New Wave of “Creative Destruction” - What I Plan to Present To Energy’s Biggest Players

Commodities / Oil Companies Mar 06, 2015 - 05:20 PM GMTBy: Money_Morning

Dr. Kent Moors writes: Greetings again from London!

Dr. Kent Moors writes: Greetings again from London!

The Annual Energy Consultation of the Windsor Energy Group is set to begin at Windsor Castle later this afternoon.

Over the course of the next three days, I’ll be briefing some of the biggest, most influential players in the energy world on three of the most pressing issues of the day.

I discussed two of them on Tuesday – the massive shortfall in future infrastructure spending and the building wave of consolidation, especially among oil and gas producers.

Today, I’d like to address the most serious short-term concern of them all or what I call the 800 lb. gorilla in the room.

This widening crisis will undoubtedly be the most important part of my Windsor briefing…

This is a $210 Billion Ticking Time Bomb

As I touched on last week, driven by large volumes of high-risk energy debt, a dangerous squeeze is about to hit the energy markets.

In fact, there are actually two very different problems here. The first is the energy component of national (or sovereign) debt. In the interest of time, I will not be discussing this facet of the problem at my Castle briefing. However, it is the primary topic in several upcoming meetings since the initial consequences of this squeeze have already begun to unfold.

You see, despite the recent stabilization, the multi-month dive in crude oil prices has deeply depressed export revenues.

For countries whose central budgets are dependent upon cross-border oil sales, like Venezuela and Ecuador, this puts additional strain on already tight budgets. That severely hampers the ability of countries like these to service issued Eurobonds and other such debt.

With a devalued ruble and the growing difficulty state-controlled companies face in meeting forward currency insurance spreads, Russia is also getting hit.

These insurance spreads are set up to protect foreign partners from catastrophic loss due to a change in currency exchange rates. But with the ruble losing half of its value against the greenback over the past several months, these guarantees are landing hard on Russian companies. Even so, the Russian Central Bank does have ample hard currency reserves and there is little likelihood Moscow will default on any sovereign bonds, although it may suspend trade in currencies from time to time (as it did yesterday morning).

It’s the second facet of the energy debt problem that I’ll be addressing at Windsor.

It involves $210 billion in high-yield bonds that were recently floated by energy companies. That’s roughly 15% of the $1.4 trillion (and rising) high-yield bond market.

It’s a problem because high-yield is synonymous with high-risk. These issues trade at premium interest rates (hence the term “high-yield”) since they are a lower grade of debt.

Much of this issuance is effectively below investment grade, and is often referred to simply as “junk.” As a result, it always carries a more advanced possibility of default.

Now, you might not think that $210 billion of this stuff presents much of a problem. If only that were true. As we had to learn the hard way in other crises, any portion of a debt portfolio that is considered toxic will infect a much larger category of obligations, undermining broader credit stability.

Unfortunately, that is only a small part of the escalating problem. Disregarding other loan encumbrances representing leveraged and collateralized debt, along with credit swaps and other more exotic paper, we have another, more serious, concern.

It’s derivatives.

A Potential Rerun of the Subprime Fiasco

As you may remember all too well, the collapse of the subprime mortgage-backed security market, itself a small portion of the derivatives market in face value or “nominal” terms, caused a worldwide credit freeze and the paper loss of trillions in dollar-denominated holdings.

Now, the same exact scenario is beginning to emerge in oil and gas debt.

In fact, I predicted as much in my recent book The Vega Factor. This can arise from several sources, any one of which can cause great difficulty in determining the actual market value of crude oil.

Today, we are seeing this play out because of the debt problems caused by low oil prices.

The extent of the current debt crisis will only worsen if oil prices stay below $60 a barrel for West Texas Intermediate benchmark-based future contracts in New York.

There is a simple reason for this: Companies that are dependent upon debt to fund drilling projects are reliant on drilling revenues to meet operating expenses, provide profits for investors, and pay off the debt.

Remember, the American shale oil and gas revolution is very much based upon the very high-yield (and high-risk) debt that is now weakening.

Of course, to keep it in perspective, the sky is not falling nor is life ending as we know it. After all, both the housing and mortgage markets survived the subprime mess. Nonetheless, the credit crunch that results creates a significant loss of book value.

At the moment, the current situation in high-yield energy debt is getting worse and there are four main points I’m going to emphasize in my briefing.

First, the spread between high-yield debt in general and energy high-yield debt in particular is worsening as demonstrated by the graph below.

“LHS” refers to the “left hand side” or bid side in the valuation of the debt. Through the end of 2014, the spread between general high-yield and energy high-yield debt has skyrocketed.

While these yields in general ended the year averaging an annualized rate of 688 basis points (bps, or 6.88%), the energy component had spiked considerably higher to nearly 1300 bps, or almost 600 bps higher. As you can see, going back to the beginning of July the two were virtually identical.

This widening spread is a direct consequence of two factors: The market’s increasing recognition of the risk associated with the paper; and the declining quality of the new debt issued. Both of these reflect the suddenly reduced credit worthiness of the issuers.

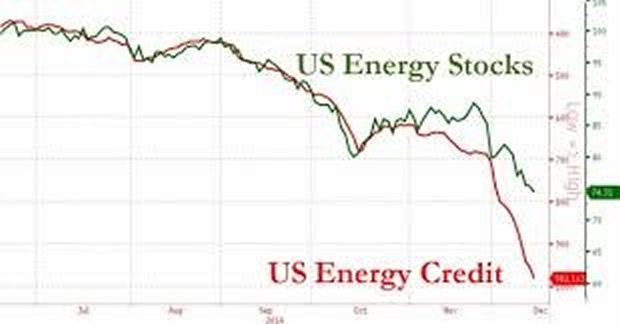

Second, the decline in creditworthiness certainly parallels the rapid decline in oil prices. However, the impact on the debt side was more pronounced than the hit taken on the equity side, as demonstrated by the chart below.

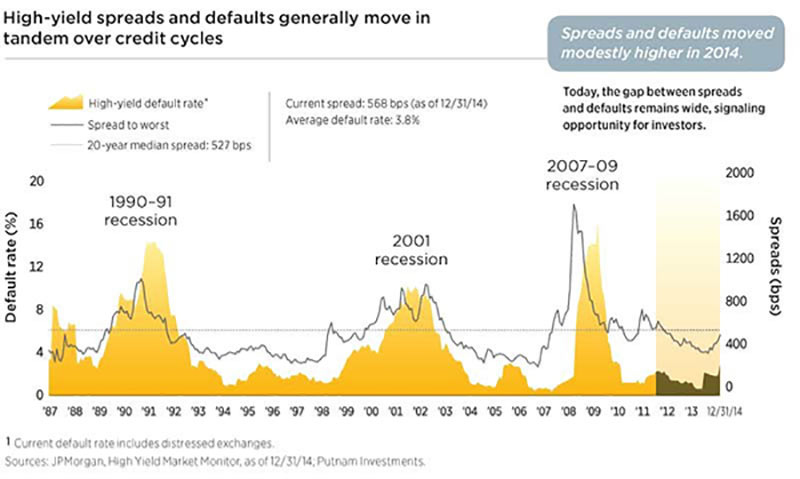

Third, pressure is building for another cycle of junk debt default, with trends at the end of 2014 reminiscent of the last three historical cycles.

As you can see from the chart below, each of the last three spikes in spreads and defaults accompanied a recession. There may be an unusual disjunction this time around, although a spread of the default contagion from energy to other debt may increase the possibly of a general economic downturn this time as well.

A New Wave of “Creative Destruction”

Finally, it’s important to note that we are in the early stages of this cycle. The real problem will hit 12-14 months out. That’s because most companies carrying the debt also have hedged future oil and gas prices this far out.

Over 80% of the forward extraction is already hedged, although continuing low prices will make the cost of pushing that curve further out too expensive to bear.

As oil prices increased a bit over the first six weeks of the year, this situation improved. Unfortunately, we will experience another down move in late March and April as banks readjust their loan portfolios and the risk spread intensifies.

As I’ve noted before, a widening number of experienced analysts are now predicting a rise in oil prices over the next several quarters. This is a view I share. The depth of the energy debt problem is closely tied to the continuing low price of the commodity.

Yet, the prevailing weakness of the debt cycle will remain. And we may see some shorter cycles of volatile rate adjustments in the future, regardless of the price of oil.

At $90 a barrel or above, energy debt is quite safe and spreads are secure. The problem is we won’t reach those levels for some time.

As a result there will be another round of “creative destruction” that will transform the oil and gas playing field.

And yes, we will be making hefty profits off of that as well.

Source :http://oilandenergyinvestor.com/2015/03/plan-present-energys-biggest-players-windsor-castle-part-ii/

Money Morning/The Money Map Report

©2015 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.