Recession is On The Way; Beat The Stock Market Crowd, Panic Now!

Stock-Markets / Stock Markets 2015 Feb 28, 2015 - 04:32 PM GMTBy: Mike_Shedlock

In 2006-2007 I called for a recession. We got a big one. I called for another one in 2011, as did the ECRI. That recession never happened.

In 2006-2007 I called for a recession. We got a big one. I called for another one in 2011, as did the ECRI. That recession never happened.

50% is not a very good recession predicting track record except in comparison to consensus economic opinions that have never once in history predicted a recession. Consensus opinion is batting a perfect 0.00%

Investigating the Record

By the way, the ECRI was late in calling the recession of 2007. They still deny it. And questions regarding the 2001 recession and ECRI have still not been answered.

I have talked about all of this before, and it's worth a recap, if for no other reason than to note the difficulty of calling recessions in real time.

February 24, 2012: ECRI Sticks with Recession Call on CNBC; More than a Bit of an Exaggeration by Achuthan to Make His Call?

November 29, 2012: ECRI Sticks With Recession Call

October 13, 2009: A Look at ECRI's Recession Predicting Track Record

That third link above seriously calls into question the ECRI's recession calling capabilities.

I am not calling out just the ECRI. Open up the middle link and you will find this statement by me:

"The ECRI is sticking with its 'US is already in recession' call based on four coincident indicators. Very few agree, but for what it's worth (perhaps nothing) I am one of those in agreement."

I have already admitted my error. It's been silence from the ECRI, which has been my biggest objection to them over the years.

The moral of this story is: "If you cannot admit your mistakes, someone else is sure to admit them for you."

Word About Predictions

Yogi Berra said it best: "It's tough to make predictions, especially about the future."

Nonetheless, and throwing caution to the wind, on January 31, I stated Canada in Recession, US Will Follow in 2015.

Also on January 31, I went Diving Into the GDP Report and noticed "Some Ominous Trends" on imports and exports.

This was my call...

US Recession

The US won't decouple, just as China did not decouple from the global economy in 2008-2009 (a widely-held thesis I also knocked at the time).

Indeed, now that virtually no economist expects a US recession, I believe we are finally on the cusp of one, just as the Fed seems committed to hike.

Contemplating My Own Insanity - Again

With the above backdrop, Albert Edwards at Society General had me laughing at his own personal assessment in his Global Strategy Weekly Email Update (no link available).

He titled his research "Contemplating My Own Insanity - Again." Here are a few snips.

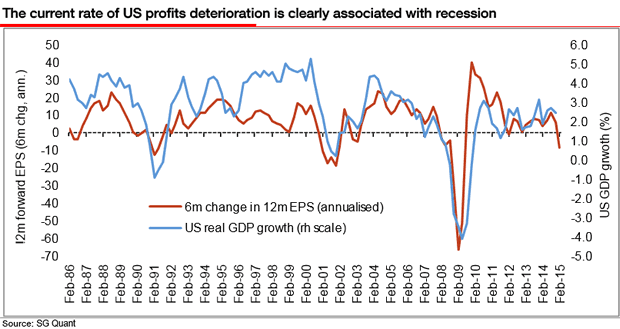

With equity markets galore hitting record high s clearly I must be missing something big! We are at that stage in the cycle where I begin to doubt my own sanity. I've been here before though and know full well how this story ends and it doesn't involve me being detained in a mental health establishment (usually). The downturn in US profits is accelerating and it is not just an energy or US dollar phenomenon - a broad swathe of US economic data has disappointed in February. One of the positive surprises, payrolls, is a lagging indicator. The $64,000 question is not if, but rather when will investors realize what is going on?

My colleague Kit Juke summed it up nicely in his morning note "Whatever the Fed does, they will not risk the economic recovery. That bias is why rates won't get anywhere near 'neutral' before they peak. The economic cycle will be brought down by asset bubbles bursting long before 'tight' policy has any effect. Lessons were learned from the Global Financial Crisis, but not that one."

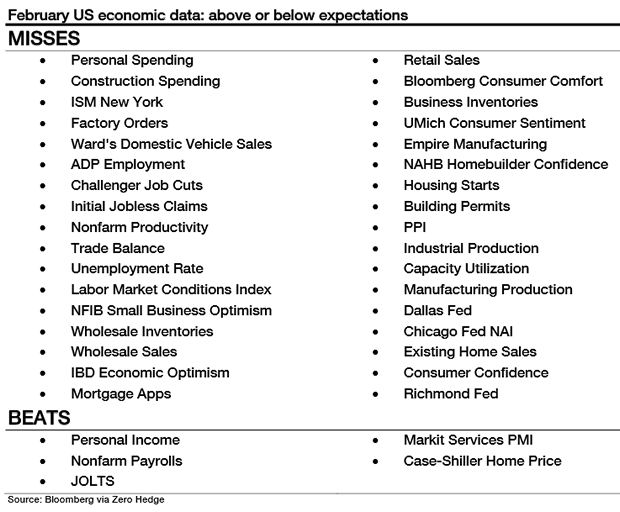

Investors are transfixed instead by the Fed and when it will tighten rates and can't see the wood for the trees. The Fed's focus on payrolls, a lagging indicator, is most perplexing but not unusual at this stage in the cycle. The reality is that the vast bulk of economic, as well as earnings, data (even outside the energy sector), has been simply dreadful.

Current Rate of Profit Deterioration

February US Data Above and Below Expectations

If you believe profit deterioration is a solely or even mostly related to the collapse in oil prices you are mistaken.

Fed Study Shows "Persistent Fed Overoptimism"

The Society General report is all the more amusing because nearly every Fed economic forecast has been on the optimistic side since 2007.

I commented on this phenomenon on February 2 in Fed Study Shows "Persistent Fed Overoptimism about Economic Growth"; What Will They Do About It?

US GDP Slow-Down

File this one in the "If I am wrong, I am at least in good company category."

Via email on Thursday, Steen Jakobsen pinged me with his thoughts.

US Q4 GDP revisions are out tomorrow and will most likely show a slow-down from 2.6% to 2.0%: (Source: Bloomberg - WECO US)

This makes Q3(2014) the peak in this cycle and I expect QoQ growth in the US will hit ZERO by Q3 or Q4 - there are several factors for this including rising real rates, malinvestment into energy but most importantly is the falling earnings in the US.

[Also referring to the society general chart] ... The point however is US data been worsening for a long time - I personally think we are in period where we yet again hand-over the growth engine from the US to emerging market but via a significant new low in growth which will make Europe looks good.

The expected path for me is: Slow down confirmation in the US over the next two months - that will kill the improvement in Europe by end of Q2 and leave it stable - not growing for the year.

Meanwhile emerging market will come back as market realize the FOMC is years away from 'talking up' rates. The June or September initial hike (if it comes) still leaves the FOMC 100 bps above Wall Street on its projected long-term path for growth - a Wall Street who on their own is also too optimistic about future growth. The Fed sees 3.0-3.5% growth while Wall Street sees 2.5-3.0% on average. In other words there is room for a +100 bps correction to the sustainable long-term growth which will render 10-year rates a 1.0-1.5% before we over with this part of the cycle. I label this: Restarting the business cycle.

QE and targeted "help" for banks is running out of time if not out time. The inequality and low salary to GDP base simply can't produce enough domestic consumption anywhere for the middle class to be able to afford the products the stock market listed companies produce.

Macro Conclusion

We are in an "in between period" where the US will slow down and ultimately hand over the growth engine to emerging market by the earliest Q4-2015 but firmly in 2016.

The problem is emerging market are not ready due to high US dollar debt, waning commodity prices, and Europe is still too weak to contribute net to world growth leaving a growth vacuum for new growth.

Europe will show one more month of improving data, then global slowdown of EM and US will drag down the data to flat performance.

Fixed Income

I still only have one very strong view and that's 10 YR fixed income will trade at 1.5%, possibly even potentially 1.0% this year. Everything else will lag this move by 9 month or so. In other words, if the low in yields comes in Q3 (as I expect) then the summer of 2016 will be the lift-off we all have talked about.

The US Dollar will peak this quarter and probably has peaked for this cycle. The weaker US Dollar will stabilize commodities and emerging markets, creating the conditions for a hand-over at the end of this year. The US dollar should be very sensitive to this relative slow-down in the US, especially as Europe is anachronistically improving.

Gold remains top of my list for new investment. I'm long and adding. I have also re-sold Brent/Crude as the marginal cost of producing oil is still rising, meaning global impact still is negative net-net.

Jeremy Grantham excellently argues that for world to benefit from falling energy prices, it has to come with falling marginal cost. The opposite is the case now: lower prices and higher production/extraction costs.

Stock Market

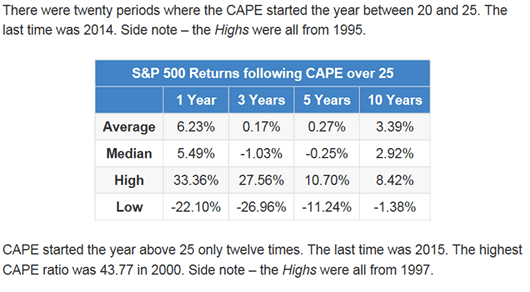

It's not time yet to call the top, but preparing special report on valuations and models, or the lack of it. Conclusion will be: There is potential for a 5-10% gain this year but also for a 25% correction.

The problem of course being that the market is very expensive by traditional standards, but these are hardly normal times.

The expected return for reference over 1, 3 and 10 years can be seen above - the upside is the first year still can carry market higher. The downside is a possible drop for the next 9-10 years!

CAPE Notes

CAPE stands for "cyclically adjusted price earnings ratio."

CAPE started the year over 25.

Business Insider writer Sam Ro commented on CAPE yesterday in Robert Shiller's Revered Stock Market Valuation Ratio is Crappy at Predicting 12-Month Returns.

I laughed at that headline because CAPE was never meant to be a timing signal. Rather it's a medium-to-long term warning signal.

"In other words, don't dump stocks and hide in cash because the CAPE is at 26. Rather, just be prepared [for] lower average returns for years to come," said Ro.

Lower or Negative?

Ro totally misses the boat. The warning is not about "lower" returns; it's about likely "negative" returns.

A Word About "Panic"

It's fitting to see such articles at this time, especially with earnings plummeting and everyone latching on to lagging indicators like jobs.

Yes, I have said this for a couple years. But CAPE has been stretched for a couple years.

CAPE was stretched in 1998 too. Yet, one could have had big gains through March 2000, if one held on, then cashed out at the top.

With that in mind, I have three questions for those who think like Ro.

- How many held on, then cashed out at the right time?

- How many panicked and cashed out at or near the bottom?

- How many held stocks that never recovered at all?

Here's a bonus question: Did anyone buy a basket of stock in 1999, ride them up and down for 15 years, only to find themselves once again at the break even point?

I ask that bonus question because the Nasdaq 100 Index is just below the March 24, 2000 peak.

In spite of the above, we see the same perennial advice today that we saw in January of 2000 "don't dump stocks."

If one has a dedicated, no-panic investment commitment with a time horizon of 15 years or longer, such advice, coupled with dollar cost averaging, may make sense.

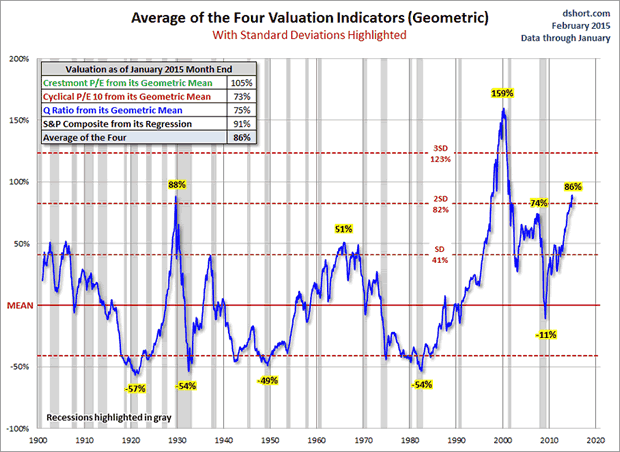

Four Evaluation Metrics

Doug Short at Advisors perspectives has an even more interesting chart of valuations in his post Equity Valuations, Recessions and Stock Market Declines.

Using an average of four popular valuations metrics, the only higher blowoff tops in history were 1929 and the dotcom bust in 2000.

However, ahead of and during the dotcom bust, many market segments were very attractively priced. The same cannot be said now.

Panic Now!

If one doesn't have a dedicated, no-panic investment commitment (that they will realistically stick with), "Don't dump stocks and hide in cash because the CAPE is at 26", is not a good philosophy.

"Panic before everyone else does" is far more appropriate.

Given massive baby boomer retirements, coupled with strong doubts that people can and will have a dedicated time horizon long enough to matter, I offer simple advice: Beat the Crowd, Panic Now!

Outside the Box

For those willing to think outside the box, I echo this sentiment of Steen Jakobsen "Gold remains top of my list for new investment. I'm long and adding."

I also like "perennially despised" US treasuries along with Steen, and I am a big proponent of yen-hedged Japanese equities (a position I believe different than his).

Finally, and also of a contrarian nature, Russia looks quite attractive to me at this time. It's beaten up, off everyone's investment radar, and will do well if the ruble or oil rallies. Typically stocks turn before currencies.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2014 Mike Shedlock, All Rights Reserved.

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.