Spain €100 billion Bank Bailout Necessary But Not Sufficient, Italy Federalism, Debt Traps and Competition

Interest-Rates / Eurozone Debt Crisis Jun 12, 2012 - 07:03 AM GMTBy: John_Mauldin

We woke up this weekend to a €100 billion "rescue" of Spanish banks, and the initial reaction of the market was relief. But did we not just see this movie, but with Greek subtitles rather than Spanish? Was this another of those "necessary but not sufficient" plot lines that Europe is so good at? Kick the can down the road and hope for a happy ending?

We woke up this weekend to a €100 billion "rescue" of Spanish banks, and the initial reaction of the market was relief. But did we not just see this movie, but with Greek subtitles rather than Spanish? Was this another of those "necessary but not sufficient" plot lines that Europe is so good at? Kick the can down the road and hope for a happy ending?

Pardon my skepticism, but I see numerous problems. In the first place, €100 billion will not be enough. While the current estimates are closer to €40 billion (if you ask the Spaniards), JP Morgan estimates it will be more like €350 billion. Others estimate more or less, but €100 billion is decidedly optimistic. Even the Spanish authorities are acknowledging that there is another 35% downside for the housing market, which is the main source of the losses. It appears that has NOT been included in the guesstimates.

Secondly, this saddles Spain with yet more debt, which will force the rest of already-sold Spanish debt into a subordinated position (more on that from Louis Gave, below). It does not address the problem that Spain is running an almost 10% of GDP deficit and will need to access the markets for very large sums in the near future. For all intents and purposes, they have been shut out of the bond market, which is why they needed a "rescue."

Third, it does not address one of the fundamental problems, which is the subject of this week's Outside the Box from Charles Gave: it does not help solve the trade imbalance between Germany and the periphery nations.

Germany has two very bad choices. It can finance the multiple trillions of euros of debt of Spain and Italy (and France), converting it into eurozone debt, while giving up its own fiscal sovereignty and allowing a eurozone-wide fiscal union and taxing authority; or the Germans can spend trillions of euros allowing the eurozone to break up, either by exiting themselves or allowing the southern countries to exit.

The market is not going to finance Spain, Italy, et al. in the short term (i.e., this year). That means the ECB will have to print money or some European entity will need to have a basically unlimited blank check at the ECB, if those countries are not allowed to default on their debt. Someone, or some group of someones, is going to have to write a rather large check. The question is whether it costs more to stay or to go. Germany leaving the euro would not be good for German exports, which are 40% of their economy.

Finally, it is not clear exactly how this bailout (let's call a spade a spade) is going to come about. There will have to be, I assume, agreement from the eurozone countries if the EFSF or ESM funds are to be used. Further, if you make this deal for Spain, then Greece, Portugal, and ESPECIALLY Ireland are going to demand a reset. I am sure there is a coherent plan here somewhere, but I can't find it as of Monday night. What I did find is this quote in the Financial Times (jumping to the end of the story):

" 'Many Irish people looking at the deal this morning will be asking themselves why is there one set of conditions for us and another for Spain,' said Mr Doherty. Ireland's economic crisis closely resembles the situation in Spain, where a property crash has morphed into a banking crisis, leading to calls that Dublin should renegotiate its existing EU-IMF bail out deal. Aware that it is unlikely to persuade the troika to reopen its own bailout program, however, Dublin moved quickly on Sunday to deny that Spain's program would be less onerous than its own.

"The Spanish program could also produce political problems outside current bailout countries, particularly over the issue of which of the eurozone's two bailout funds is used for the rescue.

"Dutch and Finnish officials have warned they do not want the new bailout funded through the existing rescue system, the €440bn European Financial Stability Facility, because its lending is treated like any other private lender, meaning it has no seniority in the repayment queue." (emphasis mine)

The Spanish prime minister played the Germans very well. He got what appears to be a much better deal than the Irish. But then, he was playing hardball. This note from Joe Weisenthal at Business Insider:

"According to El Mundo, Spanish PM Mariano Rajoy sent a stunning text message to FinMin Guindos prior to the bailout negotiations. He said, according to El Muno editor Pablo Rodriguez:"Resist, we are the 4th power of the EZ. Spain is not Uganda." Translation: We're a major power, not some random IMF-case banana Republic.

"The followup message (according to Google translate) "If you want to force the redemption of Spain will prepare 500,000 billion euros and another 700,000 for Italy, which will have to be rescued after us."

"Bottom line: hold out for something good. We are powerful, and if they don't give in, the whole thing will go down. It will cost Europe 500 billion if Spain goes bust, and then another 700 billion if Italy goes bust. No wonder Der Spiegel, which represents the German point of view, has an article blasting Spanish blackmail."

And before we get to Charles's piece, let's look at this quick analysis by his son Louis Gave, the CEO of GaveKal, writing from Hong Kong ( www.gavekal.com):

"As we go through the few scant details of the bank bailout offered to Spain, we cannot help but shake an uneasy feeling of deja-vu all over again:

- Banks confronting a deposit flight – check.

- Sovereign shut out from debt market – check.

- Loans provided to help sovereign deal with the situation – check.

- Potentially pushing current sovereign debt investors into a subordinated position – check.

"It is on this last point that the Spanish 'bailout' could prove to do more harm than good. Indeed, as we highlighted with Greece, when policymakers transform government debt into subordinated debt, they may as well shut down that market for good. This for a very simple reason: most investors who buy government debt do so on the premise that the paper is the most 'risk-free'. These are not equity investors, carefully weighing the risk-reward of a current asset.

"Investors into sovereign debt are all about minimizing risk. The reason one buys government bonds is first and foremost for capital preservation and portfolio diversification. Subordinated debt does not meet those requirements. Thus, Europe's policymakers, from one day to the next, could potentially not only increase the Spanish debt load by 9% of GPD but simultaneously make Spanish debt considerably more risky, and thus more unattractive. Beyond an immediate knee-jerk reaction, it seems unlikely that the Spanish contraction in spreads will be meaningful or lasting."

What Europe did over the weekend was put a band-aid on a very deep gash. To actually fix the problem, Europe must remove bank liability from the various nations and make them joint and several. But that is going to be something that Germany and other nations will fiercely resist. When the dust settles, the markets will realize, I think, that this latest move did not solve the real problems. It was just a way to stop the immediate pain. There is more to come, and it will require a lot more money and the loss of a great deal of national sovereignty if the eurozone is to hold together. It took the US decades, if not a century, to get to that place. Europe has a few years under its belt at most, and the crisis is right on top of them.

I am in New York tonight, just back from dinner with some of "the guys." (Jonathan Carmel of his eponymous hedge fund, Dan Greenhaus of BTIG, Barry Ritholtz of the Big Picture, and Rich Yamarone of Bloomberg). The topics were all over the board. I am not certain we solved any big problems ourselves; but the Chinese food at Shun Lee was sure good, and the conversation was sparkling.

It is time to hit the send button. Note: There will be no new postings on the Over My Shoulder website for the next 24 hours, as we do a major web-hosting switchover.

And now, let's turn it over to the always-incisive Charles Gave.

Your sorry to rain on Spain analyst,

John Mauldin,

Editor Outside the Box

Federalism, Debt Traps and CompetitionBy Charles Gave

At times I have this feeling that I am living on a different planet than most economic commentators. Everyone is waiting to see if Germany will bite the bullet and mutualize the EMU's debt—thus saving the euro. Not only will this not work, but it would make the situation even more unmanageable, by papering over what are essentially debt-trap situations for a number European countries. The only escape for these struggling countries is through a growth-boosting improvement in competitiveness, which cannot be done under a monetary union.

Let us take the example of Italy:

Italy's economic growth has stagnated since entering the euro, yet its debt load has grown apace. Now heading into its fourth recession in 10 years, the country will see tax receipts collapse as automatic stabilizers kick in, and as a result its budget deficit will magnify. This will push the cost of capital up even higher, which in turn will depress growth further—the classic vicious cycle of a debt trap. We are seeing this quagmire not just in Italy but in many of the troubled EMU economies, including Spain.

Why is Italy in a debt trap? The answer is deceptively simple: Italy is not competitive. From 1982 to the euro's start in 2000, German and Italian industrial production expanded at the same growth rate. However, as the chart overleaf underlines, rebasing the German industrial production index to 2000, we see it has moved from 100 to 111 while Italy's IP index shrunk from 100 to 76. Italy is clearly having a harder time competing against Germany since they joined a common monetary union.

The explanation of this phenomenon can partly be explained by the next chart. In the past, the Italians could devalue now and then to increase productivity vis-a-vis the Germans. Without this option, Italy's real labor productivity has sorely lagged Germany's—i.e., the Germans are getting more bang for every "euro" buck.

With lower productivity and a higher cost of capital, one would have to be brain dead to put a factory in Italy, especially if one knows that the tax rate in Italy is going to go up to try to close the budget deficits (as if a tax increase ever led to a reduction in the deficit!). Needless to say, the financial markets have perfectly anticipated this state of affairs and expect the unavoidable re-emergence of the lira.

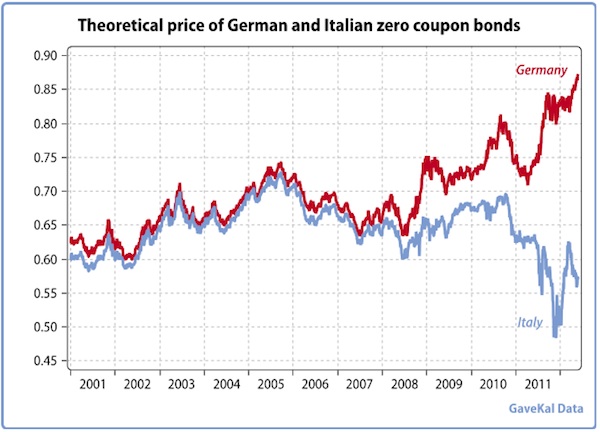

Please have a look at this graph:

Based on current 10-year sovereign prices, the chart tells us what the market is willing to pay for 10-year zero bonds of Germany and Italy. The difference between the two lines (see next chart) is about 32%—which means a 32% devaluation is already priced into the market.

The marvelous thing is that the expected devaluation and or write-off of the debt also can be seen as pricing in differences in labor costs.

Enter federalism

Let us explore now the possibility that Germany and other EMU hold- outs agrees to accept joint responsibility for all EMU debt. Then one would expect the German and Italian rates to converge again towards an average of roughly 4%, which has been more or less constant for the best part of the last 14 years, and with a very small standard deviation:

This would imply a massive bull market in Italian bonds and a massive bear market in German bonds. Since the German banks are already not very robust, they need a quasi collapse in the German bond market like a hole in the head.

However the decline in Italian yields to 4% would solve none of the Italian problems. Most crucially, it would not solve the key issue of lack of competitiveness against EMU powerhouses like Germany. Italy will not be able to grow itself out of its current bind under the yoke of currency which is overvalued for a country like Italy. Which means the structural growth rate will never catch up with the cost of capital — Italy might still have to write-off some of its debt.

And keep in mind—Italy is a country that will have its cost of capital lowered by debt mutualisation. A country like France will be much worse off as its cost of capital rises by at least like 150 bp at a time when she is also heading into a recession—drastically lowering the odds that France can escape a debt trap.

With German yields rising, one could probably say goodbye to the bull market in real estate in Germany and with three of its main clients going under one should start worrying about Germany too.

I am flabbergasted. Why would anybody believe that a federalization of the debt is a solution to the Euro crisis is beyond my understanding? Such a move would make the economic and financial situation far worse than it is today for almost every player, Italy , France, Germany Spain, Portugal.

Unfortunately, since it is at the same time idiotic and counterproductive, I fully expect the European elites to try to and go for it. If so, I would recommend selling across the board in Europe—currencies, bonds, equities—and become very cautious on the rest of the world.

My only hope is that the markets and the Greeks will stop this new suicidal move. Let's wait for the Greek elections and hope for the bad guys to win.

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2012 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.