Silver Production Has “Huge Decline” In 2nd Largest Producer Peru

Commodities / Gold and Silver 2017 Apr 19, 2017 - 02:16 PM GMTBy: GoldCore

– Silver production sees “huge decline” in Peru

– Silver production sees “huge decline” in Peru

– Production -12% in one month in 2nd largest producer

– Silver decline is due to ‘exhaustion of reserves’ in Peru

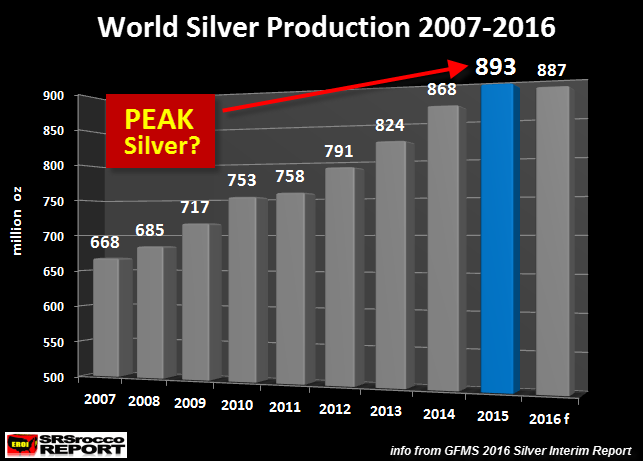

– GFMS recognise that ‘Peak Silver’ was reached in 2015

– Global silver market had large net supply deficit in 2016

– Silver rallied 13.5% in Q1 in 2017

– Base metal production accounts for 56% of silver mining

– Base metal demand under threat from global economy

– Own financial insurance of silver coins and bars

Investors and silver stackers should position themselves for falling silver production around the globe. Peru has just posed another 12% fall in silver production – Peak Silver is here.

SRSrocco Report has drawn attention to falling silver production in Peru and how this is likely to be echoed across the globe in the wake of the looming debt crisis in an article published yesterday.

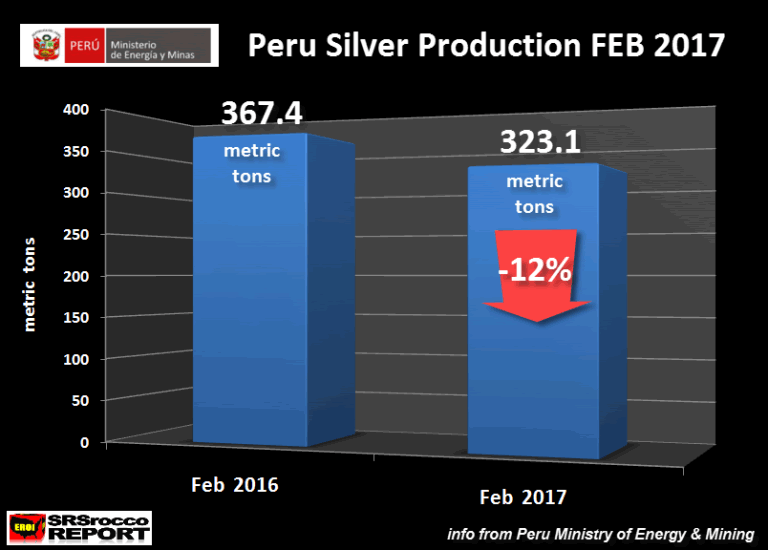

The world’s second largest silver producer, Peru, has reported a 12% fall in February’s silver production to 323.1 metric tons, from the same period last year.

As written about in SRSrocco’s report on the matter, Peru’s ‘silver production fell 12% to 323.1 metric tons (mt) this February versus 367.4 mt the same month last year.’

The author calculates that this is a fall of 1.5 million ounces (44mt) in just one month. The Peruvian Ministry of Energy and Mining explains the fall:

The decrease is explained by the lower results (-23.53%) of the main producer: Minera Yanacocha S.R.L. Whose operations in Cajamarca have been affected by an exhaustion of the reserves in the current deposits in operation.

Both GoldCore and SRSrocco have been bringing the issue of Peak Silver to the word’s attention. Concern regarding Peak Silver has yet to impact the silver market in a material way.

In 2016 the uptick in demand for silver was (according to GFMS) primarily due to safe haven demand but also due to ‘swelling concern about mine supply reduction in the future.’

This latest set of data from Peru confirms the declining situation regarding global silver supply. The situation in Peru is not unique, it is a story that will likely appear in many silver producing countries.

The story will not be about defining silver production because of silver price but because of its place in the much wider global economy – the impact of base metal mining, falling energy fuel levels and the damage the debt-laden economy will have on the sector.

Silver is a special metal – it is a hedging instrument, money and it is a valuable commodity. The nature of how it is mined means it is intricately tied to both the performance of the economy and other commodities.

Silver is 56% byproduct

Only 30% of silver is mined as a primary source, it is more often a byproduct of base metal production. 34% of silver production (in 2015) came from lead/zinc mining and 22% from copper.

According to the 2016 World Silver Survey, the biggest increase in silver production as a byproduct has come from copper mines, which saw a 7% increase 2015-2016.

Therefore, silver production is not just a matter of which mine is producing it and what the demand for the metal is at that time, but it is also affected by the global markets and their demand for the base metals. Base metal prices have taken significant hits in recent years thanks to the financial crisis and recently base metal prices have been falling as precious metal rose on concerns about economic growth and increased risk aversion.

Should copper demand decline, which it is likely to as we look ahead to an impending burst of the global debt bubble and slowing economic activity then silver production will also begin to fall.

An economic slowdown means reduced industrial demand for the base metals, which means some 56% of silver supply will be under threat.

Silver – an energy drain

We must also not forget that mining is not just about demand for the metals and their byproducts. It also takes a huge amount of energy to mine precious metals.

As SRSrocco explains in a November article, it takes a huge amount of fuel to produce base metals (and therefore silver).

…the Chilean Copper Commission stated in a 2014 report, that the country consumed 535 million gallons of liquid fuel to produce 5.7 million tons of copper. Thus Chile’s copper industry consumed 94 gallons of liquid fuel for each tonne of copper produced.

On the other hand, Pan American Silver burned 20.5 million gallons of liquid fuel to produce their 26.5 million oz of silver in 2015. Which means, each ounce of silver production took 0.80 gallons of liquid fuel. If we use Pan American Silver as a guide, then the 269 Moz of primary silver production in 2016 consumed 215 million gallons of liquid fuel. However, I would imagine the global primary silver production average is much less, more like 0.50 gallon per ounce of silver. So, we are talking about 135-150 million gallons of liquid fuel to produce all the primary silver in the world.

Now, the world produced a total of 18.4 million tons of copper in 2014. Taking Chile’s average of 94 gallons per tonne of copper produced and providing a conservative estimate of say 75 gallons per tonne for entire globe, then the world consumed roughly 1.4 billion gallons of liquid fuels to produce its copper in 2014.

This is about ten times the amount of fuel it took to produce all the primary silver production.

A financial collapse will see oil and energy fuels levels fall as there will be a global slowdown. Demand will fall as will production. Given what appears to be a rising cost in terms of the amount of energy used to mine base and precious metals, it is not a leap too far to estimate that silver production will fall further on account of falling energy stockpiles.

Physical silver deficit at 1.5 billion ounces

Falling mine supply means that there is a growing deficit in above ground silver stocks, as the demand for physical silver shows little respect for mining figures.

Since 2011 there has been an annual physical deficit of silver (the one exception was in 2012 when there was a surplus of just 2 million ounces). Between 2014 and 2015 the deficit grew by 60%. Since 2004 the total annual silver deficits are 1.5 billion ounces, judging by past World Silver Surveys.

This is exactly as it sounds, we are at Peak Silver and the situation is unlikely to improve. Even the mainstream is beginning to see and acknowledge it.

In the December release of the World Silver Survey GFMS stated:

• We estimate that mine supply peaked in 2015 and will trend lower in the foreseeable future.

• Declining total supply is expected to be a key driver of annual deficits in the silver market going forward.

Conclusion – Own silver coins and bars as insurance

We write ‘unlikely to improve’ but actually this depends on which side of the silver pile you’re on. In reality a declining silver supply is excellent for those who have chosen to invest in silver, it is also good news for those who are holding assets in silver mines as the product will be come increasingly sought after. A weak economy means more demand for safe havens, such as gold and silver bars and coins.

The factors that point towards declining silver supply – reduced economic activity, declining energy markets and weakening base metal markets – are all the same reasons to own it. Whilst GFMS might separate the safe haven demand from the demand for silver because of reduced mining levels, in truth they are one and the same thing. Investors are rushing to own silver because they know that it is a useful and very rare commodity and a valuable hedge and form of financial insurance.

When it comes to the base metals they suffer when they can no longer be ‘used’ by the booming economy. They have no role when the producing economy no longer needs them. Silver demand contrasts this. When the economy is no longer able to buy, sell, produce and grow things then we know that governments are in trouble. Silver still has a role – as a hedge and insurance.

Silver is a necessary safe haven during times of financial turmoil. During these times (as we see now) governments greatly increase the production of fiat paper and electronic money.

With silver, this cannot happen and this is why we should own safe haven silver coins and bars. A fall in silver production is beneficial sign and a positive fundamental both in terms of its price but also as an indication of its value vis a vis other assets.

Full article on SRSrocco Report

Gold Prices (LBMA AM)

19 Apr: USD 1,282.05, GBP 9,999.74 & EUR 1,196.79 per ounce

18 Apr: USD 1,285.00, GBP 1,025.82 & EUR 1,205.46 per ounce

13 Apr: USD 1,286.10, GBP 1,025.28 & EUR 1,208.42 per ounce

12 Apr: USD 1,272.30, GBP 1,018.22 & EUR 1,199.02 per ounce

11 Apr: USD 1,255.70, GBP 1,011.47 & EUR 1,183.75 per ounce

10 Apr: USD 1,253.60, GBP 1,011.15 & EUR 1,184.40 per ounce

07 Apr: USD 1,264.30, GBP 1,017.38 & EUR 1,188.82 per ounce

Silver Prices (LBMA)

19 Apr: USD 18.22, GBP 14.19 & EUR 16.99 per ounce

18 Apr: USD 18.42, GBP 14.56 & EUR 17.27 per ounce

13 Apr: USD 18.56, GBP 14.80 & EUR 17.45 per ounce

12 Apr: USD 18.31, GBP 14.65 & EUR 17.27 per ounce

11 Apr: USD 17.94, GBP 14.44 & EUR 16.91 per ounce

10 Apr: USD 17.94, GBP 14.47 & EUR 16.97 per ounce

07 Apr: USD 18.40, GBP 14.81 & EUR 17.31 per ounce

Mark O'Byrne

This update can be found on the GoldCore blog here.

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.