Gold Is Undervalued Say Leading Fund Managers

Commodities / Gold and Silver 2017 Feb 17, 2017 - 09:42 AM GMTBy: GoldCore

Gold is undervalued according to a record number of fund managers

Gold is undervalued according to a record number of fund managers- Last time gold was considered undervalued, the price surged

- BAML surveyed 175 money managers with $543 billion in assets under management

- 34% of investors believe protectionism is the biggest threat to markets

- Gold viewed as the best protectionist investment by a third of investors

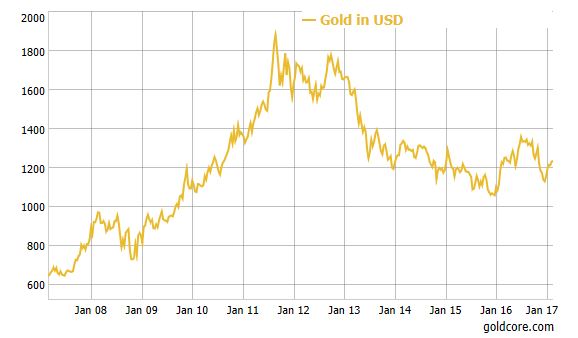

Gold in USD – 10 Years (GoldCore)

For the third time in a decade fund managers surveyed by Bank of America Merrill Lynch (BAML) believe that gold is undervalued. After the last two occasions the price of gold shot up.

The Bank of America Merrill Lynch Fund Managers survey spoke to 175 money managers with $543 billion in assets under management. It provides key indicators each month of those who run and manage the world’s investments. The news that they are buying gold and believe it is undervalued, is worth paying attention to.

As we often mention the status quo amongst money managers is for them to be bearish about gold, regardless of the price and state of the global economy. But this month, a majority of those surveyed (by a net margin of 15%) believe that gold is a buy, something that hasn’t been seen since January 2009 and January 2015.

As Brett Arends writes on Marketwatch, this is significant:

“The latest survey opinion is of more than passing interest. These guys typically do not hold gold in their portfolios. Indeed, to buy some, most of them will have to go through investment committees, which takes weeks or months. But if they are interested, and they stay interested, that will presumably drive more demand for gold as an investment in the months ahead.”

But why are they only interested now, what has them running for gold and what does this mean for gold investors?

Inflation, stagflation and protectionism

The interest in gold comes from two parts.

Firstly the clear risks on the horizon. Namely stagflation, inflation and protectionism. As well as rising interest rates and potential conflict (trade and otherwise) around the world. The second part is our increasingly familiar friend, uncertainty.

This may come as a surprise given the boost to economic projections thanks to Trump’s win. But even an initial enthusiast of Trump’s policies Ray Dalio, head of the world’s biggest hedge fund, Bridgewater Associates, has since changed his mind. In a recent letter to clients he explained:

“Nationalism, protectionism and militarism increase global tensions and the risks of conflict. For these reasons, while we remain open-minded, we are increasingly concerned about the emerging policies of the Trump administration.”

In the BAML survey, fund managers are optimistic about the macro outlook, with 23% saying they expect a “boom” compared to 1% one year ago but when it comes to the fundamentals things don’t look so good, with 43% saying they expect “secular stagnation”.

36% said European elections raising disintegration risk were the biggest tail risk closely followed by a trade war (3%) and a crash in global bond markets (13%).

The most likely bear market catalyst according to 34% of respondents was protectionism, followed by higher rates (28%) and a financial event (18%).

So whilst things might be looking rosy at the moment, the future is making investors’ nervous. It is the uncertainty surrounding these potential events, not knowing what specifically they will be, what they will impact and when they might happen that adds to list of unknown uknowns that we were talking about earlier this week.

Trump trade could take you too close to the Sun

Staying too positive about Trump’s impact on the US and wider economy has lead some to issue warnings. Michael Hartnett the chief investment strategist at BAML and his team wrote of the Icarus trade, earlier this year.

“Our tactical view: after a Jan/Feb wobble, we believe stocks & commodities will have one last 10% melt-up in H1. Call it the ‘Icarus trade.’ The current melt up, which started back in Feb 2016, will be followed by a meltdown later in ‘17,” they wrote.

For those who need reminding Icarus was the son of Daedalus. When his father made him some wings held together by wax he was warned not to fly too close the sun, but Icarus ignored his father’s warnings and did just that. His wings melted and he plunged back to earth.

The decision by fund managers to go long gold is a reflection of this Icarus trade. These investors are buying gold as a form of insurance. In the same way that we should have insurance for our homes or cars but we just cannot predict the future, investors are now appreciating gold will do well when financial and political upheaval unexpectedly take a turn for the worst. However, this is a short-term perspective and many are saying that these fund managers are not looking at gold in the long-term, playing a crucial role in their portfolios.

Big money gets into gold

The news that fund managers are getting into gold should really come as no surprise, we have brought you multiple stories of wealthy investors, fund managers and family offices diversifying into gold.

In June 2016, gold accounted for 8% of the £2.8 billion portfolio managed by Rothschild’s investment house RIT Capital Partners.

Reasons for the portfolio allocation were given as

‘”The six months under review have seen central bankers continuing what is surely the greatest experiment in monetary policy in the history of the world. We are therefore in uncharted waters and it is impossible to predict the unintended consequences of very low interest rates, with some 30 per cent of global government debt at negative yields, combined with quantitative easing on a massive scale. In times like these, preservation of capital in real terms continues to be as important an objective as any in the management of your company’s assets.”

More recently we reported on Stanley Druckenmiller buying gold in late December and January, having sold on the night of the election claiming that “all the reasons I owned it for the last couple of years seem to be ending”.

However since then Druckenmiller has bought gold back seemingly because he too believes it is currently undervalued, he “wanted to own some currency and no country wants its currency to strengthen…Gold was down a lot, so I bought it.”

And just this week we brought an interview with Jim Rogers to you in which he warned investors to “Get prepared” as “we’re going ‘to have the worst economic problems we’ve had in your lifetime or my lifetime’. With this in mind he is holding onto gold and silver and is accumulating bullion on dips, looking to ‘own more’.

Conclusion: unconventional appeal of gold as insurance

Despite the apparent support of some investment managers this is seen as very much short-term and gold is still not seen as a conventional investment.

Coverage of this most recent BAML survey has picked up on this rekindled love for gold and generally writes that the metal is being bought as an insurance policy, as opposed to a key investment ‘mainstay’.

This idea suggests that there are times when it isn’t necessary to have gold in your portfolio.

The approach of the fund managers seems a funny way to look at things when you consider the long-term appeal and strength of the gold price. In the short-term the price does well during periods of declining confidence, as we are seeing now but in the long-term having an allocation to gold to gold in your portfolio has been shown to benefit the long-term performance, as we have written about in our investment guides.

These money managers who are now investing in gold as a sort-of short term insurance are certainty looking at things from a narrow focused perspective. This is something that Doug Kass drew our attention to earlier this year.

Kass quoted Howard Marks who wrote:

“First-level thinking is simplistic and superficial, and just about everyone can do it (a bad sign for anything involving an attempt at superiority). All the first-level thinker needs is an opinion about the future, as in: ‘The outlook for the company is favorable, meaning the stock will go up.’

However, Kass writes that to be good investors we need to engage in ‘second-level thinking’ which is ‘deep, complex and convoluted…The second-level thinker takes many things into account:’

Few assets seem to generate as much controversy as gold when it comes to mainstream investors and the media. Many like to point to Warren Buffet who argues that we just dig it out of the ground in order to store it in another hole in the ground. Critics like to argue that it offers no yield, no dividend, and is difficult to value according to modern financial theory.

Yet, interest in what is happening with the gold price and who is buying gold will always be covered by the mainstream. There is in an innate fascination with gold, but the majority only turn to it when it seems there is an obvious reason for it to climb.

The reason gold has survived so many years and performed so well is because there is no such thing as an intrinsic value calculation – too many elements feed into the gold price, and most of them are unknown until they occur. Hence why it performs so well during times of uncertainty.

Gold is money. It is a borderless currency that cannot be inflated, devalued or controlled by central bankers and politicians. Contrast that to the likes of the US dollar (and indeed the euro or sterling) which can fall victim to all of those things, and given Trump’s comments on the strong dollar, perhaps more than we have ever seen before.

Gold is undervalued at present and will no doubt benefit from the bullishness of these money managers. However it is not just undervalued and worth buying because people fail to appreciate the impact of protectionism, stagflation and inflation.

It is undervalued for many reasons, the main one is the lack of understanding of gold as a proven safe haven asset and of how well it performs during times of uncertainty.

Gold Prices (LBMA AM)

16 Feb: USD 1,236.75, GBP 988.41 & EUR 1,163.29 per ounce

15 Feb: USD 1,225.15, GBP 985.27 & EUR 1,161.81 per ounce

14 Feb: USD 1,229.65, GBP 986.67 & EUR 1,157.84 per ounce

13 Feb: USD 1,229.40, GBP 982.04 & EUR 1,155.64 per ounce

10 Feb: USD 1,225.75, GBP 980.23 & EUR 1,151.35 per ounce

09 Feb: USD 1,241.75, GBP 988.18 & EUR 1,161.04 per ounce

08 Feb: USD 1,235.60, GBP 989.47 & EUR 1,160.10 per ounce

07 Feb: USD 1,231.00, GBP 995.14 & EUR 1,154.43 per ounce

06 Feb: USD 1,221.85, GBP 978.34 & EUR 1,138.15 per ounce

Silver Prices (LBMA)

16 Feb: USD 18.10, GBP 14.49 & EUR 17.02 per ounce

15 Feb: USD 17.88, GBP 14.38 & EUR 16.93 per ounce

14 Feb: USD 17.91, GBP 14.37 & EUR 16.85 per ounce

13 Feb: USD 17.97, GBP 14.34 & EUR 16.89 per ounce

10 Feb: USD 17.62, GBP 14.15 & EUR 16.55 per ounce

09 Feb: USD 17.71, GBP 14.10 & EUR 16.58 per ounce

08 Feb: USD 17.74, GBP 14.20 & EUR 16.66 per ounce

07 Feb: USD 17.60, GBP 14.21 & EUR 16.49 per ounce

06 Feb: USD 17.60, GBP 14.10 & EUR 16.39 per ounce

Mark O'Byrne

This update can be found on the GoldCore blog here.

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.