Volatile Week Ends With Signs of Improving Credit Markets

Stock-Markets / Financial Markets Oct 19, 2008 - 09:36 AM GMT

What a crazy week! A week in which the Dow Jones Industrial Average managed to record both its largest single-day points increase (+936 points on Monday) and its second-largest one-day points decline (-733 points on Wednesday) since its start in 1896. On Thursday the CBOE Volatility (VIX) Index surged to a record high of 81.17, with the Dow closing the week 4.7% higher after the previous week's record 18.2% decline.

What a crazy week! A week in which the Dow Jones Industrial Average managed to record both its largest single-day points increase (+936 points on Monday) and its second-largest one-day points decline (-733 points on Wednesday) since its start in 1896. On Thursday the CBOE Volatility (VIX) Index surged to a record high of 81.17, with the Dow closing the week 4.7% higher after the previous week's record 18.2% decline.

Source: Cartoonbank.com

Compiling this round-up, I invariable thought of John Crudele's ( New York Post ) comment: “… I'm as sick of writing about financial problems as you are of reading about them. But, as your mother probably said, just sit still and take the medicine. It's good for you.”

Governments around the globe launched unprecedented and concerted rescue operations for major banks in order to unfreeze short-term credit markets and avoid a collapse of the world's financial system. It has also been announced, according to The New York Times , that President Bush had agreed to play host to a summit of world leaders soon to discuss the global response to the financial crisis.

Reflecting on the origins and fall-out of the credit debacle, a quote from Winston Churchill comes to mind: “The inherent vice of capitalism is the unequal sharing of the blessings. The inherent blessing of socialism is the equal sharing of misery.”

Throughout the week, investors remained preoccupied with concerns about the intensifying economic damage that inevitably follows financial damage. Deleveraging of hedge funds continued unabated, and commodities and emerging-market stocks, bonds and currencies plunged on the back of risk aversion.

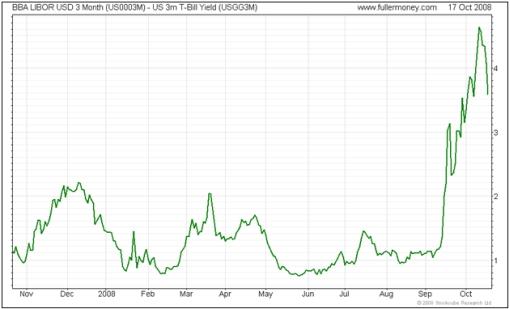

On a positive note, credit markets saw signs of improvement, with the overnight dollar Libor rate dropping to 1.66% from 5.09% last week, commercial paper rates falling to 1.05% from 3.50%, and the Ted spread – the difference between what banks charge each other for three-month loans (three-month dollar Libor) and what the Treasury pays (three-month Treasury Bills) – narrowing by 100 basis points to 3.63%.

“By the time the Ted spread is safely beneath 100 basis points once again, I expect the next bull market in equities to be well under way. The global economy should be recovering as well,” added David Fuller ( Fullermoney ) from across the pond.

Source: Stockcube Research

Next, a tag cloud of the text of the dozens of articles I have devoured during the past week. This is a way of visualizing word frequencies at a glance. Not too many surprises here, especially seeing “banks” featuring so prominently.

Warren Buffett, in an Op-Ed article in The New York Times , said that he was buying American stocks for his personal portfolio and encouraged others to do the same. “I can't predict the short-term movements of the stock market. I haven't the faintest idea as to whether stocks will be higher or lower a month – or a year – from now. What is likely, however, is that the market will move higher, perhaps substantially so, well before either sentiment or the economy turns up. So if you wait for the robins, spring will be over,” said Buffett.

Jeremy Grantham (GMO) summarized his investment recommendations in his latest quarterly newsletter as follows: “At under 1,000 on the S&P 500, US stocks are very reasonable buys for brave value managers willing to be early. The same applies to EAFE and emerging equities at October 10 prices, but even more so. History warns, though, that new lows are more likely than not.

“Fixed income has wide areas of very attractive, aberrant pricing. The dollar and the yen look okay for now, but the pound does not. Don't worry at all about inflation. We can all save up our worries there for a couple of years from now and then really worry!

“Commodities may have big rallies, but the fundamentals of the next 18 months should wear them down to new two-year lows. As for us in asset allocation, we have made our choice: hesitant and careful buying at these prices and lower. Good luck with your decisions.”

I am of the opinion that stock markets are in a broad phase of bottoming out. In a post a few days ago I asked the question “Is the financial storm over?”, concluding: “One could argue that stock prices are oversold, creating the potential for a further advance through year end, especially if credit spreads tighten (i.e. normalize) further. However, stock market valuations are not at the same oversold level as prices, arguing that a secular low may not necessarily have been reached. The third-quarter earnings season should provide part of the puzzle.”

Before highlighting some thought-provoking news items and quotes from market commentators, let's briefly review the financial markets' movements on the basis of economic statistics and a performance round-up.

Economy

“Global business confidence plunged last week to a record low. The financial panic has unnerved businesses, particularly in the US and Europe, but sentiment has also turned sharply lower in South America and even in Asia,” according to the Survey of Business Confidence of the World conducted by Moody's Economy.com . “The global economy is taking a body blow from the financial turmoil.”

Economic reports released in the US during the past week consisted of a battery of worrisome updates. Fed Chairman Ben Bernanke's depiction of the outlook for the economy in his address to the Economic Club of New York on Wednesday best described what was in store for the economy.

“Stabilization of the financial markets is a critical first step, but even if they stabilize as we hope they will, broader economic recovery will not happen right away. Economic activity had been decelerating even before the recent intensification of the crisis. The housing market continues to be a primary source of weakness in the real economy as well as in the financial markets, and we have seen marked slowdowns in consumer spending, business investment, and the labor market.

“Credit markets will take some time to unfreeze. And with the economies of our trading partners slowing, our export sales, which have been a source of strength, very probably will slow as well.

“These restraining influences on economic activity, however, will be offset somewhat by the favorable effects of lower prices for oil and other commodities on household purchasing power. Ultimately, the trajectory of economic activity beyond the next few quarters will depend greatly on the extent to which financial and credit markets return to more normal functioning.”

BCA Research commented on the economic situation as follows: “The combination of a deteriorating economic outlook and continued severe financial stress points to an early cut in the Fed funds rate to 1%. The recently released Beige Book provided further confirmation that economic activity is weakening across the country, and there is little doubt that a deep rather than mild recession is unfolding. A zero funds rate within the next few months is possible if financial conditions do not soon improve.”

To which Frank Holmes ( US Global Investors ) added: “The Treasury and its counterparts in the G-7 have started the monetary process by dropping interest rates and increasing the money supply, and that has started the healing process. Now we need the government to have a fiscal plan to create sustainable jobs rather than one-time ‘stimulus' checks that get spent on consumer goods. We advocate no new taxes and cuts for wasteful spending, and that the government dedicate itself to infrastructure projects that will create new jobs and repair the nation's roads, bridges and other critical facilities.”

Elsewhere in the world, economic data also showed an acceleration in the weakening of activity.

Week's economic reports

Click here for the week's economy in pictures, courtesy of Jake of EconomPic Data .

Date |

Time (ET) |

Statistic |

For |

Actual |

Briefing Forecast |

Market Expects |

Prior |

Oct 13 |

2:00 PM |

Treasury Budget |

Sep |

- |

NA |

NA |

NA |

Oct 15 |

8:30 AM |

Retail Sales |

Sep |

-1.2% |

-0.5% |

-0.7% |

-0.4% |

Oct 15 |

8:30 AM |

Retail Sales ex-auto |

Sep |

-0.6% |

0.0% |

-0.2% |

-0.9% |

Oct 15 |

8:30 AM |

Core PPI |

Sep |

- |

0.1% |

0.2% |

0.2% |

Oct 15 |

8:30 AM |

NY Empire State Index |

Oct |

- |

-8.5 |

-10.0 |

-7.4 |

Oct 15 |

8:30 AM |

PPI |

Sep |

-0.4% |

-0.4% |

-0.4% |

-0.9% |

Oct 15 |

8:30 AM |

Retail Sales |

Sep |

- |

-0.3% |

-0.7% |

-0.3% |

Oct 15 |

8:30 AM |

Retail Sales ex-auto |

Sep |

- |

0.1% |

-0.2% |

-0.7% |

Oct 15 |

8:30 AM |

Core PPI |

Sep |

0.4% |

0.1% |

0.2% |

0.2% |

Oct 15 |

8:30 AM |

NY Empire State Index |

Oct |

-24.6 |

-8.5 |

-10.0 |

-7.4 |

Oct 15 |

10:00 AM |

Business Inventories |

Aug |

- |

0.6% |

0.5% |

1.1% |

Oct 15 |

10:35 AM |

Crude Inventories |

10/11 |

- |

NA |

NA |

NA |

Oct 15 |

2:00 PM |

Fed's Beige Book |

- |

- |

- |

- |

- |

Oct 16 |

8:30 AM |

Core CPI |

Sep |

0.1% |

0.1% |

0.2% |

0.2% |

| Oct 16 | 8:30 AM | CPI | Sep | 0.0% | 0.0% | 0.1% | -0.1% |

| Oct 16 | 8:30 AM | Initial Claims | 10/11 | 461K | 475K | 470K | 477K |

| Oct 16 | 9:00 AM | Net Foreign Purchases | Aug | $14.0B | NA | $30.0B | $8.6B |

| Oct 16 | 9:15 AM | Capacity Utilization | Sep | 76.4% | 78.0% | 78.0% | 78.7% |

| Oct 16 | 9:15 AM | Industrial Production | Sep | -2.8% | -0.8% | -0.8% | -1.1% |

| Oct 16 | 10:00 AM | Philadelphia Fed | Oct | -37.5 | -5.0 | -5.0 | 3.8 |

| Oct 16 | 11:00 AM | Crude Inventories | 10/11 | 5611K | NA | NA | 8123K |

| Oct 17 | 8:30 AM | Building Permits | Sep | - | 845K | 840K | 854K |

| Oct 17 | 8:30 AM | Housing Starts | Sep | - | 880K | 870K | 895K |

| Oct 17 | 10:00 AM | Mich Sentiment-Prel. | Oct | - | 68.0 | 65.0 | 70.3 |

Source: Yahoo Finance , October 17, 2008.

In addition to Fed Chairman Ben Bernanke testifying at the House Budget Committee on Monday, October 20, next week's US economic highlights, courtesy of Northern Trust , include the following:

1. Leading Indicators (October 20): Interest rate spread, vendor deliveries, consumer expectations and money supply are the components likely to make a positive contribution in September. Stock prices, manufacturing workweek, initial jobless claims, and building permits are expected to make negative contributions. Forecasts of money supply and orders of consumer durables and non-defence capital goods are used in the initial estimate. The net impact is a 1.0% drop in the leading index during September after a 0.5% drop in August. Consensus : -0.2%.

2. Existing Home Sales (October 24): Sales of existing homes are most likely to have declined to an annual rate of 4.80 million units in September. Consensus : 4.92 million versus 4.91 million in August.

Click here for a summary of Wachovia's weekly economic and financial commentary.

A summary of the release dates of economic reports in the UK, Eurozone, Japan and China is provided here . It is important to keep an eye on growth trends in these economies for clues on, among others, the direction of the US dollar.

Markets

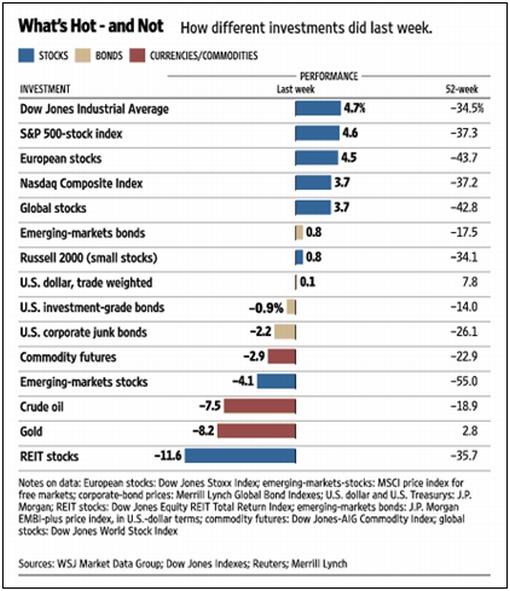

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , October 17, 2008.

Equities

Although very volatile, developed stock markets closed the week with fairly good gains – largely as a result of Monday's record surge – as shown by the MSCI World Index improving by 4.4% after the previous week's record decline of 20.1%. This was the first positive week since the second week of September. Leading the pack were Italy (+6.7%), Canada (+5.5%), Germany (+5.2%) and Japan (+5.0%)

On the other hand, risk-averse investors caused the MSCI Emerging Markets Index (-4.1%) to stumble further after losing 20.2% the week before. The week's largest decline was recorded by the Russian Trading System Index, giving up 21.0% to bring its total decline since the Index's high of May 18, 2008 to 68.2%.

The performance of the Dow Jones World Index (green line) and the MSCI Emerging Markets Index over the past two weeks are shown in the graph below.

The US stock markets all improved over the week as shown by the major index movements: Dow Jones Industrial Index +4.7% (YTD -33.3%), S&P 500 Index +4.6% (YTD -35.9%), Nasdaq Composite Index +3.7% (YTD -35.5%) and Russell 2000 Index +0.8% (YTD 31.3%).

The Dow needs to rise to 10,141 – 14.6% higher than its current level of 8,852 – in order to be officially classified as being in a bull market again. The Index will be required to increase by 22.1% to reach its 50-day moving average and 34.3% to get to the key 200-day line.

Market map, obtained from Finviz.com , providing a quick overview of the performance of the various segments of the S&P 500 Index over the week.

The investment bank & brokerage group (+28%) was the best-performing group during the past week. Goldman Sachs (GS) and Morgan Stanley (MS) were up on news that the government would provide funding to the two companies as part of a broader effort to restore confidence in the stressed financial system.

The automobile manufacturer group (+26%) was the second-best performer. According to media reports, General Motors (GM) is negotiating a possible merger with privately owned Chrysler.

Five of the ten worst-performing groups last week were related to the commercial real estate market. The worst-performing group was the real estate services group which plunged by 32%. Four real estate investment trust groups were also among the underperformers, showing investors' concerns about a weakening commercial real estate market brought on by the credit crunch.

The US stock market is in the middle of the Q3 earnings reporting season. According to Bespoke , 159 companies covered by analysts have so far reported their quarterly numbers, of which 60% have beaten estimates, 32% have missed and 8% have reported as expected.

Fixed-interest instruments

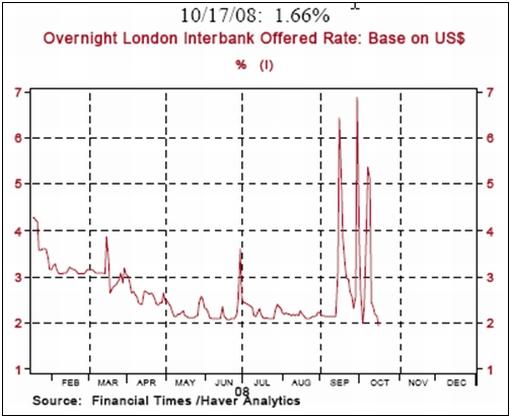

As mentioned in the introductory paragraphs, interbank and commercial lending rates started to ease during the past week. The overnight Libor rate dropped to 1.66% on Friday from a high of 6.87% on September 30.

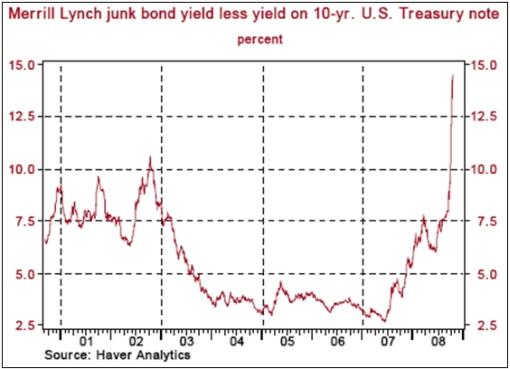

However, at the long and risky end of the credit market the situation was less encouraging, with the spread between the yield on junk bonds and the ten-year Treasury Note yield at 14.51% on October 16, which is higher than the spread of 14.23% on October 10.

Also, credit default swaps (CDS) for emerging markets – notably Hungary, Ukraine and Russia – widened considerably amid concerns about the health of their banking systems.

Movements in government bonds yields were as follows: the ten-year US Treasury Note increased by 7 basis points to 3.95%, the UK ten-year Gilt yield climbed by 20 basis points to 4.67% and the German ten-year Bund rose by 4 basis points to 4.04%. Emerging-market bonds suffered as investors shunned risky assets.

US mortgage rates increased, with the 30-year fixed rate rising by 36 basis points to 6.45% and the 5-year ARM by 5 basis points to 6.01%.

Currencies

The major currencies experienced a relatively quiet week as plans to implement unlimited US dollar currency swaps between the Federal Reserve and other major central banks brought some stability.

Although not a long-term bull on the greenback, Bill King ( The King Report ) highlighted that the “greatest short squeeze of all time” was occurring in the US dollar, and yen to a lesser degree. “Virtually all US private and public sector debt is a dollar short. The other big short is the yen via the ‘carry trade',” said King.

Over the week the US dollar gained against the Japanese yen (+1.0%) and Canadian dollar (+1.2%), but lost against the euro (-0.1%), the British pound (-1.4%) and the Swiss Franc (-0.1%).

The announcement of coordinated plans by Australia and New Zealand to safeguard their banking systems resulted in a rebound of their currencies, with the Australian dollar and New Zealand dollar gaining 7.3% and 3.9% respectively against their US namesake.

Emerging-market currencies, especially those with large current account deficits, lost heavily as global recession risks increased. Examples of losses against the greenback include the Hungarian forint (-5.7%), the South African rand (-7.1%), the Turkish lira (-6.4%) and the Korean won (-8.4%).

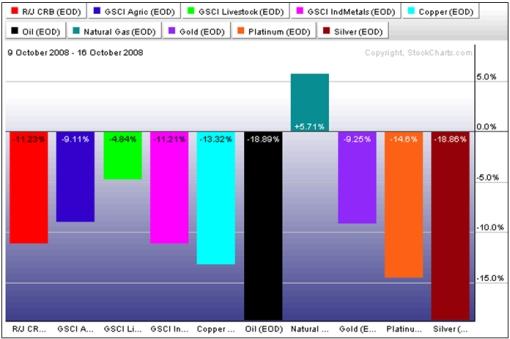

Commodities

Fears that the deteriorating global economic situation was causing demand destruction resulted in strong selling pressure for all commodities. The Reuters/Jeffries CRB Index dropped by 11.2% during the week, resulting in a loss of 39.7% since its high of July 2, 2008.

The chart below shows the relationship between the CRB Index and the Baltic Dry Index – an index covering dry bulk shipping rates and seen as a rough proxy for global growth.

West Texas Intermediate crude prices on Thursday fell below $70 a barrel for the first time since August 2007, but recovered to $72.13 on Friday to bring the decline since the record high of mid-July to more than 50%. This prompted OPEC, the oil-exporting countries' cartel, to schedule an emergency meeting for Friday, October 24 to discuss production cuts.

Notwithstanding steep declines in oil and gold prices, Merrill Lynch analysts, according to MarketWatch , said gold prices could hit $1,500 as global plans to rescue the financial industry are set to increase inflation pressures. The analysts didn't say when gold would hit the price target. They also predicted oil prices will rise to $150 a barrel.”

The following graph shows the past week's severe declines for various commodities:

Now for a few news items and some words and charts from the investment wise that will hopefully assist in guiding our investment portfolios through these troubled times. And remember the quote from Charles Dow : “Exercise enough patience for six men.”

That's the way it looks from Cape Town.

Source: Slate

PBS: Bill Moyers talks with comedian Jon Stewart

“Bill Moyers talks with comedian Jon Stewart, host of Comedy Central's The Daily Show, about how faking the news can reveal more of the truth than all of the Sunday-morning talk shows put together.”

Source: PBS, Bill Moyers Journal , October 17, 2008.

Warren Buffett (The New York Times): “Buy American. I am.”

“The financial world is a mess, both in the United States and abroad. Its problems, moreover, have been leaking into the general economy, and the leaks are now turning into a gusher. In the near term, unemployment will rise, business activity will falter and headlines will continue to be scary.

“So … I've been buying American stocks. This is my personal account I'm talking about, in which I previously owned nothing but United States government bonds. (This description leaves aside my Berkshire Hathaway holdings, which are all committed to philanthropy.) If prices keep looking attractive, my non-Berkshire net worth will soon be 100% in United States equities. “Why?

“A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when others are fearful. And most certainly, fear is now widespread, gripping even seasoned investors. To be sure, investors are right to be wary of highly leveraged entities or businesses in weak competitive positions. But fears regarding the long-term prosperity of the nation's many sound companies make no sense. These businesses will indeed suffer earnings hiccups, as they always have. But most major companies will be setting new profit records 5, 10 and 20 years from now.

“Let me be clear on one point: I can't predict the short-term movements of the stock market. I haven't the faintest idea as to whether stocks will be higher or lower a month – or a year – from now. What is likely, however, is that the market will move higher, perhaps substantially so, well before either sentiment or the economy turns up. So if you wait for the robins, spring will be over.

“A little history here: During the Depression, the Dow hit its low, 41, on July 8, 1932. Economic conditions, though, kept deteriorating until Franklin D. Roosevelt took office in March 1933. By that time, the market had already advanced 30%. Or think back to the early days of World War II, when things were going badly for the United States in Europe and the Pacific. The market hit bottom in April 1942, well before Allied fortunes turned. Again, in the early 1980s, the time to buy stocks was when inflation raged and the economy was in the tank. In short, bad news is an investor's best friend. It lets you buy a slice of America's future at a marked-down price.

“Over the long term, the stock market news will be good. In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497.

“You might think it would have been impossible for an investor to lose money during a century marked by such an extraordinary gain. But some investors did. The hapless ones bought stocks only when they felt comfort in doing so and then proceeded to sell when the headlines made them queasy.

“Today people who hold cash equivalents feel comfortable. They shouldn't. They have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value. Indeed, the policies that government will follow in its efforts to alleviate the current crisis will probably prove inflationary and therefore accelerate declines in the real value of cash accounts.

“Equities will almost certainly outperform cash over the next decade, probably by a substantial degree. Those investors who cling now to cash are betting they can efficiently time their move away from it later. In waiting for the comfort of good news, they are ignoring Wayne Gretzky's advice: ‘I skate to where the puck is going to be, not to where it has been.'

“I don't like to opine on the stock market, and again I emphasize that I have no idea what the market will do in the short term. Nevertheless, I'll follow the lead of a restaurant that opened in an empty bank building and then advertised: ‘Put your mouth where your money was.' Today my money and my mouth both say equities.”

Source: Warren Buffett, The New York Times , October 16, 2008.

Charlie Rose: A conversation with FT's Martin Wolf

Source: Charlie Rose , October 14, 2008.

BBC News: Financial crisis – world round-up

“A look at the regions of the world most affected by the financial crisis, and what governments are doing to try to alleviate the financial turmoil.”

Click here for the full article.

Source: BBC News , October 16, 2008.

CNBC: President Bush on the financial rescue plan

“President George W. Bush discusses the government's efforts to solve the financial crisis.”

Source: CNBC , October 14, 2008.

Bloomberg: Paulson says capital injection focused on banks, thrifts

“US Treasury Secretary Henry Paulson talks with Bloomberg about Treasury's plan to inject capital into regulated financial institutions, the $700 billion bank rescue plan and Paulson's priorities during the final months of his tenure at Treasury.”

Source: Bloomberg , October 16, 2008.

Bloomberg: Trichet says crisis curbs price risks, justified cut

“European Central Bank President Jean-Claude Trichet speaks about the financial crisis and the response by central banks. Trichet delivers the keynote address at the Economic Club of New York luncheon.”

Source: Bloomberg , October 14, 2008.

Bloomberg: Soros calls Europe plan to support banks “positive” step

“George Soros, chairman of Soros Fund Management, speaks at a news conference in Washington about European leaders' pledge to guarantee new bank financing, the causes of financial market turmoil and his book ‘The New Paradigm for Financial Markets: The Credit Crisis of 2008 and What It Means.'”

Source: Bloomberg , October 13, 2008.

Financial Times: UK launches £37 billion bank rescue

“The government has begun to nationalise the UK banking system by injecting £37 billion into three of the country's biggest banks.

“The historic step could end up with Gordon Brown's government owning a majority stake in Royal Bank of Scotland, one of the world's biggest banks, and more than 40% of the combined Lloyds TSB and HBOS, which is set to be the country's largest mortgage lender.

“RBS, Lloyds TSB and HBOS have agreed to scrap their dividend payments as part of the government plan which will result in the UK banks being some of the best capitalised in Europe.

“Under the terms of the bailout, Royal Bank of Scotland, Lloyds TSB and HBOS will be prevented from paying dividends on ordinary shares until they have repaid in full a total of £9 billion in preference shares they are issuing to the government. Barclays, which is hoping to avoid government support by raising around £6.6 billion from private investors, has scrapped its final dividend for 2008 in a move designed to save £2 billion.

“Gordon Brown defended his government's ‘unprecedented but essential' decision on Monday morning, saying the effective partial nationalisation was intended to be temporary only.

“The British prime minister stated that he expected other countries to follow suit. ‘I think we'll find in Europe over the next few days … the same things are going to happen,' he said as Eurozone countries began to announce their own rescue packages.”

Source: Peter Thal Larsen, Financial Times , October 13, 2008.

Financial Times: Tim Bond on UK bank rescue package

“Tim Bond, head of global asset allocation at Barclays Capital, says the UK rescue package resembles what Sweden did 1980s. Mr Bond says it was effective because it stemmed the financial crisis but it didn't stem the economic crisis.”

Source: Tim Bond, Financial Times , October 10, 2008.

Financial Times: Switzerland unveils bank rescue plan

“Switzerland has joined the list of countries taking unprecedented measures to strengthen their banks with the government taking an indirect SFR6 billion stake in UBS, and Credit Suisse raising SFR10 billion from private investors and the Qatar Investment Authority. FT's Peter Thai Larsen talks to Daniel Garrahan about what has happened and how this bailout differs from others.”

Click here for the full article.

Source: Financial Times , October 16, 2008.

Financial Times: Australia and NZ launch bank safeguard plan

“Australia and New Zealand launched co-ordinated plans to safeguard their banking systems on Sunday, hoping to stem heavy losses suffered by their currencies and markets last week.

“The two governments, which were previously unique among developed states in not providing any explicit deposit guarantee, pledged on Sunday to guarantee all bank deposits. Canberra went further, guaranteeing all term wholesale funding by Australian banks in international markets and doubling its pledge to purchase residential mortgage-backed securities to A$8 billion.

“‘Australian banks, despite the fact that their balance sheets are in excellent shape, now have to compete with these foreign banks for funding on global financial markets, foreign banks which despite their weaker balance sheets, now have the advantage of a government guarantee,' said Kevin Rudd, Australia's prime minister. ‘As prime minister of Australia, I will not stand idly by while Australian banks are disadvantaged … because of the actions of foreign governments.'

“New Zealand, which is in recession, has offered to guarantee retail deposits for the next two years, with deposit-taking finance companies also included.”

Source: Peter Smith, Financial Times , October 12, 2008.

Asha Bangalore (Northern Trust): Treasury, Fed, and FDIC implement new measures of support

“Treasury, Fed, and FDIC instituted new measures to support the crumbling financial system. The US Treasury announced today, October 14, a voluntary program where financial institutions can sell preferred equity to the US government to enhance their capital starved status. Nine major financial institutions have agreed to be part of the program. This capital infusion plan follows the strategy adopted in many of the major European nations.

“Participating institutions will supposedly prevent unnecessary foreclosures and preserve homeownership. The details of which are not available as yet. The recapitalization program will amount to $125 billion for these nine banks and an additional $125 billion will be available to other banks or bank holding companies. Under this program, banks can continue to pay dividends capped at 5% for five years and 9% after this period.

“The FDIC will provide a 100% guarantee for newly issued senior unsecured debt for three years ending June 30, 2012. The guarantee would apply to debt of all maturities issued before June 30, 2009. The guarantee includes ‘promissory notes, commercial paper, inter-bank lending, and any unsecured portion of secured debt.' The FDIC also guarantees funds, without a limit on size, in non-interest bearing accounts until December 31, 2009. For interest bearing accounts, the guarantee is limited to $250,000.

“The Fed, beginning October 27, 2008, will provide funds to businesses under the Commercial Paper Funding Facility (CPFF). The Federal Reserve Bank of New York will finance the purchase of unsecured and asset-backed commercial paper from eligible issuers through its primary dealers. The CPFF will finance only highly rated, US dollar-denominated, three-month commercial paper.

“These are the facts of the measures put in place, all details are not available. The entire operation is underway to build confidence, get the credit machine working again and preserve the global financial infrastructure. Here are some related questions and answers (there are many more questions, some with answers, some without):

“(1) Have these actions and those of the counterparts of the Fed and Treasury across the world prevented a recession? No, a global economic recession is nearly certain. The US economy is already in a recession; we are waiting for the National Bureau of Economic Research to make an official announcement. That said, intervention of recent days was necessary to preserve the working of the market. Excesses caused the current crisis and extraordinary measures had to be taken to prevent a systemic collapse. Capital shortage has far reaching implications on the world economy. A financial institution short of capital will suspend lending which appears as smaller credit lines or refusal of credit lines to companies and consumers. In simple terms, every dollar of capital shortage results in a loss of multiple dollars of lending.

“(2) Will the recapitalization of banks solve the problem? Capital was essential but it is not the cure all. First, a thorough and honest audit of financial institutions is essential. The aim of the audit should be to recognize losses, write-down illiquid assets and clean-up balance sheets. Perceptions of counterparty risk will be minimized only if transparency of balance sheets is established.

“(3) Does the infusion of capital by purchase of preferred shares dilute earnings? Stakeholders of all hues are paid from the same profit pool. Therefore, there is little doubt that there is a dilution of earnings.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary , October 14, 2008.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.