Could A Compound Debt Interest Rate Payments Wildfire Threaten US Solvency?

Interest-Rates / US Interest Rates Jan 23, 2014 - 06:11 PM GMTBy: Dan_Amerman

For the first time since the end of World War II, the total US federal debt now equals 100% of the size the US economy. But while that is obviously a situation of great concern, it may not be the worst of the danger.

For the first time since the end of World War II, the total US federal debt now equals 100% of the size the US economy. But while that is obviously a situation of great concern, it may not be the worst of the danger.

Instead, the greatest debt-related threat to the solvency of the United States government and the value of the dollar could be the fact that the US isn't actually making any net principal or interest payments on its debt.

That is, the US government is borrowing money to make the interest payments, even as it borrows to roll over the principal payments – even as it borrows still more to fund the general spending which is in excess of taxes collected.

This creates the risk of a potential compounding and acceleration of interest payments on that debt.

Now government debt in an environment of ongoing massive deficits doesn't work like mortgages or other consumer debt that most people are familiar with. If interest rates rise, then the money needed to make interest payments will naturally rise, and the annual deficit must increase as well.

However, as shown in the graph above, the heart of the risk is that if interest rates were to rise substantially, there is an acceleration effect that kicks in. At higher interest-rate levels, the cruel mathematics of borrowing to make interest payments on debt – which was itself borrowed to make interest payments on debt – can flash out of control with shocking speed, much like a wildfire in a tinder-dry canyon.

Instead of taking six years for the government to reach $22 trillion in debt outstanding, it could happen in two years. And instead of taking twenty years to reach $35 trillion in debt outstanding – it could happen in about a quarter of the time, or five and a half years.

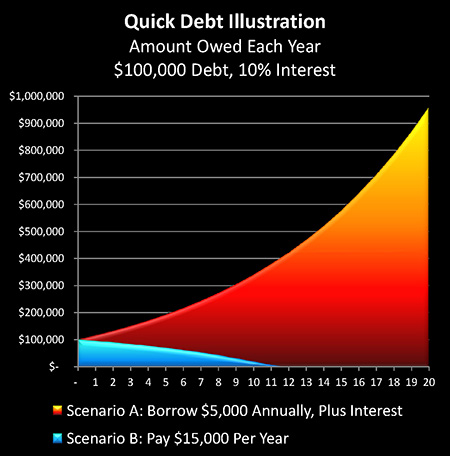

Quick Debt Illustration

When a government can't pay its basic bills – let alone the interest payments on outstanding debt – then the debt works in a very different way than most of us are familiar with as individuals.

For consumer debt, the required payments are usually higher than the interest charged, so there is money available to pay down principal each month.

This common situation is illustrated with Scenario B in the graph above, using the round numbers of a $100,000 debt, a 10% interest rate, and a borrower making a fixed payment of $15,000 per year.

After paying $10,000 in interest, $5,000 is available to pay down debt in the first year, which reduces the debt to $95,000, which lowers the interest that is due to $9,500, which frees up $500, which means $5,500 can be paid down in the second year, This continues until the debt is extinguished in only 11 years, rather than the 20 years it would take with constant $5,000 principal payments.

However, this is not the situation of the United States government, which currently is paying neither principal nor interest out of its tax revenues, but is instead borrowing the money to make interest payments, as well as borrowing to roll over the principal payments, on top of borrowing to fund additional spending every year.

If the average person were to behave like the United States government, then they would find themselves in Scenario A above. They would borrow the $10,000 to pay their first year's interest, and they would borrow another $5,000 beyond that to fund their lifestyle.

Which means they would end the first year not $100,000 in debt – but $115,000 in debt. This higher debt level adds $1,150 to their interest due, meaning they now have to borrow $11,500 to meet interest payments in the second year, on top of the $5,000 that's helping to fund their lifestyle.

Debts aren't paid down when interest payments are borrowed, but rather an opposite form of mathematics takes hold – that of compounding. As shown in the illustration above, at the end of 20 years, this unfortunate individual's debt would have compounded to a total of $951,125.

At a 10% interest rate, this means they would need to borrow an additional $95,912 in the next year alone, just to continue to make interest payments, including:

1) $10,000 in interest due on the original $100,000;

2) $10,000 in interest due on the $100,000 borrowed over the next 20 years; and

3) $75,912 in interest due on the $759,125 borrowed to make 20 years of interest payments.

Like a major wildfire, when debt begins to compound out of control it can create its own weather system, in which the dominant force can quickly become not the original debt, nor the additional borrowings to fund normal spending, but the payment of interest on money borrowed to make interest payments. Which means that the interest rate paid on borrowings can quickly become more important than the spending itself, or even the starting amount of debt.

This is indeed the case with the United States government, meaning that on top of the well-known issues with annual deficits and total debt outstanding, there is a third closely related but distinctly different threat, which is the far more acute exposure to the risk of rising interest rates than is generally recognized.

Simply stated, debtors who must borrow the money to make their interest payments have a far greater exposure to rising interest rates over time, than those who make interest payments from ongoing cash flow.

To better understand, we'll explore the issue by applying three interest rate scenarios to the US government's debt and deficits. But first, we need to consider what has kept this debt compounding out of the headlines so far.

The Hidden Agenda Behind Quantitative Easing

Arguably, the current financial viability of the United States, and its protection against interest payment firestorms accelerating out of control, is based upon the process of quantitative easing that the Federal Reserve has been engaged in since 2008.

Quantitative easing is the creation of massive sums of money by the tens of billions of dollars every month out of the nothingness, that are not spent by the government in the general economy – but are instead currently used to purchase bonds and mortgage-backed securities, for the purpose of lowering interest rates.

It is the purchase of those bonds and mortgage-backed securities that has kept interest rates so low for US government borrowings, as well as supported the real estate market through making housing much more affordable for home buyers.

So while other reasons are given to the media and the public in terms of why quantitative easing exists, what needs to be understood is that if it didn't exist, and interest rates were to rise to true market levels – this could set off an acceleration in the compounding of interest payments by the federal government that at current debt levels could become completely impossible to meet.

The Current Situation

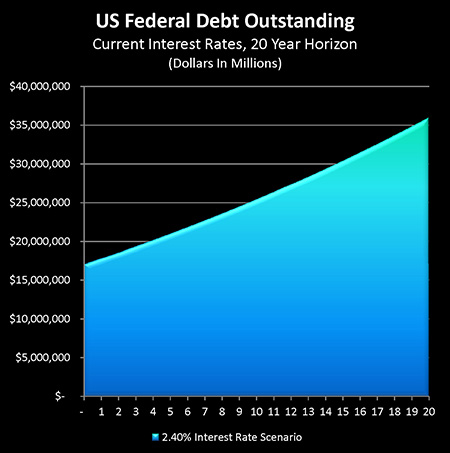

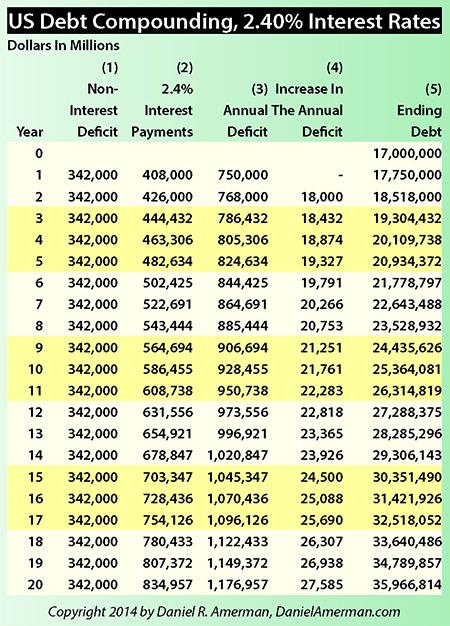

As shown in column (5) of the chart above, our starting situation is that the US government has about $17 trillion in debt officially outstanding. The true total debt which includes unfunded obligations is a separate matter, but for now we'll stick just to what's officially on the books.

According to the United States Treasury Department, the average interest rate on all outstanding US federal government debt is about 2.40%. As shown in column (2), when we multiply that interest rate times the rounded $17 trillion in debt outstanding, we get an annual interest payment of about $408 billion per year (this shifts a little bit with monthly changes in interest rates).

As shown in column (3), a round number for the current US deficit is about $750 billion per year, with the reduction from previous years being the result of the massive tax increase that took effect at the end of 2012.

That annual deficit has two components: general spending that isn't supported by taxes, and interest payments on the debt, which are also not supported by taxes. For our exploration it is essential that we split the two components. So we take the $750 billion total deficit in column (3), we subtract the $408 billion in interest payments shown in column (2), and we get the non-interest annual deficit of $342 billion in column (1).

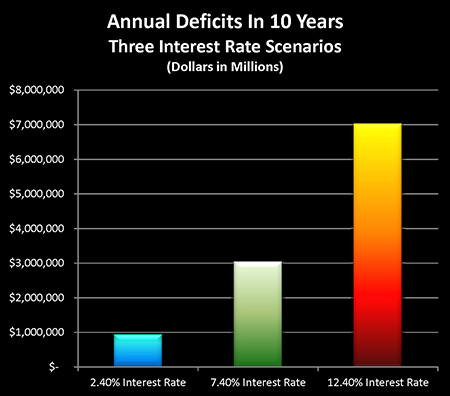

Increasing Interest Payments

As can be seen with this scenario, with nothing else changing, the federal deficit would compound to be over $20 trillion in four years, it would be over $25 trillion in 10 years, it would reach $30 trillion in 14 years, and after 20 years we would have about $36 trillion in debt outstanding.

That is such a fantastic sum as to be almost incomprehensible. To put it in perhaps more personal terms, it represents approximately $370,000 per current above-poverty line US household.

But what is little examined and remarked upon is that even this situation – impossible as it is – depends upon extremely and artificially low interest rates, that are themselves currently based on the massive creation of new money by the Federal Reserve in the form of quantitative easing.

Instead, we are repeatedly told that things are getting back to normal, and the Federal Reserve will be backing off this very temporary technical intervention that none of us should really worry about.

So let's now consider what would happen if we returned to let's say a more typical level of interest rates that we have seen over the last 30 to 40 years.

Government Deficits With Higher Interest Rates

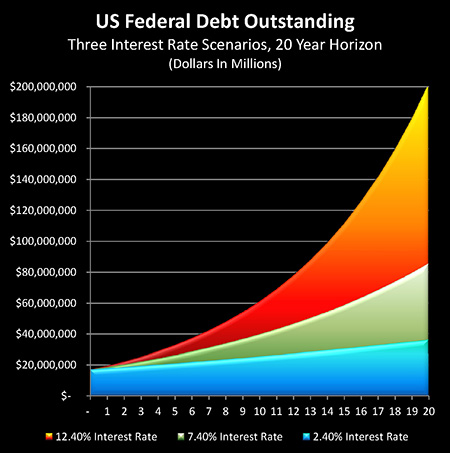

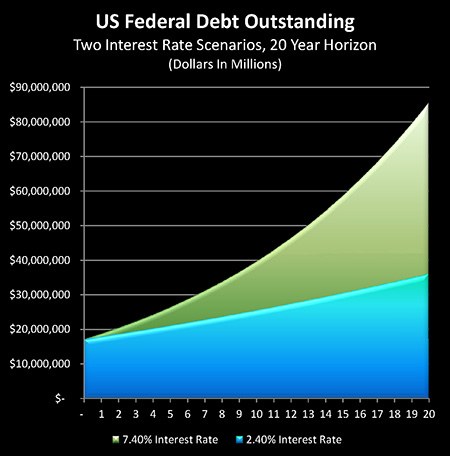

The graph and chart below explores what happens to US federal government deficits over time if interest rates were to return to what could be called a more historically normal level, over the period from the mid-1970s to the end of the 1990s. (There is a crucial reason why we are not using interest rates from the 1950s and 1960s, which we will visit later on.)

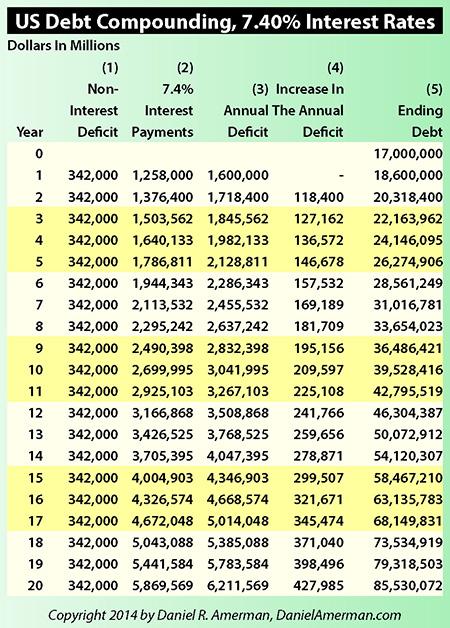

The chart is identical to the previous chart, with one exception – we assume interest rates are 5% higher, so the average interest paid on federal debt outstanding becomes 7.40% instead of 2.40%.

At this higher rate, annual interest payments on $17 trillion in debt jump from $408 billion per year to $1.3 trillion per year (column 2). That is a tripling of the annual interest cost.

When we include the same non-interest payment deficit of $342 billion per year, we now have an annual increase in the deficit of $1.6 trillion, meaning we have just doubled the rate of increase in the overall deficit.

Now mathematically, this quickly has an extraordinary effect.

It means that instead of taking four years to reach $20 trillion in debt outstanding, it only takes two years.

It means that instead of ten years to go past $25 trillion in debt outstanding, it only takes five years. And to reach our total of approximately $36 trillion in federal debt outstanding no longer takes twenty years, but takes only nine years.

This is how compound interest works.

Now some people consider "compound interest" to be something close to magic when it comes to investing money over the long term, and one could even arguably say that the very heart of conventional financial planning is all about the mathematics of compound interest in one form or another. (Or at least this is true when we look at things on a pre-inflation and pre-tax basis.)

As shown in the usual investment projections, we take remarkably small sums of money, preferably starting 20, 30, 40 years in advance, and after some years go by it is the earnings on our earnings that begin to exceed our annual contributions, and then things really start to take off.

However, in the case of a debtor who must borrow to fund the interest payments on their debt, there is a dark side to compound interest as well.

And when we look at the US government as this debtor, and we return to what has been reasonably common interest rate levels over the decades when there weren't massive governmental interventions going on, then we see that this very quickly creates an explosive and impossible situation for the US government.

(It should be noted that there are two major simplifying assumptions with this analysis.

One is that we are treating the interest rates on all US debt as increasing simultaneously. In practice of course, there is a term structure with US debt outstanding, with some of it being very short term, while some is medium term and some is long term.

Debt obligations with fixed rates and longer terms will keep their current low interest rates until the time comes to roll them over.

So if interest rates were to jump to substantially higher levels, this would actually take a number of years to fully reach the level shown in this analysis. That said, due to the potency of the mathematics, the compounding of short-term debt interest payments alone would still be enough to radically bring forward the date at which debt levels become truly unmanageable.

However, of more importance, as previously mentioned, we're not including the rapid increases in non-interest payment deficits over the years, as 4 million Baby Boomers per year reach retirement age and become eligible for Social Security and Medicare. When we take that into account, then the actual picture is worse than what is shown here.)

Much Higher Interest Rates

What would happen if we had true market interest rates for an effectively insolvent government?

When we talk about $17 trillion in federal debt outstanding, what must first be understood is that this sum is based upon the miracles of governmental accounting. The rules are very much written in the favor of presenting numbers that look good when it comes to election time – even if the use of governmental accounting by private corporations or individuals could in fact relatively quickly lead to prison time.

So when we expand our view of federal debt outstanding to take a private sector approach, then as has been reasonably well-established in late 2012 by Archer and Cox, the former head of the House Ways and Means Committee and former head of the Securities and Exchange Commission respectively: based on the numbers in the Medicare trustees report, if we include the unfunded obligations of expected future payments for Social Security and Medicare that are not covered by expected tax revenues in the future, then we have an additional $70 trillion in debt outstanding that is "off the books".

Add that to the official $17 trillion in debt outstanding, and we have a total of $87 trillion in real unfunded obligations outstanding.

Fortunately, interest payments only have to be made on the $17 trillion in official debt (although for those financially-oriented, the compounding as present value becomes future value in each year is its own form of compound interest, which radically increases the real annual deficit).

In other words, the US government is effectively insolvent, absent some major changes. Which is exactly why, as my readers know well, my consistent position has been that we need to anticipate that there will be major changes.

Now let's make a crucial assumption for the sake of exploration, and say that we move to a true free market in interest rates in the future, with no governmental interventions. This would likely mean a substantially higher market interest rate because let's face it, inflation is the only way that these debt levels can be dealt with.

And if we're looking at increased inflation in the world, and a debtor nation that realistically can't pay its bills other than with inflation, then we should expect even higher free market interest rates.

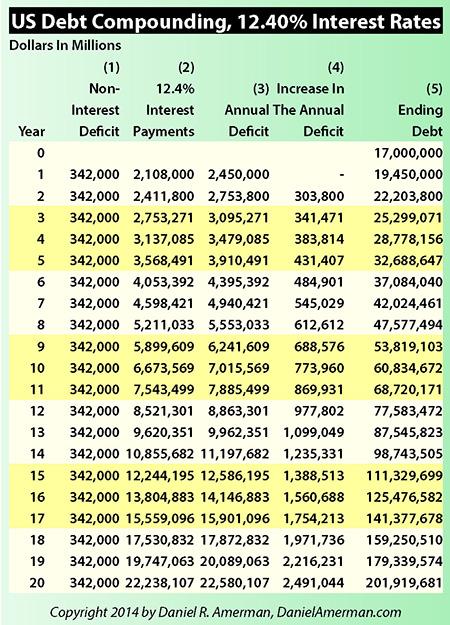

What is examined in the graph and chart above is what the debt and deficit compounding situation would look like if we had interest rates return to more like what they were at the peak of the previous (and lesser) financial crisis during the late 1970s and early 1980s.

Again the chart is identical, except this time we have moved the interest rate up a full 10% to 12.40%.

Now interest rates in the first year are no longer $408 billion, but five times higher at a level of $2.1 trillion (column 2). Add in our official non-interest payment deficit, and we're at almost a $2.5 trillion annual deficit level (column 3).

That means that we reach the $25 trillion debt outstanding mark (column 5) not in ten years, as with current interest rates, and not in five years, as with a 5% increase interest rates – but we reach it in three years.

We are $36 trillion in debt not in twenty years or nine years, but in six years. By the time ten years is reached, the US government becomes $61 trillion in debt.

And by the time twenty years out is reached, the US government would be $202 trillion in debt.

What this shows is that for a debtor nation such as the United States, which has an amount of debt outstanding that's equal to the size of the national economy – an increase in interest rates can very quickly become an existential event.

Now a government can have high debt levels. And a government can have high interest rates on its debt. But a government which must borrow to make interest payments, can't combine both high debt levels and high interest rates for more than a relatively brief period of time without setting off an explosive compounding of interest payments and debt.

So then, why do we have quantitative easing in the United States?

It's because forcing artificially-low interest rates on the markets is crucial for a government trying to meet its debt payments and reduce its reported annual deficit over the coming years.

Now if the federal government judges that interest rates can be restrained in other ways, whether through a compliant market, or by returning to explicit statutory interest-rate controls as we've seen in previous decades, this does allow for the ability to back off on the quantitative easing, or even end it.

But something to always keep in mind when looking at mainstream financial analysis, or at Federal Reserve press releases, is how close to the edge the United States is walking right now when it comes to interest-rate payments. If a return to market levels substantially increases interest rates – then we can anticipate that there will be no return to market levels.

We are truly walking the edge of a precipice when it comes to the amount of federal debt outstanding, and interest-rate levels.

The Heart Of The Conflagration

The 2nd half of this article explores:

1) The acceleration of debt, and how higher interest rates could be much more dangerous - and in a shorter time - than is commonly recognized;

2) The extraordinary information value when it comes to tapers, quantitative easing, and other governmental interventions; and

3) How the government's need to avoid the compound interest trap could lead to investors being cheated out of market yields for years and possibly decades to come.

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

© 2014 Copyright Dan Amerman - All Rights Reserved

Disclaimer: This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.