Why Krugman, Roubini, Rogoff And Buffett Dislike Gold

Commodities / Gold and Silver 2016 Sep 30, 2016 - 02:44 PM GMTBy: GoldCore

By Jan Skoyles Edited by Mark O’Byrne : A couple of weeks ago an article appeared on Bitcoin Magazine entitled ‘Some economists really hate bitcoin’.

By Jan Skoyles Edited by Mark O’Byrne : A couple of weeks ago an article appeared on Bitcoin Magazine entitled ‘Some economists really hate bitcoin’.

I read it with a sigh of nostalgia. As someone who has been writing about gold for a few years, I am used to reading similar criticisms as those bitcoin receives from mainstream economists, about gold.

As with bitcoin, gold is just a step too far for many economists. Criticism is often, as with bitcoin, targeted at the people who invest in it, rather than the asset’s own track record, fundamentals and safe haven attributes – classic attacking the ball and not the man.

This frequently involves name calling and the pejorative ‘goldbug’ label. This is used to try and discredit anyone who says anything positive about gold including being bullish on the price or seeing it as an important diversification. Often some of the gold naysayers refuse to distinguish between gold as a diversification in an investment or pension portfolio and gold’s role as a hedge against currency devaluations on one side and on the other calls for a gold standard.

Two completely separate matters – one pertaining to monetary policy and the other to investing, saving and personal finances.

In my experience to invest in gold is seen by the critics as the ultimate rejection of central banks, financial systems and government. These critics believe that faith in something that just gets mined out of the ground is baseless compared to something that ‘involves human endeavors (like stocks)’ as Joe Weisenthal of Bloomberg argued.

This ignores the fact that the production of gold, refining of gold, minting and fabricating of coins and bars and indeed the brokering, delivery and storage of bullion, and the running of the myriad of different precious metal companies involved in this quite large industry involves human energy, innovation and endeavours.

Below I touch upon some of those critics who continue to dismiss either gold as an investment or as a form of money which may play some role in the monetary system.

Nobel Prize Winning Krugman

If anyone could be accused of having a caricature of gold, it would be Paul Krugman. For him, gold investment is a push for the gold standard and anyone who advocates diversifying into gold is a lunatic, right wing “gold bug”.

Krugman most recently riled fans of gold when he went after Republicans during candidate nominations and mocked their apparent desire to return to a gold standard. (Despite it being a Republican who ended the gold standard).

What Krugman failed to acknowledge was that the push for gold in the financial system is not just coming from a the “Tea Party” movement and a bunch of Republican voters, but rather it is coming from the East – from China and the People’s Bank of China and indeed the Russian central bank who are buying up all the gold they can.

It’s coming from Western investors who are looking for a hedge against economic risk and for portfolio diversification. It is coming from countries who still see gold as a form of money and a safe haven, such as the people of India and people in Germany and Switzerland in Europe.

When asked why he celebrated the fall of the gold price in 2013 he told Business Insider:

“Well, the inflationistas/goldbugs are really, really annoying — all this air of having the secret wisdom when they actually haven’t a clue. And they have been a real destructive factor in policy debate, standing in the way of effective policy by raising fears of Weimar and Zimbabwe. So seeing the one thing they got right — betting on higher gold prices — turn sour is cause for a bit of celebration.”

To be fair, the gold price had fallen sharply in 2013 but Krugman ignored the performance over the medium and long term – a cardinal sin in investing which should always be about the long term.

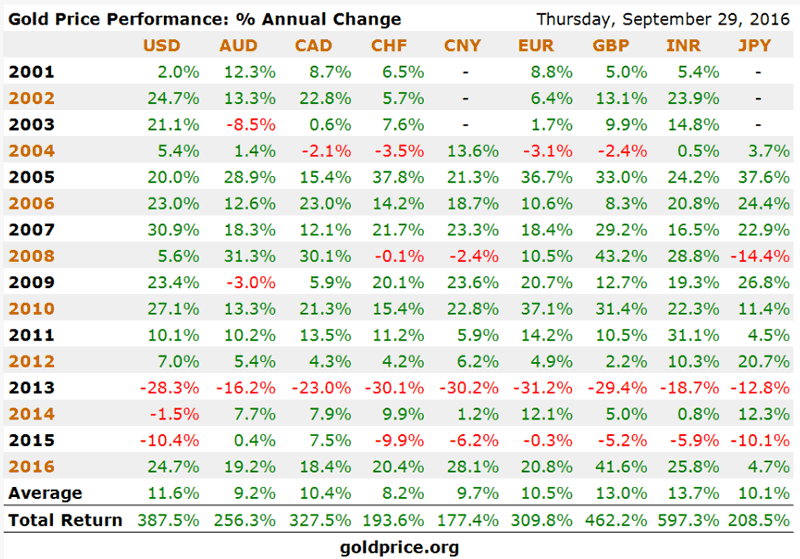

Even at the end of 2015 when a few of us were doing some soul-searching and asking ‘did we miss something? It wasn’t as though we had returned to the days of a few hundred dollars per ounce. Gold and silver were some of the best assets to hold before, during and after the global financial crisis. Gold rose every single year from 2001 through to 2012, prior to the sharp correction in 2013. Gold rose in all fiat currencies – none of which acted as a safe haven during the financial crisis.

Gold acted as a hedge during the crisis when most property, stock and bond markets had seen sharp falls. When these markets stabilised and began to recover, gold prices fell. Exactly what a hedge should do.

This year gold and silver prices were up 26% and 38% respectively, in the first half of the year and have consolidated on those gains in Q3, 2016.

Stocks in many markets have come under pressure in 2016 – especially in Japan and Germany and some currencies have been devalued including the British pound after Brexit. Gold is acting as a hedge again in 2016 – exactly when investors around the world need a hedge.

To my knowledge Krugman is yet to address this year’s gold performance. The last time he did try to explain the bull-market in gold (early September 2011) he dismissed the idea that it was because of inflationary concerns. But for some reason used numbers that exclude inflation to support his argument.

He did, however make the valid point (which I entirely agree with) that “because expected returns on other investments have fallen” is why more people were buying gold. Yet given near negative and negative interest rates today, and the fact the “expected returns” on deposits, bonds and indeed the entire pensions complex “have fallen”, you would think that Krugman might now understand and concede the value of diversification an allocation to gold in a diversified portfolio.

Ideologues of the right and the left never allow the facts to get in the way of their arguments.

Oracle of Omaha, Warren Buffet

Warren Buffett is not an economist but you can guarantee that more investors pay attention to the Oracle of Omaha’s views than the majority of those economists – particularly statist ideologues.

Buffet has even debated with Marc Andreeson over bitcoin. Many believe that he dislikes bitcoin, but this may not be the case, he may just see it as a development in the world of payments – an upgrade from writing a cheque or sending a wire transfer. It is not ground-breaking stuff.

Where Buffet’s problem with bitcoin lies is exactly where it lies with gold – he fails to see the intrinsic value of it. Bitcoin is ‘not a currency’ it is a ‘mirage’ according to Buffett.

When interviewed by CNBC in 2009 he said of gold “… it’s a lot better to have a goose that keeps laying eggs than a goose that just sits there and eats insurance and storage and a few things like that,” he said. “The idea of digging something up out of the ground, you know, in South Africa or someplace and then transporting it to the United States and putting into the ground, you know, in the Federal Reserve of New York, does not strike me as a terrific asset.”

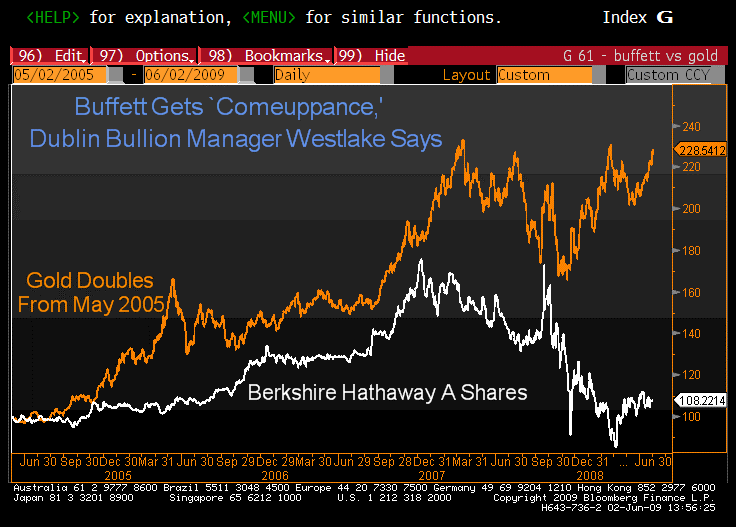

At the beginning of the year Berkshire Hathaway increased its shareholding in oil refining company Philips 66 to 13.7%. This was seen as a bet on oil prices. The company had chosen to ignore the current top performing commodities that were gold and silver, and the shares of Berkshire Hathaway were underperforming in comparison.

In 2009, prior to gold going parabolic from 2010 to 2012, GoldCore also pointed out how gold has performed Berkshire Hathaway over a 4 year and a 10 year period. We pointed out and were quoted by Bloomberg how gold’s utility was simply “in balancing a portfolio.” We said that the point is that gold had “preserved a chunk of wealth that would have been otherwise taken down with other financial instruments,” see here.

The Daily Reckoning also pointed out “an investor who purchased gold at any time after January of 1998 would have received a higher investment return over the following 10 years than an investor who purchased Berkshire Hathaway.”

This is not to suggest that Berkshire Hathaway has not been a great investment for its owners – it has. Rather it shows that there are periods of time when gold outperforms most, and frequently all, other investments and hence its importance as a hedging instrument and a safe haven asset.

Dr. ‘Doom’ Roubini

We have some respect for Dr Roubini as a macroeconomist and have indeed shared many of his concerns in many years and shared them with our clients and the wider public as long ago as 2005 and 2006 when he and we warned that the US would soon follow in Iceland’s footsteps and have its own financial crisis. However, giving financial advice is not his expertise and he may be better suited focusing on his strengths.

As Roubini is regarded as a guru by many experts and opinion makers internationally, there is a real risk that his opinions regarding gold could lead to poor and imprudent investment decisions.

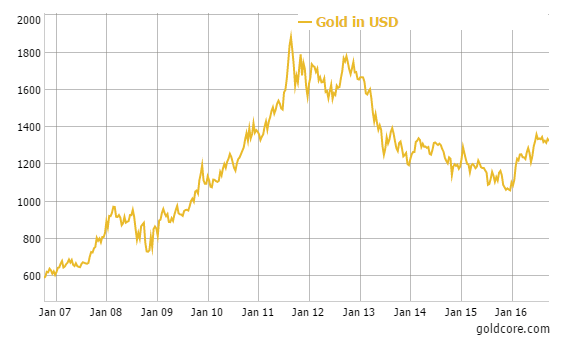

In December 2009, when gold was at $1,100/oz, he said that “all the gold bugs who say gold is going to go to $1,500, $2,000, they’re just speaking nonsense.”

In the following years gold rose to over $1,500/oz and nearly reached $2,000/oz when it surged to $1,915/oz in 2011.

One of our clients actually sold their gold allocation on the basis of this statement. Despite gold being the one asset class that had protected them in the early stages of the crisis in 2007, 2008 and 2009. Gold nearly doubled after Roubini’s pronouncement.

Gold in USD – 10 Years

In August, 2013, when gold has already fallen in price and was trading at $1,300/oz, Roubini predicted that gold would fall another 23%, back to $1,000. Not only that but he said that this would happen “at the end of next year”.

Reasons given were that: “Now with the economy recovering, nobody wants to be in rocks that don’t pay any dividends. Real interest rates are rising. That kills gold…Governments with debt issues are selling gold…Gold was juiced by right-wing fanatics in the US. That boom is over… gold remains John Maynard Keynes’s “barbarous relic,” with no intrinsic value and used mainly as a hedge against mostly irrational fear and panic.”

Where to start with this logic and poor analysis? There has not been an economic recovery of real substance, real interest rates do not appear to have risen and the gold price has performed quite well over the medium and long term. Gold has gone sideways after a period of multiple annual yearly gains.

To be fair, it is difficult to call Roubini an all out gold-hater as he does suggest that “all investors should have a very modest share of gold in their portfolios as a hedge against extreme tail risks.” However, he doesn’t think it’s crucial and that “other real assets can provide a similar hedge, and those tail risks – while not eliminated – are certainly lower today than at the peak of the global financial crisis.” Given the deteriorating financial position of systemic Deutsche Bank, Roubini may need to revise that assumption soon.

Roubini has been very vocal in his anti-gold stance. Indeed, he has even engaged in Twitter wars with GoldCore’s Mark O’Byrne and James Rickards, over the gold standard.

There is little doubt that Roubini is a very smart economist, however he just cannot get to grips with the role of gold. Describing those who like gold as ‘gold bugs – a combination of paranoid investors and others with a fear-based political agenda.’ He likes to throw gold and bitcoin fans into the same category. He tried to engage Jim Rickards and goldbugs in Twitter war back in April 2013. When Rickards pointed out a few truths about the gold price he turned his attentions “Gold-bug suckers found another irrational useless bubble fad, the Bitcoin, the bubble flavor of the day. So they are dissin gold 4 Bitcoin.”

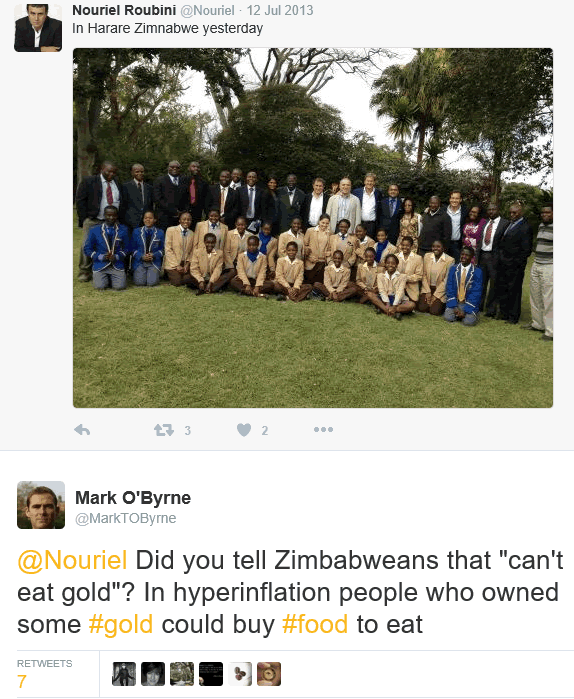

Roubini has also resorted to the silly old argument that “you can’t eat gold” and said that: “If you want to hedge against inflation, stock up on Spam or other canned food”

Ignoring the somewhat obvious fact that you cannot eat any investment or currency – whether that be stocks, bonds or dollars, euros or pounds. Unlike, spam and canned food, gold is one of the most traded assets and liquid investments in the world – especially in a crisis. There is always a market for gold and it can always be exchanged for cash or indeed used to buy food, farms, property and businesses. A cursory analysis of gold’s performance in economies suffering financial and economic crisis would show Roubini the value of gold as a currency hedge and indeed a hedge against systemic contagion in an economy.

Thus, Roubini has a questionable track record when it comes to gold and his arguments against it are poor.

Rogoff

In many ways I have saved the best until last, but at the same time wish to not say too much here as I have a further article planned around the Grand Chess master, American economist, Kenneth Rogoff.

Many of you will recognise the name as his latest book ‘The Curse of Cash’ was released over the summer. As someone who straddles both the fintech world as well as the gold world I am used to the push for a cashless society.

Going cashless is seen as the new sexy side to financial services as it is purported to prevent bad things happening with money and will allegedly empower the poor of the Developing World and the unbanked. Save your scoffing, I’ll deal with those claims in my later article.

For Rogoff the clamp down on cash would be beneficial because of its impact on money laundering and tax evasion. Why would this mean that he is against gold? It might not. In fact he has quite prominently appeared to support gold (or at least not dismiss it) earlier this year.

In May, writing on Project Syndicate he outlined how emerging economies should shift their US dollar reserves entirely into gold, praising it as ‘an extremely low-risk asset with average real returns comparable to very short-term debt.’. He argued that emerging economies should ignore the West’s push to demonetise gold, ‘There has never been a compelling reason for emerging markets to buy into the rich-country case for completely demonetizing gold. And there isn’t one now.’

But, in a recent interview to promote his book he told CNBC that there was a need to clamp down on assets that could be used instead of good, sturdy fiat money, ‘“You have to play whack-a-mole with all these things,” he stated during a recent appearance on CNBC. “There are always going to be these other things: gold coins, uncut diamonds, [and] now bitcoin.”

‘These other things’ are real, tangible assets (forget bitcoin for now). They allow freedom of movement, of purchases and there can be significantly less counterparty risk than when using fiat money. The push for a cashless society, for all the talk of fighting crime, is really to support the banking system.

As we outline in our upcoming/recent report on bail-ins. The push for a cashless society will help to support the new bail-in regime. With assets such as gold, bail-ins become trickier and not as straightforward as using customer deposits to prop up a failing bank system.

Rogoff dislikes gold because it removes power from the banking system within reach of tax strapped governments, and puts it back in the hands of the saver who opts to save in gold bullion rather than fiat, electronic currency.

In this vein, libertarian academic economist, Saifedean Ammous, wrote on Twitter

“Statist economists hate Bitcoin for same reason taxi drivers hate Uber: it frees the rest of us from their bull$h*t …”

How true. Substitute the words Bitcoin for gold and it reads just as well if not better:

“Statist economists hate gold for same reason taxi drivers hate Uber: it frees the rest of us from their bull$h*t …”

Conclusion

Keynes once argued “gold has become part of the apparatus of conservatism and is one of the matters which we cannot expect to see handled without prejudice.” This is certainly true with regards to gold today and the many prejudices and lack of evidence based research regarding gold and its role as a hedging instrument and safe haven diversification.

“The modern mind dislikes gold because it blurts out unpleasant truths” said economist and political scientist Joseph Schumpeter. The unpleasant truth today is that today’s financial and monetary system is fragile in the extreme and likely to suffer another financial crisis very soon.

For all of those mentioned above the main dislike for gold appears to be due to a combination of a lack of understanding and the desire to keep the unsustainable status quo going. A surging gold price frequently makes their analysis and prognosis look bad. In the case of Buffett, were a the ‘chunk of metal’ gold to outperform his Berkshire Hathaway shares his God-like ‘Oracle’ status would be questioned.

In the words of my karaoke go-to Taylor Swift “Haters gonna hate, hate, hate …”

Gold Prices (LBMA AM)

30Sep: USD 1,327.90, GBP 1,025.01 & EUR 1,187.67 per ounce

29Sep: USD 1,320.85, GBP 1,016.92 & EUR 1,177.14 per ounce

28Sep: USD 1,324.80, GBP 1,020.10 & EUR 1,181.06 per ounce

27Sep: USD 1,335.85, GBP 1,031.01 & EUR 1,187.84 per ounce

26Sep: USD 1,336.30, GBP 1,033.23 & EUR 1,188.91 per ounce

23Sep: USD 1,335.90, GBP 1,027.17 & EUR 1,192.16 per ounce

22Sep: USD 1,332.45, GBP 1,019.59 & EUR 1,186.68 per ounce

Silver Prices (LBMA)

30Sep: USD 19.35, GBP 14.92 & EUR 17.33 per ounce

29Sep: USD 19.01, GBP 14.61 & EUR 16.95 per ounce

28Sep: USD 19.12, GBP 14.69 & EUR 17.05 per ounce

27Sep: USD 19.42, GBP 14.99 & EUR 17.26 per ounce

26Sep: USD 19.44, GBP 15.04 & EUR 17.29 per ounce

23Sep: USD 19.82, GBP 15.28 & EUR 17.66 per ounce

22Sep: USD 19.88, GBP 15.22 & EUR 17.69 per ounce

This update can be found on the GoldCore blog here.

Mark O'Byrne

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.