The Stock Market Global Central Bank Put Option

Stock-Markets / Stock Markets 2015 Nov 18, 2015 - 12:02 PM GMTBy: Bob_Kirtley

Highly accommodative monetary policy and the increased responsiveness of central banks globally to economic shocks and other crises has led to a situation where, if such a shock occurs, then central banks ease monetary policy quickly in response. This action calms markets, resulting in minimized selloffs and contained volatility while driving equities higher.

Highly accommodative monetary policy and the increased responsiveness of central banks globally to economic shocks and other crises has led to a situation where, if such a shock occurs, then central banks ease monetary policy quickly in response. This action calms markets, resulting in minimized selloffs and contained volatility while driving equities higher.

This phenomenon can be described as the Central Bank Put Option, as the situation effectively means that investors have a put option given to them by the central banks. We will discuss its origin and how it is currently in play, and then cover different strategies that can be used to take advantage of the put. Following this we will also look to analyse whether the Central Bank Put will be in play next year and how it may be traded going forward.

The Bernanke Put

The term “Greenspan Put” was first coined in 1987 to describe the situation of then Fed Chair Alan Greenspan adding monetary liquidity to avert a further deterioration of the markets after the 1987 crash, and throughout his term as Fed Chair. With Ben Bernanke taking over as Fed Chair in 2006, the term “Bernanke Put” became widely used as the Fed continued the practice of lowering rates to counter falling markets.

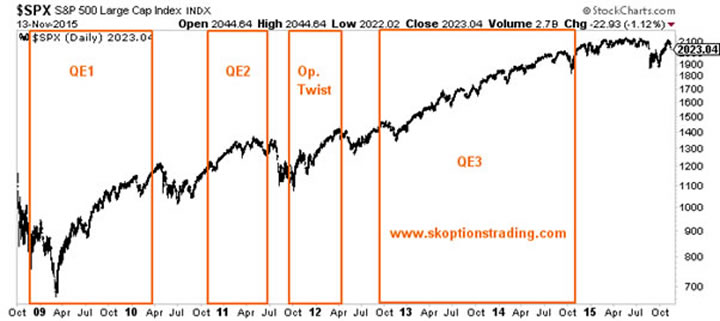

Following the GFC and during the Great Recession the Fed took on a highly dovish stance, cutting interest rates repeatedly and engaging in monetary easing on a massive scale. This has resulted in a massive bull market in equities, with the periods of greatest strength coming during periods of increased dovish activity by the Fed.

Less than three months into QE1 the stock market ceased its decline, following which the S&P rallied more than 70%. The next round of easing lasted only six months, but QE2 nonetheless saw the S&P push a solid 15% higher. During Operation Twist markets rallied again, this time by more than a quarter. Throughout its span QE3 saw the S&P rally another 40%.

It is important also to consider the movement in stocks in between these gains. The most telling of these is the weeks between QE2 and Operation Twist. This gap saw markets decline considerably, erasing the gains made during QE2 and threatening to move lower. Thus we have a situation of markets falling without new action from the Fed and the Fed responding with further easing that drove markets higher again.

Therefore, investors could speculate on the stock market without the fear of a crisis negatively affecting their portfolio’s, as the Fed would quickly intervene with new easing measures to ensure that any selloff was quickly reversed. This means that if an investor held a long position on equities, then they had protection from the Fed Chair Bernanke on any downside. Thus, we have the Bernanke Put.

The Global Central Bank Put

Major central banks, such ECB, BoJ, and BoE to name a few, took highly accommodative stances on policy following the GFC. The effects on their stock markets has been much the same as the Fed’s has been on US equities. European markets can rally knowing that if things go south, the ECB will step in.

Taking this a step further and without loss of generality, we see that European markets also know that the Fed will take action if the US economy suffers an economic shock, and vice versa. This means that every stock market is far less vulnerable to overseas shocks, as a result of foreign action, and is far less vulnerable to domestic shocks as their own central bank will take action in that situation.

The chart above shows that during QE1 and QE3 European stocks also rallied well. During QE2 stocks in Europe did not perform as well, however this was mirrored to a lesser extent in the S&P and was a result of a lack of action from the ECB in response to the Greek debt crisis. We will discuss this risk in further depth below. Now that the ECB has a QE program in place European stocks rallied well before the concerns around China’s growth panicked markets. However, these fears are now passing with the People’s Bank of China taking action. As a result both US and European equities have rallied back.

Therefore, we have a Global Central Bank Put Option in play, the effect of which is much stronger than a Bernanke Put due to the spill over of all major central banks having similar policies in place. The result is that crises with the potential to harm the global economy can be much better absorbed and without significant negative effects.

Trading the Global Central Bank Put

The Fed has been moving towards an interest rate hike this December. However, their overall stance has still been highly accommodative throughout 2015, as has the stance of central banks globally. This means that the global central bank put has been in play during 2015. We have taken advantage of this through a number of strategies, namely by selling downside protection on equities and selling volatility spikes.

We sold downside protection on equities by shorting in the money put spreads on SPY, the ETF that tracks the S&P. During February we sold SPY Dec ’15 $185/$180 vertical put spreads for $1.30. Provided that SPY remained above $185, or equivalently the S&P above 1850, we could collect the maximum gain by holding the trade until expiration.

Even with the correction made in August the S&P has not traded as low as 1850 all year. We chose to tactically exit the position after just 29 days to bank a 13.24% profit, and have used the strategy regularly since then as a part of our trading arsenal.

We have also made a number of trades selling spikes in volatility, all of which have been profitable. During the Ebola panic last year the VIX, the index that tracks S&P 500 volatility, more than doubled when it spiked to over 30. Given that the Central Bank Put was in play, we knew that this spike was highly unlikely to last. Either markets would calm of their own accord, or central banks would take action to ensure that equities rallied back and that volatility would consequently fall. Accordingly, we heavily shorted the VIX index by buying XIV, the inverse ETF for the VIX.

We allocated 25% of our portfolio in total, using 5% and 10% clips to progressively increase our volatility short as the VIX index rose. As markets calmed and the VIX fell back to normal levels below 12 we took profits on our short, gaining as much as 18.14% on just one of these positions.

While the profits banked on these types of trades are less than our average of 28.41%, they carry highly favourable risk reward dynamics. The likelihood of a loss is very low as the Central Bank Put greatly increases the probability that profits can be banked if the trade is set up correctly. Each of the trades we made have also been with limited risk, so we knew the maximum losses going into the trade.

Consider the alternatives to these type of trades that also look to take advantage of the Central Bank Put. One could have sold puts that would expire worthless if markets remain high. This is similar to our vertical put spread trades, but involves unlimited risks if markets fall, which we do not believe is prudent to take on.

The Central Bank Put does not guarantee that markets will rally, but rather protects against the downside. This means that upside directional plays, such as buying calls or stocks outright, are not ideal to take advantage of the Central Bank Put. These type of trades have their place and we regularly use them, but for simply making money on the Central Bank Put they are not ideally suited.

The Road Ahead

Monetary policy the world over remains highly accommodative. This is likely to remain the case in next year, even if the Fed hikes in December as we believe they will. However, does this mean that the Central Bank Put will still be in play in 2016?

Quantitative easing now has had diminished benefits. Broad based programs similar to QE1 and QE2 are unlikely to be effective enough to keep the Central Bank Put active. This means that more targeted measures, such as buying credit, will be necessary to ensure markets are confident that central bank action is sufficient maintain economic health, and thus keep markets from falling.

This means that the Central Bank Put is unlikely to be in play for markets where their respective central bankers are not able to effectively, and swiftly, evolve and advance easing methods when required. The value of the Central Bank Put is inextricably linked to the credibility of the policymakers that are targeting asset price stability. Therefore any announcements of new QE programs need to be analysed carefully if one intends to make a trade to take advantage of this Central Bank Put.

While the Central Bank Put offers many trading opportunities, there is no such thing as a free lunch. These opportunities must be treated with caution. If markets react negatively to a new, or even existing, measure, the downside risks to Central Bank Put based trades are substantial.

Consider the Greek debt crisis of 2010 when the ECB failed to act quickly with the necessary measures to calm markets. The result was that by the time the ECB announced a bailout plan fears had already set in. Markets did not have the confidence that the central bank intervention was enough when it came into play, and as a result the EuroStoxx 50 index decline more than 10% even after the bailout plan was released.

European equities therefore declined more than 17% from peak to bottom before beginning to sluggishly move higher again, finishing around 5% down on the year despite central bank action. This situation demonstrates the risks involved with taking advantage of the Central Bank Put. Had one tried to do so with European stocks in 2010 they would have very likely lost money. Any outright long trade would have finished lower on the year while an options based trade would have potentially lost considerably more.

While at present the chance of this kind of downside being realised is small, the diminishing effect of various QE programs and a shift towards tightening in the US mean that these low probabilities have the potential to grow significantly.

Therefore there is no definitive yes or no answer to our question of whether the Central Bank Put will be in play in 2016. We believe it is likely that there will still be trades that can benefit directly from the Central Bank Put next year, however the nature of these positions will very likely vary. Therefore, as with all trading strategies that we employ, we will continually examine and re-examine the risk reward dynamics involved.

We believe that this will allow us to find and take advantage of those opportunities and, more importantly, avoid those trades that will be likely to lose money. If you wish to find out the results of this analysis throughout the changing market dynamics the next year will hold, please visit www.skoptionstrading.com to learn more.

Go gently.

Bob Kirtley

Email:bob@gold-prices.biz

URL: www.silver-prices.net

URL: www.skoptionstrading.com

To stay updated on our market commentary, which gold stocks we are buying and why, please subscribe to The Gold Prices Newsletter, completely FREE of charge. Simply click here and enter your email address. Winners of the GoldDrivers Stock Picking Competition 200

DISCLAIMER : Gold Prices makes no guarantee or warranty on the accuracy or completeness of the data provided on this site. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This website represents our views and nothing more than that. Always consult your registered advisor to assist you with your investments. We accept no liability for any loss arising from the use of the data contained on this website. We may or may not hold a position in these securities at any given time and reserve the right to buy and sell as we think fit.

Bob Kirtley Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.