Debunking The Velocity Myth Once And For All

Economics / Economic Theory Jun 11, 2014 - 12:20 PM GMTBy: Jeff_Berwick

Ed Bugos writes: - “Things are not what they appear to be: nor are they otherwise”

Ed Bugos writes: - “Things are not what they appear to be: nor are they otherwise”

At TDV we demonstrate this truth almost every day – in our blog, our tweets, and in our newsletters.

Just last week Jeff discussed the fallacy of GDP, comparing our lot to that of Jim Carey’s as Truman Burbank, the unaware mark in the Truman Show. In that blog, Jeff discussed one of the main problems with relying on GDP (Gross Domestic Product) as a measure of economic growth.

He reminded us of how the government manipulates this number – by inflating the money supply and massaging the price data – since GDP is basically just the sum of the monetary values of various goods (mostly consumption) adjusted for the government’s own hedonically massaged price deflator.

But that is just the tip of the iceberg.

You just can’t fit these types of things into models and equations, even if your intent was honest.

James Grant highlights the overwhelming problem neatly, “Imagine deciding which nation produces what in a global supply chain. Or correcting price for quality improvements. The mind boggles.”

Yet that still just deals with the practical aspect of the calculation.

Consider the theoretical equation for GDP: C+G+IM

I can’t tell you how many hours I used to waste going over the income accounts to make sense of the moving parts of “the economy” as a young stockbroker. Not once did I ever stop to wonder, what exactly the government (G) ADDS to the equation. I took it at face value. I’ve always known that it has no original wealth of its own, and that it cannot create wealth; it just never occurred to me in those years to question an equation that was taught to me in a formal school…sanctioned by government!

Only once I took the Rothbardian red pill could I begin to see through the fake sky painted on the ceiling. But it still takes a lot of thinking and questioning to see well beyond it.

Another problem with the GDP framework, for example, besides overweighting consumer spending relative to capital/investment spending, is that it has only two dimensions: that is, it is either growing or not. It does not allow us to distinguish between sound or lasting growth – where the pool of savings is being invested wisely in the formation of new capital that increases our productivity and real wages – and unsound growth – where savings are consumed, and part of the existing capital structure and labor is misallocated towards unprofitable ends (financed not by savings but by fractional reserves) so that a crisis and/or bust becomes inevitable when the stimulus from the monetary policy is withdrawn.

The bust allows the bad investments to clear (liquidate) and savings to replenish, and for the patterns of production and consumption to return to a sustainable balance, which essentially means reforming around society’s needs, rather than the central planners’. A boom built on the back of unsound credit is on shaky ground because actual saving does not back it. It is nothing but a consumption binge that expenses savings, and hence any lasting capital and wealth formation…i.e. things that tend to support a rising standard of living. Increasing consumption does NOT cause growth; it is a product of growth.

The paradox of savings that still haunts Krugman was solved long ago.

He just didn’t get the memo.

The entire idea of the GDP statistic is incoherent. Aggregating different goods (apples and oranges) into one homogenous two-dimensional lump of shit is no way to look at an economy full of individuals.

Likewise, there is no such thing as an average price.

These are abstract concepts, and even their creators warned of their many flaws.

GDP is really nothing but a neo-Keynesian relic created for war time planning.

And yet, many investors wait with bated breath for wall street’s estimates of the government’s figures, so they know it is safe to keep buying stocks. The figure is expanding, all is okay, government says.

I can write pages and it would still just be the tip of the iceberg.

So much of the data that money managers think is important is really not.

It takes entire careers just to figure that out.

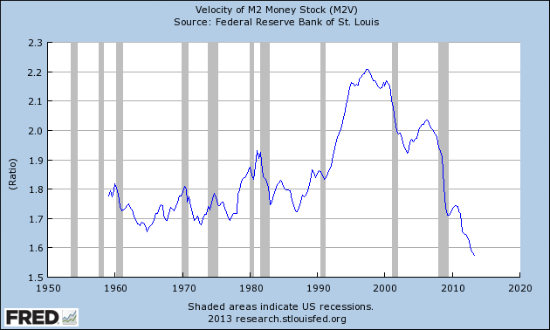

But, one of my all time biggest pet peeves in this business besides “the deflation” is the concept of “velocity”, which is not unrelated. In fact, it is thought of as part of the reason and fix for deflation.

“Velocity Of Money In The U.S. Falls To An All-Time Record Low”!!

“When an economy is healthy, there is lots of buying and selling and money tends to move around quite rapidly. Unfortunately, the U.S. economy is the exact opposite of that right now. In fact, as I will document below, the velocity of M2 has fallen to an all-time record low.

This is a very powerful indicator that we have entered a deflationary era, and the Federal Reserve has been attempting to combat this by absolutely flooding the financial system with more money. This has created some absolutely massive financial bubbles, but it has not fixed what is fundamentally wrong with our economy. On a very basic level, the amount of economic activity that we are witnessing is not anywhere near where it should be and the flow of money through our economy is very stagnant.” Click the link to see the full article

I’ve underlined the problematic or erroneous statements.

This week, in reaction to a similar analysis in Europe, the ECB decided to penalize banks for maintaining excess reserves by charging 10 basis points on any balances kept with it, incentivizing a flood of lending by the European banks. This is known as a negative interest rate policy.

It is the opposite of what the Fed has done.

The Fed is paying interest on reserves; the ECB is now charging interest.

Banking analysts believe that despite previous attempts at QE by both the ECB and the Fed, the commercial banks aren’t pyramiding on their freshly printed reserves. Instead they are sitting on them, and this is causing the central planners great pain because they want to boost spending.

The problem – which is more perceived than real in the first place – is the low velocity.

Of course, the ECB is acting as though it didn’t realize the sky was just part of the ceiling in Truman’s world. For, as you now know, “the amount” of economic activity is unimportant in the scheme of things. A healthy economy does not require an unsound bank credit expansion to stimulate it.

And interest rates are supposed to be more than just a lever that gooses lending and spending.

As Robert Murphy put it recently, "interest rates coordinate production and consumption decisions over time. They do a lot more than simply regulate how much people spend in the present." Hence, when it comes down to it, this type of policy is, on the one hand, nothing but papering over the actual problems, and on the other hand, it is one of the key contributors to the existence of those problems.

What is the Velocity of Circulation?

It is often the semi-sophisticated person to use this phrase.

In fact, even some Austrian economists will tend to use the term –though unfortunately they can’t hear me jumping up and down and screaming at them through my computer when they do. The odd thing about this though is that the Austrian school has rebuked the theory countless times. Ludwig von Mises has dealt with it. Henry Hazlitt has dealt with it. Shostak has dealt with it. I’m sure Block and Rothbard have as well. I too have dealt with it in the past, though here I hope to explode it entirely!

“Velocity” is simply the GDP divided by the money supply.

Like all bad things, it comes from this Irving Fisher equation for “the economy”,

M*V = P*T (money supply x velocity = price level x quantity of transactions)

Although, to be fair, Fisher didn’t invent the concept. He only revived it, all the while ignoring the insights of the Mengarian contribution to subjective value theory at the turn of the 20th century.

Originally the concept came about as an explanation for the variation in the effects of increasing money quantities on prices. The quantity theory of money was originally “mechanistic” in that its proponents would argue that an “X” percentage increase in money would produce a proportionate increase in the price level. Since in the real world humans are the intermediaries through whom the technocrats are constantly trying to transmit price increases, and their actions tend to be subjective, prices tend not to be proportionate. The original explanation for this was thought to be velocity.

But it has since been shown to be misleading and irrelevant.

In a nutshell, the fallacies involved here are as follows,

-

can’t separate T and V; and V is the dependent variable

-

velocity is an effect not a cause –doesn’t ‘cause’ anything

-

a poor substitute for the concept of the demand for money

-

money does not actually circulate, nor is that an economic driving force

-

lacks a consistent directional relationship with prices

Demand for Money, Not V

The economics profession, guided by people like Irving Fisher, tended to ignore the contributions of the Austrian School at the time, including their work on the subjective theory of value.

I still find that people automatically fall back into the classical trap on value –where they assume that the value of a good is determined by the sum of its costs to production plus some arbitrary amount representing the productivity of capital (for interest).

But for the most part economists have come to accept the precept that the value of a good is determined by the supply and demand for it on the free market irrespective of what it costs to make, and that the factors (costs) of production are derivative to the value of the good.

Mises applied this insight to monetary theory, ultimately explaining that money too is a good, and that its value is subjectively determined by the judgments of individuals…that a demand for money meant the demand to hold or acquire cash balances…as a store of purchasing power. This made velocity obsolete because it was quickly seen that fluctuations in the demand for money explained its turnover.

A NY Times and WSJ journalist way back in the day named Henry Hazlitt picked up on Mises and the rebirth of the Austrian School under Mises in the early part of the 20th century. Hazlitt put together a wonderful piece that I discovered here, where he argued that changes in the demand for money over time, and not velocity, explain variations in the effects of changes in money supply on prices in general. This explained why prices did not change in proportion to money supply changes. Murray Rothbard later expanded on the various types of the “demand for money.”

The foremost type regards the intensity of trade “T” in the formula above. If I want to buy a car, I am expressing a demand for that car. But the seller of the car is expressing a demand for my cash.

The more exchanges, the more expressions of a demand for money. The two are two sides of the same coin. They are inseparable to be sure. But there are other types of demand expressions that come into play, including the kind that is affected by inflation and deflation expectations. At any rate, changes in prices and other economic factors can now be more accurately (and better) explained by changes in the intensity of the demand for money than they could by changes in its circulation velocity.

Money Never Circulates

There is no flow or circulation. In most transactions the sum of money involved is never actually mobilized, only the title to its ownership changes. Regardless of how high that statistic climbs, money spends the vast majority of its time in the form of someone’s cash holdings or balances – neither in motion nor exactly idle, but rather, always ready to be used. That is its purpose, as Mises put it,

“The service that money renders does not consist in its turnover. It consists in its being ready in cash holdings for any future use. The main deficiency of the velocity of circulation concept is that it does not start from the actions of individuals but looks at the problem from the angle of the whole economic system. This concept in itself is a vicious mode of approaching the problem of prices and purchasing power. It is assumed that, other things being equal, prices must change in proportion to the changes occurring in the total supply of money available.”

Velocity is a Statistic, It Cannot CAUSE Anything

“What we have to deal with, in the so-called circulation of money, is the exchange of money against goods. Therefore V and T cannot be separated. Insofar as there is a causal relation, it is the volume of trade which determines the velocity of circulation of money rather than the other way around... the velocity of circulation of money is, so to speak, merely the velocity of circulation of goods & services looked at from the other side. If the volume of trade increases, the velocity of circulation of money, other things being equal, must increase, and vice versa.”

Changes in the velocity of circulation are clearly the effect, and not the cause, of changes in the demand for money and/or goods. The statistic has no more bearing on the value of money (its purchasing power) than the concept of “inventory turnover” has on the price of the individual units of inventory. If trade is on the rise, circulation (velocity) must rise. Individuals are expressing a demand for money in selling their wares, and the less there is, the more it must circulate or turnover.

“People who are more eager to buy goods, or more eager to get rid of money, will buy faster or sooner. But this will mean that V increases, when it does increase, because the relative value of money is falling or is expected to fall. It will not mean that the value of money is falling, or prices of goods rising, because V has increased... It is the changed valuation by individuals of either goods or money or both that causes the increased velocity of circulation as well as the price rise. The increased velocity of circulation, in other words, is largely a passive factor in the situation." Hazlitt

No Consistent Relation Between Velocity and Prices

Hazlitt found that velocity would vary with the intensity of speculation on Wall Street and other financial centers. There was no directional significance. Sometimes it would increase with falling prices. Other times with rising prices. The same occurs in consumption in its relation to general purchasing power.

An increase in the volume of trade, for example, represents an increase in the demand for money, which tends to result in an increase in velocity. But here the pressure would be on prices to fall.

On the other hand, a reduction in the demand for money caused by inflation fears will tend to increase velocity but put pressure on prices to rise. And vice versa. An increase in the demand for money due to deflation fears can cause prices to fall and decrease velocity while a decline in the demand for money due to a fall in trade might see prices higher depending on other factors while velocity declines.

So it is ignorant to simply state that higher velocity causes higher price inflation and vice versa.

It is equally ignorant to presuppose that economic health depends on spending, lending or velocity.

Conclusion

One of the main causes of the decline in this statistic is simple to explain.

Money growth has outpaced the growth of GDP for over a decade so that the denominator in the calculation of “V” continues to grow.

Another plausible explanation, at least prior to the past 18 months, was the hoarding of cash that seemed evident broadly.

But the causes for the decline in V do not matter.

The decline itself does not matter.

However, a policy intent on stimulating this variable is just as misguided as a policy that is directed at increasing “the amount” of wasteful economic activity at the expense of real prosperity.

There is no doubt that the ECB policy will work to increase lending and money growth, as well as intensify inflation expectations. This will reduce the demand for money, which may or may not result in an increase in V depending on other factors, but it is sure to bring about a renewed euro crisis.

[Not necessarily right away!]

The deflation bogeyman is just that – a myth – used by politicians and central bankers to fear monger the masses into allowing it to inflate. It has never been anything more.

Irving Fisher was one of the earliest authors of the debt-deflation-delusion, and it was he who lobbied for creation of the Fed, and advised the subsequent abandonment of the gold standard.

Clearly the ECB is solidifying his legacy.

But as far as the velocity of money goes, let’s defer to Hazlitt,

“Monetary theory would gain immensely if the concept of an independent or causal velocity of circulation were completely abandoned. The valuation approach, and the cash holdings approach, are sufficient to explain the problems involved.

[Editor's Note: Don't miss Ed's incisive analysis found in the TDV Newsletter three times each month, where you'll find Austrian analysis on the economic topic which affect you today.]

Anarcho-Capitalist. Libertarian. Freedom fighter against mankind’s two biggest enemies, the State and the Central Banks. Jeff Berwick is the founder of The Dollar Vigilante, CEO of TDV Media & Services and host of the popular video podcast, Anarchast. Jeff is a prominent speaker at many of the world’s freedom, investment and gold conferences as well as regularly in the media.

© 2014 Copyright Jeff Berwick - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Jeff Berwick Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.