Alan Greenspan: The Age of Hubris (and the long road back)

Economics / Money Supply Apr 27, 2008 - 08:56 AM GMTBy: Clif_Droke

Hubris is an amazing thing. It causes those infected by it to justify actions that would normally be indefensible.

Hubris is an amazing thing. It causes those infected by it to justify actions that would normally be indefensible.

Take Alan Greenspan, for instance. He recently penned an editorial in the Financial Times claiming that under his leadership, the Federal Reserve is blameless on the property bubble. No way could the Greenspan Fed have foreseen the devastation its money policy of 2001-2006 would inflict on the housing market and the larger economy. “It wasn't my fault. Don't blame me,” claims Alan.

He even suggested that the “core of the subprime problem” lies with the “misjudgments” of the investment community. Blame the securitizers. Blame investors. But don't blame the “maestro.”

The ironic twist to this self-justifying piece is that many financial commentators seemed to fall for it. Martin Wolf, writing in the Financial Times, wrote an editorial in response to Greenspan's claim of innocence entitled, “Why Greenspan does not bear most of the blame.” In it he opined, “U.S. monetary policy cannot be responsible for all these bubbles.” Instead of blaming Greenspan, he suggests that we look elsewhere. Try blaming the combination of low long-term real interest rates; the global savings glut; the lengthy experience of economic stability; and above all, “the liberalization of mortgage finance in many countries.” Blame any or all of these factors. But don't blame Greenspan!

The financial press seems committed to defending the monetary policy blunders of their beloved “maestro.” Not long ago, the Financial Times published a prime example of the lionizing spirit the press has adopted toward the former Fed chief. Alan Greenspan's picture was splashed prominently across the front page along with the headline, "Greenspan alert on homes,” in reference to the danger confronting the housing market.

Alert on homes? This statement hardly needs elucidation. It speaks volumes about the sheer arrogance and utter audacity of a man who shares much of the blame for creating the mortgage mess through his ultra volatile monetary policy.

Wasn't Greenspan the one who, as Fed chairman, advised home buyers to take out Adjustable Rate Mortgages...just as interest rates were about to turn up? And wasn't he the one who helped create the housing balloon in the first place by lowering Fed fund rates too low during 2001-2003 and overdoing the pump priming? Yet he has the temerity to proclaim, belatedly, that housing prices were in a "bubble" and that there could still be a "double-digit" fall in property values before all is said and done.

I've given it some thought and I think you'll agree the word that best describes Greenspan's reign as Fed chairman is “rollercoaster.” This refers to his on again, off again money supply policy during his tenure. If long-time Fed Chairman William McChesney Martin was famous for his “leaning into the wind” monetary policy, then Greenspan was notorious for going too far at both extremes of the business cycle.

Indeed, with Greenspan at the helm, it often felt like we were riding an economic rollercoaster. Let's look at the final 10 years of his chairmanship for an example. First came the rise of stock prices to vertiginous heights in the mid-to-late 1990s with his extremely loose money supply policy. This led to the Internet stock bubble and coincided with the strong dollar policy of then Treasury Secretary Robert Rubin. Then the old “maestro” slammed on the money supply brakes in 1999, which helped catalyze the tech wreck and Internet stock crash, followed by a serious bear market and economic recession into 2001.

Realizing his blunder, Greenspan saw to it that the economy received a massive liquidity injection in 2001-2003. This ended the recession and eventually lifted the stock market out of the doldrums. As was his tendency, however, the Greenspan Fed went too far and let interest rates drop too low, which encouraged speculation in real estate. The rest is recent history which bears no repeating.

There is one aspect to the story that hasn't been emphasized by most pundits. While everyone is quick to point out Greenspan's error in letting credit expand too rapidly following the 2000-2001 recession, the fatal blunder which sparked the credit conflagration is rarely mentioned. It was the rapid reversal of his easy money policy in 2004 which started the economy on its road to starvation. The rate hikes which followed every step of the way helped seal the doom of the housing bubble. Once again, the rollercoaster ways of Alan Greenspan inflicted most of the damage and the economy is still feeling the after effects.

In the previously mentioned issue of the Financial Times there is yet another article featuring Greenspan's take on the Fed's decision to publish U.S. inflation targets. "I just don't see any benefits to an institution such as the Federal Reserve saying we will adhere to such-and-such a policy," he said. Imagine that, the Fed actually adhering to a policy!

The problem is that when Greenspan was Fed chairman he had no policy to adhere to and that's why his monetary "policy" was all over the place. He created a tumultuous rollercoaster ride for the financial markets and the economy, amplifying the business cycle many times worse than it had to be.

Yet everyone from the ivory towers of academia to the newsrooms of the mainstream press seems to worship and adore this man. They've conveniently forgotten the hardships his tenure as Fed chairman caused for many (and is still causing). All they seem to remember is the late '90s super bull market and white hot economy, a brief spark in the 20-year reign of Greenspan that did little to erase the major policy blunders of his other years as chairman.

Last year Greenspan embarked on a major publicity campaign to promote his autobiography. At a press gathering he had the gall to state, "I am coming to the conclusion that bubbles are inevitable. Human beings cannot avoid them...They cannot learn."

Spoken like a true megalomaniac. It was Greenspan's irrational, rollercoaster money policy that contributed to more bubbles being created – and later popped – than any other Fed chairman in history. How fitting that he entitled his self-aggrandizing tome, “The Age of Turbulence.”

So much for Mr. Greenspan and his Age of Hubris. Thankfully, his chairmanship is now a thing of the past and we no longer have to ride the rollercoaster controlled by ol' Irrational Exuberance. Now there is a new chairman at the helm, one who is said to be opposed to many of the same ideologies that Greenspan was enslaved to. Is there actually hope then that for the first time in nearly two decades, the U.S. economy can step off the rollercoaster created by Greenspan and onto a smoother, less volatile path?

In contrast to Greenspan, Fed Chairman Bernanke believes that money supply, and not interest rates, hold the key to the economy (a tenable position to be sure). According to Adrian Van Eck, over the course of his career as an economics professor and central banker, he has enunciated that “he does not believe in a slow, stretched-out process of bringing new life to the economy – as marked by the many terms of previous Chairman Alan Greenspan. Instead, Bernanke advocates a policy of hitting hard and moving very fast.”

That's just what the doctor ordered to resuscitate the U.S. economy from the somnambulant state induced by Greenspan before he left. Bernanke is known as “Helicopter Ben” for being an advocate of rapid monetary response to financial crises.

In a recent commentary we looked at the dramatic improvement in the Treasury yield curve, which portends recovery. There is some lag time between the improving yield curve and economic performance, but probably by mid-summer we'll be seeing some noticeable improvements in the economy. We should see the beginning of recovery in the consumer economy next month when the checks from the $160 billion stimulus package passed by Congress will begin to arrive in May. The strongly positive slope of the yield curve guarantees that improving liquidity will eventually translate into an improved economic outlook.

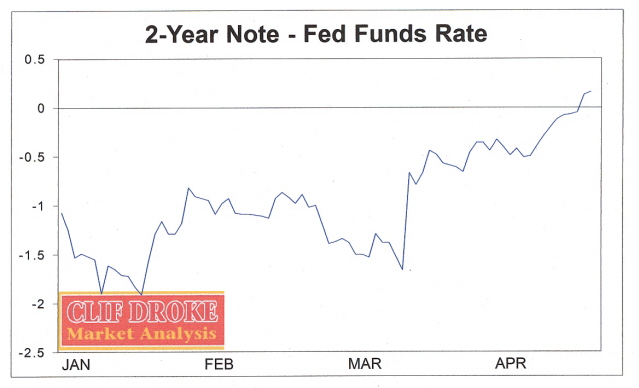

We also previously examined the relationship between the yield on the 2-year T-Note and the Fed funds rate. I'm pleased to report that as of April 24, the 2-year yield pushed high enough to exceed the Fed Funds Target Rate for the first time in over two years! This is a very positive event for the financial sector as well as the economy, for it indicates that liquidity will be showing some strong improvement from here and will allow financial institutions to take advantage of it after being hurt by the crisis in confidence. Check out the chart below, which shows the line going into positive territory for the first time since 2006.

Another point worth considering as we look at the prospects for economic recovery is the huge increases in money supply in recent months. Donald Rowe, in the April issue of The Wall Street Digest, writes, “In addition to the $200 billion made available to the credit markets, the Fed has aggressively increased the growth of the money supply to accelerate economic growth. Adrian Van Ecks' research indicates that the Fed has probably created approximately $400 billion in M3 money since early December. While $400 billion may seem unimpressive to you, a ten percent fractional reserve banking system will multiply that sum to $4 trillion during 2008.”

As Rowe points out, the annual GDP of the U.S. was $14 trillion 2007, therefore a $4 trillion increase in cash that passes through the banking system and into the economy in coming months will greatly facilitate the economic recovery. Quoting Rowe, “Great events always cast long shadows.”

Indeed, the road to recovery from Greenspan's “Age of Hubris” begins here.

By Clif Droke

www.clifdroke.com

Clif Droke is the editor of the three times weekly Momentum Strategies Report newsletter, published since 1997, which covers U.S. equity markets and various stock sectors, natural resources, money supply and bank credit trends, the dollar and the U.S. economy. The forecasts are made using a unique proprietary blend of analytical methods involving internal momentum and moving average systems, as well as securities lending trends. He is also the author of numerous books, including "How to Read Chart Patterns for Greater Profits." For more information visit www.clifdroke.com

Clif Droke Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.