Basel’s Capital Curse, Beating the Drums of Bank Recapitalization

Interest-Rates / Credit Crisis Bailouts Dec 18, 2012 - 09:50 AM GMTBy: Steve_H_Hanke

In the aftermath of the financial crisis, the oracles of money and banking have been beating the drums for “recapitalization” — telling us that, to avoid future crises, banks must be made stronger. To accomplish this, governments across the developed world are compelling banks to raise fresh capital and strengthen their balance sheets. And, if banks can’t raise more capital, they are told to shrink the amount of risk assets (loans) on their books. In any case, we are told that one way or another, banks’ capital-asset ratios must be increased — the higher, the better.

In the aftermath of the financial crisis, the oracles of money and banking have been beating the drums for “recapitalization” — telling us that, to avoid future crises, banks must be made stronger. To accomplish this, governments across the developed world are compelling banks to raise fresh capital and strengthen their balance sheets. And, if banks can’t raise more capital, they are told to shrink the amount of risk assets (loans) on their books. In any case, we are told that one way or another, banks’ capital-asset ratios must be increased — the higher, the better.

Virtually all the establishment figures in economics and politics have jumped on this bandwagon. In 2010, the world’s central bankers, represented collectively by the Bank of International Settlements (BIS) handed down Basel III — a global regulatory framework that, among other things, hikes capital requirements from 4% to at least 7% of a bank’s riskweighted assets.

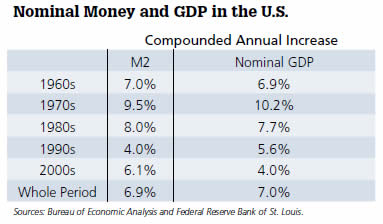

For some time, I have warned that higher bank capital requirements, when imposed in the middle of an economic slump, are wrong-headed because they put a squeeze on the money supply and stifle economic growth. As we can see in the accompanying table, this is cause for concern, because the quantity of money and nominal national income are closely related.

Not surprisingly, as banks have pared their balance sheets in anticipation of Basel III’s 2013 implementation, broad money growth in most participating economies has stagnated, at best. The result, thus far, has been financial repression — a credit crunch. This has proven to be a deadly cocktail to ingest in the middle of a slump.

One would think that upon observing the miserable results of their labor over the past few years, the oracles of money and banking would now be looking to undo their blunder. Or, at least they would begin to question the efficacy of the recapitalization frenzy.

On the contrary, central bankers (BIS, the Bank of England, the Fed, etc.), along with an alphabet soup of regulatory bodies — from Britain’s Financial Services Authority (FSA), to the United States’ Financial Stability Oversight Council (FSOC), to the G20’s Financial Stability Board (FSB), to the European Union’s European Banking Authority (EBA) — have begun to clamor for yet another round of hikes in bank capital adequacy requirements. The most recent calls have come from outgoing Bank of England Governor Mervyn King, who, as we will see, is among the “founding fathers” of the recapitalization movement. Why would the oracles want to saddle the global banking system with another round of capital-requirement hikes — particularly when Europe has just gone into a doubledip recession, and the U.K. and U.S. are mired in growth recessions? Are they simply unaware of the devastating unintended consequences this creates?

In reality, there is more to this story than meets the eye. To understand the motivation behind the global capital obsession, we must begin with Britain and the infamous Northern Rock affair, which has been well documented by Prof. Tim Congdon, in his book Central Banking in a Free Society. Incidentally, and contrary to popular belief, the opening act of the financial crisis was not the September 2008 Lehman Brothers bankruptcy. Rather, the initial volley was fired in England, with the collapse of the Northern Rock, in 2007.

On August 9, 2007, the European money markets froze up after BNP Paribas announced that it was suspending withdrawals on two of its funds that were heavily invested in the U.S. subprime credit market. Northern Rock, a profitable and solvent bank, relied on these wholesale money markets for liquidity. Unable to secure the short-term funding it needed, Northern Rock turned to the Bank of England for a relatively modest emergency infusion of liquidity (3 billion GBP). This lending of last resort might have worked, had a leak inside the Bank of England not tipped off the BBC to the story on Thursday, September 13, 2007. The next morning, a bank run ensued, and by Monday morning, Prime Minister Gordon Brown had stepped in to guarantee all of Northern Rock’s deposits.

The damage, however, was already done. The bank run had transformed Northern Rock from a solvent (if illiquid) bank to a bankrupt entity. By the end of 2007, over 25 billion GBP of British taxpayers’ money had been injected into Northern Rock. The company’s stock had crashed, and a number of investors began to announce takeover offers for the failing bank. But, this was not to be — the U.K. Treasury announced early on that it would have the final say on any proposed sale of Northern Rock. Chancellor of the Exchequer Allistair Darling then proceeded to bungle the sale, and by February 7, 2008, all but one bidder had pulled out. Ten days later, Darling announced that Northern Rock would be nationalized.

Looking to save face in the aftermath of the scandal, Gordon Brown — along with King, Darling and their fellow members of the political chattering classes in the U.K. — turned their crosshairs on the banks, touting “recapitalization” as the only way to make banks “safer” and prevent future bailouts.

In the prologue to Brown’s book, Beyond the Crash, he glorifies the moment when he underlined twice “Recapitalize NOW.” Indeed, Mr. Brown writes, “I wrote it on a piece of paper, in the thick black felt-tip pens I’ve used since a childhood sporting accident affected my eyesight. I underlined it twice.” I suspect that moment occurred right around the time his successor-to-be, David Cameron, began taking aim at Brown over the Northern Rock affair.

Clearly, Mr. Brown did not take kindly to being “forced” to use taxpayer money to prop up the British banking system. Nor did the taxpayers take kindly to having their precious pounds pulled from their wallets. But, rather than directing his ire at Mervyn King and the leak at the Bank of England that set off the Northern Rock bank run, Brown opted for the more politically expedient move — the tried and true practice of bank-bashing.

It turns out that Mr. Brown attracted many like-minded souls. As the financial crisis intensified, politicians, regulators, and central bankers around the world pointed their accusatory fingers at commercial bankers. In the months following the British Financial Services Authority’s announcement of higher capital adequacy requirements for U.K. Banks (November 2008), momentum for bank recapitalization swelled, culminating in Basel III (September 2010).

The establishment has erupted in cheers at the increased capital-asset ratios. They assert that more capital has made the banks stronger and safer. While, at first glance, that might strike one as a reasonable conclusion, it simply is not. In response to Basel III, banks have shrunk their loan books and dramatically increased their cash and government securities positions, which are viewed under Basel as “risk-free,” requiring no capital backing.

Even the International Monetary Fund (IMF) and the Paris-based Organization for Economic Co-operation and Development (OECD) quietly acknowledge that this will hamper GDP growth and raise lending rates. But, thus far, they have failed to fully assess the negative impact of raising capital requirements during an economic slump. The problem is that they are not properly focused on the money supply. Indeed, when viewed in terms of money — bank money, to be exact — the picture comes into sharp relief.

For a bank, its assets (cash, loans and securities) must equal its liabilities (capital, bonds and liabilities which the bank owes to its shareholders and customers). In most countries, the bulk of a bank’s liabilities (roughly 90 percent) are deposits. Since deposits can be used to make payments, they are “money.” Accordingly, most bank liabilities are money.

To increase their capital-asset ratios, banks can either boost capital or shrink risk assets. If banks shrink their risk assets, their deposit liabilities will decline. In consequence, money balances will be destroyed.

The other way to increase a bank’s capital-asset ratio is by raising new capital. This, too, destroys money. When an investor purchases newly-issued bank equity, the investor exchanges funds from a bank account for new shares. This reduces deposit liabilities in the banking system and wipes out money.

So, paradoxically, the drive to deleverage banks and to shrink their balance sheets, in the name of making banks safer, destroys money balances. This, in turn, dents company liquidity and asset prices. It also reduces spending relative to where it would have been without higher capital-asset ratios.

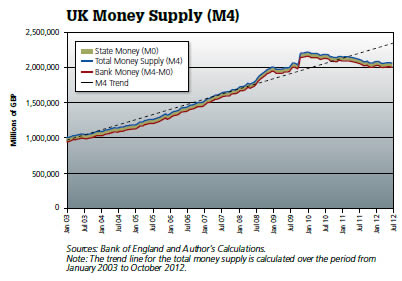

In England, this government-imposed deleveraging has been particularly disastrous. As the accompanying chart shows, the U.K.’s money supply has taken a pounding since 2007, with the money supply currently registering a deficiency of 13%.

The source of England’s money-supply woes is the allimportant bank money component of the total money supply. Bank money, which is produced by the private banking system, makes up the vast majority — a whopping 97% — of the U.K.’s total money supply. It is bank money that would take a further hit if Mervyn King’s proposed round of bank recapitalization were to be enacted.

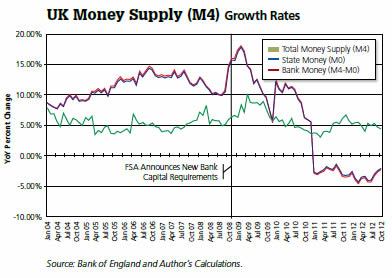

As the accompanying chart shows, the rates of growth for bank money and the total money supply have plummeted since the British Financial Services Authority announced its plan to raise capital adequacy ratios for U.K. Banks.

How could this be? After all, hasn’t the Bank of England employed a loose monetary policy scheme under King’s leadership? Well, state money — the component of the money supply produced by the Bank of England — has grown by 22.3% since the Bank of England began its quantitative easing program (QE) in March 2009, yet the total money supply, broadly measured, has been shrinking since January 2011.

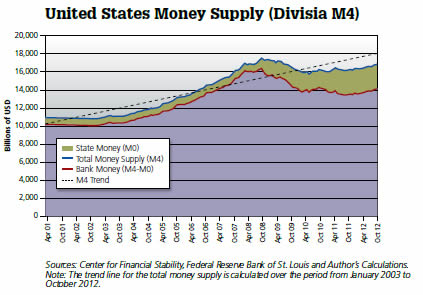

The United States has also employed this loose state money/tight bank money monetary policy mix. With bank money making up 85% of the total U.S. money supply, broadly measured, it should come as no surprise that the U.S. is also registering a money supply deficiency — 6.73% to be exact (see the accompanying chart).

For all the talk of QE3 and Fed’s loose monetary policy, the inconvenient truth is that overall money supply in the U.S. is still, on balance, quite tight. It is true that the Fed has had its foot to the monetary accelerator for several years, leading to artificially low interest rates — what Prof. Ronald McKinnon described in his 2006 book, Exchange Rates under the East Asian Dollar Standard: Living with Conflicted Virtue, as a zero-interest-rate trap. But, rather than stimulate the economy, this is only has succeeded in further exacerbating the credit crunch, all the while punishing savers and retirees with depressed yields.

This is the case because, under Basel, a bank’s capital adequacy is calculated as a ratio of equity capital over riskweighted assets. This feature of Basel regulations counts cash and, more importantly, government securities as “riskfree” assets. In consequence, banks can load up on certain government securities, without having to adjust their capital ratios. So, in terms of capital adequacy, government securities are “cheaper” assets to have on your balance sheet than loans. But, how can banks make money without issuing wholesale and/or retail loans?

Well, it’s easy and “risk free” to boot. In the U.S., for example, by holding the Federal Funds Rate near zero, the Fed creates an opportunity for banks to borrow funds at virtually no cost. Banks can then use these funds to purchase two-year U.S. Treasury notes, with a spread of about 8 basis points. That doesn’t sound like much. But, since banks don’t have to hold capital against U.S. Treasuries, their positions in U.S. government securities can be leveraged to the moon. Well, not really. But, at a leverage ratio of 20, a bank can do quite well by playing the Treasury yield curve.

Banks have responded to this incentive, and the result has been a decrease in bank loans, further deepening the credit crunch. And, since credit is a source of working capital for businesses, a credit crunch acts like a supply constraint on the economy. Even though it appears as though the economy has loads of excess capacity, the supply-side of the economy is, in fact, constrained by the credit crunch. It is not surprising, therefore, that the economy is not firing on all cylinders.

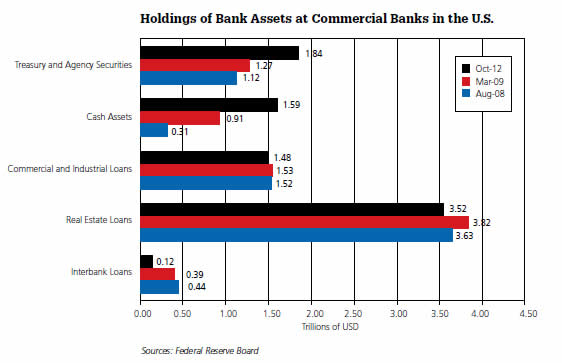

So, what have the oracles accomplished? Well, for starters, their saber-rattling put the banking system on notice that higher capital requirements were on the way. Since the mere expectation of higher capital requirements is reason sufficient for banks to begin deleveraging, banks began trimming their balance sheets, even before Basel III was finalized. As the accompanying chart for the U.S. illustrates, banks have continued to shrink their balance sheets in anticipation of further actions by regulators.

In consequence, if the political chattering classes continue to call for ever higher capital requirements for banks, expect to see tight credit, anemic growth, and an unhealthy money supply picture for the foreseeable future.

Some might argue that this is an acceptable price to pay for “safe” banks. But, do the Basel III capital requirements actually make banks “safe”, particularly when imposed in the middle of a slump? Central bankers claim that higher capital requirements will create a buffer that will protect against future bailouts of the banking system. The dirty little secret of the recapitalization advocates is that — for a highly-leveraged bank — a Basel III-level capital-asset ratio (7%) is unlikely to be a sufficient buffer against a massive loss. Indeed, The Economist estimates that Lehman Brothers had a capital asset ratio of about 11%, just five days before it declared bankruptcy. Clearly, it didn’t take long for Lehman to blow through that “healthy” capital buffer.

The problem is that by trying to implement these capital requirements now — in the middle of an economic downturn — the financial and political establishment have only succeeded in stifling the money supply, and thus overall economic growth. In consequence, Basel III capital requirements have actually made economies more vulnerable and have thus made banks less safe. When combined with artificially low interest rates approaching the zero bound, it should come as no surprise that we’re having trouble waking up from this economic nightmare.

The solution? Scale back untimely, excessive bank capital requirements and put an end to the zero-interest-rate trap. The oracles have done enough — now, it’s time to let the market repair the damage.

his article appeared in the January 2013 issue of Globe Asia.

By Steve H. Hanke

www.cato.org/people/hanke.html

Steve H. Hanke is a Professor of Applied Economics and Co-Director of the Institute for Applied Economics, Global Health, and the Study of Business Enterprise at The Johns Hopkins University in Baltimore. Prof. Hanke is also a Senior Fellow at the Cato Institute in Washington, D.C.; a Distinguished Professor at the Universitas Pelita Harapan in Jakarta, Indonesia; a Senior Advisor at the Renmin University of China’s International Monetary Research Institute in Beijing; a Special Counselor to the Center for Financial Stability in New York; a member of the National Bank of Kuwait’s International Advisory Board (chaired by Sir John Major); a member of the Financial Advisory Council of the United Arab Emirates; and a contributing editor at Globe Asia Magazine.

Copyright © 2012 Steve H. Hanke - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

|

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.