Gold and Silver Price Forecast for the Second Half of 2015

Commodities / Gold and Silver 2015 Jun 17, 2015 - 12:23 PM GMTBy: ...

MoneyMorning.com  Peter Krauth writes: Investors considering gold or silver as an investment or hedge need a good handle on the factors driving their prices.

Peter Krauth writes: Investors considering gold or silver as an investment or hedge need a good handle on the factors driving their prices.

That's where supply, demand, trend, and sentiment data come in.

With global economic and market factors painting no clear picture about the near-term prospects for many investments, many of you might be considering whether it makes sense to add gold or silver to your portfolios.

To help you decide, here's my take on the direction of gold and silver prices in the second half of 2015.

A Look at the Direction of Gold

Gold commands and dominates the precious metals space, so that's where we'll start.

In Q1 global demand was nearly flat, down just 1%, or 11 metric tons, from 2014, according to World Gold Council (WGC) figures.

Jewelry was down slightly by 3% at 600.8 metric tons, but has remained above its five-year average of 570.3 metric tons. Chinese jewelry demand was down 23 metric tons, but India compensated by climbing 27 metric tons. In China's case, it seems a combination of slower GDP growth and strong stock markets combined to dent demand. In the case of India, jewelry demand popped 22% year over year, due mainly to unusually weak buying in Q1 2014.

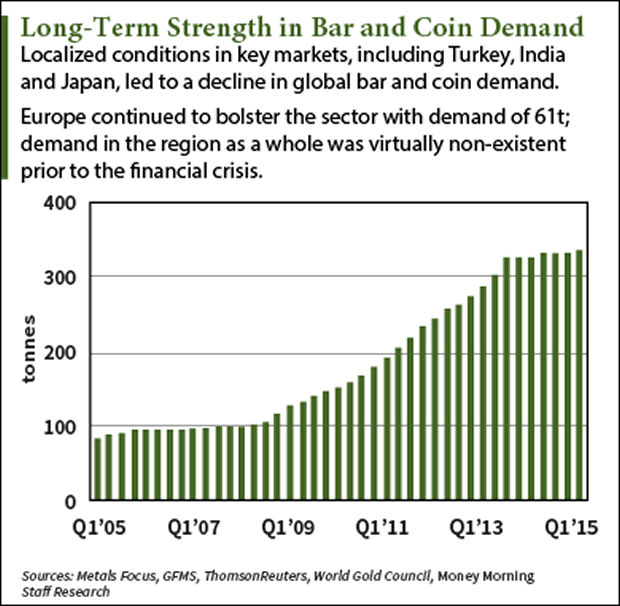

Investment buying boasted an 11th consecutive Q1 increase, with ETF inflows rising an impressive 4%. The demand for physical bars and coins was 253.1 metric tons, down 28 metric tons from last year, but still relatively strong.

European physical gold demand got a strong 16% boost, thanks likely to Grexit fears and the Ukrainian conflict, while Asian physical demand faded.

Central banks have remained conspicuous net buyers, with the current trend now stretching into 17 consecutive quarters. Russia was the standout, adding more than 30t in Q1.

On the other side of the equation, gold supply was up 2% or 16.7 metric tons. The growth has come from select Asian, North American, and African mines. But the WGC expects that the second half of 2015 will be different, with gold mine production leveling off.

I expect that the effect of the last couple of years of persistently weak prices will finally kick in, causing flat or lower output just as prices are near a bottom.

As for sentiment within commodities, gold ranks as one of the least favored, making for a great contrarian indicator. Essentially, the bulk of investors are close to abandonment levels. Sentiment towards gold stocks is also at extreme lows, and the ratio of the gold price to gold stocks also points to bottoming behavior.

We saw gold prices bounce strongly in January, peaking at $1,300 from $1,140 lows in November. That too fizzled into mid-March as the price reversed, bottoming around $1,150. Since then, it's been a mostly sideways move around the $1,200 level. Technically, the gold price has continued to meander within a channel, roughly between $1,170 and $1,210.

So what might we expect in the second half of 2015?

While sentiment has remained weak, conditions are setting up for a possible reversal. Price action in November and then in March looks like a textbook double-bottom, with higher lows since then.

Seasonally, we could well be setting up for a strong H2. Over the last 15 years, my research shows that gold prices tend to provide a strong showing in the second half of the calendar year. On average, gold prices climb about 8% between July and December.

Considering physical supply and demand, sentiment, and the technical price patterns for gold so far this year, I expect we could see some reasonable strength in the second half. Just seasonal strength could be sufficient to push gold back up to the $1,300 level. At the same time, strength could be tempered by a possible Fed rate hike, which would be positive for the U.S. dollar while weighing on gold.

But overall, I think we'll see some constructive movement upwards, enough to challenge the $1,300 highs we saw in January, and perhaps even top them this year.

Where Gold Heads, Silver Should Follow

Silver tends to follow in gold's footsteps. From an investor's point of view, it can be highly volatile, but equally profitable. Let's see where the silver market's been so we might glean insight on its future direction.

According to figures compiled by the Silver Institute, silver demand is essentially made up of 65% industry, 23% jewelry, 6% photography, and 6% silverware.

Industrial demand for silver has been essentially flat for the last three years or so at roughly 620 million ounces annually. The biggest changes have been in photography, which slid 5% last year, while photovoltaic uses (solar panels) were up 7%.

Silver jewelry consumption gained in the last two years, with 2014 up 1.5% over 2013, setting a new record in the process. There's little doubt that onerous import duties on gold imports into India have caused jewelry consumers to increasingly favor silver.

In fact, recent research points to massive silver imports in India of nearly 3,000 tons in the first 4 months, which, if the pace continues, would translate into a staggering 9,000 tons this year. That would equal almost 33% of the total yearly mining output worldwide, and a 27% hike over 2014 levels.

Silverware fabrication was up 3% in 2014, most of which is also attributed to Indian demand.

On the investment side, silver ETFs have remained stable. Gold ETFs have had sizeable outflows, while their silver counterparts have experienced slight positive growth.

As for sentiment, silver appears to be benefitting from a more positive perception than gold. And that is despite (or thanks to?) having experienced much more downside volatility than gold in the last 4 years. Gold is about 37% off its 2011 peak, while silver is down about 67%. As well, the gold:silver ratio is currently at an historic high of 74, which bodes well for silver prices going forward.

Technically speaking, silver appears to be bottoming in November and following gold strongly upward into late January. Here too we have what looks like a November-March double-bottom. Silver's behaved similar to gold since then, but moving slowly higher in a more well-defined upward trend channel.

Again, much like gold, physical supply and demand (and, to a lesser extent, sentiment) and also technical and seasonal influences are likely to be supportive of silver as we move into the second half of 2015.

I think silver has a strong chance of challenging its early 2015 peak near $18.50 and ending the year above that level. That would mean a better than 15% gain from here.

Overall, the second half of 2015 appears to be setting up for an exciting period, one in which gold and silver might be ready to resume their long-term bull markets.

Chinese Tanks Are Secretly Smuggling Gold… The People's Liberation Army is covertly bringing gold into China to hide in its central bank "off the books." In this must-see interview, the CIA's Financial Threat and Asymmetric Warfare Advisor reveals why many in the U.S. Intelligence Community fear this secret stockpile will soon be used to launch an unstoppable attack on the U.S. dollar. Click here to see his startling evidence…

Source :http://moneymorning.com/2015/06/17/your-gold-and-silver-forecast-for-the-second-half-of-2015/

Money Morning/The Money Map Report

©2015 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.