Real Interest Rates, The Key To Reading The Gold Bull

Commodities / Gold and Silver 2012 Apr 09, 2012 - 03:38 PM GMTBy: Submissions

Mark Motive writes: After peaking at $1,780 in late February, gold dropped over $100 in March, finishing the month at $1,662.50.

Mark Motive writes: After peaking at $1,780 in late February, gold dropped over $100 in March, finishing the month at $1,662.50.

Whenever there is a big move up or down, we all naturally seek confirmation and reassurance of our investment strategy, which is why investors must use objective measures to evaluate and re-evaluate their positions.

As someone who is invested in gold bullion, I enjoy speaking with like-minded people. Many agree that the United States' massive budget deficits and global monetary inflation support the gold bull market. I don't see this changing in the near future. Still, sentiment is not enough upon which to rely - I need a yardstick.

For me, that yardstick is US real interest rates. Real interest rates represent the inflation-adjusted interest rate on 'risk-free' assets, such as US Treasuries. In other words, if a Treasury bond is held to maturity, the real interest rate shows if the bond investor is losing money due to inflation even if the bond posts a profit.

Calculating Real Interest Rates

There are many variations of this measure, but I use 1-year, constant-maturity US Treasury Bill yields as my starting rate and 1-year US food inflation as the adjustment factor.

Using food as a proxy for inflation is insightful for a few reasons: 1) it's a good that everyone buys, so it has an impact on most everybody, 2) agricultural commodity price increases are quickly incorporated into consumer food prices, so it's quick to mirror real world inflation, and 3) the food industry is well-developed, so food prices already incorporate savings gained by large-scale production.

By no means is my methodology the only way to calculate real interest rates. Some investors choose to use longer-dated Treasuries and various other measures of inflation, such as the Consumer Price Index (CPI). However, I don't use the CPI because I believe it has been heavily manipulated over the years and may not be a fair representation of inflation. For example, the goods and weightings used to calculate CPI have been revised over time based on changing quality and the availability of substitutes. This means that CPI is more of a cost of living measure than a pure price measure.

That said, regardless of the methodology used, most calculations of real interest rates will vary only in magnitude, not direction.

Why Use Real Interest Rates?

Let's look at 2011 to illustrate how negative real interest rates affect investors. A 1-year US Treasury Bill purchased on the first trading day of 2011 would have earned about 0.29% if held until maturity. Meanwhile, during 2011, US food prices rose a whopping 4.4%. Using my methodology, someone who placed his savings in a 1-year US Treasury Bill at the beginning of 2011 would have lost 4.11% in purchasing power over the course of the year, despite investing in "safe" US government bonds. This is very bullish for gold.

Negative real interest rates are a direct result of the Federal Reserve's official policy to maintain favorable government borrowing costs: print money to buy Treasuries at artificially low yields and create inflation to allow the Treasury to pay back the debt in cheaper dollars. This is default by stealth and a direct transfer of wealth from savers to borrowers. The common term for this phenomenon is 'financial repression'.

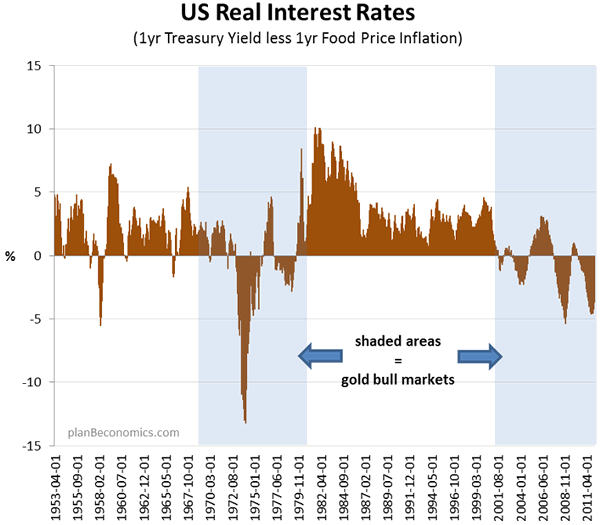

The chart below shows the US real interest rate over the past 60 years. The shaded areas are periods in which gold experienced a bull market. As you can see, these periods occurred when real interest rates were low or negative and highly volatile. By contrast, the gold bear market of the 1980s and 1990s occurred when real interest rates were higher, positive, and relatively steady. (Prior to the late 1960s, the gold price was still heavily influenced by the Bretton Woods system and gold prices were fairly flat.)

Source: Plan B Economics

While this does not prove the causality of the relationship, it makes sense intuitively. Gold performs well during periods of negative real interest rates because there are fewer alternatives for investors seeking to preserve capital and purchasing power. If a US Treasury bond provides a negative after-inflation yield, can it still be considered a safe haven? Most sophisticated investors would answer "no," because it's a money-loser right out of the gate (and has a lot of downside risk if nominal yields rise).

Additionally, real interest rate volatility implies that investors are uncertain about Treasury prices and future inflation. This could be caused by financial conditions that are strained beyond the realm of the normal business cycle, such as an unresolved global banking crisis or unsustainable debt. We're facing both of these crises today.

The Big Picture

Even during periods of negative real interest rates, there are times when US Treasuries perform well in comparison to hard assets - usually during short-term periods of financial stress when investors are scrambling. However, under normal conditions, a US Treasury bond can be expected to provide a total return that is close to its coupon rate, which today is below the rate of inflation.

Any investor using real interest rates to gauge the gold bull market must look through short-term fluctuations to see the secular trend. And today - while the US is overloaded with debt and the Federal Reserve is printing money without hesitation - the secular trend of negative real interest rates remains intact.

What does this mean for the current gold bull market? One day, the gold bull market will end, but given the current outlook for continued negative and volatile real interest rates, but the evidence suggests that day is well in the future.

Mark Motiveis the pen name of a respected business journalist. He is the author and editor of Plan B Economics, a source for insights into finance and economics. Follow him on Twitter for free eBooks, documentaries and more: ;@planbeconomics

This article first appeared in the April 2012 edition of Peter Schiff's Gold Report, a monthly newsletter featuring original contributions from Peter Schiff, Casey Research, and other leading experts in the gold market. Click here for your free subscription.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.