Stocks Bull Market Not Over Till the Fat Lady Goes on a P/E Diet

Stock-Markets / Stock Markets 2015 Jul 15, 2015 - 06:02 PM GMTBy: John_Mauldin

For the vast majority of investors, portfolio returns are generated by the equity markets or at a minimum heavily influenced by the equity markets. We have enjoyed an almost six-year bull market run in the stock market, which has helped heal portfolios after the devastating market crash of the Great Recession. So much so that many prominent market analysts have proclaimed the beginning of a new secular bull market. If we have indeed entered such a new phase, we need to recognize it for what it is, because – as I’ve written for 17 years – the style of investing that is appropriate for a secular bull market is almost the exact opposite of what is appropriate for a secular bear market. I think that most analysts would agree with that last statement. The disagreements would revolve around whether we are in a secular bull or a secular bear market.

For the vast majority of investors, portfolio returns are generated by the equity markets or at a minimum heavily influenced by the equity markets. We have enjoyed an almost six-year bull market run in the stock market, which has helped heal portfolios after the devastating market crash of the Great Recession. So much so that many prominent market analysts have proclaimed the beginning of a new secular bull market. If we have indeed entered such a new phase, we need to recognize it for what it is, because – as I’ve written for 17 years – the style of investing that is appropriate for a secular bull market is almost the exact opposite of what is appropriate for a secular bear market. I think that most analysts would agree with that last statement. The disagreements would revolve around whether we are in a secular bull or a secular bear market.

Thus the answer to the seemingly arcane question of whether we are in a secular bull or bear market makes a great difference in the proper positioning of your portfolios. And getting it wrong can have serious consequences.

Towards the latter part of the ’90s and especially in the early part of last decade, I was rather aggressively asserting in this letter that we should look at whether we are in a secular bull or bear market – not in terms of price but in terms of valuation. Early in that period, Ed Easterling of Crestmont Research, who was then based in Dallas, reached out to me; and we began to collaborate on a series of articles on the topic of secular bull and bear markets, a series that we want to continue today. Longtime readers know that I’m a big fan of Ed’s website at www.CrestmontResearch.com. It’s a treasure trove of fabulous charts and data on cycles and market returns. Ed has been working on a video series (we will offer a few free links below) to explain market cycles.

I want to provide a little current context before we jump into the argument about whether we are in a secular bull or bear market. For some time now, I’ve been saying that the US economy should bump along in the Muddle Through range of about 2% GDP growth. The risk to that forecast is not from something internal to the United States but from what economists call an exogenous shock, that is, one from outside the US. In particular I have said that a crisis in both Europe and China at the same time would be very negative for both US and global growth. We now see potential crises in both regions. It would be convenient if they could arrange not to have them at the same time. But those who are paying attention to global markets are certainly experiencing a bit of market heartburn as they watch both China and Europe manifest the volatility that they have over the last few weeks. I will become far less sanguine about the US economy if full-blown crises develop in those two regions.

There are observers who think the Greek crisis will be contained, and then there are equally astute but pessimistic observers, like Ambrose Evans-Pritchard, who wrote this week about the potential for a full-scale European meltdown. His recent column entitled “Europe Is Blowing Itself Apart over Greece – and Nobody Seems Able to Stop It” is reflective of those who think the European monetary experiment is problematic. It now appears that Tsipras has essentially caved on a number of issues in order to get a deal. The deal he has proposed reads almost exactly like the one the Greek referendum overwhelmingly rejected.

My own personal view is that, if this deal is agreed upon, it simply postpones the crisis for a period of time, as Greece simply has no way to grow itself out of its debt dilemma. And it is not altogether clear that Tsipras can hold his coalition together, given the referendum. He might actually need the opposition to get this deal passed, which becomes problematical for him, as it might force him to call an election. But the banks would open, and Greek life would go on until the Greeks run out of money again in the sadly not-too-distant future, as there is no way on God’s green earth they can meet the growth requirements that this deal demands.

The monetary union is an absurd creation based on political hopes, not economic reality. Politics can keep it together for longer than it should otherwise exist, but unless the entire southern periphery of Europe turns German in character, the peripheral nations are going to suffer under a monetary policy not designed for their economies. That ill-fitting economic straitjacket is going to mean slower growth and higher unemployment and fiscal instability. How long will they endure that? So far, a lot longer than I thought they could, 15 years ago.

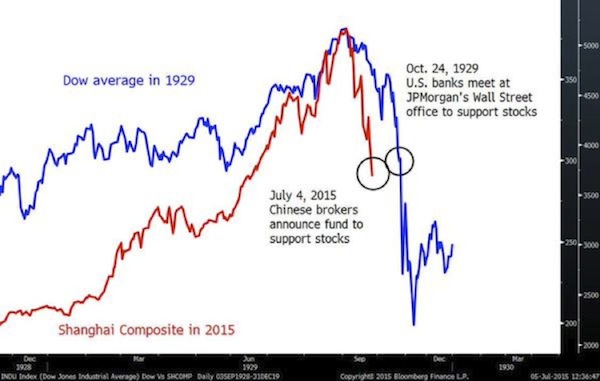

China’s stock markets are having a meltdown, although there has been a rebound the last few days as the Chinese government has stepped in with the decision to destroy their markets in order to save them. My friend Art Cashin commented that it is amazing what you can do if you tell people that they will either buy stocks and make them go up or get executed. It certainly clarifies your trading position. Further, the Chinese government basically created a rule which said that anybody who owns more than 5% of any particular equity issuance is not allowed to sell for the next six months. Neither are directors, supervisors, or senior management of any public company. The government has evidently pressured banks into creating a buying consortium. Historians who are familiar with the stock market crash of 1929 will see an interesting parallel, illustrated in the chart below (sent to me by my friend Murat Koprulu).

Hundreds of Chinese stocks have been taken off the market because they are essentially locked limit down or because company management simply halted trading in their shares, as there seemed to be no bottom to the pricing. That is an interesting way to run a supposedly liquid equity market exchange. And it creates an overhang, in that, under the current rules of the exchange, those hundreds of stocks have to go back on the market within 30 days. Theoretically, they were falling in value, which was why they were taken off the market to begin with. Will their valuations somehow magically change?

I wonder if all the major indexing firms are happy with their recent decisions to include China as a major portion of their indexes, given that liquidity in their markets is available only when markets are going up. Just curious, but how in the Wide, Wide World of Sports do you price or even maintain an index if you can’t sell and have daily liquidity and price discovery? If 7% of your index is based on a valuation that is not real, what price do you then base daily liquidity on? The last trade? So the seller gets out at a price that might be significantly higher than what the issue would actually trade at? Who sues whom? Or maybe the issue then trades higher, not lower, so that the seller should have gotten more? Index fund managers have to be pulling their hair out over this one.

Is this collapse of the Chinese market just the result of irrational exuberance, or is there something more fundamental going on? We will have to watch the situation carefully in the coming weeks.

By the way, China is far more critical to the global economy than Greece is. So much so that I recently asked a number of my friends to give me their best thoughts on China. These are experts in markets, demographics, economics, geopolitics, and so on, all with specialties in China. I’ve compiled those thoughts along with my own and those of my co-author, Worth Wray, in an e-book called A Great Leap Forward? You can get it on Amazon, iTunes, and Nook for a mere $8.99. It is an easy read that will give you an understanding of China’s challenges, from the best China experts we could find. Now, let’s talk about where the market is going in the US.

Are We There Yet? Secular Stock Market Cycle Status

By John Mauldin and Ed Easterling

We were both talking about secular bear markets back in 1999 and 2000. It’s been 15 years. Aren’t we there yet? Isn’t the stock market rising?

Of course you’re getting impatient; so are we. When will the stock market shift from secular bear to secular bull – or did it already? The implications are significant. Through much of the 2000s and into the 2010s, individual and institutional investors have weathered quite a storm of low returns and high volatility. Are we done being battered? From today, can you reasonably expect above-average secular bull returns like we saw in the 1980s and ’90s … or do we face another decade or longer of below-average secular bear returns? [For a 3-minute video explaining the term secular, click this link.]

In short, we use secular to describe a particular valuation environment. If you use valuations as a tool for thinking about cycles, the cycles become much more clear and easily understandable. Simply using price gives you no objective criterion for determining where you are in a long-term cycle. Within our longer-term secular designations there can be numerous and significant cyclical bull and bear markets, which are determined by price and not valuations.

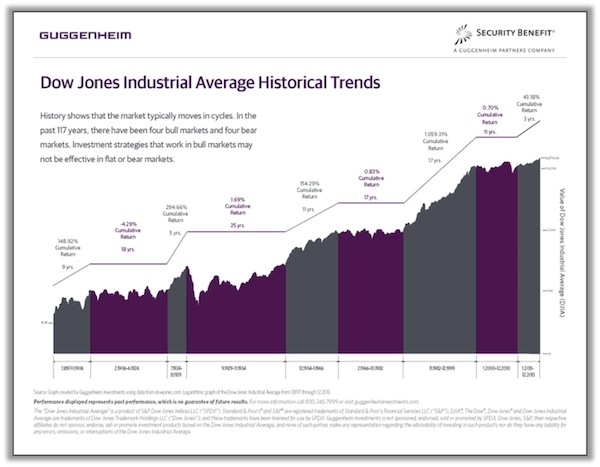

For years, analysts and pundits throughout the industry have agreed (though it took a number of years for many of them to come around) that the new millennium brought with it secular bear conditions. In the past few years, however, opinions have once again diverged. Notable heavyweights, including Guggenheim Investments, Raymond James, and BofA Merrill Lynch, are on the record that the stock market has now entered a long-term secular bull market. (They are certainly not the only ones, but they do provide nifty charts that make it easy to analyze their thoughts.)

As shown in Figure 1, Guggenheim clearly marks the transition point between the end of the secular bear that got underway in January 2000 and the start of the new secular bull market. They place that transition point at December 2010, so that by their reckoning the secular bear lasted eleven years and produced near-zero annualized returns. Then, according to Guggenheim, a new secular bull market was unleashed with New Year 2011.

Figure 1. Guggenheim Secular Bull Started January 2010

| From today, can you reasonably expect above-average secular bull returns like we saw in the 1980s and ’90s … or another decade or more of below-average secular bear returns? |

Now, four years and a cumulative +54% later, the Guggenheim chart appears to lead investors to expect a future of above-average secular bull returns. They are somewhat subtle about it: note the implicit investment advice in the upper-left area of the chart: “Investment strategies that work in bull markets may not be effective in flat or bear markets.”

To continue reading this article from Thoughts from the Frontline – a free weekly publication by John Mauldin, renowned financial expert, best-selling author, and Chairman of Mauldin Economics – please click here.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.