Is Gold Still the Answer for Investors?

Commodities / Gold and Silver 2011 Nov 22, 2011 - 11:07 AM GMTBy: Casey_Research

Bud Conrad, Casey Research writes: Though late to the party as usual, the proverbial man on the street – along with members of mainstream media and Wall Street heavyweights – is finally waking up to the decade-long, 700% increase in the price of gold, joining a growing buzz around the monetary metal. From questions whether gold is in a bubble to predictions that soaring prices are just around the corner, one thing is clear: a new phase of awareness for gold is upon us. How far might it move before these troubling times are over?

Bud Conrad, Casey Research writes: Though late to the party as usual, the proverbial man on the street – along with members of mainstream media and Wall Street heavyweights – is finally waking up to the decade-long, 700% increase in the price of gold, joining a growing buzz around the monetary metal. From questions whether gold is in a bubble to predictions that soaring prices are just around the corner, one thing is clear: a new phase of awareness for gold is upon us. How far might it move before these troubling times are over?

The Big-Picture Economic Environment

Kicking things off, I would like to explore several themes in order to put the current economic situation in context.

For example, continuing weakness in employment and housing indicates that the big slowdown that started in 2007 persists. Actually, the economy never exited the recession but rather – thanks to massive intervention – enjoyed a temporary reprieve that I have called the "Eye of the Storm."

We experienced the first part of the storm from 2007 to 2009, but by late 2009 and into 2010 massive bailouts, stimulus, and deficit spending produced a false-dawn recovery. This recovery was most pronounced in the financial sector where the government transferred toxic private-sector debt – including large amounts held at Fannie and Freddie – onto the government's own balance sheet.

We now are entering the second half of the storm, as it is becoming impossible to ignore the unprecedented and intractable sovereign debt problems sweeping the globe. These problems are especially obvious in the weak countries of Europe where punitive levels of interest rates are pushing weaker members of the eurozone to the brink. As the parts begin to fail, so will the whole.

And the US is not so far behind, with its own historic levels of government debt and deficits running at levels never seen before.

As we at Casey Research have warned of ahead of time, in their attempts to avert a 1929-style depression, governments took on the bubble in toxic private debt, stupidly transferring that burden onto the government (and taxpayers), causing the problem to morph into today's sovereign debt crisis. Simply, with the government debt too big to ever be repaid, we are now beyond the point of no return.

The private debt problem is not resolved, either. That's because much of the bad debt on the books of corporations and financial institutions was hidden through "Extend and Pretend" practices, starting with the elimination of mark-to-market accounting requirements. Much of this debt will eventually be revealed to be in default.

Worse, because sovereignties around the world have caused their finances to deteriorate to such extreme levels, they are now ill prepared, and maybe even unable, to step in yet again to soften the blow of private-debt deleveraging and write-downs. As a consequence, the next part of the storm could be prolonged as companies and banks are dragged down.

Furthermore, due to their poor decision-making to this point in the crisis, the governments themselves are now facing a loss of confidence in their sovereign debt, evidenced by soaring interest rates and the rising cost of credit default swaps (CDS) for the PIIGS.

There is no way to recapitalize the Greek debt, and Finland is right to demand collateral, which it recently has. The contagion will extend to the other PIIGs and to the stronger European countries of Germany and France – they can't also bail out Spain and Italy, which are too big to fail, without destroying confidence in their own economies. Yet absent such a bailout, massive restructuring of weak-country debts held on the books of the banks in the stronger countries will further exacerbate and extend the crisis.

Meanwhile, the European Financial Stability Facility (EFSF) is too small, and the resources to cover all the countries in trouble just aren't there. Economists now understand that the PIIGS are well past the point of no return with 130% or so of debt to GDP. The European Central Bank (ECB) will be expanded, like other central banks, to print more euros, but still the system is going to face more debt problems.

The ratio of debt to GDP in Europe, the US, and elsewhere (which is projected to only increase from here) will lead to the sort of problems historically associated with Latin American banana republics, collapsed communist states, and certain countries in Africa. While this is not being adequately discussed in the mainstream, the debt of the supposedly advanced countries is projected to explode beyond the levels that are already tormenting the PIIGS. Put another way, in the decade just ahead, I expect the advanced countries to undergo the same pain we are already seeing in the weak countries.

Supporting that contention, a new paper by the Bank for International Settlements (BIS) points out that when government debt approaches 80% to 100% of GDP, there is a weakening in the economy. Greece and the euro system aren't just facing an economic weakening but a breakdown of the financial system.

Importantly, the debt-to-GDP ratio of the United States is now (conservatively) at 95%, and demands from a tidal wave of retiring baby boomers will make the deficits far worse. Remarkably, annual deficits of a trillion dollars or more over the coming decade are projected. The US debt-to-GDP ratio will break above 100% in two years or less, and debt could double in the next decade if interest rates rise in concert with a widespread loss of confidence in the government's ability to manage its fiscal and monetary affairs.

The next logical step in this sovereign debt crisis is for us to see further signs of a loss of confidence in the currency. Such a currency crisis is usually measured by rising inflation that, in turn, leads to higher interest rates, which make the crisis worse. That’s because a vicious debt "death" cycle begins to form, with interest on the debt begetting ever-worsening deficits begetting ever higher interest rates that, in time, leave the country unable to even pay the interest on its debt, let alone pay down the debt itself.

Sounds dramatic, I know – but that is what is happening in Greece. The major difference from historical events of a similar nature is that this time, it is not just the smaller, less developed countries – the so-called banana republics – that are in the throes of a financial collapse but most of the world's advanced economies. This is certain to end badly.

In the short term, the central banks will print up money for their governments and bankers, but in the long run, the loss of confidence will become so great that currencies self-destruct. As the problems extend around the globe, currencies and bond markets will be wiped out together.

In time, new currencies will have to be issued, almost certainly with some form of link to gold and other commodities. To survive what's coming, you need to understand the process and try to gauge how fast it may unfold. To shed further light on those issues, in the following I provide data on how serious the situation is and conclude with my predictions for the price of gold.

Central Banks Can Print Paper, But They Can't Print Gold

Gold is the only real money. In contrast, the power of central bankers to create fiat money out of thin air has distorted our financial systems beyond anything imagined in the early days of slips of paper issued for gold held at the local goldsmith's.

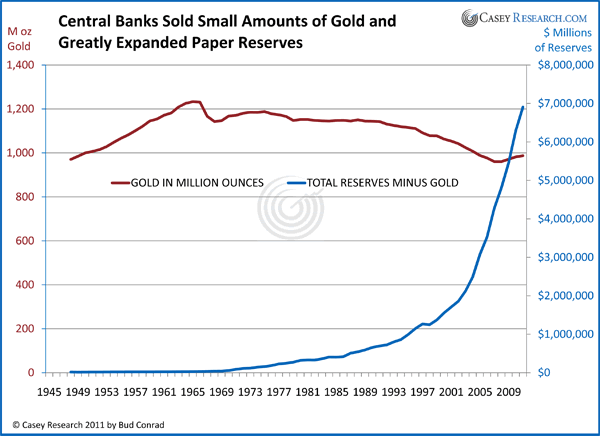

To get a sense of the distortion, we'll start by looking at the difference between the quantity of gold held by central banks and the amount of paper money they have issued. As you can see in the chart below, the amount of gold held has been surprisingly stable. But the blue line, a close reflection of the narrow definition of money that has been created globally, shows that the quantity of all forms of financial assets has grown dramatically.

The clear point of this chart is that the nominal quantity of the paper money in circulation has been growing much faster than the gold that formerly underpinned that currency and may be called upon to do so again before this is over. Regardless, as the power of money creation greatly benefits the money printers, we expect profligate money spending and creation to continue apace.

Importantly, central banks are no longer selling off their gold but rather are increasing their holdings. You can see that shift in the small upturn in the red line at the right of the chart. Central banks halting gold sales and becoming net buyers of gold decreases supply and increases demand, leading to higher gold prices.

As a related anecdote, Venezuela's President Chavez recently recalled gold reserves not currently held in Caracas, exciting the gold bulls with the thought that the withdrawal of some 150-200 tonnes of gold from the Bank of England and bullion banks will force a squeeze on traditional stockpiles of gold. Chavez is further proposing to nationalize Venezuela's gold mines. His many faults aside, I think Chavez understands the situation perfectly and is using his dictatorial powers to move back towards gold faster than slower-moving nation-state competitors.

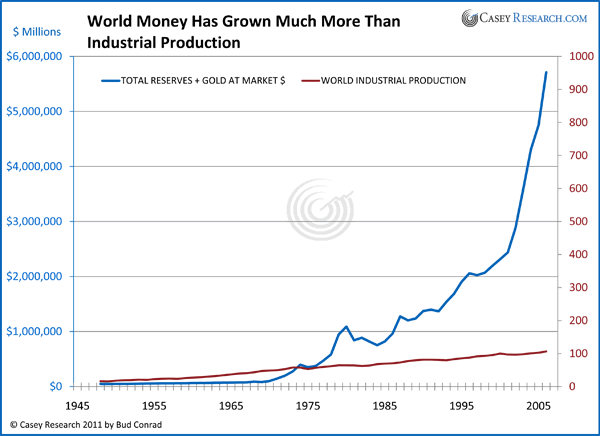

Another way to measure the debasement of the world's currencies is to compare global industrial production to the global quantity of currency in circulation. As you can see in the next chart, industrial production has only moderately increased over time. Since Nixon closed the gold window in 1971, the quantity of currency in which that output is priced has grown exponentially. Is it any wonder that the nominal price of the average car has soared from $3,542 in 1971 to almost $30,000 today?

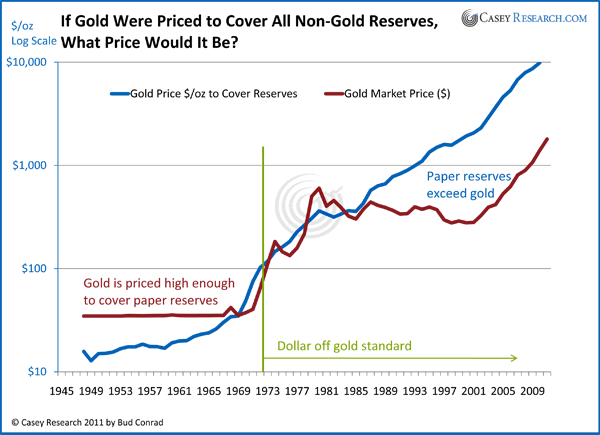

Of course, the price of gold as measured in these currencies has increased over time. At least in theory, the ratio of the dollar value of gold to the dollar value of all currencies in the world, shown in the next chart, should give us a basic measure as to whether gold is overpriced.

As you can see, gold would need to trade closer to $10,000 per ounce to cover all the paper issued over the period. This confirms, in my mind, that although gold is rising rapidly towards $2,000 an ounce, gold investors need not fear that it is in a bubble or that its upward momentum is nearing an end.

Federal Government Deficits Are "Beyond the Point of No Return"

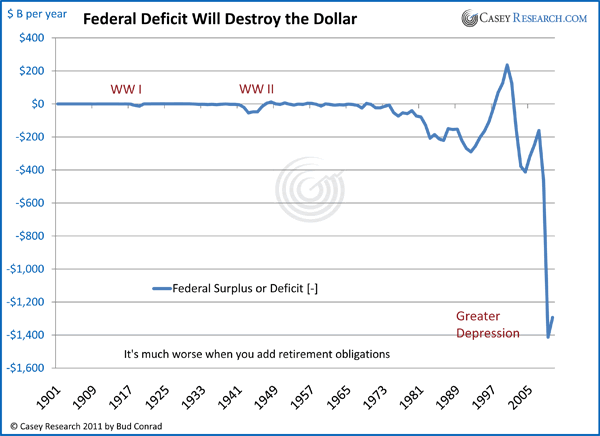

The government's debt has accumulated to an amount so enormous that it won't ever be paid back. The annual deficit is unmanageable as Democrats cry for more spending and Republicans want to continue tax cuts. The chart below shows that the current deficit is at a completely new level, even in comparison to the two world wars.

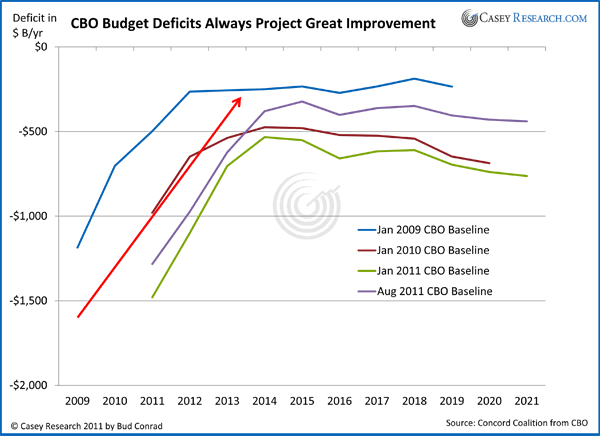

Looking at the future of government deficits, the Congressional Budget Office (CBO) starts with a baseline projection of the expected government budget deficit based solely on laws already enacted. In other words, the baseline doesn't account for new laws, which invariably expand spending. Not surprisingly, as you can see in the chart here of previously published baseline forecasts, the CBO's deficit projections are always optimistic about the expected deficit.

For a look at a more reasonable assessment of the impact of yet-to-be-enacted legislation on future deficits, we turn to a set of data assembled by the Concord Coalition that show much higher deficits going forward. Here are the modifications that underpin what they call a "plausible" scenario:

The CBO baseline is adjusted to assume appropriations increase at the same rate as the economy (GDP growth). This increase is closer to the historical average rate of increase. They assume that supplemental appropriations do not continue indefinitely. For the wars in Iraq and Afghanistan, troop levels slowly decrease to about one-third of their level at the time of the estimate. They assume that Medicare physician payment cuts (under the Sustainable Growth Rate (SGR) are postponed, as they have been for the last several years.

The major tax cuts are assumed to extend beyond 2010. One-year patches to the Alternative Minimum Tax are enacted, holding the level of taxpayers hit by the tax roughly constant throughout the baseline period. A calculation for the increased debt service (interest payments) that these policies cause is added.

As bad as are the resulting deficit forecasts, however, the assumptions behind even these "plausible" scenarios are so far off from my expectations that I am confident they err on the side of being much too conservative. For example, in the Concord Coalition's assumptions, the Consumer Price Index never rises above 2.3% – all the way out to 2021 – and the unemployment rate drops to 5.4% by 2016. Along the same optimistic lines, 10-year Treasury interest rates never climb above 5.3% and GDP will reach 5% in real terms by 2015.

While no one can see the future, all of my work leads me to expect much higher inflation, much higher interest rates and a much slower growth of GDP over the time period.

And I can think of worse scenarios, like a recession that cuts tax revenue and higher interest rates that cost more to service the government's debt. The expansion of war to Libya and Pakistan, and a comment from Obama that the Syrian president "must go" indicate that military spending will continue to be high.

My point is that even under the CBO's Pollyanna projections, US deficits ensure that total debt continues to rise into increasingly dangerous territory – but actual deficits are likely to be much worse than those projections, and quite possibly devastatingly so. Deficits debase the dollar and are bullish for gold.

The economic situation in the US is declining rapidly, with zero net jobs created for August and the numbers from the previous month adjusted to show a further loss of 58,000. And even those dismal numbers understate things: embedded in the latest report were 81,000 jobs added from a flawed birth/death model that estimates new jobs from small business.

Elsewhere in the economy, housing prices remain weak and consumer confidence has turned down sharply.

The likelihood of continued recession adds to the deficits by decreasing taxes and increasing demands for government spending on unemployment and stimulus.

Adding it all together, it becomes clear that the trajectory for government deficits, and therefore more debt, is to continue to go up, and dangerously so.

The Fed Papered over the Private Debt Crisis But Is Creating Future Inflation

The Federal Reserve jumped into the credit crisis with both feet, tripling its balance sheet since 2008. It did this by creating deposits at the Federal Reserve out of thin air to buy mortgage-backed securities and Treasuries to the tune of $1.6 trillion. Historically, when the Fed paid no interest on deposits, banks would draw down these new deposits to lend out to borrowers in order to make a return, expanding the money supply in the process. By expanding credit, this process also can help prime the economy. That hasn't happened this time around, and credit has not grown in the private sector.

The deposits at the Fed are obvious in the chart below. Banks receive 0.25% interest on the deposits, which is better than they can currently earn with short-term loans and T-bills, so the Fed has $1.6 trillion of deposits it never had before.

It is helpful to understand the details of what we call printing money and the physical paper money in circulation. The chart above shows that the outstanding currency in circulation (blue area of the chart) is growing at a relatively slow rate. The amount of paper money is not really decided on by the Fed; it is the result of the preference of the population to carry cash as opposed to having deposits at their bank. When people withdraw cash, as they do around the Christmas holidays, for example, the demand for paper dollars increases at the commercial banks. A commercial bank can send a Brinks truck to the Fed, ask for more dollar bills and have the Fed decrease its account at the central bank. In other words, the process is not driven by the Fed but the consumers and the banks.

If the Fed wants inflation, stopping the interest-rate subsidy of paying interest on deposits to the banks would be a good place to start. Then banks would look for places to loan money and inject it into the system.

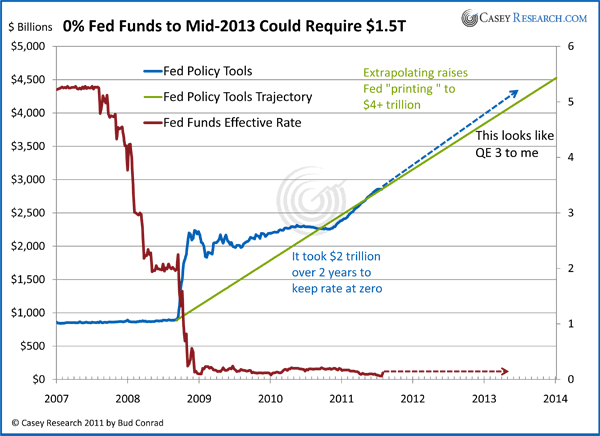

The Fed surprised the market by extending its policy of a 0 to 0.25% fed funds rate to mid-2013.

Most people reading that the Federal Reserve plans to maintain current low interest rates out to 2013 probably shrugged and went about their business. But I think it's important to understand that the only way the Fed will be able to meet its low interest rate pledge is to buy Treasuries with newly created money – essentially printing money to purchase the government's unending supply of Treasuries. Quantitative easing, anyone?

The big question is whether the policy will have a sizeable effect on markets. The chart below shows the historical jump in the Fed's combined policy tools that were used to lower rates and bail out financial institutions through a variety of programs. These include the big purchase of mortgage-backed securities (MBS) called QE1 and the large purchase of Treasuries called QE2.

The point of the extrapolation in the chart is to guesstimate how much more money the Fed might need to create to keep the rate extremely low for another two years. By connecting a straight line from the start of the unusual policy tool expansions in late 2008 to today's number and then extending it to 2013, we can estimate that the policy might require about $1.5 trillion in order to keep the rate low.

The Fed doesn't calculate the amount of money that might be required and probably doesn't know for sure. They just keep buying on the open market until the rate target is reached. If there were a loss of confidence in the dollar, the amount of the purchases required could become very large – and in the extreme, printing more money contributes to that loss of confidence, which in turn causes runaway inflation. We are not there yet. But this kind of open-ended promise is a dangerous precedent because we can't be sure of the ultimate cost of the commitment. And make no mistake, it is an astounding commitment. At the meeting where the decision was made, even more aggressive operations to expand the money supply were discussed.

The long-term direction of the Fed is not in doubt: they are debasing the dollar.

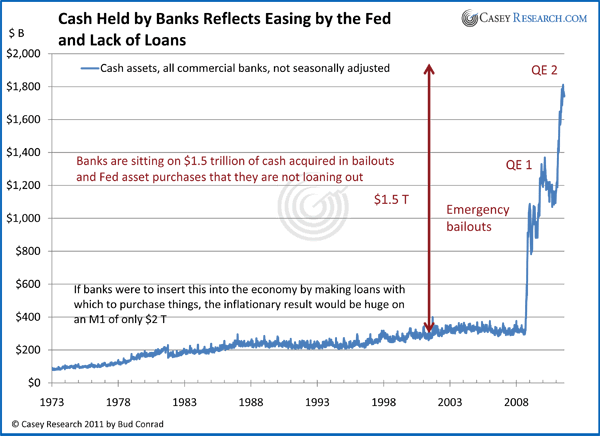

In the next chart, we look at the mirror image of the commercial bank deposits at the Fed – the cash being held on the balance sheet of the banks. As you can see, this confirms that instead of making loans, they are holding cash, mostly in the form of these Fed deposits. The effect is that the Fed policies have had much less effect on the economy outside of the banking system than would usually be the case, given their extreme bailouts and money "printing." Inflation has been contained to commodities, and interest rates have remained at record lows.

The fact that this money sits mostly as cash deposits at the Fed is why the QE programs have had little effect on the economy. Rather, it is clear that the Fed’s priority has mostly been to provide support for the banking system. Though going forward, these deposits – almost $2 trillion – could be easily loaned into the system, and the result could be very inflationary.

Europe Is Turning to the US Dollar and to Gold for Safety

The loss of confidence in a country is most obvious when lenders demand high interest rates to loan money to a government by buying their bonds. With the yield on two-year Greek government-issued notes now at 45% and one year being quoted at 70%, the situation in Greece has gone beyond the level where the government can operate.

The risk in Europe is rapidly becoming more acute as the promised bailouts aren’t happening and the population of Germany is turning against a further expansion of the European Financial Stability Facility (EFSF) that was set up in an attempt to calm the situation. A series of routs for German Chancellor Angela Merkel’s political party in recent local elections reflects the public discontent with further bailouts at the German taxpayer’s expense.

The Wall Street Journal reported on September 5: "The suspension of the talks in Athens between the government and a group of officials representing the providers of Greece's bailout cash came, officials said, amid a dispute about how to address new gaps opening up in the government budget deficit."

In September, the Bundestag (the German parliament) is expected to decide on a package that empowers the EFSF to buy bonds preemptively and recapitalize banks. While the bill is likely to pass, the furious debate leaves no doubt that Germany will resist moves to boost the EFSF's firepower yet further. Some say the fund needs €2 trillion to stop the crisis from engulfing Spain and Italy.

In short, the very fate of the European monetary union is hanging by a thread. And, as noted earlier, the banking crisis will be more difficult to handle this time – the governments are in much worse shape because they took on so much additional debt in bailing out the banks to this point. So this time a private banking crisis could become much worse, leaving the central banks as the buyers of only resort for government debt. Should that occur – though we at Casey Research believe it's a matter of when, not if – it will be the starting gun for the end of the fiat currency systems.

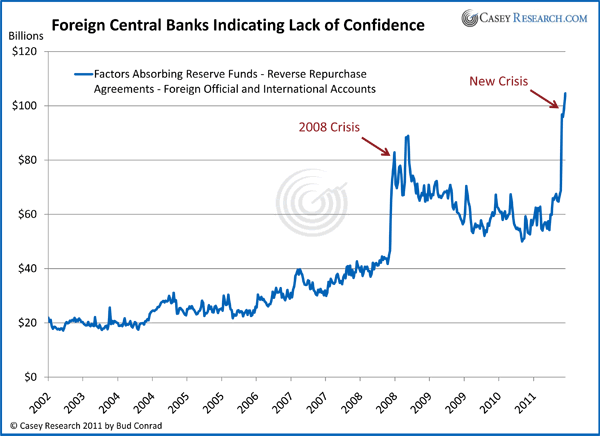

In the meantime, the next chart shows clear signs that foreign central banks are beginning to run scared – indicated by a soaring willingness to park money with the Fed. They were big users of reverse repos when the Lehman collapse signaled the onslaught of the credit crisis, and their holdings just spiked again in the face of European weakness.

The interpretation is that foreign central banks are finding the safety and returns in the US more attractive than their own banks. Regardless of the causes, this measure reflects banking system fear and is indicating more trouble ahead.

The result of a loss of confidence in Europe is a flight to safety, i.e., to the Swiss franc, the dollar, and to gold. The dollar has been less coveted because of its own flaws.

US Money Growth Is Picking Up

Recently, the money supply has taken a jump with Fed liquidity, and commodity prices have risen.

We need to consider that international forces may be a factor in driving US money growth. A European loss of confidence is decreasing the attractiveness of keeping deposits in European banks and may be behind the increase in deposits at US banks. Cash assets at foreign institutions in the US have jumped from $400 billion to $800 billion since the beginning of 2011. It is certainly not a booming US economy driving the US money supply; this increase in foreign deposits is suggesting the money supply increase is due in some part to a flight to safety from worried Europeans.

Back to Gold

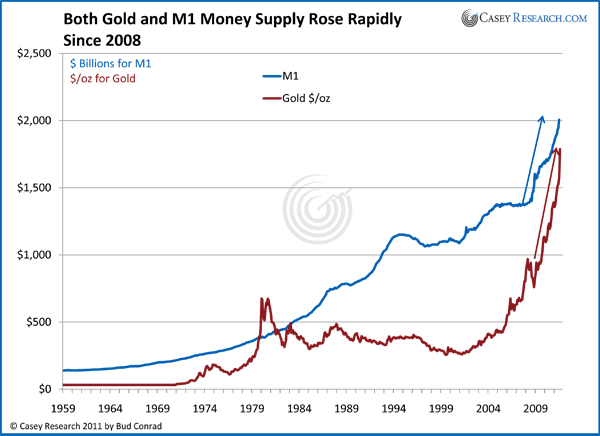

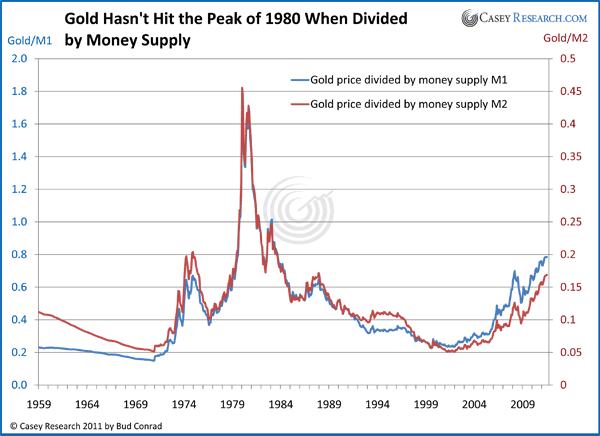

As we are trying to revisit our base case for gold going forward, let’s return to the ultimate safe harbor. The next chart illustrates, through the ratio of gold to the increase in M1 and M2, that gold is still well below its peak of 1980.

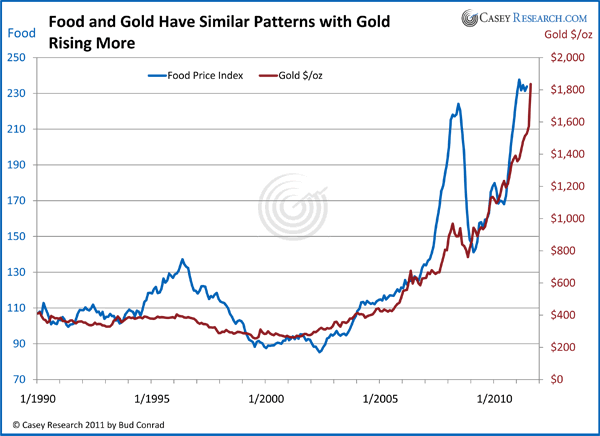

In the chart below, I look at one slice of the analysis that shows that money printing and fiscal deficits have driven commodity prices higher. As you can see, the index of world food prices has risen 40% over the last year. It was rising fast before the credit crisis, dropped during the worst of the crisis and is rising again, along with gold.

As should be clear, deflation is not part of the story for food or gold. The path forward points to higher prices, especially if the banks return to their core business of lending. The right way to look at the speculative fever is not to look at the gold market but to what the government is doing to the currency. There is a lot more debasement to come – which means a lot more price rise ahead.

Gold Is Not Record High in Inflation-Adjusted Terms

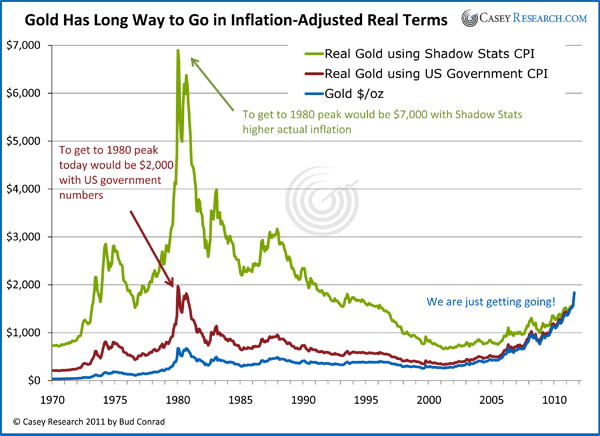

Gold is just bouncing off $1,900/oz highs, a record in nominal terms. The blue line shows the average monthly price of gold. As you can see, the previous peak was in 1980 at $675 per ounce monthly average, which included an intraday high of $850. But the dollars of 1980 would purchase more than the dollars of today. To estimate the number of today's dollars that would be required in 1980, we can use the inflation index of the Consumer Price Index (CPI). The red line indicates that even by this manipulated government measure, the 1980 price of gold in today's dollars would be $2,000. We are getting close but have not yet reached the old peak.

However, as you are probably aware, the government's CPI numbers seriously underreport the amount of inflation. The government has made a number of significant adjustments to its CPI calculations, all of which cause it to be understated compared to the CPI as constituted in 1980. Thus, for example, today's CPI uses rental equivalent for housing costs; inflation is revised downward based on new improvements in products; and even the basket of commodities used in the calculation is changed when an item becomes expensive.

Another view of inflation comes from John Williams of Shadow Stats, who removes the adjustments and concludes that inflation is much higher than the CPI admits to. Applying his inflation numbers suggests that the 1980 gold price peak would have been $7,000 in today's dollars, as indicated in the green line. The visual conclusion is that in inflation-adjusted terms, gold still has a ways to run.

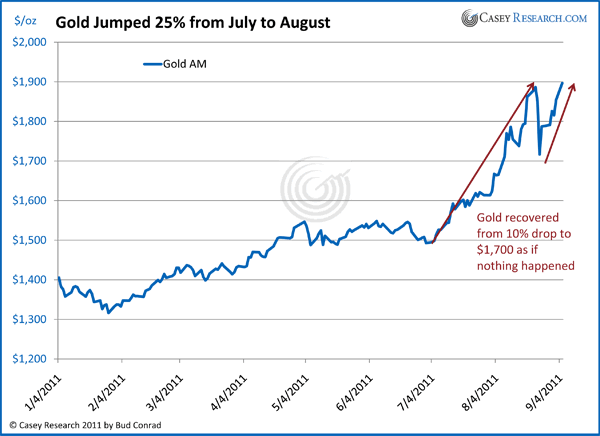

A one-year chart of gold shows it already exceeding my prediction of rising to $1,800 by the end of the year. The subsequent drop of 10% from $1,900 to $1700 was surprising, but not enough to indicate a change in direction because gold had risen so much just since July. The drop may have been inspired by exchange margin hikes, which hurt momentum and highly leveraged traders, but margins do not change fundamentals. The margin hike of 27 % in August was in line with the preceding price rise, and the subsequent price recovery confirms that the effect was short lived.

Gold Is Entering a New Phase of Public Acceptance

The fundamentals of government deficits and the Fed's loose monetary policies have, if anything, become worse. We at Casey Research have been pounding the table for years that gold is a must-have, long-term hold for protection against a demise of the dollar. The 700% increase over the decade – running laps around the performance of Warren Buffett's much-touted Berkshire-Hathaway fund – has confirmed that we were right.

Looking at the landscape, I am observing changes in the attitude of the media and others about the direction for gold. This market has been mostly under the radar of mainstream media; despite its unparalleled performance, gold was not considered a mainstream alternative for investment dollars. You could think of the past decade as a "stealth" bull run.

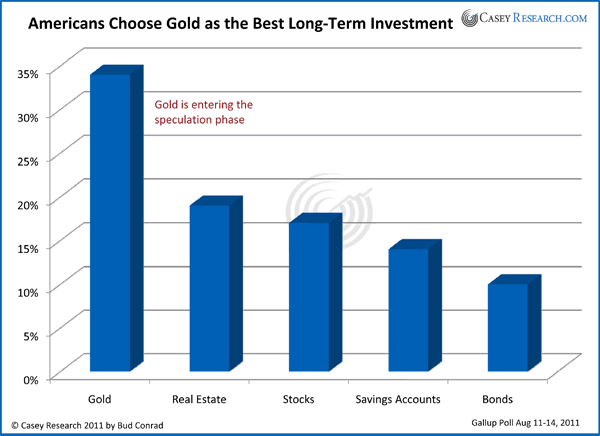

We seem to be entering a new phase where a much wider population of investors is now aware of what's been happening in gold. Evidence abounds, including a recent Gallup poll that, for the first time, included gold as an option to its question of what is the best long-term investment, and it was the most popular.

In addition, CNBC is airing an 11-part report called The Golden Age of Gold, and Fidelity brokerage now offers physical gold and silver, something unheard of for a firm that thrives on mutual funds.

These and many others are mainstream sources that would rarely discuss gold in years past, and if they did discuss it, it was derisively. Their arrival on the scene raises the question if we are at the point of euphoria where there is too much interest in gold. Yes, we could have a pullback from this impressive rise again to $1,900, but I don't think we are close to the end of the golden bull.

Many people I know keep asking the question whether it is too late to join the game. I think a better interpretation is that we are moving from the stage of stealth increase in price toward the final stage of mainstream involvement that will bring wider participation and even higher prices. Before this is over, we will see a true mania in gold, and prices will soar.

Which begs the question, by how much?

The Long-Term Case for Gold

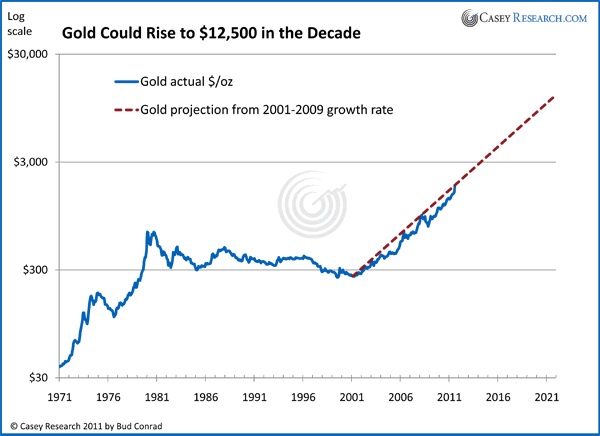

Given that the stars are lining up for gold to continue on the path of resuming its important role as a monetary metal – and given the almost certain collapse in the fiat currency systems that is heralding a return to that role – it is entirely possible that gold could rise at the same rate in the next decade as it has in the last decade.

Therefore, using the same growth rate and extending the gold price as a straight line on a semi-log curve, we can come to the resulting price at the end of the decade. Under this projection, by 2021 the dotted line rises from today's $1,825 to $12,500. (More detail on the method is contained in my book Profiting from the World's Economic Crisis in Chapter 15 on gold.)

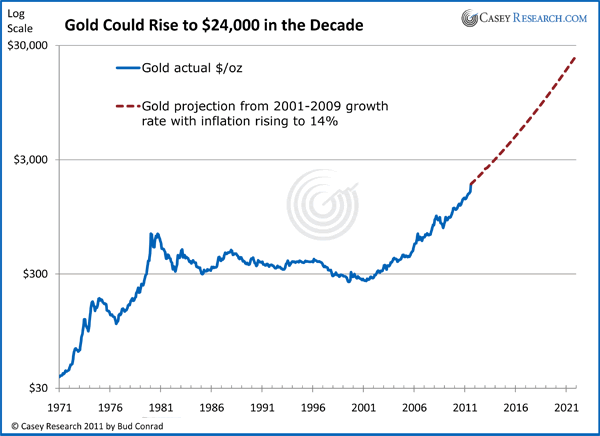

The increases due to price inflation and the flight from fiat currencies to gold are combined in the above chart. I think price inflation has been relatively low in the last decade but will certainly rise going forward.

To reflect my forecast for higher price inflation, I separated the two components by calculating the rise in the real price of gold since 2001 and projecting that forward. I then projected a rise in CPI that eventually matches the rise in the inflationary 1970s, when it ultimately reached 14%, and then applied that data to the real price of gold, for a combined projection that is much higher. You’ll see it below as the dotted line with a small curve upward for the increasing inflation that I expect over the decade. The result: gold could reach $24,000 by 2021, a decade from now.

This fits with my scenario of escalating loss of confidence in the dollar and the preference for gold that will be the fallout from continuing huge government deficits.

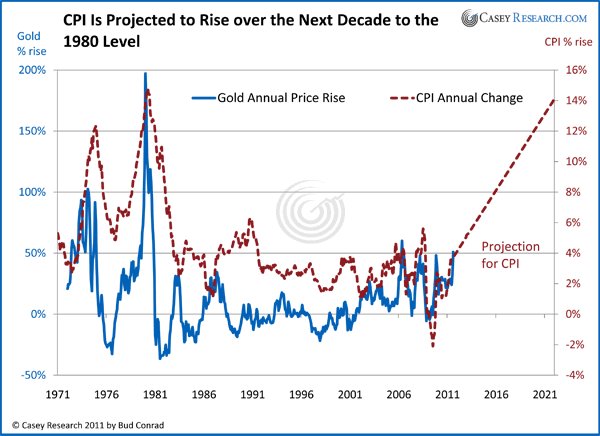

The chart below establishes the case for the CPI to reach the same 14% level that it peaked at in 1980. It shows both the CPI and gold annual percent changes. The correlation is obvious in the 1970s. The projection for a gradual rising CPI used in the above chart is specified in the rising line after 2011:

This confirms the historical sensibility for a 14% CPI for the more complex two-part analysis, but it is not the only method for calculating a scenario for $24,000 gold.

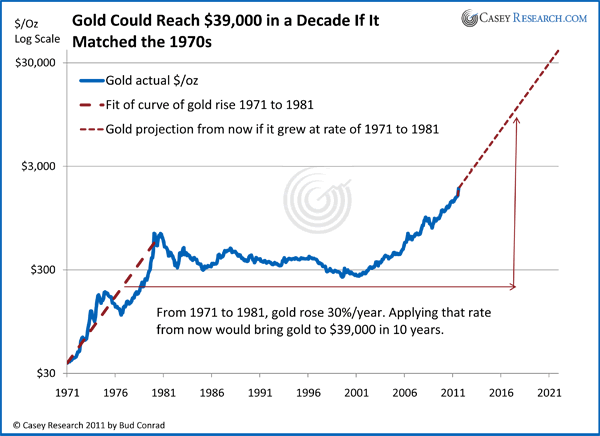

If gold rose at the rate it did in the 1970s, it would rise well above $30,000 over the coming decade. A visual of that projection is shown in the graph below.

The dashed line on the left shows the fit to the rise from 1971 to 1981 at a bit over 30% per year. Applying that rate of increase to the current price for the decade ahead, as in the dashed line on the right side of the graph, we get to a price of $39,000.

Of course, reality is always more complex than a straight line on a semi-log graph; for example, in the 1970s there was a big pullback in the middle when the first oil shock slowed the economy and disrupted the trend. Also, the 1970s were playing catch-up for gold being fixed to the dollar ever since Roosevelt's hike of the price to $32 in 1934. The point is not to conclude that this is a prediction made with great precision but rather that gold's amazing price acceleration over the past ten years has historical precedent, and much greater gains are certainly not out of the question.

Ultimately, the probability that we will see the sort of projections discussed here will depend on whether the loss of confidence in the dollar going forward will match or even exceed what happened then. Given that things are much worse today than they were back then, I think that is an entirely reasonable scenario, which makes the astounding headline number a very real possibility.

The models are summarized in the following table indicating the gold $/oz expected:

| Dec 2011 | Dec 2012 | Dec 2021 | |

| Simple 2001 to 2011 Growth Extended | $1,950 |

$2,400 |

$12,500 |

| Real Gold 2001 to 2011 Growth + CPI Rise to 14% | $1,960 |

$2,500 |

$24,200 |

| 1971 to 1981 Growth Applied to Next Decade | $2,030 |

$2,800 |

$39,200 |

I consider the rising CPI model, highlighted above as the middle case, to be the more likely one, because I expect continued loss of confidence in the dollar over the decade from the spending patterns, out-of-control deficits and Fed actions.

The seasonal aspect of gold investing gives a strong upward bias for the fall season that is not included in these models, so I think a $2,000 prediction for the end of 2011 is a sensible uplift to the short-term prediction.

My projection of $2,500/oz for 2012 represents a 25% increase next year, just modestly above the rises of recent years. In other words, for these predictions to come to pass it does not require an extreme event or major new disruption. The extension for 10 years could easily be much less, or much higher, as the scenarios indicate.

Calibrating the Prediction

I predicted $1,800/oz for the end of 2011 at the beginning of the year. (We started the year at $1,421, so this was an increase of 27%.) For reference, the table below summarizes the view from a variety of well-known sources, which were all lower. My $1,800 was the outlier on the high side.

| Gold Price Predictions from Last Year | |

| Gold 2011 | |

| Morgan Stanley | $1,315 |

| Goldman Sachs | $1,690 |

| Society General | $1,485 |

| BNP Parabas | $1,500 |

| Barclays (Q3) | $1,490 |

| Bank of America | $1,425 |

| (Source Reuters) | |

| Average | $1,484 |

| Bud Conrad | $1,800 |

Predictions help us understand the future, even though they are necessarily fraught with speculation and error. Be cautioned that nobody knows the future precisely, but here I have divulged my methods so you can see how I came to these estimates. Use them with your own judgment.

My conclusion is that we face very serious financial problems ahead. The situation is far more out of control than any previously faced in the United States. I see no way to ever pay off the government debt, and Congress has shown itself incompetent in all things, but especially in applying the brakes to soaring deficits.

Elsewhere, the Federal Reserve has already indicated that it plans to abandon the dollar in favor of printing new money to support the economy and the banks. The combination of both doesn't bode well for the survival of the dollar.

My fear is that the situation will turn out to be much worse than the historically projected trends referenced above, with the price of gold escalating well beyond the numbers shown. So as we go forward, you can use these benchmarks to see whether we remain on a trajectory to significantly higher gold prices.

Of course, if confidence in the fiat currencies erodes to the point approaching failure, the value of gold denominated in worthless paper approaches incalculable numbers – Zimbabwe-like numbers that would be meaningless.

Summed up, until there are fundamental changes in government fiscal and monetary policies – and a recognition that the sovereign debt is unpayable and therefore needs to be restructured – there is no reason to fear gold pullbacks and every reason to expect even more positive returns in the gold mining stocks that are still catching up to the rapid gold rise.

Even higher prices than mentioned here are possible from the flight to safety out of the euro, the seasonal rise into the new year, and the accelerating action of gold from a shift in sentiment of the investment public to a relatively small market. Gold is by far the best "answer," and now is still the best time to invest.

[Historically, gold has always been a great inflation and crisis hedge, and today again inflation is eating away at the meager gains many mainstream investors make. Did you know that if your portfolio grew by even 3% last year, you may have actually LOST money? More in this report.]

© 2011 Copyright Casey Research - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.