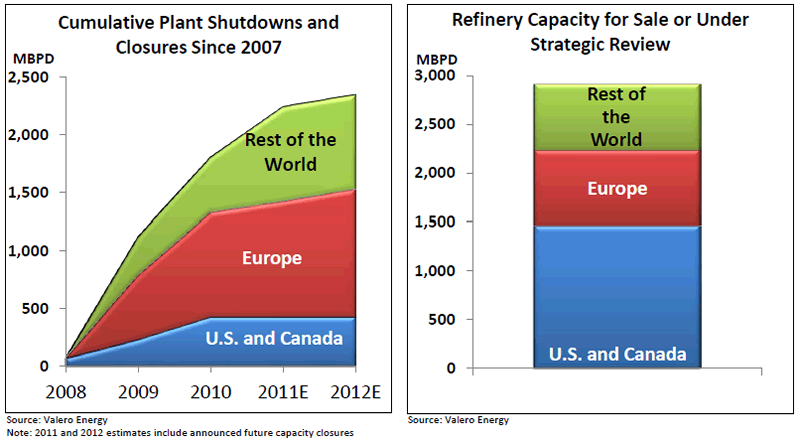

So the surging price of African light sweet crudes has been the kiss of death to U.S. and European refineries that are not equipped to either crank up the higher-margin diesel production, or unable to process the cheaper heavy sour crude into products that are compliant with environmental regulations. That was part of the reason Sunoco closed down two refineries in the Philly area and exited the refining business all together. More refineries in the U.S. as well as on a global basis could also be at risk. ((See Chart Below)

|

|

|

|

|

However, the closure of two Sonoco refineries could mean a loss of about 300,000-4000,000 b/p gasoline and 250,000 to 300,000 b/p of diesel supplies. Amid the new 10-year low gasoline demand trend, the potential loss of gasoline supply would not be a big deal. But diesel is a sector with increasing global demand and with more refinery closures on the horizon, diesel could see significant price spikes in the coming months.

So petroleum products as well as refinery capacity and configuration are increasingly dictating the price direction of crude oil, which also reflects the diminishing relevance of WTI and Brent oil markers. Moreover, despite WTI's steep discount to Brent, U.S. product prices will continue to trend with Brent since only a handful of midwest refiners can get their hands on WTI crude at the low WTI price.

Near term, our prediction in May of $80/bbl WTI oil price by September has materialized, and for now we expect WTI to be range-bound between $80 to $90 a barrel levels for the rest of the year, but it could get sold down to as low as $75 (Saudi's "floor") or as high as $95 (Christmas Rally). Longer term, WTI and Brent spread is not expected to narrow significantly till the pipeline takeaway capacity in Cushing come online in the 2013-2015 time frame.

So U.S. crude oil market could see mostly sideway moves hinging on macroeconomic indicators well into 2012 or 2013, which would suggest limited income upside for the U.S. producers. However, refiners such as Valero and PBF Energy that have made the necessary shift to more distillate production and heavy sour crude processing could see increasing market share and good product prices and margins.

By EconMatters

The theory of quantum mechanics and Einstein’s theory of relativity (E=mc2) have taught us that matter (yin) and energy (yang) are inter-related and interdependent. This interconnectness of all things is the essense of the concept “yin-yang”, and Einstein’s fundamental equation: matter equals energy. The same theories may be applied to equities and commodity markets.

All things within the markets and macro-economy undergo constant change and transformation, and everything is interconnected. That’s why here at Economic Forecasts & Opinions, we focus on identifying the fundamental theories of cause and effect in the markets to help you achieve a great continuum of portfolio yin-yang equilibrium.

That's why, with a team of analysts, we at EconMatters focus on identifying the fundamental theories of cause and effect in the financial markets that matters to your portfolio.

© 2011 Copyright EconMatters - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.