Iran's Hyperinflation Economic Death Spiral

Economics / HyperInflation Oct 22, 2012 - 05:07 PM GMTBy: Steve_H_Hanke

My October 2009 Globe Asia column was titled "Iran's Death Spiral." In light of the recent events that have transpired in Iran, I think I might have been onto something back in 2009.

My October 2009 Globe Asia column was titled "Iran's Death Spiral." In light of the recent events that have transpired in Iran, I think I might have been onto something back in 2009.

Since early September, there has been an accelerated slide in the value of the Iranian rial. This slide has been punctuated by dramatic collapses in the demand for the rial. With each collapse, there has been something akin to a "bank run" on rials — with a sharp rise in the black market (read: free market) IRR/USD exchange rate (see the accompanying chart). Ironically, Iranians are clamoring for U.S. Dollars.

It is worth mentioning that the black-market rate is an unbiased metric. In a land where the signal-to-noise ratio is very low, the black-market rate represents an important piece of objective information. It says a great deal about the state of the Iranian economy and the populace's expectations.

On 8 September 2012, the black-market IRR/USD exchange rate was 23,040. In the course of just under a month, after two big sell offs, the rate settled at 35,000 on 2 October 2012. That is a 34.2% depreciation in the rial, relative to the greenback. It was at this 35,000 IRR/USD rate that I first calculated the monthly inflation rate implied by the rial's depreciation. The implied monthly inflation rate was 69.6%. Since the hurdle rate to qualify for hyperinflation is 50% per month, Iran registered what appears to be the start of the world's 58th hyperinflation episode.

With that, the Iranian authorities swung into action and introduced a new multiple-exchange-rate regime. There is an official exchange rate of 12,260 IRR/USD, which is available for Iranians who are importing essential goods, such as grain, sugar, and medicine. In addition, there is a "non-reference" rate, which is available at licensed dealers and can be used by importers of non-essential goods, such as livestock, metals and minerals. This rate is purportedly 2% lower than the black-market rate, though it currently (as of 10 October 2012) sits at 25,480 IRR/USD — representing a significant discount relative to the black-market rate. And then, there is the freemarket (black-market) rate that is available to anyone willing and able to avoid the ever-watchful eyes of the police.

Among other things, the multiple-exchange-rate regime generates noise in the Iranian economy. Indeed, more than one price for the same thing creates prices that lie, and lying prices make it difficult for Iranians to determine the true cost of what they are producing and ultimately selling. The multiple-exchange-rate regime, therefore, is just one more monkey wrench that is being thrown in the wheels of the economy.

The announcement of Iran's hyperinflation aroused the priesthood. In addition to implementing the new multiple exchange- rate regime, the Iranian authorities have boosted the police presence in the bazaars of Tehran and cracked down on currency traders.

As the accompanying chart shows, Iran's hyperinflation has, of course, sent the Iranian misery index to the moon. Talk about a death spiral.

Before leaving the Iranian misery index, it merits mentioning that the index was elevated prior to the 1979 Revolution. Recall that, before the last Shah was pushed off the Peacock Throne, his visions of grandeur had led him to embrace Soviet-type schemes, such as five-year plans, megaprojects, rural collectivization, model towns (shahraks), and central planners. In short, the "Soviet" Shah, who was propped up by the United States, made a mess of the economy and kept the misery index elevated.

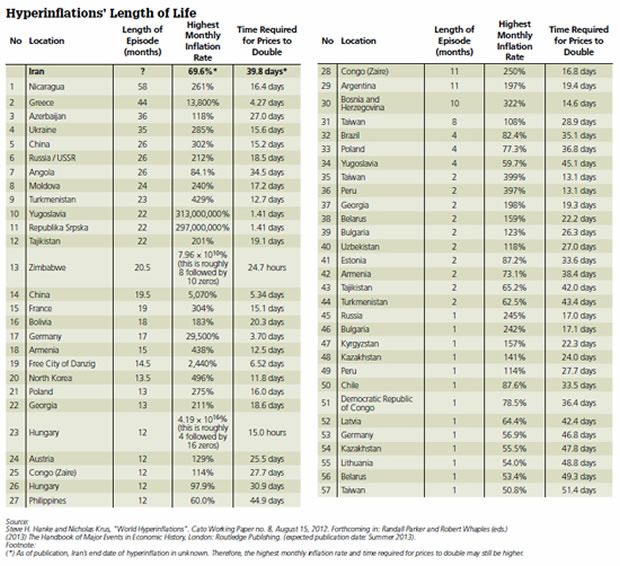

With the commencement of hyperinflation, we are left with an obvious question: "How long will Iran's hyperinflation last?" The accompanying table ranks the 57 known hyperinflations by the length of each episode. The average duration is roughly 12 months, with the longest hyperinflation being that which occurred in Nicaragua. It lasted four years and 10 months. At the other extreme, there are 13 episodes that fizzled out after one month.

So, how does one stop a hyperinflation? In my experience, as someone who has been involved in stopping 10 of the 57 known hyperinflations, there are two sure-fire ways: instituting a currency board or adopting a foreign currency (dollarization). In Bulgaria, where I was President Stoyanov's adviser, hyperinflation peaked at a monthly rate of 242%, in February 1997. On 1 July 1997, Bulgaria installed a currency board, under which the Bulgarian lev was issued. It was backed 100% by German mark reserves and fully convertible at a fixed rate with the mark. As the accompanying chart shows, hyperinflation stopped immediately and Bulgaria's misery index fell like a stone.

In Zimbabwe, President Mugabe simply looked the other way as the hyperinflation roared ahead. It peaked in mid-November 2008, reaching the second-highest level ever recorded in the world. At that point, the daily inflation rate was 98%, and it took only 24.7 hours for prices to double. Faced with this, Zimbabweans abandoned the Zimbabwe dollar, and the economy spontaneously, and unofficially, dollarized, eventually forcing the government to officially dollarize its accounts. With this, Zimbabwe's hyperinflation abruptly ended, and the misery index plunged (see the accompanying chart).

What course will Iran take? Neither the Bulgarian freemarket currency board nor the Zimbabwean spontaneous (and eventually official) dollarization appear to be in the cards. As long as the Iranians can sell some oil, the regime will attempt to muddle through.

But, there is a catch — a dangerous one — what if the sanctions advocates get their way and the screws are tightened so hard that Iranian oil exports dwindle to a trickle? The Supreme Leader might just play the ace he has up his sleeve and order the Straight of Hormuz to be blocked, among other mischiefs. This would cause more havoc than any bomb in the allies' arsenal. After all, 35% of the world's crude oil, and 20% of the world's liquefied natural gas, flow through the Strait of Hormuz.

If a diplomatic solution cannot be found (admittedly a very difficult task), then Iran promises to be one of those situations that produce a "horrible end" or a "horror without end."

By Steve H. Hanke

www.cato.org/people/hanke.html

Steve H. Hanke is a Professor of Applied Economics and Co-Director of the Institute for Applied Economics, Global Health, and the Study of Business Enterprise at The Johns Hopkins University in Baltimore. Prof. Hanke is also a Senior Fellow at the Cato Institute in Washington, D.C.; a Distinguished Professor at the Universitas Pelita Harapan in Jakarta, Indonesia; a Senior Advisor at the Renmin University of China’s International Monetary Research Institute in Beijing; a Special Counselor to the Center for Financial Stability in New York; a member of the National Bank of Kuwait’s International Advisory Board (chaired by Sir John Major); a member of the Financial Advisory Council of the United Arab Emirates; and a contributing editor at Globe Asia Magazine.

Copyright © 2012 Steve H. Hanke - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.