Lessons from Japan: Prepare for 0% US Interest Rates

Interest-Rates / US Interest Rates Apr 08, 2008 - 02:51 PM GMTBy: Jim_Willie_CB

The prospect of a US Fed 0% rate becoming a reality has been on my mind since August when the subprime made news hit. In my view, the entire mortgage bond structure would suffer massive losses in a successive of waves, beginning with subprimes, extending to primes, and concluding with commercials. How could housing distress not spread to nearby shopping malls, office complexes, and urban centers? First, USTreasurys would draw huge sums of money, reducing bond yields across the entire set of maturities. Second, the coincident event would be a painful recession. The US financial system would be unable this time to pull the US Economy out of the quicksand. Far too many vicious cycles would kick into gear, unleashing powerful feedback loops. We are seeing them in full glory now. Housing prices and foreclosures, bank write downs with sliding home collateral, US Dollar decline with a slower US Economy, household spending with rising costs, they are work to sustain more pain.

The prospect of a US Fed 0% rate becoming a reality has been on my mind since August when the subprime made news hit. In my view, the entire mortgage bond structure would suffer massive losses in a successive of waves, beginning with subprimes, extending to primes, and concluding with commercials. How could housing distress not spread to nearby shopping malls, office complexes, and urban centers? First, USTreasurys would draw huge sums of money, reducing bond yields across the entire set of maturities. Second, the coincident event would be a painful recession. The US financial system would be unable this time to pull the US Economy out of the quicksand. Far too many vicious cycles would kick into gear, unleashing powerful feedback loops. We are seeing them in full glory now. Housing prices and foreclosures, bank write downs with sliding home collateral, US Dollar decline with a slower US Economy, household spending with rising costs, they are work to sustain more pain.

Unlike Japan , the approach toward 0% would kill the US financial system. The reaction would have to be unprecedented attempts to rebuild the core capital of the banking system. The US bank capital went negative in February, confirming a forecast of mine made in the summer of 2006. The US banking system has gone from barely insolvent to deeply negative in capital core during the last four weeks, in a dramatically worsening slide. The Federal Reserve balance sheet reports a worsening negative capital core position, according to Barrons . What was a MINUS $8.5 billion US bank reserves capital core in early March has turned to a MINUS $61.8 billion capital core by March 31. Refer to non-borrowed reserves. A shocking reversal of fortune has befallen the US banking system since mid-December, when free reserves logged in at PLUS $43.8 billion.

With no trade surplus, not much left in an industrial base, no giant private savings, the United States compares very badly versus Japan . The Land of the Rising Sun managed to tread water for over a decade, until its banks were lifted into solvency. The US does not have such a luxury. Instead, the US Federal Reserve has made numerous overtures to the Scandinavians, in order to learn about how Sweden , Norway , and Finland recovered from bank crises in the early 1990 decade. As the US Fed opts to pursue the Nordic formula, they might find themselves stuck with the Japanese insolvency nightmare, and soon might have 0% offered. The land of Vikings ordered strict recovery rules, accounting rules, numerous bank seizures, but were spared the ignominy of credit derivative rooftops dictating the policy maneuvers. The Sword of Damocles is directly above Wall Street banker heads in the form of these savage derivatives. The cokeheads on Wall Street (truth or dare?) have held the US banking system and USEconomy hostage to their lunatic unregulated leverage games, with a virtual free rein on fraud due to collusion. How can Wall Street be expected to tread a path of honesty when the highest offices of the USGovt engage in questionable wars, shred the Constitution, undermine financial markets with constant interference, condone fraud with hurricane relief, and lie on national economic statistics? How can Wall Street be expected to fear rules enforcement when men of their own stained cloth sit in regulatory offices? How can Wall Street be expected to use discipline when USFed bank oversight cannot begin to understand what their complex and exotic financial contract instruments do?

CHORUS OF WARNINGS

In the banking sector, nonsense continues to spew about the worst being over. The reality is that not even half the pain has been witnessed nor suffered yet. Paul Krugman expects to see a $1000 tag on bank losses, but worse, perhaps 20 million homeowners by year end mired in negative equity, equal to one quarter of the total count of homes in the nation. He sees home equity value lost will easily reach $5 trillion ($5000 billion). He expects the current USEconomic recession to extend into 2010 or perhaps 2011, identified by a pickup in employment. That gives the USFed a long time to continue cutting official interest rates, and the gold bull roaming through broad pastures. In synch with my forecast, he expects the USFed will stop cutting interest rates again and again down to 0%, mimicking the Japanese Zero Interest Rate Policy (ZIRP). A year ago, my urge was to claim this forecast, but instead a 1% forecast was suitable. That is certain to cause havoc with the USDollar and major US banks. No doubt about it, the key factor is the housing decline, which in no way has stabilized. Worsening home collateral will be a continuing hot knife to cut into bank balance sheets via the mortgage bonds arteries.

In the housing market, up to 40% of home sales in Las Vegas and San Diego involve foreclosures. No stability whatsoever is visible, as inventory is supplied from failed homes amidst failed lives. National sales assistance agencies report that new supply arrives faster than they can be sold, like twice as fast. First American CoreLogic estimates that foreclosed properties accounted for 493k of all homes on the market for sale in January, up from 231k one year ago. That makes for an 11% ratio now versus a 6.7% ratio a year ago. Both Merrill Lynch and Goldman Sachs expect continued significant housing price declines in the current year. The result will be much more bank writeoffs, steps into insolvency, requests for USFed aid, and possible high profile bankruptcies.

Charles Morris, author of “The Trillion Dollar Disaster” expects $1000 in total defaults and writedowns. He writes, “The sad truth is that subprime is just the first big boulder in an avalanche of asset writedowns that will rattle on through much of 2008.” Precisely! He regards the US financial system as contaminated with hidden debt, inflated valuations, and phony AAA ratings. He points to hedge funds as owning the last tailing pit of toxins, now the site of heightened weakness. Their equity stands at $750 billion. Wall Street shoveled tons of damaged bonds to client hedge funds at discount several months ago, now worth even less. Several waves of their failures are likely on an ongoing basis. In fact, Wall Street banks will be tempted to use the USFed lending facilities at the same time as ordering margin calls on their own hedge fund clients, forcing raids on their best assets. They have seen the playbook used by JPMorgan against Bear Stearns, and are likely to use it themselves. This complex angle into an open door of a different aspect of the Mussolini Fascist Business Model is analyzed fully in the April issue of the Hat Trick Letter, due out in midweek.

John Mack of Morgan Stanley expects two more quarters of bank bond pain, in a candid public statement made today. He foresees pain coming in the commercial mortgage backed security arena, which seems on nobody's radar these days. He called progress at the 4th and 5th innings for commercial mortgages. To date, a hefty $120 billion has been written off as losses by major banks and investment banks. Goldman Sachs economists believe that leveraged institutions in the United States have written off less than half of the losses coming from the current mortgage debacle. They did not fix blame on the subprime loans, properly. Of the cumulative losses, GSax expects 15% to 20% to come from commercial mortgages, the next shoe to drop.

The commercial CMBX mortgage index spreads imply a huge number of commercial defaults in the next couple quarters. Nitwit emails have come to me, stating that pessimism has peaked, blood flows in the streets. No, worse comes. The elite GSax firm expects a continued tightening of credit supply for lending as the banks pull back to preserve capital, as fewer loans will be approved and granted. They forgot to mention that the next wave of bank bond losses couple send even Goldman Sachs into insolvency. A mere 3.6% fall in their $1100 billion portfolio of assets would render them broke. A mere 3.0% fall in the Merrill Lynch $1000 billion portfolio of assets would render them broke. Even less, a mere 2.3% fall in the Citigroup $2100 billion portfolio of assets would render them broke.

Further declines in bank assets are highly likely events. No! The worst has not been seen for big leveraged financial institutions, not yet, not by a long shot. They are walking the Battan Death March, seeking reprieves, forced to eat their own fecal diets. They might have shipped toxic bonds worldwide, but they stuffed plenty in their own cupboards and refrigerators, now ending up on their dinner tables. WE HAVE YET TO SEE THE FAILURE OF BOATLOADS OF INNOVATIVE PRIME ADJUSTABLE MORTGAGES. They are called Exploding ARMs for a reason. Unlike subprime loans which force monthly payments up by 30% to 50%, Exploding ARMs force monthly payments up by double or triple. They punish homeowners for their negative amortization violations, whereby they underpaid interest and tripped upper limit thresholds.

Such folks are in real big trouble, since in most cases, they face being underwater with negative home equity at the same time, owing more to the bank than the home is worth. And then there is the $1000 billion in shaky credit card debt, and the gaggle of failing car loans. Car repossession rates have jumped to a decade high. And car thieves are stealing catalytic converters in pursuit of platinum, worth up to $1000 per unit on large SUVs. Oy oy oy! The nightmare of housing, including trashing foreclosed properties, bribes for keys to the homes (called Anger Escrow), food stamp usage on the rise, all is covered in the April HTL newsletter. The US is slowing sliding into a Third World nation, whose premiere trait is puppet governmental leaders of corrupt variety.

GREENSPAN ORIGINAL SIN

Sir Alan Greenspan has come under fire from many fronts, justifiably. He is the chief architect, apologist, and underwriter of the banking system that busted last year. He boasted of sophisticated risk offloading models that brought about stability. He boasted of innovative financial instruments that enabled a long housing boom with more participants. Too bad his design was heretical and flawed! Few seem to properly recognize what his original sin was, committed in 1994. It was then that he departed from a responsible monetary policy. He publicly defended an important change. Instead of permitting the money supply to grow in consistent step with economic growth, he unleashed money supply growth, letting it grow more briskly. Only if the Consumer Price Index showed a warning sign in a rise would the Greenspan Fed halt monetary growth. What an insane concept!!! The CPI is by far the most corrupted economic statistic, now under-stating price inflation by almost 6%.

Two years later, he gave his famous ‘Irrational Exuberance' speech decrying the stock frenzy, as the Dow Jones Industrial index jumped from 4000 to 5000 to 6000. Here was the root problem, the original sin, the initial heretical act by a central banker, where the seeds of financial crises were sown. The wreckage came in the Asian Meltdown in 1997, the Russian Default in 1998, the US tech telecom stock bust of 2000, and the housing & mortgage debacles from 2007 through 2011. This final crisis is the worst of all, since home equity losses will match stride for stride the bank bond losses, trillion$ for trillion$. However, the ultimate disaster will be what we see now, TOTAL DESTRUCTION OF THE US BANK INDUSTRY. This is the Greenspan Legacy! The desperate attempts to fight it will send gold to $2000 easily, and silver to $40 easily.

US BANKS PALE TO JAPANESE STRENGTH

The United States does NOT compare well to Japan , as written in a seminal article of mine before the launch of the Hat Trick Letter. A look back, another quick read, and this article seems timeless, written a long time ago, but so relevant today. “ Japan , Argentina , Weimar , or Muddle?” (click here ) was published in April 2003. Its main points are worth a quick summary. Differences between the US and Japan are very unfavorable, relating to currency valuation, bankruptcy ease, saving propensity, foreigner debt ownership, financial engineering, monetization techniques, basic integrity, and intervention willingness:

• unlike Japan , USEconomy cannot tolerate a declining USDollar

• unlike Japan , USEconomy permits bankruptcies as a regular course of business

• unlike Japan , USEconomy depends upon consumption & spending

• unlike Japan , much US debt is owned by foreigners, with a trade gap widening

• unlike Japan , US Structured Finance has created a megalith monster

• unlike Japan , US Federal Reserve is a monetization machine on steroids

• unlike Japan , US institutions harbor widespread corruption

• unlike Japan , US maintains a pervasive interventionist attitude

The United States is gradually entering a Liquidity Trap bearing strong resemblance to the one that had ensnared Japan 's economy during most of the 1990 decade. Denials that the US compares badly seem patriotic at best, and obtuse at worse. The trap of low interest rates is now very evident inside the USA . It is not characterized by low liquidity, but rather high liquidity. Official monetization initiatives are kept secret, directed increasingly toward Wall Street cronies, while the public is denied loans under harsher terms. The current liquidity trap is much worse than such a minimal label describes. The US banking system is dysfunctional, suffering seizures and lockups, plagued by collateral distrust, reporting gigantic losses not seen since the Great Depression. Banking and economic leaders would be thrilled to ONLY have a liquidity trap problem.

ABN Amro of the Netherlands leads the pack in recognition of the potential reality of 0% US rates as a reality. US bankers learned from the Japanese experience in the last ten years, seeing 0% ZIRP as a last defense against an outbreak of deflation, in acceptance of an inflation buffer. UBS chief economist Robert Lind said, “Senior officials have already laid out the potential policy choices. Given the scale of the potential shock to aggregate demand, I suspect policy makers are already contemplating the constraint of the zero bound.” Lind believes along with 0%, the USFed could use other tools as well. Japanese financial services minister Watanabe points out that an important difference exists between the past Japan crisis and the current US crisis. In Japan , the problem was contained within the banking sector. In the US , it has grown in a contagion to render extreme damage and seizures to many areas of the financial industry. He finds it difficult to properly assess the level of damage, since the fire is still spreading. He warns that a severe USDollar crisis could result, if cooperative action is not taken by other major central banks.

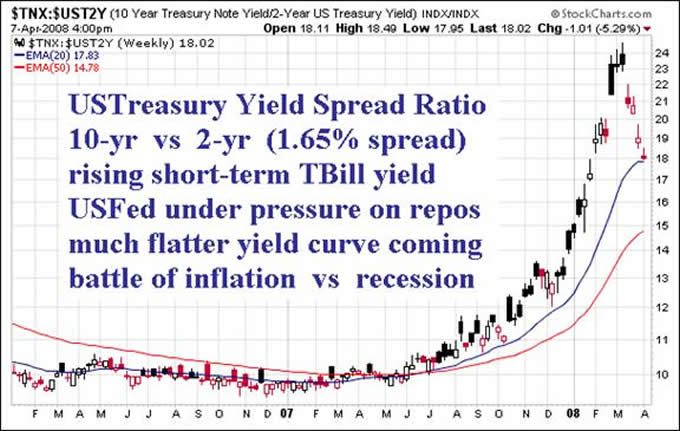

The USFed has essentially become a bond pawnbroker in a bad neighborhood dominated by white collar criminal looters, where the police get ripe payoffs. The compromised central bank has limitations, and soon could run low on balance sheet quality. They stepped into the banking void and filled it. Unfortunately, they did so with reckless abandon as they exposed the corrupt nature of JPMorgan, its extreme vulnerability, and has encouraged those with access to the USFed lending facility windows to execute similar raids. This is a moral hazard of another ugly side, yet high order. Next comes USGovt massive stimulus, larger than the puny $600 per household, construction finally of the New Resolution Trust Corp in the mortgage complex, and grand spillover into the USEconomy. The USTreasury yield curve has flattened lately, explained in the April HTL issue. The USFed must juggle its balance sheet. If foreigners do not abandon the USTreasurys and USDollar, the yield curve will flatten further. A recession would keep long-term bond yields down, but also motivate foreign sellers.

THE NATIONAL BALANCE SHEET IS WRETCHED. So an increasing number of banks have negative core capital, an increasing number of homeowners have negative home equity, and an increasing number of car owners have negative car equity. The USGovt runs gargantuan federal deficits, and the USEconomy runs mammoth trade deficits. The entire USEconomy is fighting desperately to avoid insolvency and bankruptcy. The USFed and USGovt response will be a powerful wave of monetary inflation for a few years. The result will power gold and silver to unexpected heights.

A detail. Did anyone notice that the March Jobs report details? Even though at MINUS 80k jobs in the non-farm payroll count, a hefty job loss to be sure, it could have been worse. The final tally was heavy doctored by the lunatic Birth-Death Model, which added 142k jobs from small businesses supposedly thriving in this environment. Are you kidding me? The March Jobs should have been MINUS 222k jobs. The same was true of February. Its B-D Model added 135k jobs from a thriving small business climate. Are you kidding me? The USFed must be panicking. They will cut rates again and again, until they have no ammunition left. They will soon print money and monetize their refunding operations. The USDollar will be under siege. But fortunately for the downtrodden buck, foreign economies are slumping. Foreign central banks will also be cutting official interest rates. The USDollar will find support from global rate cuts, which will send gold and silver prices soaring again, but on more continents. It is basically ‘Inflate or Die' still.

GOLD WILL RIDE THE USFED SURFBOARD

Gold was ambushed in mid-March. The motivated authorities were sweating bullets. They ordered banks to deliver margin calls. Speculators led by hedge funds were forced into broad liquidation. However, the trend is intact. The moving averages are rising. Support has been found. The gold price had a deep reluctance to stay under the 900 level. Stability has returned, enough to start the creation of a new base. The big breakout since August has now registered two noticeable corrections in classic style, a small one followed by a large one. With nothing having been solved on US bank problems, and USEconomic recession worsening, the additional stimulus and rabid monetary growth will send gold flying again soon. Look for an assault on the 1100 level within two or three months.

Silver is behaving with more of a stiff backbone than gold. Sure, it took a big hit, enough to give investors a nice discount on silver additions to the portfolio. Silver displays a stronger adherence to its uptrend line. It too has rising moving averages. All the volatility seen since mid-March remarkably has not done much technical damage on the chart. A new base is being created, for a price advance into the 20s soon, like this spring. Do not be surprised if silver vaulted toward the 25 level within two or three months.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

“Your financial commentaries are extremely insightful and have saved me a ton of money. The subscription has more than paid for itself. This should be an interesting year to say the least!” (RickF in Texas )

“The unfortunate demise of Dr. Kurt Richebacher leaves Jim Willie, Bob Chapman, and Jim Sinclair as the finest financial minds on the scene today.” (DougR in Nevada )

“There are four writers that I MUST READ. You are absolutely one of those favorites!! William Buckler, Ty Andros, Richard Russell, and YOU!!” (BettyS in Missouri )

“Your newsletter caught my attention when the Richebächer report ended. Yours has more depth and is broader in coverage for the difficult topics of relevance today. You pick up where he left off, and take it one level deeper, a tribute.” (JoeS in New York )

By Jim Willie CB

Editor of the “HAT TRICK LETTER”

www.GoldenJackass.com

www.GoldenJackass.com/subscribe.html

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise like a cantilever during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by heretical central bankers and charlatan economic advisors, whose interference has irreversibly altered and damaged the world financial system. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy. A tad of relevant geopolitics is covered as well. Articles in this series are promotional, an unabashed gesture to induce readers to subscribe.

Jim Willie CB is a statistical analyst in marketing research and retaicl forecasting. He holds a PhD in Statistics. His career has stretched over 24 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.