The Ultimate Cash-Management Guide

Personal_Finance /

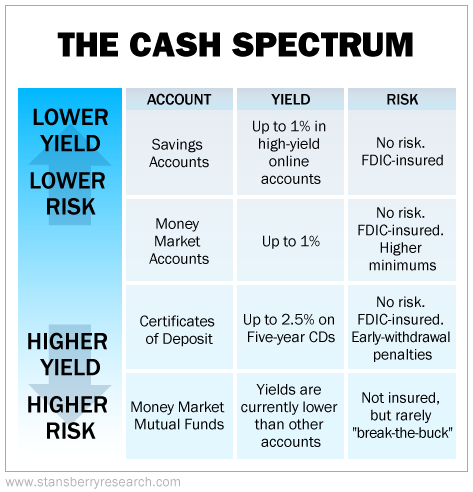

Savings Accounts

Aug 27, 2015 - 06:33 PM GMT

By: DailyWealth

Dr. David Eifrig writes: No one talks about how to manage your cash.

But you need to give some thought to where you put it...

As with every investment, when you look at where you put your cash, you need to balance yield and risk.

Some of these cash accounts I'm going to cover today are 100% risk-free. Others claim to be low-risk, but may have hidden risks that are difficult to understand.

We'll start with the lowest-risk, most "pure" cash accounts... And we'll proceed through investments that could offer a higher yield.

Checking and Savings Accounts

The safest cash accounts are FDIC-insured checking and savings accounts with banks.

FDIC insurance means that even if the bank makes disastrous loans or a bank manager absconds with the money in the vault, the Federal Deposit Insurance Corporation will make depositors whole, up to $250,000.

These accounts are liquid, meaning you can access your cash almost instantly via online banking or at a branch office.

Checking accounts are a good example. You can write checks directly from your account. However, they pay little in interest. I recommend keeping your checking balance just high enough to avoid any overdrafts. Or do what I do and link your checking accounts to your savings account for overdraft protection.

Savings accounts offer better yield, with the same safety.

Were it not for historically low interest rates, this would be a Golden Age for savings accounts. The advent of secure online banking has removed geography from the equation. So smaller banks looking to boost deposits often offer higher rates to anyone.

Big national banks, like Bank of America and Wells Fargo, offer savings accounts that currently yield 0.01% and 0.03%, respectively. You can do much better with a little searching. Websites like Bankrate.com or Nerdwallet.com/rates can help you find the best rates.

A word of caution: Always read the fine print to be certain that your account is FDIC-insured. Just because you've walked into an FDIC-insured institution (or visited their website), it doesn't mean every account is insured. These banks offer all kinds of products and many don't fall under the FDIC's watch.

Money Market Accounts

One such FDIC-insured product is a money market account, or MMA.

MMAs, sometimes referred to as money market deposit accounts, will usually have higher minimum deposit requirements than savings accounts, though this can be as low as $500 in some cases.

If you meet those minimums and have your checking accounts covered, MMAs almost always pay a higher rate than savings accounts. So use them when you can.

Again, you can use the tools at the websites we've mentioned to find the highest rates on MMAs.

For both savings accounts and MMAs, regulations state that you can't have more than six transfers per month into or out of the accounts. So it takes a little planning to make sure that your checking balances can handle whatever you need.

Certificates of Deposit

Certificates of Deposit, or CDs, have many of the benefits of savings and money market accounts... For example, they're FDIC-insured, with no risk of loss unless our entire government collapses... with just one drawback.

However, that drawback comes with a higher yield, and it just may be the perfect place to place your cash depending on your needs.

The risk they do carry is liquidity risk. When you put your cash in a CD, you agree to leave it there for a particular amount of time, between three months to five years.

If you want to get it back before then, you need to pay a penalty.

Since the money is locked up, the bank will give you a higher interest rate. You can collect about 1%, or even 1.15%, on a one-year CD from some of the more competitive banks... with higher yields for longer time periods. Check the websites we've recommended to find the best rates.

Given that your money is locked up, CDs work better for the cash allocation of your portfolio as you approach retirement, not your emergency fund.

Money Market Mutual Funds

All the prior cash accounts have a major advantage: They are FDIC-insured. The peace of mind that should give you can't be overstated.

When you branch out into money market mutual funds (or MMMFs), you do not have an FDIC guarantee. You now face the risk of loss. You have become an investor, and not a saver.

That's not how MMMFs are sold, though. They are sold as ultra-safe places to hold your cash savings. You'll see language from fund companies like, "[the fund] seeks to provide current income and preserve shareholders' principal investment by maintaining a share price of $1."

This $1 share price is the central focus of MMMFs. You buy shares for $1 and the fund invests that cash in short-term securities. By law, the investments must expire within 90 days.

When the fund makes money, its share price doesn't rise. Instead, it creates more $1 shares and adds them to your account. If you check your balance, it doesn't look like you're an investor. It looks like your dollars are growing.

Here's the trick with MMMFs...

They are exceptionally safe... until they aren't.

MMMFs use a wide range of securities to generate their returns. There is a massive market of short-term securities that you've likely never explored.

They use securities like short-term Treasury bonds and T-bills, but they also use things like overnight repurchase agreements, or repos. This is a complex system whereby a bank will borrow $99.99 overnight and pay back $100 the next day. Of course, this is happening on the scale of trillions of dollars.

This system is called the "shadow banking" system. It works flawlessly almost all the time. But when things go wrong, there's trouble.

This is what happened in the financial crisis. In 2008, the short-term paper markets froze up. People were too scared to lend to one another, even overnight loans to the biggest banks. The market was in a panic.

A few funds got themselves into trouble. The Reserve Primary Fund was one of the largest and most respected funds, with $68 billion in assets. In particular, it had a big pile of securities issued by Lehman Brothers. Since everyone was in a panic, the fund couldn't figure out what these loans were worth.

The fund was unable to maintain its $1-per-share value. This is known as "breaking the buck."

Investors in the Reserve Primary Fund had their cash frozen while the fund sorted things out. It was more than a year before a court ordered the fund to pay out whatever funds it did have to shareholders.

Some people had hundreds of thousands of dollars in "cash"... but they couldn't access a penny.

Now, trouble like this doesn't happen often. Prior to 2008, not a single fund broke the buck in the 37-year history of MMMFs.

So you shouldn't fear MMMFs... but you do need to understand what's happening with your cash when it no longer has FDIC insurance.

There are also some tricks you can use to ensure you get the best MMMFs.

The shadow banking system is a highly efficient market. That means if a fund has a higher yield than its competitors, it's taking on more risk.

You should also back out the fees. For instance, take two funds that each yield 1% after fees. You would think that they have the same risk. However, one might charge a 0.5% management fee and the other might charge 0.25%.

That means the fund with the higher fees has to use riskier investments to get the same yield. In this case, the low-fee fund is unequivocally better than the high-fee fund.

And diversification will benefit you here as well. If you have a substantial amount of cash and you don't want it frozen during a crisis, spread it around a few different MMMFs managed by different investment companies. Three different funds should be enough.

MMMFs do have some remote risk, and right now their yields are not high enough to justify taking those risks relative to FDIC-insured accounts.

MMMFs, on average, yield only about 0.01% today. When you look up funds, you'll see it quoted as the seven-day yield. This uses the fund performance from the last seven days to determine its annual yield.

Considering you can earn much better than that in an FDIC-insured savings account, we consider MMMFs mostly off the table until interest rates rise.

MMMFs might not be such a great investment then, either. The U.S. Securities and Exchange Commission has drawn up a new set of rules for MMMFs to make them safer. The trouble with MMMFs comes partly when everyone tries to withdraw their funds at the same time.

So, effective October 2016, MMMFs used by individual investors can deny you access to your money for up to 10 days, or they can charge a redemption fee of 2%.

To make that worth it, MMMFs are going to have to yield a heck of a lot more than they do today.

To sum up:

Most people don't spend too much time thinking about their cash.

But sitting down and taking a rational look at your cash needs can provide for emergencies and immediate needs without sacrificing long-term returns.

And making sure you hold your cash in the right place can help you sleep well at night while keeping inflation off your back.

Here's the good thing about getting your cash investments in order: Once you do, it takes little time to keep things in order.

If you're an income investor, you should be successfully generating cash month after month and quarter after quarter. This essay should help you know what to do with it.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Editor's note: Yesterday, Doc hosted a special live training event where he revealed the secret behind his extremely successful Income Intelligence newsletter. If you missed it, don't worry... We've put together a special follow-up presentation to make sure you have all the information you need to maximize your income.

Doc has also agreed to extend a second offer for those who couldn't tune in... Until midnight on Sunday, August 30, you can get not one, but two full years of

Income Intelligence for less than a cup of coffee a day (a savings of more than 25%). And by signing up today, you'll have six months to see if his service is right for you. To learn more about this incredible offer,

click here.

http://www.dailywealth.com

The DailyWealth Investment Philosophy: In a nutshell, my investment philosophy is this: Buy things of extraordinary value at a time when nobody else wants them. Then sell when people are willing to pay any price. You see, at DailyWealth, we believe most investors take way too much risk. Our mission is to show you how to avoid risky investments, and how to avoid what the average investor is doing. I believe that you can make a lot of money – and do it safely – by simply doing the opposite of what is most popular.

Customer Service: 1-888-261-2693 – Copyright 2013 Stansberry & Associates Investment Research. All Rights Reserved. Protected by copyright laws of the United States and international treaties. This e-letter may only be used pursuant to the subscription agreement and any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), in whole or in part, is strictly prohibited without the express written permission of Stansberry & Associates Investment Research, LLC. 1217 Saint Paul Street, Baltimore MD 21202

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.