Long-Term Treasury Bond Market Paradox

Interest-Rates / US Bonds Jul 10, 2008 - 09:05 PM GMTBy: Jim_Willie_CB

The US Treasury Bond market can be confusing. Price inflation in the United States is intentionally made confusing. That keeps the public ignorant and poorly prepared to interrupt grand larceny and elite control of the printing press, the result of which has been a few decades of hidden confiscation of Middle Class work, wealth, and dreams. Long-term bond yields have many fundamental reasons why they should fall lower in the United States . They are interwoven and integrated. The US Economy is being killed by rising costs, in no way justifying higher borrowing costs. Yet amateurish opinions seem to coalesce in an absurd consensus. The Asian renaissance contributes mightily to both the impoverishment of America and its economic stagnation. Anyone who believes the US and Europe should share a consistent rhyming monetary policy is asleep at the analytic wheel. In the zero-sum game that is currencies, higher prices in the United States come with lower prices in Europe . Refer to marginal incremental movement in prices.

The US Treasury Bond market can be confusing. Price inflation in the United States is intentionally made confusing. That keeps the public ignorant and poorly prepared to interrupt grand larceny and elite control of the printing press, the result of which has been a few decades of hidden confiscation of Middle Class work, wealth, and dreams. Long-term bond yields have many fundamental reasons why they should fall lower in the United States . They are interwoven and integrated. The US Economy is being killed by rising costs, in no way justifying higher borrowing costs. Yet amateurish opinions seem to coalesce in an absurd consensus. The Asian renaissance contributes mightily to both the impoverishment of America and its economic stagnation. Anyone who believes the US and Europe should share a consistent rhyming monetary policy is asleep at the analytic wheel. In the zero-sum game that is currencies, higher prices in the United States come with lower prices in Europe . Refer to marginal incremental movement in prices.

MONETARY INFLATION VS PRICE INFLATION

My personal observation of the entire inflation debate is one of awe, for the ignorance is beyond description. Neither the public nor the financial community has a clue what inflation is, how it affects the US Economy, how it should price bonds, how it produces imbalances. A smirk comes when an email hits my in box asking about inflation versus deflation. My answer usually covers a few key economic items and how each is subject to rising prices or falling prices. Lost is the meaning of inflation, which is the increase in money supply above and beyond economic growth. My favorite example to clarify that price inflation is not simply rising prices comes from the orange example. If frost hits Florida and the orange crop is partially ruined, higher market price for oranges is a basic response to reduced supply. Demand might drop a little, but supply dropped a lot, and price fires higher. That is supply & demand doing its job, and in no way related to inflation. Crude oil nowadays is suffering from reduced supply of easy deposits once available in older huge oilfields, higher degree of difficulty for newer production areas like deep water and remote locations, almost weekly bandit interruption of important production zones, not to mention the outright treachery displayed by certain energy warlords (see Putin, Chavez , Nigeria ). Thus supply & demand dictates a higher oil price, against a backdrop of a thoroughly decimated US Dollar in which it is priced.

The US financial markets have become a comedy. Investors jump with the slightest jawboning from central bankers as though they possess wisdom, as though they understand the hellish outcome wrought by their failed financial engineering, as though they actually have ANY policy options left. US central bankers, which include the rookie chairman, the governors, and the regional presidents, are as scared witless as they are hopelessly lost. They have become inflation apologists, struggling to explain how staggering monetary inflation has produced staggering asset deflation, how a robust housing boom has produced a totally wrecked banking system, how the pursuit of low cost solutions in China & India has produced an ocean of failed debt instrument like derelict crafts cast among flotsam and jetsam. Their arguments have become replete with twisted logic, so much that if their brain stems were closely examined, they would likely resemble pretzels. Be sure, those stems are much smaller than we realize.

THE WALL STREET CONMEN

We are witnessing the destruction of the US financial foundation to its very core, with most of its appendages wrecked as well. The bankers cannot offer any solutions except for the public till to rescue them before they become abject paupers. The have become beggars on the political steps, offering no wisdom, only blueprints for rescuing their own hides. Amazingly like today, Bernanke and Paulson each were on the receiving end of bootlicking by Congressmen, when they should have been vilified. They propose taking more control of the system, when they have destroyed the system. They act as authorities still, when they should be defendants in grand larceny and grand fraud cases before the world court. When the Wall Street human wrecking crews come before the US Congress to propose solutions, they might better spend their time to explain how their financial engineering failed and why they should not be banned from all government and regulatory posts. The public cannot bail them out as taxpayers. The bills will continue to be paid by foreign investors via credit supply. What they refuse to pay, the US will rely on the ultimate quicksand to print counterfeit money, which will deliver the next severe blow to the US Dollar The foreign wealth centers have begun to shun the US Dollar and US Treasury, except for the Arabs, who harbor some last drop of pity for their military master keepers, all part of a vast protection racket.

THE GREAT CENTRAL BANK SCHISM

A split has occurred. The Europeans have forged their own path. The Americans are on their own, more isolated than in their recent 40-year history. So the Germans and Trichet want higher interest rates.

What they might be thinking is that a still higher euro exchange rate can reduce the actual cost of commodities, from energy to metals to paper to grains. The lower cost comes from the strong euro currency discount. Such is the vagary of the Competing Currency Wars , which seemingly nobody discusses anymore even as it heats up like never before. Meanwhile, back in the Untied States or Untied Snakes or Uppity Snoops, the benefit that Europe realizes in cost smacks the Americans in the face as higher prices. As the US Dollar falls, or even stays depressed here, the practical effect is for a broad powerful deep increase in costs throughout the US Economy At the same time, the US Economy has failed to invest in energy supply, metals supply, or much of any other supply properly, including ethanol and grains, which has harmed its entire supply chain enough to cause a higher price response. SINCE WHEN IS THAT INFLATIONARY??? Robust increase in the cost structure without matching wage gains stands as the most utterly obvious and powerful basis for economic recession imaginable. As the two great Western continents go their separate course, why would anyone expect their two government bond markets to be coordinated? Not only is the US split from the European Union in crucial policy and self-destructive behavior, but Europe itself is split. This is covered in the Hat Trick Letter July upcoming Gold & Energy Report. Welcome the Latin Euro, a real possibility. Otherwise, why would Germans deny redemption of Spanish or Italian government bonds into German Bunds?

PLANNED US MIDDLE CLASS IMPOVERISHMENT

The primary objective of US central bankers is to keep wages down. Think about what that means. Their primary objective is to prevent Americans from being in a position to pay for rising cost of living, which translates into impoverishment and often insolvency, eventually many bankruptcies.

The ruling elite in the US has for three decades looked to Japan and the Pacific Rim in the 1980 decade, the Mexicans in the 1990 decade, and the Chinese & Indians in the 2000 decade to reduce their corporate cost structure. We have seen capitalism at its best, but in the process, an abandonment of US workers, a knife in the heart of US labor unions, and a relentless decline in the Middle Class wealth of the nation. This is the primary objective of the ruling elite, who work in close concert with their subordinates, the central bankers and other bank leaders.

Nowhere has the impoverishment of the US worker been more plain that the invitation to subcontract US industrial needs to China . Nowhere has the spread of poverty to US Middle Class been so obvious, blatant, and vicious than the refusal to permit wages to rise. Central bankers call it ‘Secondary Inflation Effects' in queer tone. The plan has been to passively permit costs to rise from a falling US Dollar while actively blocking wages from rising. Nowhere has the hypocrisy been thicker among US banking and political leaders than to talk about a ‘Strong Dollar Policy' as the primary directive and boast of export gains out of the side of their mouths.

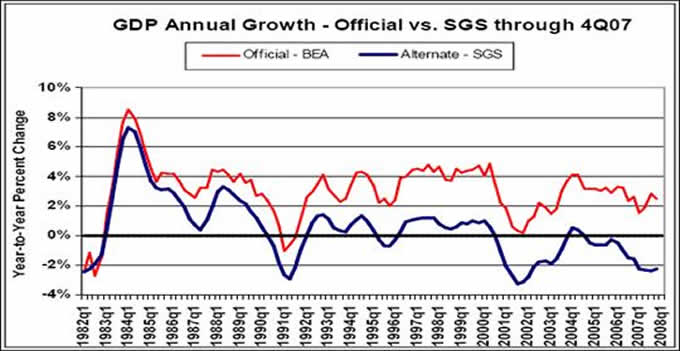

The grant of Most Favored Nation status to China in 1999 opened the door to Asia . It closed the door on America . The Shadow Govt Statistics folks do great work. One can rely on them to provide clean data series during dirty times for economic growth (shown below) in the Gross Domestic Product, for the price inflation, for the unemployment rate, and for the money supply growth rate. Notice the chronic US Economic recession that began to show in 2001, and has returned in 2004. It coincides with the stock bust in 2000 and the emergence of China in 2003. As their savings account has grown to over $1800 billion, the impoverishment of the United States has dovetailed in occurrence, as debts rose in staggering fashion. As long as China & India are prominent players, expect continued recession and extremely sluggish economic activity in the United States . Their gain is our loss. Their job creation is our job loss. Their growth comes at the expense of our recession. It is that simple. China stands as the biggest external reason why bond yields should remain flat to down, as they impose a profound wage and price ceiling in the US Economy In fact, it has locked the Untied States in a recession ever since year 2001, except for one or two quarters.

Notice that since China achieved the Most Favored Nation status in 1999, the US Economy has had only one or two quarters of positive growth, according to the SGS data. The US Economy has been stuck in horrendous mud for over seven years, the heavy penalty from globalization. That trend is defined as exploiting cheap Chinese labor and sending components across vast oceans at great energy expense before final assembly, then sending finished products across the same oceans again at great energy expense. Has anyone figured out that higher crude oil prices could be a result of globalization's horrendous inefficiency? Now there is a waste of oil. The effect on the US Economy has been a backfire, as many higher shipping and distribution costs are directly attributable to the globalization theme. If the US built what it needed in regions near where the products were delivered by people who used their own output, then less energy would be wasted in transport and prevalent wages would enable their purchase. That is logic too simple for total moron US economists, the stupidest breed of two-legged animals on the planet.

THE GREAT HIDDEN TAX

In the Hat Trick Letter Special Report entitled “The Schizophrenic Bond Market” a detailed but not comprehensive analysis is given for the troubled and confusing US Treasury Bond market. To be sure, price inflation has risen tremendously in recent months. However, it has done so on the cost side without benefit of wage increases to households or much pricing power to businesses. Thus, the inflation has a net suppressive effect on the US Economy like a giant tax, since it shows up on the cost side of the economic ledger.

Analysts understand tax hikes to push toward recession, but miss how cost inflation does the same. Many reasons are provided, ten in a list within the report, as to why long-term US Treasury Bond yields should remain flat to down in the intermediate term. The 10-year US TNote yield deserves close watch, since its chart pattern might be showing a hint of powerful upward bond yield move. JP Morgan stands as the biggest interventionist reason why bond yields should remain flat to down, since they have essentially destroyed that market. Imagine a gorilla at your dinner table every night, as parents pursue a balanced diet for their children. Your children will tend to lose weight, just as the USTBond's will fall in yield.

CONFIRMATION IN BY SHORT-TERM USTBILLS

The confirmation of lower sustained US bond yields, NOT higher, has come from both the 1-month US Treasury Bill and 2-year US TBill. Since the US Fed was unmasked at their last FOMC meeting, exposed on their bluff of inflation vigilance, the short-term US TBill. yields have come down, especially the 1-month. It flirted with 3.0% on the actual FOMC debutante ball event, where Young Benjamina not only failed to wear a nice gown, but she wore nothing at all. Since then, the 1-month TBill yield has slipped down to below 2.5% incredibly. That takes pressure off the rate hike. The 2-year US TBill. yield has come down below the magic 2.0% mark and has come down to below 1.5% incredibly. That actually puts pressure to cut rates by the US Fed, who have almost as little control as they have credibility. Bear in mind that the US Fed and their megaphone are rarely known to speak either words in sensible language or plain truth. Their job is to obfuscate. When they cannot raise interest rates to defend the beleaguered US Dollar, they talk about vigilance. When they have no policy options left to address rising prices, they hint of rate hikes. Their credibility is nil, a subject addressed in the July Hat Trick Letter Macro Economic Report out yesterday.

TEN KEY FACTORS KEEP BOND YIELDS DOWN

In the shizophrenia Special Report, ten reasons are provided in a list as to why long-term US Treasury Bond yields should remain flat to down in the intermediate term. They are tracked from diverse arenas and sources, some of which are mysterious. In my view, they are compelling. The consensus expectation of higher long-term bond yields in my view is incorrect. The only way that they could rise substantially is if a global boycott becomes deeply rooted, and the Untied States simply cannot any longer fund its capital requirements. In other words, the world might permit the US to fail financially, but at a great cost to themselves from reserves wealth stored, banking system foundations, and a lost market for exports.

• The rising costs have resulted in squeezed profit margins, squeezed households, depleted wealth, and broad bankruptcies. The great untold story is that wages have fallen since 2003, like over 25% on an inflation adjusted basis in the United States .

• Recession outcomes lift USTBond's The most profound elements of the US Economy are a housing market bust, a mortgage bond debacle, an insolvent banking system, tightened credit supply, evaporation of commercial bank paper, grotesque debt collapse, and ruined confidence. Hardly a combination urging to hit of the brakes with higher long-term bond yields.

• Funds flow from stocks to bonds typically occurs in cyclical rotation. Corporate profits are on the decline, as are most estimates for future quarters. That harms stocks. When US banks begin the orchestrated liquidation process this late summer or early autumn, a flight to perceived safety will occur into USTreasurys.

• Many bond spread trades are anchored in USTreasurys. They involve mortgage spreads, corporate spreads, emerging market spreads. All have widening bond differences, as many are being unwound. The process requires buyback of the USTBond anchors, a strong demand in the cover to unwind.

• The monstrous JP Morgan credit derivative book keeps the lid on long-term USTBond's They comprise 85% of the total credit derivatives. They are not subject to ordinary accounting rules, a license to corrupt markets and commit fraud. The behemoth remains very actively to keep long-term rates down by using basic and exotic credit derivatives.

• The most powerful reason is the strong Chinese presence in global trade has an enormous effect on the all important labor market. Together with India , the two nations create a vast ceiling on labor wages for the majority of manufacturing industry and a sizeable slice of service industry. The US Economy is held firm in a constant state of sluggishness and recession.

• Back in the 1990 decade, the ‘Bond Vigilantes' as they were known, had a powerful role in the bond market. They are not a dying breed. Vigilantes see the price inflation as embedded in costs, thus pulling the US Economy deeper into recession. Vigilantes are buying USTBond's

• An unorthodox reason (more a personal tool) is that a certain group of analysts forecast higher long-term US Treasury Bond yields. They tend to offer carefully articulated, but wrong forecasts. They tend to have vested interests in the system. They have a bad track record.

Other reasons appear in the Hat Trick Letter, related to petro-dollars and more. Too little time and space. Gotta go. The Special Report goes into much more detail. It includes a brief technical analysis of the 10-year US Treasury Note yield (TNX). A potential powerful reversal pattern is presented, one that must be watched closely. A rising Head & Shoulders pattern must be watched for. If it exerts itself in a reversal lift of bond yield, a move up in the TNX yield could shoot up toward 5.2% in the next few months. No immediate threat for an upward breakout is yet evident. Watch to see if the TNX falls below 3.8%, its neckline support. If the 10-year bond yield goes below that level, the H&S pattern is busted, and the TNX will again test lows. Given its downward momentum, and how cyclical indicators on a weekly basis in no way show exhaustion of the decline in yields, look for the reversal pattern to break down soon. My forecast is for the TNX to retest 3.5% by autumn, when the panic starts.

The Special Report goes into more detail also about JP Morgan, the pit bull on Wall Street, defender of the ‘Garbage Can' that is alive, full to the brim, whose stench is offshore just like the rancid effluent stench associated with Enron. Bear in mind that JP Morgan taught Enron all they knew, while Arthur Anderson looked the other way and was blamed for the entire mess. Back then the corrupt financial device was the Special Purpose Entity. Now Wall Street prefers to deploy a revolving door of identical illicit devices with changing names like Structured Investment Vehicles, Variable Interest Entities, Unidentified Financial Objects (my favorite UFO), and more. Be amused, don't be fooled. The mess today in the Shadow Banking System is directly related to the failure of Enron-style devices that never went away. JP Morgan is the secret weapon for keeping down long-term US Treasury Bond yields. They do so in order to prevent the entire US banking system from imploding. They defend the risk price model. The other side of the shadow banking system operating on US soil derives funds from the Afghan product, another scummy story at times hinted, but never in detail, always steeped in darkness.

APPENDIX ON SILVER

Hardly unrelated to the decline in US Treasury yields since the last FOMC meeting in late June, the gold & silver prices have recovered nicely. They have set the stage for a powerful upward move. The other stage is being fully designed and planned for a pulled plug on several major US banks. A panic is coming within a couple months possibly. The precious metals have responded, and will continue to respond.

The silver chart displays a Double Cup & Handle reversal pattern. Some call it a W-shaped reversal pattern. If the 18 level holds for silver upon consolidation after a strong move since the June FOMC meeting from 16.50 up by 10%, then look out above! A quick assault on the 20 level is assured. Also, even as the US Dollar found some lift after the euro gave back 200 points from 158.5 to 156.5, silver held on strong. In fact, the euro shows a similar W-shaped reversal pattern. It is analyzed in the second July Hat Trick Report, with plenty of fundamental factors as well. The base for silver and gold have been constructed, enough to serve as a strong base for a powerful upward summer and autumn move in price. My long-term silver price forecast is 50 before year 2010 is over.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

“Your unmatched ability to find and unmask a string of significant nuggets, and to wrap them into a meaningful mosaic of the treachery-*****-stupidity which comprise our current financial system, make yours the most informative and valuable of investment letters. You have refined the ‘bits-and-pieces' approach into an awesome intellectual tool.” - (RobertN in Texas )

“I am astonished at the level and depth of your writing. There is, to my knowledge, no one who comes close to your commitment to finding the truth and putting it out there for us. I am hooked. You tower above your competition. Keep it up.” - (DavidP in Florida )

“Your reports scare the hell out of me every month, probably more so over time, since so many of your predictions have turned out to be very accurate. I am afraid you might be right that by the end of 2008, we are in a pretty severe situation, with civil unrest and severe financial stress on Main Street .” - (GeorgeC in Minnesota )

“You are able to consume and regurgitate complicated information into layman's terms. It shows that you understand your subject well. It is very easy to take complicated material and repackage it as complicated material. You, however, have the ability to take the complicated and make it understandable to the common man.” - (RickS in California)

by Jim Willie CB

Editor of the “HAT TRICK LETTER”

Home: Golden Jackass website

Subscribe: Hat Trick Letter

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by compromised central bankers and inept economic advisors, whose interference has irreversibly altered and damaged the world financial system, urgently pushed after the removed anchor of money to gold. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy.

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 25 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.