12 Reasons Why Gold Price Will Rebound and Make New Highs in 2014

Commodities / Gold and Silver 2014 Oct 25, 2013 - 09:24 AM GMTBy: Jason_Hamlin

Investor sentiment towards precious metals is at the lowest level in over a decade. Many analysts believe the bull market is over and are calling for sub-$1,000 gold in 2014. Even diehard gold bugs are losing faith, as the correction has been longer and more severe than most had anticipated.

Investor sentiment towards precious metals is at the lowest level in over a decade. Many analysts believe the bull market is over and are calling for sub-$1,000 gold in 2014. Even diehard gold bugs are losing faith, as the correction has been longer and more severe than most had anticipated.

So, is it time to throw in the towel? Is the bull market in precious metals really over?

In order to answer this question, I thought it would be constructive to re-visit the fundamental drivers of the gold price and determine if anything changed over the past two years to weaken the bullish case. My conclusion is that nearly all of the fundamental factors that have been driving the gold price higher in the past decade have only strengthened in the past two years. Now that the correction has most likely run its course, I expect gold to rebound into the close of the year and bounce sharply higher in 2014. Here are the 12 reasons why…

#1 – Rapidly Growing Debt

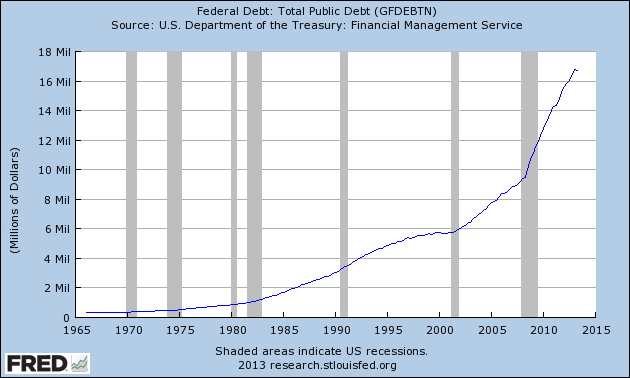

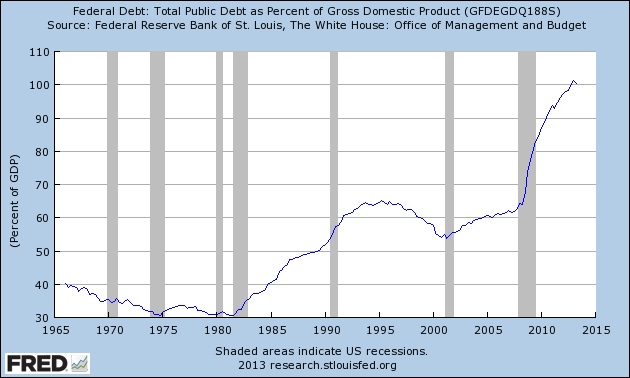

Just one day after President Barack Obama signed into law a bipartisan deal to end the government shutdown and avoid default, the US debt surged a record $328 billion, the first day the government was able to borrow money. The U.S. national debt has increased by more than a trillion dollars in the past 12 months. This pushed the total debt above $17 trillion for the first time in history. As the debt increases and GDP growth slows, the debt-to-GDP ratio will continue to rise at an accelerating pace. This is simple math and it dictates an ongoing slide in the purchasing power of the dollar and rise in the purchasing power of real assets and particularly monetary metals such as gold and silver.

The following charts show the steepening rise in total public debt and the debt-to-GDP ratio of the United States. Many economists view a debt-to-GDP ratio of 100% as the point of no return. It is a slippery slope that is certain to push higher at an accelerated rate in the coming years.

Note that alternate calculations of the total debt including unfunded liabilities and off-balance sheet items, puts the number somewhere closer to $100 trillion or more than 5 times the official figure. This equates to a debt-to-GDP ratio of over 500%, not the 100% charted below.

Takeaway: The total level of debt and the debt-to-GDP ratio have both increased substantially in the past two years. This is bullish for gold, as precious metals have a positive correlation to total debt levels.

#2 – Inept Government and Partisan Bickering

The fight over the budget and debt ceiling shut down the government for 16 days and ended up costing billions more than if the government would have remained open. Standard & Poors estimates that the 16-day government shutdown took $24 billion out of the U.S. economy, and reduced projected fourth-quarter GDP growth from 3 percent to 2.4 percent. Not only that, but it tarnished the image of U.S. financial strength and has many people worldwide questioning how the United States will continue to pay its bills. These shenanigans also led Fitch to put the U.S. on “rating watch negative” and the Chinese ratings firm, Dagong, formally downgraded its rating of the US from A to A-.

Both sides of the political aisle continue to engage in deficit spending and neither side seems serious about addressing the debt and deficit. Sadly, my guess is that they will never voluntarily reduce spending and will have to be forced to do so via default or other events. The more they shine a light on the fiscal weakness of the U.S., the faster other nations dump U.S. debt and the sooner we will see the inevitable ratings downgrade and debt default (official or via hyperinflation).

Takeaway: The Western political system is broken and the idiots running the U.S. government severely damaged government credibility and brought the country dangerously close to a technical default. They haven’t made any serious effort to balance the budget and their “solution” only kicks the can down the road for a few more months. Look for more of the same in the near future, which will further erode the creditworthiness of the U.S. government and faith in the U.S. dollar. This increases the bullish outlook for gold.

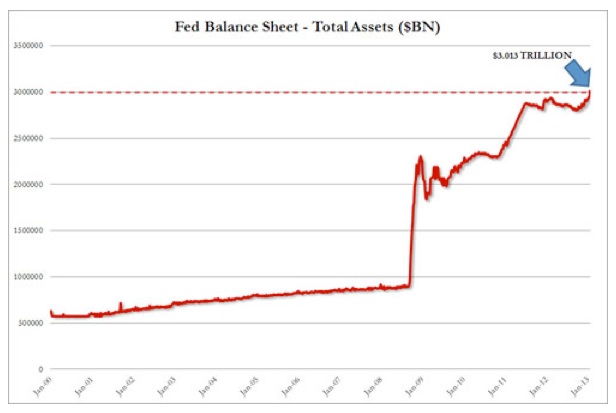

#3 – QE to Infinity Confirmed, as FED Balance Sheet Explodes

At Gold Stock Bull, we have long been calling QE3, “QE to Infinity” and doubting that any major tapering would occur. With weak economic growth and low official inflation, the FED’s dual mandates would dictate more stimulus, not less. Just weeks ago there was a consensus for tapering in September. Now, analysts are talking about March of 2014 at the earliest. My expectation is that they will change the QE program, maybe give it a different name, but the end result will always be a net increase in stimulus efforts.

The FED’s balance sheet has already increased from $869 billion in August of 2007 to $3.8 trillion today! The nomination of Janet Yellen as FED chief adds gasoline to the fire, as she is expected to be at least as accommodative as her predecessor and potentially much looser with the printing press. Helicopter Yellen?

Takeaway: The economy is addicted to QE and reliant on central bank stimulus to stay afloat. The world now understands that the FED cannot end the bond-buying program and has no intention of doing so anytime soon. If anything, we are likely to see increased quantitative easing in the future, just as a drug addict must up their dosage in order to have the same impact. This monetization of debt increases the bullish outlook on gold, as the gold price has historically trended higher along with the FED balance sheet.

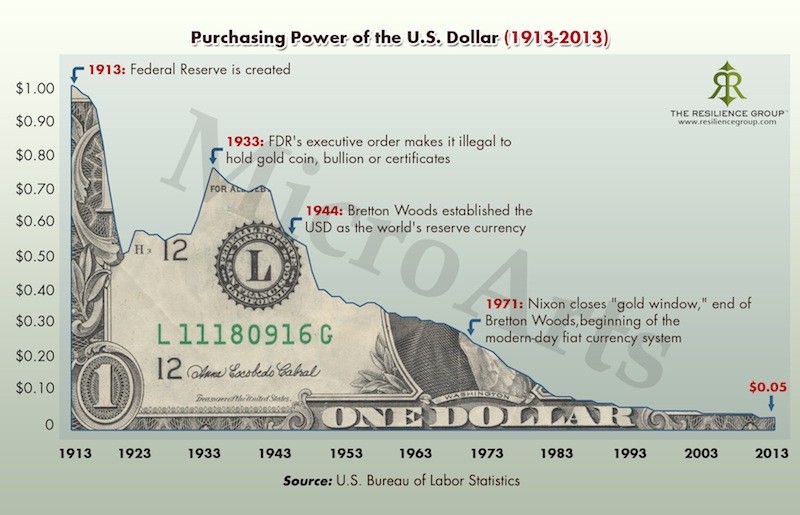

#4 – Dollar Losing Status as World Reserve Currency

The exorbitant privilege of being able to print the world reserve currency is coming to end. “It is perhaps a good time for the befuddled world to start considering building a de-Americanized world,” said a statement on Monday by Xinhua, the state news agency of China — which holds some $1.3 trillion in Treasury bonds.

“The United States will inevitably lose its reserve currency monopoly,” wrote economists Hélène Rey of the London Business School, Pierre-Olivier Gourinchas of the University of California, Berkeley, and Emmanuel Farhi of Harvard University. “It can only be a matter of time before the world becomes multipolar.” The IMF echoed this sentiment, stating how “reserves concentration in the government debt of one country introduces idiosyncratic risks to the international monetary system.”

Several nations now have bi-lateral trade agreements that bypass the dollar. China has made arrangements to swap Yuan’s for for local currencies with Japan, Russia, Australia, Iceland, South Korea, Malaysia, Brazil, India and South Africa. The BRICS nations are emerging as a powerful economic force and they are intent on conducting affairs without use of the U.S. dollar. The growing rift with Saudi Arabia also threatens the petrodollar.

Oil-rich countries that have attempted to sell their oil in currencies other than dollars include Iraq and Libya, both bombed into submission. Iran is now trading oil for gold, bypassing the U.S. petrodollar. This is likely the real reason they are now in the crosshairs of the U.S. military. Syria is seen as a stepping stone to attacking Iran, but widespread opposition from ally countries and citizens alike stopped the recent war momentum.

As the influence of the petrol-dollar continue to wane, so too will the power of the U.S. dollar as the world reserve currency. Without the ability to deficit spend and export our inflation, it will come home to roost and the dollar will suffer or even collapse as have other debt-ridden fiat currencies throughout history.

Takeaway: The dollar historically has an inverse relationship to gold. As the dollar continues to lose its role as world reserve currency and its purchasing power declines, the gold price will move higher. Mike Maloney and other analysts have calculated that the gold price needs to climb past $15,000 per ounce to account for all of the paper dollars that exist today. As more and more money is printed and debt is monetized, this target price only increases.

#5 – Global Race to Debase

It is not only the U.S. central bank that is printing money with wreckless abandon. Around the globe, central banks are trying to remain competitive in foreign trade by debasing their currency in line with the dollar. No countries are willing to admit it, but the currency war is on. As the competition heats up, they will no doubt overstep in their push to print money. This will translate into higher gold prices worldwide, measured across multiple currencies.

Takeaway: The race to debase has only intensified in the past few years, as evidenced by new stimulus programs in Europe and Abenomics in Japan. Put simply, the more fiat money that is created in this currency war, the higher the price of gold and other commodities will climb.

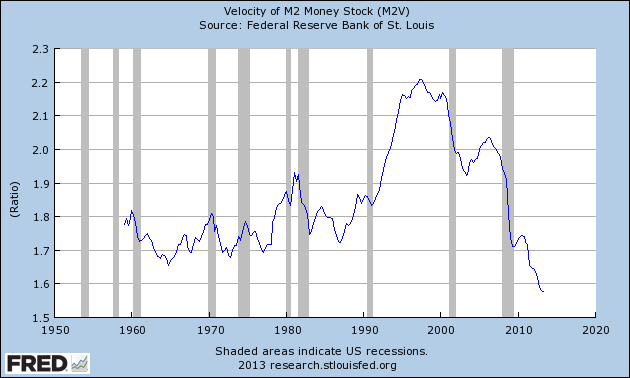

#6 – Inflation Will Pick Up as Velocity of Money Accelerates

Up until this point, a large portion of the new money printed since the financial crisis has been parked with the banks or as excess reserves with the FED. Banks are reluctant to lend and corporations are also hoarding cash. Individuals are consuming less, tightening their budgets amidst high unemployment and stagnant wages and paying down debt. This means that money has not been circulating throughout the economy at a very fast pace. The stimulus has disproportionately benefited banks and the wealthiest people in society, doing little for the middle class that continues to get squeezed.

To get money flowing, future stimulus efforts must be focused on tax breaks or refunds for the working class, who are more likely to spend that money into the economy than the rich that aren’t living near the margin. With unemployment higher than desired and official inflation lower than desired, I think we will see Yellen and the FED focus more on consumer stimulus now that the banks finances have been shored up. This will lead to a sharp increase in the velocity of money and when multiplied by all of the money created in the last few years, it could lead to high inflation or even hyperinflation if the FED fails to soak up the excess liquidity in time.

Takeaway: An increase in the inflation rate, driven by an increase in the velocity of money, will be very bullish for gold.

#7 – Diversification of Price Discovery and Decreased Power to Manipulate Commodity Markets

With the rising power and influence of the East, we are seeing the centers of global finance reposition. These include the Shanghai Exchange and Pan Asian Exchange, where an increasing amount of physical gold and silver are being traded. If you believe the COMEX and London Bullion Market Association (LBMA) are helping to manipulate the prices of precious metals, it will be welcomed news to see new exchanges emerge that can provide alternative price discovery.

Takeaway: The diversification of price discovery in the gold market will lessen the ability of Western powers to manipulate prices. As this trend plays out, the artificial downward pressure on prices should be removed and allow precious metals to more accurately reflect the fundamental conditions around them. If GATA and others are correct about the degree of manipulation, any diminishing of this manipulative ability will be very bullish for gold.

#8 – Increasing Physical Demand Worldwide, Including Central Bank Demand

Consumer demand for gold was up 53% in Q2 according to the WGC. Total bar and coin demand set a new quarterly record, exceeding 500 tonnes for the first time and U.S. silver eagles sales are on pace for a record year. Central banks continue buying at a frenzied pace, adding 534.6 metric tons to reserves in 2012, the most in almost a half century. And these are just the reported purchases. China, Russia and other nations are thought to be buying discretely via third parties.

Furthermore, there is a growing movement of gold repartriation around the globe. First Venezuela, now Germany, the Netherlands, Switzerland, Poland, Romania, Finland, Ecuador and others are demanding their gold back from the FED and Western financial institutions.

Takeaway: Increasing demand, particularly by those taking physical delivery, will also serve to lessen the impact of manipulation in the markets. Investors are increasingly losing faith in paper gold and as the real metal is removed from the market, the lower supply will put upward pressure on prices and force exchanges to settle in cash.

#9 – Stagnant or Declining Supply

Total gold supply contracted 6% during the latest quarter to 1,025.5 tonnes, driven by a sharp drop in recycling activity. There have been huge outflows from COMEX and Shanghai stocks. With prices at or near the cost of production, several mining operations have been suspended or shuttered, which will further restrict supply. Mints in the U.S. and Canada have resorted to rationing supplies of their popular bullion coins, a further signs of tightening supplies.

Takeaway: Economics 101 dictates that increasing demand and declining supply leads to higher prices.

#10 – Tiny Size of Gold Market versus Stock or Bond Market Will Provide Leverage

It has been estimated that all of the gold ever refined would form a single cube 20 m (66 ft) on a side. This cube would contain around 5.5 billion ounces of gold and be worth roughly $7 trillion. By comparison, the world stock market is estimated at $50 trillion and the bond market at around $100 trillion. So, it would only take a small percentage of money moving from these larger markets into the gold market to overwhelm available supply and send prices substantially higher.

Takeaway: Participation in the gold market is at very low levels, estimated at around 1% to 2%. Even a small rise to 4% or 5% participation, would cause demand to spike and send prices significantly higher. Sentiment is extremely bearish at the current time and can only become more bullish from here.

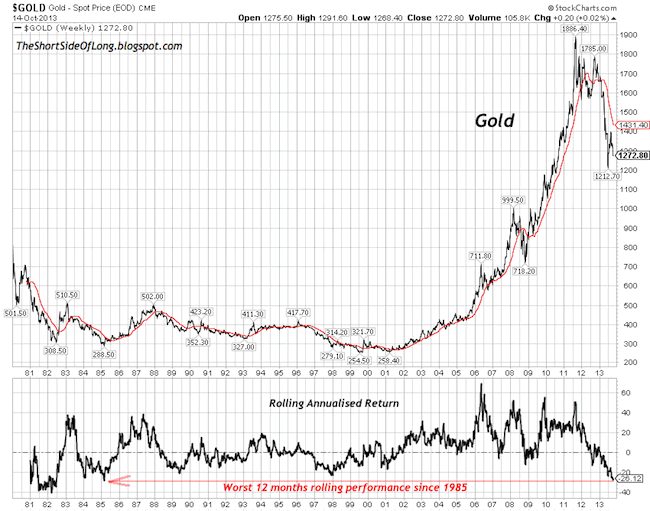

#11 – Gold Most Oversold Since 1985

According to at least one technical indicator courtesy of “The short side of long”, gold bullion is the most oversold it has been since 1985. The indicator is the simple yearly rolling performance, also known as the 52 week rate of change. This is the performance of an asset over the last 12 months and gold is having one of the worst performances ever.

Gold stocks are also severely oversold, both in absolute terms and relative to the underlying metals. The gold miners index (GDX) has fallen more than 50% in the past year. Looking at gold stocks relative to gold, we can see they are the most oversold they have been since the start of this 12-year bull market.

Takeaway: Extreme conditions, whether oversold or overbought, do not tend to last very long. The market runs through cycles and seeks a return to equilibrium after hitting extremes. A move away from the current severe oversold levels would push precious metals much higher while generating significant leveraged gains for mining stocks. Ripe pickings abound.

#12 – Prices Have Dropped to the All-In Cost of Production, Which Typically Provides Support

It is not often that a commodity will drop to a price below the cost of production. Can you think of many things that you can buy for less than it costs to produce it? At current price levels, many miners are being forced to suspend operations as their all-in sustaining cost to produce an ounce of gold makes the operation unprofitable. Even some of the best miners are just barely squeezing out quarterly earnings, propelled by increasing production and cost controls. Supply levels have already been impacted, but any further drop in the price of gold and silver will lead to additional mines shuttering operations. As these mines stop producing and supplies drop, prices will rise to reflect this change.

Takeaway: As costs rise, so do prices. Either precious metals will climb to levels where miners are profitable or they will stop mining and destroy supply levels. The price can certainly drop below the cost of production for a short time period, but it is not likely to last. This all-in sustaining cost usually proves to be a solid floor during corrections, so the downside is limited at this juncture.

Conclusion

All of the fundamental reasons to own gold and silver have only strengthened in the past two years. Against this backdrop, the sharp correction in prices over the past two years makes little sense. Whether or not the price is being surreptitiously suppressed is not the important point. The bottom line is that prices are not reflective of the fundamental economic conditions in the world today and no matter why this is occurring, it is not likely to last long. So, I would suggest that investors welcome the manipulation and take advantage of the fire sale prices while they last.

As the gold price climbs back towards its inflation-adjusted high of $2,400, Shadowstats target of $8,000 or Mike Maloney target of $15,000, we will look back at this current correction as nothing more than a bump in the road and excellent buying opportunity.

However, not all mining stocks are created equally. I have focused my research on best-in-breed companies with low all-in cash costs, rapidly increasing production, politically-stable jurisdictions and management with a proven track record. I also like the royalty and streaming companies that have been able to weather this storm fairly well. Their business model provides for limited downside risk and huge upside potential as their partner mines come online.

To view the Gold Stock Bull portfolio, receive our highly-rated newsletter and get regular updates on the stocks that we believe will generate the greatest gains during this next upleg, click here to sign up for the Premium Membership.

By Jason Hamlin

Jason Hamlin is the founder of Gold Stock Bull and publishes a monthly contrarian newsletter that contains in-depth research into the markets with a focus on finding undervalued gold and silver mining companies. The Premium Membership includes the newsletter, real-time access to the model portfolio and email trade alerts whenever Jason is buying or selling. You can try it for just $35/month by clicking here.

Copyright © 2013 Gold Stock Bull - All Rights Reserved

All ideas, opinions, and/or forecasts, expressed or implied herein, are for informational purposes only and should not be construed as a recommendation to invest, trade, and/or speculate in the markets. Any investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied herein, are committed at your own risk, financial or otherwise. The information on this site has been prepared without regard to any particular investor’s investment objectives, financial situation, and needs. Accordingly, investors should not act on any information on this site without obtaining specific advice from their financial advisor. Past performance is no guarantee of future results.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.