Uranium, Cobalt and Silver - Recognizing Investor Opportunity In Difficulty

Commodities / Commodities Trading Jun 29, 2013 - 12:44 AM GMTBy: Richard_Mills

Right now I’m a big fan of uranium, cobalt and silver. Here’s why…

Right now I’m a big fan of uranium, cobalt and silver. Here’s why…

Uranium

In 2012 world consumption of uranium was 165 million pounds versus 152 million pounds of mined uranium production. Globally there are 434 nuclear reactors operable, 67 reactors are under construction, 159 are on order or planned and 318 are proposed.

For investors the uranium supply/demand picture is interesting for several reasons:

1. Nuclear power generation is being ramped up across the globe.

2. Japan is restarting its reactors.

3. The Megatons to Megawatts deal, the HEU agreement, is coming to an end.

4. The U.S. has no uranium security of supply

Global uranium stockpiles have been filling the gap between consumption and production for more than two decades. By far the largest contributor has been the Russian Highly Enriched Uranium (HEU) agreement, providing 24 million pounds of uranium to the market every year. However, secondary supplies are drying up and the HEU agreement is coming to an end in 2013.

Cameco (one of the world's largest publicly traded uranium companies) estimates world uranium demand will increase to about 240 million pounds by 2022.

The U.S. is in an especially dire situation in regards to the security of its uranium supply and the situation doesn’t look set to improve through exploration or new mine development anytime soon. Employment for uranium exploration in the U.S. was 161 person-years in 2012, a 23 percent decrease compared to 2011. The long lead time of uranium mine development - up to ten years - means that the industry is unable to respond quickly to sudden increases in demand or significant supply interruptions. With the recent lower uranium prices, delays and cancellations of new projects is becoming the norm and exacerbating the coming global and U.S. supply crisis.

Ten percent, or just 4.9 million pounds, of the 49 million pounds U3O8e uranium loaded into U.S. civilian nuclear power reactors during 2012 was from U.S. mined uranium, 90 percent was foreign supplied uranium.

According to the World Nuclear Association (WNA) there are plans for 13 new reactors in the U.S., three reactor units are under construction, and as many as six may come online in the next decade.

Expect uranium spot prices to start climbing to equalize with long term prices and then both to begin a rapid advance as the supply squeeze starts to be felt.

Cobalt

UK-based trading company Darton Commodities said, in its 2012-2013 cobalt market review, that:

- The fundamental outlook for the cobalt market improved in 2012

- A structural price recovery is likely in 2013 as there was a five percent drop in global cobalt output in 2012

- During 2012, refined cobalt supply dropped an estimated 3,839 mt to 76,040 mt, 4.8 percent below 2011

- Global cobalt consumption grew an estimated 6.8 percent in 2012, reaching 73,900 mt

- Consumption from the battery sector saw robust growth on the back of demand for tablet and smart phone devices, with cobalt usage breaching 30,000 mt

- Demand from the super-alloy sector continued to see strong growth from the aerospace and industrial gas turbine markets, with demand reaching 14,800 mt

- Strong demand growth in 2012 saw significant destocking of cobalt materials in China over the year

- Darton estimated cobalt demand in China increased 13.7 percent from 2011 to 28,900 mt in 2012

"Demand growth led to a gradual but significant destocking of both unrefined and refined cobalt materials in China. Consequently, the overall supply and demand imbalance which has undermined the cobalt market for the past couple of years appears to have been restored resulting in a fundamentally more balanced market outlook for 2013." Darton Commodities

The Democratic Republic of the Congo (DRC) supplies 55 percent of the world’s cobalt. With much of the world’s incremental supply over the coming years expected to be sourced from the DRC expectations might be too high…

Crisis in the Congo is giving ahead of the herd investors an exciting investment opportunity.

Between an outright ban on the export of raw minerals, project ownership grabs, power shortages and armed conflict the DRC’s resource sector is imploding. Most of the DRC’s cobalt goes straight to China who refines it and sells it to the world, a major amount – 20 percent - goes to the U.S. which imports 85 percent of its cobalt needs, expect both countries to be screaming for cobalt as a supply crunch gets underway because of the ongoing Congo drama.

The supply sides of both cobalt and uranium are shrinking while demand increases and security of whatever supply there is, is far from assured - perfect storms that bode well for investments in both cobalt and uranium.

Silver

Silver bullion sales are constantly breaking records, high premiums over spot are not fazing buyers. Sales of silver coins by the U.S. Mint (one of the world’s top producers of gold and silver coins) have set a record high in the first half of 2013. That’s the best start to a year…ever.

Here’s a question worth considering – when was the last time you heard of a bull market ending, in any commodity, let alone a money metal like silver, with a period of sustained, record physical demand two years after peak prices?

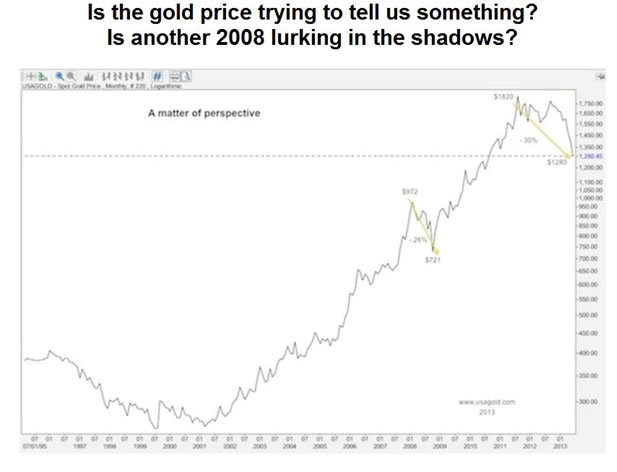

Michael Kosares, of usagold.com, has put to together this excellent chart and his short commentary follows.

“This monthly gold chart is drawn on the logarithmic scale in order to remove some of the melodrama to the latest correction. Linear charts emphasize nominal price movement while a log chart emphasizes the percentage movement. By reviewing gold’s latest correction on a percentage basis, we can put things into a little bit better perspective. The 2008 correction was 26%; the current correct thus far has been 30%. In short, we’ve been here before…” Michael J. Kosares

The high-to-low down moves in gold and silver we’ve recently witnessed are very close, percentage wise, to the down moves we saw in 2008, if the precious metals bull market corrective phase we have just suffered through has bottomed, silver will, much sooner than later, soar.

“In the middle of difficulty lies opportunity.” Albert Einstein

Investors need to ask themselves “is the precious metals bull market over?” This scribe doesn’t believe it is, and if you believe the bull is not dead here’s the opportunity in silver…

From January 2000 gold went from $300.00 per ounce to almost $1,900.00, while silver, in the same time period went from roughly $4.50 to almost $46.00. As you can see from the above charts the bulk of gains were captured from the end of 2008 to the peak prices, in both gold and silver, in the summer of 2011. Gold’s gain from roughly $750.00 to $1850.00 was impressive but even more impressive was silver’s gain – from just over nine bucks to $46.00.

Conclusion

“To recognize opportunity is the difference between success and failure.” Anon

It’s pretty obvious why, after reading the above pages, I’m a huge fan of, in no particular order, uranium, silver and cobalt.

Demand for uranium and cobalt isn’t going to disappear anytime soon, these critical, and yes strategic, green energy metals are just as necessary to the functioning of a modern economy as the water we drink to survive. Silver bullion demand is soaring because it is a monetary, industrial and miracle medical metal whose current investment potential returns from here look tremendous.

Demand for the three are going up, supply is not going to keep pace, currently the junior resource companies that search for and develop deposits of these minerals are severely undervalued and out of favor with investors.

How can this not be a good situation for investors? Shouldn’t all three sectors, and the quality, moneyed up, junior resource companies (who are still extremely active developing their projects and increasing shareholder value), be on all our radar screens? Are they on yours?

If not, maybe one should be.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including:

Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2013 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Richard (Rick) Mills Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.