Stock Market 180 in 50 Weeks. This is Different

Stock-Markets / Stock Markets 2015 Oct 01, 2015 - 02:58 PM GMTBy: Ashraf_Laidi

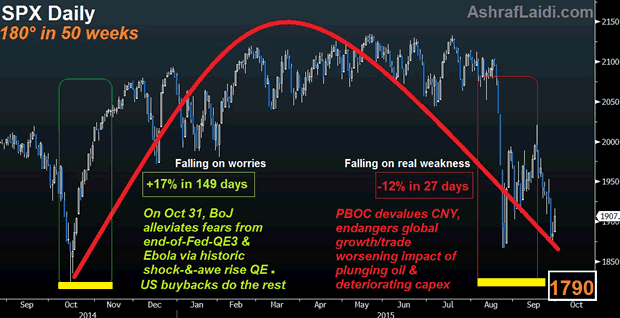

A lot has happened since that fateful October bottom in stocks, which was driven by a multitude of factors namely, market worries over end of Fed QE and escalating casualties from the Ebola virus. But those were only worries and not factual manifestations of data weakness. Today, the extended weakness in the world's biggest buyer of commodities, combined with the erosion of the "Gulf Nations' Put" as well as the decline in EM FX reserves is a de facto tightening from in and capital markets.

A lot has happened since that fateful October bottom in stocks, which was driven by a multitude of factors namely, market worries over end of Fed QE and escalating casualties from the Ebola virus. But those were only worries and not factual manifestations of data weakness. Today, the extended weakness in the world's biggest buyer of commodities, combined with the erosion of the "Gulf Nations' Put" as well as the decline in EM FX reserves is a de facto tightening from in and capital markets.

These are only some of the factors, which prompted a 180° downturn since the mid-October lows, dragging the S&P500 down 12% in a mere 27 days, following +17% in as many as 149 days from the October lows to the May highs.

As the market gradually makes its ways back to the October lows, it is important to contrast the situation between now and then.

Greater USD Fallout

The USD may have stabilised against the euro and yen, but in trade-weighted terms, it has gained an additional 14% against most major currencies since October, exacerbating the currency translation effect for US multinationals and increasing the price for US exports in the global market place.

The situation is especially ominous when considering surging costs of USD-denominated loans in emerging markets, especially in Asia where the USD has risen 8% against a basket of Asian currencies since October. In China alone, more than $900 bln in USD-denominated debt remain unpaid. Not to mention the IMF warning about surging EM debt.

Nearing Disinflation

Most market and survey-based measures of US inflation are lower than in October 2014. Unlike survey-based inflation measures, which are provided monthly, break-even rates priced off US inflation-protected bonds are available daily, with the 2-year BE tumbling near 8-month lows at 0.23% and 5-year BE rates at 1.1%, nearing its 6-year lows. These inflation measures have been criticized for being too sensitive to oil prices. But is the Fed being inadequately aware of falling oil prices? We warned here about how the Fed could be behind the curve in accounting for energy's impact on inflation.

But the Fed now risks being behind the curve in pre-empting deflation as real yields surge.

No Magic from BoJ, ECB

Two weeks after global yields and share prices plummeted in midOctober, the Bank of Japan surprised the world with a rare split 5-4 decision in its policy board to accelerate the monthly purchases of Japanese government bonds so that its holdings increase at an annual pace of 80 trillion yen.

Two weeks later, the European Central Bank signaled to markets that quantitative easing and negative interest rates would finally be pursued.

Markets' reaction to these events was a 2-month rally in global shares, which eventually stalled in January 2015 as the New Year gave its first hint of impending deflation.

China Devaluation = Antithesis of ECB, BoJ QEs

China today is far weaker than it has ever been over the last 15 years. Most services and manufacturing surveys indicate a contraction, while exports have declined for the 5th month over the last seven months, driving down currency reserves to two-year lows. Tying the yuan to the rising USD has worsened the situation since October.

Last month's CNY devaluation may have been a slight stimulus for China, but its impact on the rest of the world is the antithesis of QEs from the BoC and ECB. And once again, do not forget the disappearance of the MidEast out after reports that Saudi Arabia's Monetary Authority has withdrawn as much as $70 bn over the past six months. If you thought injections from MidEast and FarEast SWFs were instrumental in stabilizing global markets in 2007-9, then contemplate the reverse effect of these flows as Saudi Arabia and Qatar consider selling (known as restructuring their portfolios) to withstand budget imbalances resulting from falling energy prices.

We expect the October low to be revisited, before it is taken out for the next leg in what will become a bear market.

By Ashraf Laidi

AshrafLaidi.com

Ashraf Laidi CEO of Intermarket Strategy and is the author of "Currency Trading and Intermarket Analysis: How to Profit from the Shifting Currents in Global Markets" Wiley Trading.

This publication is intended to be used for information purposes only and does not constitute investment advice.

Copyright © 2015 Ashraf Laidi

Ashraf Laidi Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.