A Battle Of Titans: The Coronavirus Versus The Fed

Stock-Markets / Financial Markets 2020 Mar 09, 2020 - 03:10 PM GMTBy: Dan_Amerman

There is a potential global tragedy that is unfolding in terms of the coronavirus epidemic, that may be on the verge of becoming a global pandemic. We simply don't know - nobody knows - at this stage what the eventual impact and number of mortalities will be in the United States and in the rest of the world.

What we do know is that the global supply chain is getting hit very hard. There are many economists who believe that we are potentially on the verge of what could be called a coronavirus recession where a shutdown of the supply out of China, ripples through shutdowns in Japan and South Korea (among many other nations), which combine to hit the US and European economies with a supply side shock.

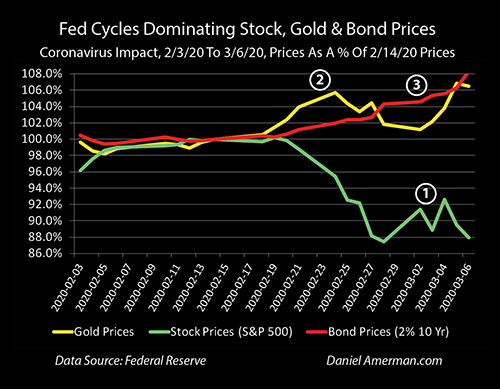

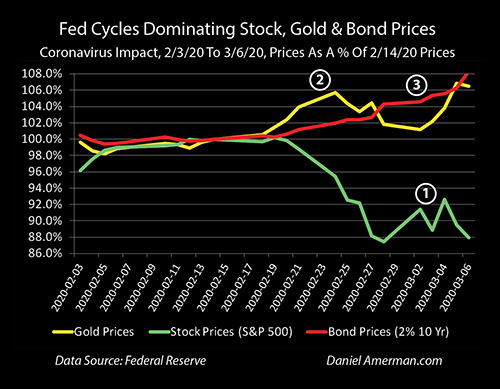

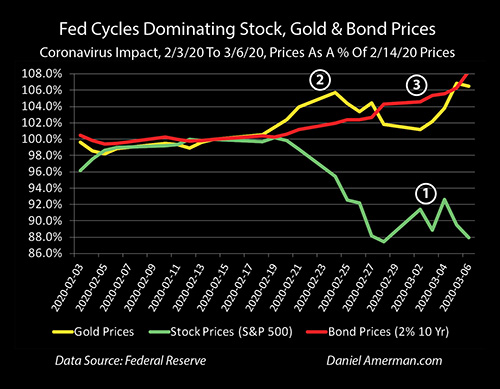

However, this rapidly worsening situation is not yet being fully reflected in stock prices, as can be seen in the graph above. If we look at the initial two weeks - then stock prices plunged, as one could argue they should have, given the rapid change in the fundamentals of the global economy.

However since that time, as can be seen with the green line and the (1) label, stock prices are highly volatile, but are not in the freefall that one might expect, given the dire economic situation.

The S&P 500 closed on Friday, February 28th, at a level of 2,954. There were seven straight days of extremely bad news when it came to the spread of the coronavirus outside of China, as well as early developments for corporations cancelling travel, falling airline traffic (with hotels doing the same, they just haven't reported yet), and an increasing number of industries facing supply side shortages. Yet, after a wild week that should have produced another round of huge price losses, the S&P 500 closed slightly up on Friday, March 6th, at a level of 2,972.

The difference is aggressive and preemptive interventions by the Federal Reserve, with its emergency half point decrease in Fed Funds Rates. Prices came back up when intervention was believed to be imminent, and the intervention was also critical in the bounce after the Super Tuesday primaries (although the impact on health care stocks of Biden outperforming Sanders was also of importance).

This analysis is part of a series of related analyses, which support a book that is in the process of being written. Some key chapters from the book and an overview of the series are linked here.

What Should Be Happening

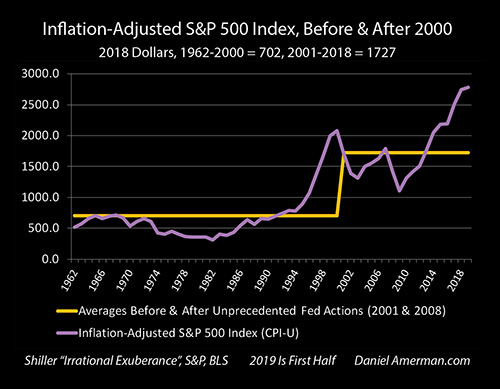

As a starting point, the stock indexes including the S&P 500 were at extraordinary levels compared to the past when the coronavirus started to hit.

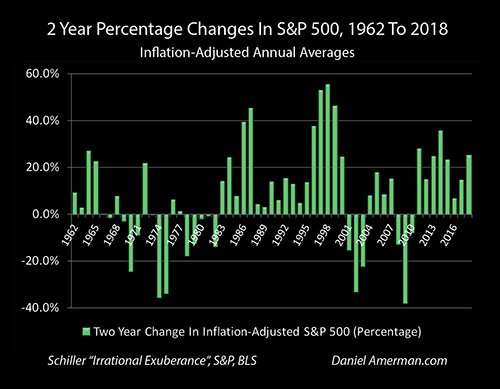

The above graph shows two year changes in the S&P 500 in inflation-adjusted percentage terms. We have been through troubles before, and a historical example of something generically like this (understanding the specifics are very different) was the oil embargo of the 1970s, where the shortage of oil created stagflation, with an exogenous supply shock creating major job losses even while prices exploded upwards. This led to major stock market losses in inflation-adjusted terms for the decade that would follow.

Using the methodology of two year inflation-adjusted percentage price changes, the sharp stock losses associated with the collapse of the tech stock bubble and the financial crisis of 2008 also become boldly visible - as does the lack of losses in the numerous other years without crisis.

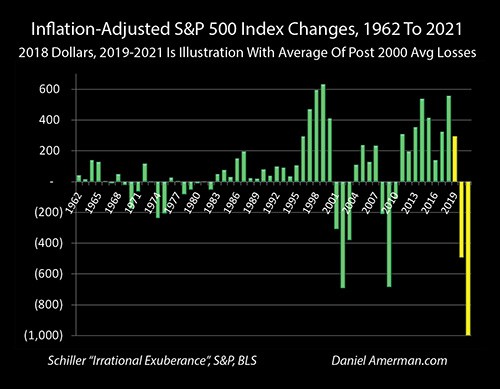

Now, if we simply say "What happens if we get another bad round?", and we multiply the S&P 500 by historic averages, then as developed in much more detail in Chapter 15, then we should expect losses in the S&P 500 of around 1000 points (in inflation-adjusted terms) over the next two years, by the time all is said and done.

If we look at the Dow Jones Industrial Average, then there is good case to be made that it should fall by in round number terms, something like 9,000 to 10,000 points over the next couple of years as a result of what appears to be happening with the coronavirus - even if it turns out to be the equivalent of a particularly severe flu in the United States. The current market threat is what is happening with the global supply chain, and that is not theory, but what is happening in real time.

Those potential losses are not some dire, extremist projection. They are what history shows us. Stocks go through long down cycles, secular bear markets, at times - particularly when we look at indexes in inflation adjusted terms. There can be long periods of calm, steadily climbing markets, and then something happens, and there are losses that are so great and so sustained that they might have been written off as unimaginable by many stock investors just the month or year before it started.

What is shown in the percentages graph above is three prior examples: the oil embargo (which then flipped into years of stagflation and a sequence of losses), the collapse of the tech stock bubble, and the financial crisis of 2008. So, all we have to do is say that a coronavirus epidemic / pandemic tearing up the global supply chain for at least a few months, perhaps longer, falls into the same general category as an oil embargo, or the collapse of a tech stock bubble, or the collapse of the subprime mortgage market, and there you go, losing a thousand in the S&P 500 or ten thousand in the Dow would be in the normal and entirely reasonable range of expectations, along with perhaps ten or more years of down markets.

What Is Happening Instead

That is not what is happening right now, and what will eventually happen is still very much in play.

The reason for that is what I've written about extensively in previous chapters of this book. We don't truly have free markets right now, nor have we for some years. Instead, what we have is markets that have been dominated by heavy handed Federal Reserve interventions, and cycles of crisis and the containment of crisis.

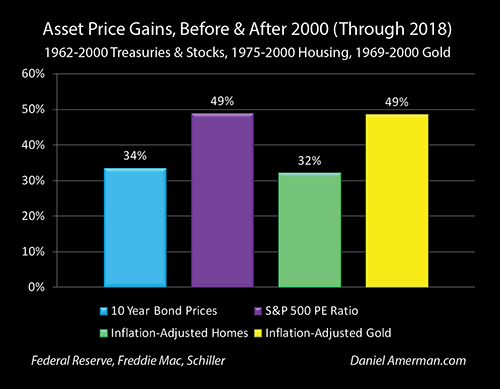

In general terms, as shown above, this has led to much higher than normal valuations for bonds because of very low interest rates, and stock prices that are very high relative to corporate earnings when compared to long term historic norms. We also have real estate values and home values that are well above historic norms.

As developed at length in the free book, starting with Chapter One (link here) these values have been created and supported by Federal Reserve using its powers to force very low interest rates on the nation.

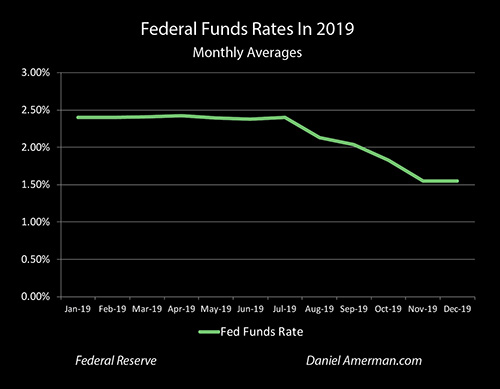

As shown in the graph above - even before the coronavirus emerged - in the preemptive attempts to prevent recession in 2019, the Federal Reserve had already forced rates down to about 1.50% (it was actually a range of 1.50% to 1.75%). Last week, meeting in an emergency videoconference, the Fed dropped rates by another 0.5%.

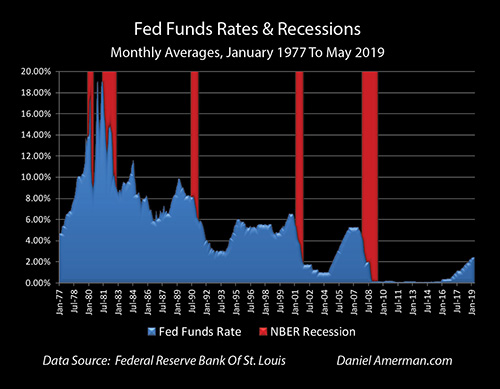

Over the past four recessions, the Fed has slammed rates down by average of 7.25% per recession to contain the damage, as covered in Chapter Four. The Fed starting very low to begin with, and then using up 0.75% of its recession fighting power in 2019, then another 0.50% on an emergency basis in early 2020, means that the Fed is down to a mere 1.0% to work with at this point, or only 14% of what it has previously used for ammunition, coming into what could become a particularly powerful recession.

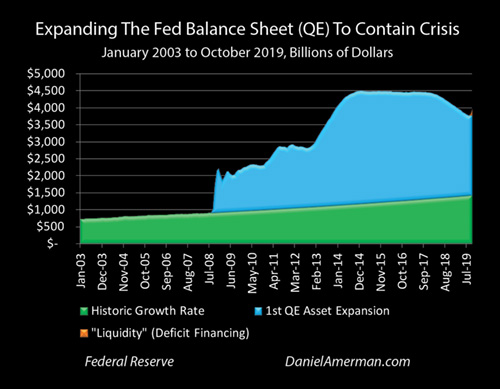

As explored in previous chapters including Eight, Thirteen, Fourteen and Eighteen, the Federal Reserve fully anticipated that it would lack the ammunition to fight the next recession with its historically proven tools. The full intention of the Federal Reserve was to fight another potential round of recession with an unprecedented degree of market interventions, that would be funded by an extraordinary degree of monetary creation.

That is not speculation - it is the publicly stated base plan. Institutional investors by and large understand this, most individual investors simply have no idea. This knowledge discrepancy is likely to lead to huge redistribution of wealth between Wall Street and the average investor as just one aspect of the current situation.

A Battle Of Two Titanic Forces - Neither Of Which Are Part Of Conventional Financial Planning

The emergence of the coronavirus is an exogenous factor - it is something extremely powerful and fundamental, that has come from entirely outside of the markets and which the Federal Reserve and the central banks have no control over whatsoever.

We don't know the future. But, at this stage, many people believe the coronavirus epidemic / pandemic has the potential to knock the entire global economy into recession while creating major supply issues - which could then create rapid inflation.

Starting from their current elevated heights, all else being equal, this should lead to potentially catastrophic results for stocks, REITs, retirement accounts and the net worths of tens of millions of Americans and others around the world.

The Federal Reserve cannot fight the coronavirus itself - but the Fed can attempt to fight the economic and market effects (with the key word being "attempt"). The tools that it fully intends to deploy are of a fantastic nature when compared to economic and financial history. In the process of deploying these tools, the Federal Reserve will be attempting to force what could be some of the largest investment price movements in history - and these will in no way be "natural", but will be the results of entirely unnatural interventions funded by monetary interventions.

As just one quick example, with the Federal Reserve having already almost entirely depleted its main recession fighting tool of forcing down short term interest rates last week, the chances also shot up that the United States will experience negative nominal interest rates - actual negative stated rates built into securities prices as with Japan and Europe. To force these negative rates is likely to require an extraordinary amount of monetary creation, with the Fed using the new money to become the main buyer of the negative rate bonds.

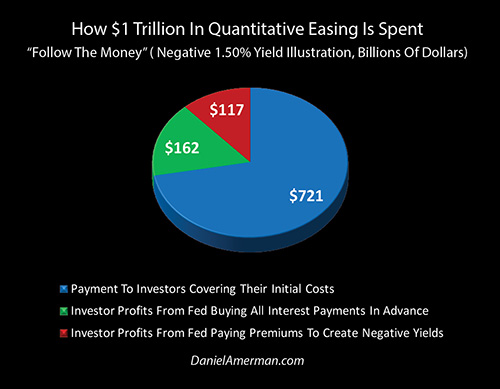

And, as explored in Chapter Fourteen (link here), the way this would be expressed is the Fed creating money by the trillions to fund one of the largest transfers of wealth to Wall Street and institutional investors in the history of the United States.

When we see how the money moves, we can also get a better understanding of one of the main reasons why long Treasury obligation prices have been moving up at such a rapid rate as the coronavirus news has worsened over the last three weeks.

Using A Framework To Anticipate Amplified Gains & Losses

If we accept that the stock market is moving up even slightly in the midst of a fundamentals-based crisis that is not being cured in any way, shape or form - then we have to accept that the very nature of the stock market and stock prices have changed.

For these radical reversals to occur on such a large scale means that the market is not being dominated by rational investors making long term judgments about the values of stocks in a process of price discovery.

Instead, stock market values are being powerfully influenced by how the markets react to the heavy-handed interventions of an outside agency - the Federal Reserve - which stands ready to use potentially trillions of dollars of raw monetary creation power to attempt to enforce its will.

So that means that if we are going to rationally value stocks and understand what is actually driving their changes in value we need to be fully taking into account not just the impact of the coronavirus, but what the Federal Reserve does in response.

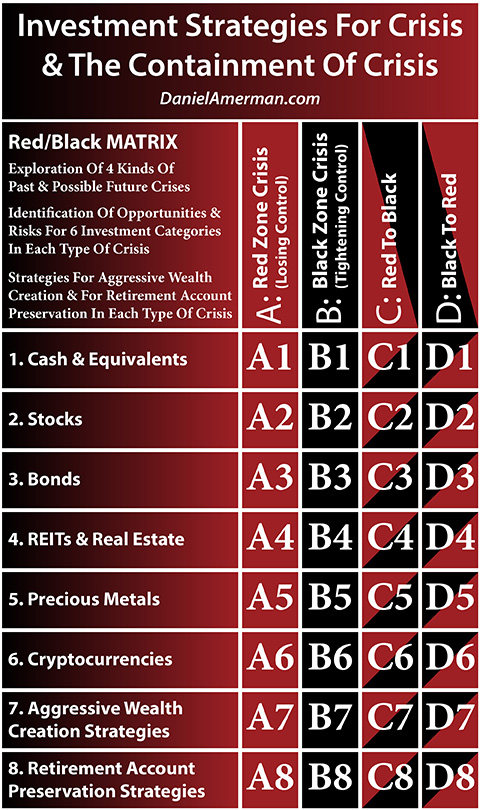

A framework for doing so is outlined in the Red/Black Matrix below. This framework is not a crystal ball - it in no way anticipated the coronavirus, or where the stress to the system would come from. However, what it does provide is a logical framework for evaluating the 1-2-3 combination of: 1) the coronavirus and 2) the Fed's extraordinary interventions to fight the economic and market effects of the coronvirus; that will 3) in combination likely determine investment price movements for the major investment categories, retirement accounts and home values over the coming months and years.

The "D" column has come into play in the last month - the cycle of the containment of crisis that has prevailed since 2008 is currently under a severe threat of the possibility of becoming a new cycle of crisis. "D" is not a certainty at this point, but the threat is very real and fast developing.

Stocks (matrix cell D2), bonds (matrix cell D3), and precious metals (matrix cell D5), are all performing pretty much exactly as would be anticipated for 1) a fast developing threat of a new cycle of crisis, with 2) the Federal Reserve acting as anticipated for an early stage response through the rapid lowering of short term interest rates, and 3) the two factors together logically determining investment prices.

The framework cannot give us an answer for the really big unknowable questions at this stage of how bad the coronavirus turns out to be, and whether the Fed and other central banks are able to prevent a market meltdown, either ultimately or even next week. However, by including both sides, the fundamental change and the response to the fundamental change, it does provide a much better guide for anticipating the possibilities for what could be happening and the investment impacts thereof.

Learn more about the free book.

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

© 2020 Copyright Dan Amerman - All Rights Reserved

Disclaimer: This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.