Bullish Global Stock Markets Climb a Wall of Worry

Stock-Markets / Global Stock Markets Dec 14, 2008 - 07:26 AM GMT

Despite a litany of bleak economic and corporate news confronting investors during the past week, global stock markets digested the bearish fodder with a sense of aplomb. The MSCI World Index and the MSCI Emerging Markets Index gained 4.4% and 10.9% respectively on the week, with other reflation trades such as gold (+9.1%) and oil (+20.4%) also putting in a strong performance.

Despite a litany of bleak economic and corporate news confronting investors during the past week, global stock markets digested the bearish fodder with a sense of aplomb. The MSCI World Index and the MSCI Emerging Markets Index gained 4.4% and 10.9% respectively on the week, with other reflation trades such as gold (+9.1%) and oil (+20.4%) also putting in a strong performance.

But investor angst was never completely allayed as seen from the yields on US one- and three-month Treasury Bills briefly trading in negative territory for the first time since 1940, indicating the willingness of risk-averse investors to pay the government for the “privilege” of holding their money. Three-month T-Bills ended the week in positive territory but barely so at a minuscule 0.036% yield, indicating that liquidity was still being hoarded. (Also see my “ Credit Crisis Watch “.)

Source: Nick Anderson, Slate

The week kicked off on a positive note after US president-elect Barack Obama had spelled out his plans on Sunday for the biggest infrastructure investment in the US since the 1950s. According to CNN , Obama said: “We understand that we've got to provide a blood infusion to the patient right now to make sure that the patient is stabilized. And that means that we can't worry short term about the deficit [which might surpass $1 trillion before his spending plans are included]. We've got to make sure that the economic stimulus plan is large enough to get the economy moving.”

“The resultant infrastructure and physical assets will be far better than endowing busted banks, insurance companies and other financial entities with US taxpayers' cash, which effectively goes down a black hole,” remarked Bill King ( The King Report ).

Financial markets reacted negatively to the US Senate's failure to agree on a $14 billion loan to the troubled automakers. The prospect of the biggest industrial failure in US history caused a sell-off on global stock markets, a widening of credit spreads and an onslaught on the US dollar.

However, the US Treasury was quick to signal its readiness to provide funds to prop up the “Big Three”, as quoted in the Financial Times : “Because Congress failed to act, we will stand ready to prevent an imminent failure until Congress reconvenes and acts to address the long-term viability of the industry.” This indication resulted in an improved tone on financial markets by the close of the week.

Next, a tag cloud from the plethora of articles I have devoured over the past week. This is a way of visualizing word frequencies at a glance. Key words such as “credit”, “debt”, “economy”, “Fed”, “government”, “market”, “rates” and “stock” occur often, but “gold” is also becoming increasingly prominent.

Back to the issue of markets shrugging off bad news for the second week running. Richard Russell ( Dow Theory Letters ) commented as follows: “On top of everything else, Lowry's Selling Pressure Index dropped substantially yesterday [Wednesday] and is now in a definite declining trend. At the same time, Lowry's Buying Power Index is trending higher. Thus, the odds are saying that the trend of the stock market is turning up.

“This is all the more dramatic since this potential upturn has arrived in the face of black-bearish news. Markets bottoming and rising in the face of bearish news are often the most profitable ones. I have never seen a bear market hit its low amid happy news headlines.”

On a fundamental note, 39% of the constituents of the MSCI World Index sell at a discount to shareholders' equity. “The cash-rich companies allow investors to pay nothing for future earnings streams,” said Jean-Marie Eveillard in an interview with Bloomberg .

A positive for the bulls is that the period post Thanksgiving through the end of the year has usually been a bullish time for stocks, based on studies by Jeffrey Hirsch ( Stock Trader's Almanac ). Should the bullish seasonal tendencies provide a tailwind on this occasion, possible first targets are the 50-day moving averages of 8,784 for the Dow Jones Industrial Index (current level 8,630) and 910 for the S&P 500 Index (current level 880).

The last word on equities goes to Hong Kong-based Puru Saxena : “I cannot say with any certainty whether we are already in the early stages of the next cycle. Under my best case scenario, we are in the very early stages of a new multi-year bull market. And under my worst case scenario, we are going to get a very strong rebound (30% move higher in the S&P 500) over a short period of time, which will probably take the markets back to their 200-day moving averages.”

Before highlighting some thought-provoking news items and quotes from market commentators, let's briefly review the financial markets' movements on the basis of economic statistics and a performance round-up.

Economy

“Global business confidence has been shattered. Sentiment is equally negative in North America, South America and Europe. Asian business confidence is not quite as dark, but it is falling rapidly,” said the latest Survey of Business Confidence of the World conducted by Moody's Economy.com . “Pricing power is quickly evaporating and approaching that which prevailed in 2003, the last time deflation was a concern.” According to the survey results, the global economy is suffering a severe recession.

Economic indicators released in the US during the past week mostly pointed to a deepening recession.

BCA Research said: “The year-end spending season will be the biggest bust in several decades, as consumers have been hit by a double whammy: a meltdown in financial and residential asset prices; and a sharp rise in layoffs. The government's failure to deliver a fiscal stimulus plan and unfreeze the credit markets imply that the recession will deepen and any recovery will be pushed farther into the future.

“The contraction in payrolls and economic growth will persist until there are some signs that policy actions are finally becoming effective. The fiscal stimulus plan needed to stabilize the economy will be massive and policy rates will stay near zero for a long time.”

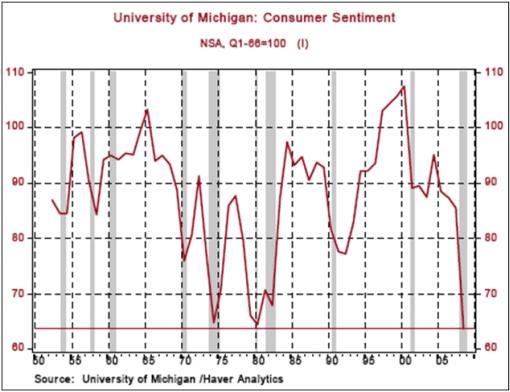

The precarious position of the US consumer is illustrated by a plunge of 21.9 points to 63.7 in the annual average of the University of Michigan Consumer Sentiment Index - the largest annual average decline in the history of the Index which began in 1952, according to Asha Bangalore ( Northern Trust ).

The Fed fund futures are pricing in a 76% chance of a 75 basis-point cut in rates from 1.0% to 0.25% when the FOMC meets on December 16.

However, Bill King questioned the Fed's approach: “[Effective] Fed funds traded at zero late last night. We have screamed for months that the official or ‘target' Fed funds rate was irrelevant because the effective funds rate was much lower, and near zero. Now Fed funds are trading at zero. Yet there will be pundits and experts that will assert that the Fed might cut its target funds rate this week to 0.50% or even 0.25% - even though the cut in the target rate is meaningless. Now that the Fed is paying interest to banks, why did the Fed allow the funds rate to trade at zero? Yep, they are terrified by something.”

Also, the Fed is considering issuing its own debt to further expand money supply without clogging up bank balance sheets and making it harder for the Fed to maintain interest rates at the desired level. RGE Monitor said: “… there are upper limits to Treasury issuance and lower limits to the amount of Treasuries the Fed can sell off from the asset side of its balance sheet. One hurdle to issuing Fed bills: The Federal Reserve Act doesn't explicitly permit the Fed to issue notes beyond currency.”

Elsewhere in the world, economic reports compounded anxiety about a severe global recession. Specifically, Chinese exports in November declined by 2.2% from a year earlier as a result of a drastic slowdown in demand in many of its main markets. The figures were far below forecasts and the +19% figure for October. “This is the worst collapse in Chinese exports since 1999 and is probably just the beginning of a prolonged export contraction,” said Isaac Meng, economist at BNP Paribas, as reported by the Financial Times .

Week's economic reports

Click here for the week's economy in pictures, courtesy of Jake of EconomPic Data .

Date |

Time (ET) |

Statistic |

For |

Actual |

Briefing Forecast |

Market Expects |

Prior |

Dec 9 |

10:00 AM |

Pending Home Sales |

Oct |

-0.7% |

- |

-3.0% |

-4.3% |

Dec 10 |

10:00 AM |

Wholesale Inventories |

Oct |

-1.1% |

-0.2% |

-0.2% |

-0.4% |

Dec 10 |

10:35 AM |

Crude Inventories |

12/06 |

392K |

NA |

NA |

-456K |

Dec 10 |

2:00 PM |

Treasury Budget |

Nov |

-$164.4B |

NA |

-$171.0B |

-$98.2B |

Dec 11 |

8:30 AM |

Export Prices ex-ag <!--[if !supportAnnotations]--> riculture |

Nov |

-2.9% |

NA |

NA |

-1.3% |

Dec 11 |

8:30 AM |

Import Prices ex-oil |

Nov |

-1.8% |

NA |

NA |

-0.9% |

Dec 11 |

8:30 AM |

Initial Claims |

12/06 |

573K |

520K |

525K |

515K |

Dec 11 |

8:30 AM |

Trade Balance |

Oct |

-$57.2B |

-$53.5B |

-$53.5B |

-$56.6B |

Dec 12 |

8:30 AM |

Core PPI |

Nov |

0.1% |

0.1% |

0.1% |

0.4% |

Dec 12 |

8:30 AM |

PPI |

Nov |

-2.2% |

-2.1% |

-2.0% |

-2.8% |

Dec 12 |

8:30 AM |

Retail Sales |

Nov |

-1.8% |

-2.1% |

-2.0% |

-2.9% |

Dec 12 |

8:30 AM |

Retail Sales ex-auto |

Nov |

-1.6% |

-1.9% |

-1.8% |

-2.4% |

Dec 12 |

10:00 AM |

Business Inventories |

Oct |

-0.6% |

0.0% |

-0.2% |

-0.4% |

Dec 12 |

10:00 AM |

Mich Sentiment-Preliminary |

Dec |

59.1 |

58.0 |

55.0 |

55.3 |

Source: Yahoo Finance , December 12, 2008.

In addition to interest rate announcements by the FOMC (Tuesday) and the Bank of Japan (Thursday), next week's US economic highlights, courtesy of Northern Trust , include the following:

1. Industrial Production (December 15): The 1.4% drop in the manufacturing man-hours index in November suggests a 1.0% decline in industrial production. The operating rate is projected to have dropped to 75.7. Consensus : -0.8%; Capacity Utilization: 75.7 versus 76.4 in October.

2. Consumer Price Index (December 16): A 0.7% decline in the CPI is forecast for November versus a 1.0% drop in October, reflecting largely lower energy prices. The core CPI is expected to have moved up by 0.1% after a 0.1% decline in October. Consensus : 1.3%, core CPI +0.1%.

3. Housing Starts (December 16): Permit extensions for new homes fell by 9.2% in October, inclusive of a 12.6% drop in permits issued for single-family homes. These figures suggest a sharp drop in housing starts (730,000). Consensus : 740,000 versus 791,000 in October.

4. Leading Indicators (December 18): Interest-rate spread and money supply are the only two components likely to make a positive contribution in November. Stock prices, initial jobless claims, manufacturing workweek, consumer expectations, vendor deliveries, and building permits are expected to make negative contributions. Forecasts of money supply and orders of consumer durables and non-defense capital goods are used in the initial estimate. The net impact is a 0.5% drop in the leading index during November, assuming building permits fell. Consensus : -0.5 %

5. Other reports : NAHB Survey (December 15), Current Account (Q4) (December 17), Philadelphia Fed Survey (December 18).

Click here for a summary of Wachovia's weekly economic and financial commentary.

Markets

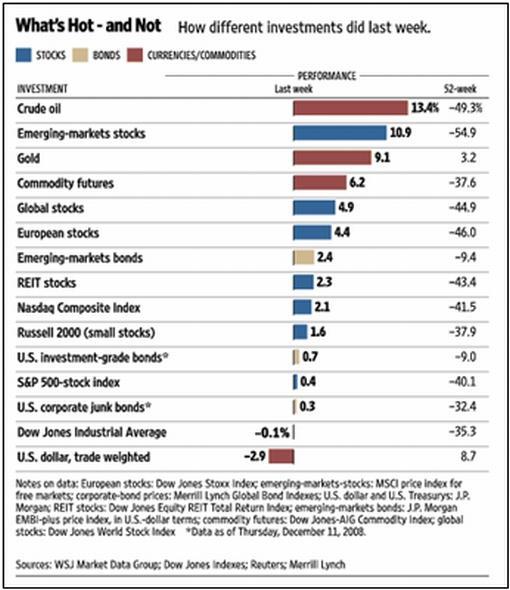

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , December 12, 2008.

Equities

Global stock markets rallied strongly during the past week as bargain-hunters looked past the grim economic and corporate reports. Both mature and emerging markets participated in the rally, as shown by the gains of the MSCI World Index (+4.4%) and the MSCI Emerging Markets Index (+10.9%). Notwithstanding the improvement, these indices were still down by 47.4% and 58.8% respectively since the peaks of October 2007.

Particularly noteworthy, the MSCI Emerging Markets Index has been outperforming the Dow Jones World Index since late October (rising green line), after a period of solid underperformance from May to October (falling line).

The chart below shows the performance of the four BRIC countries since the November 20 lows. Brazil (orange line), India (green) and Russia (red) have all recovered sharply, but China (blue) has underperformed after initial outperformance following the climactic [MR2] November 10 sell-off.

A ( pleasantly green) market map, obtained from Finviz , providing a quick overview of last week's performances of global stock markets (as reflected by the movements of ADR stocks).

The Dow Jones Industrial Index was one of the few major indices to record a negative return during the past week, with US markets in general lagging other bourses as shown by the major index movements: Dow -0.1% (YTD -34.95), S&P 500 Index +0.4% (YTD -40.1%), Nasdaq Composite Index +2.1% (YTD ‑41.9%) and Russell 2000 Index +1.6% (YTD -38.8%).

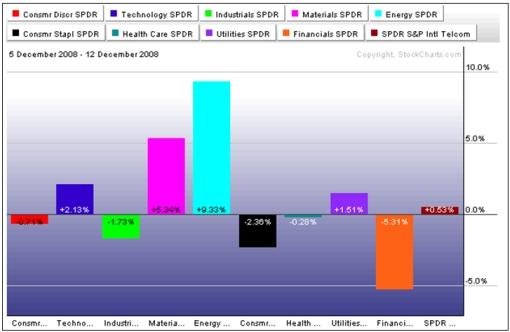

The bar chart below shows the US sector performances over the week, and specifically how strongly energy and materials have recovered. Nine of the ten best-performing groups were related to commodities (diversified metals & mining, coal & consumable fuel, aluminum, steel, gold, oil & gas drilling, oil & gas exploration & production, gas utilities [MR3] , and oil & gas equipment & services).

Jamie Dimon, JPMorgan Chase's (JPM) chief executive, prompted a sharp fall in financial shares with a warning that his bank was having a tough fourth quarter after a “terrible” November and December. Goldman Sachs' (GS) earnings report on Tuesday is keenly awaited.

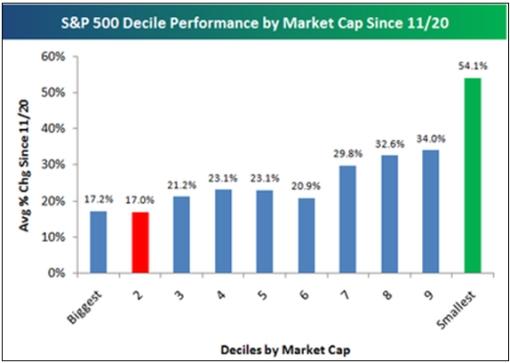

Based on the outperformance of emerging-market stocks and the sharp recovery of commodity-related groups, it would appear that investors are becoming less risk averse. Another example is the outperformance of small caps since the November 20 lows. A study published by Bespoke on December 8 highlighted the decile performance of stocks in the S&P 500 Index based on market cap. As shown by the chart below, the two deciles of the largest-cap stocks in the S&P 500 increased by about 17%, while the decile of the smallest-cap stocks was 54% higher.

Fixed-income instruments

The yields on government bonds generally edged up during the past few trading days after a record-breaking plunge since the beginning of November.

The UK ten-year Gilt yield increased by 17 basis points to 3.60% and the German ten-year Bund rose by 26 basis points to 3.30%. Although the US ten-year Treasury Note yield declined by 7 basis points to 2.59% on the week, the yield edged up from an earlier five-decade low of 2.48%.

John Hussman ( Hussman Funds ) expressed his concern about the level of Treasuries: “The problem with Treasury yields here is that while there are good economic reasons for the downward yield pressures, the levels are low enough to invite explosive spikes that can easily wipe out a year or more of yield-to-maturity in a few days.”

Emerging-market bonds moved in an opposite direction to mature bonds, with the JPMorgan EMBI Global Index gaining 2.4% during the week.

US mortgage rates were almost unchanged on the week, with the 30-year fixed rate rising by 2 basis points to 5.71% and the 5-year ARM declining by 1 basis point to 5.95%

The CDX and iTraxx credit indices, US Treasury Bills and high-yield spreads are still at distressed levels. Some improvement has been seen as a result of the central banks' actions, notably the tightening of the TED and LIBOR-OIS spreads, and lower mortgage rates. However, credit spreads need to narrow further to indicate that liquidity is moving freely again and credit markets are starting to thaw. (Also see my “ Credit Crisis Watch “.)

Currencies

The US dollar fell sharply as the recent relationship between risk aversion and dollar strength weakened as a result of US-specific factors like the deterioration in the US trade balance and the automaker woes. The greenback plummeted to a 13-year low against the Japanese yen and touched its lowest level against the euro for seven weeks.

As shown by the chart below, the dollar has broken below its 50-day moving average and seems to be topping out. Are foreign investors coming to the conclusion that the US currency, which briefly last week yielded a negative yield, is no longer an attractive option?

Over the week the US dollar lost ground against the euro (-5.0%), the British pound (-1.8%), the Swiss franc (-3.6%), the Japanese yen (-1.8%), the Canadian dollar (-2.0%), the Australian dollar (-3.0%) and the New Zealand dollar (-2.2%). The US currency also fell against emerging-market currencies [MR4] , like the South African rand (-2.0%).

The British pound came under renewed pressure as the worsening economic situation triggered concerns of a currency crisis. Sterling's trade-weighted index fell to its lowest level since record-keeping began in 1981.

Commodities

The Reuters/Jeffries CRB Index (+8.8%) closed higher by the end of the week - only its sixth positive week since commodities peaked early in July. The Baltic Dry Index - a benchmark for shipping major raw materials including coal, iron ore and grain - bounced by 15.2% from very oversold levels.

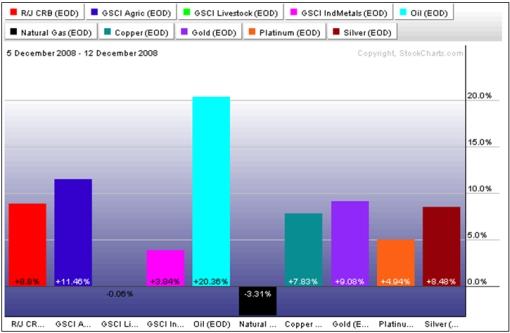

The graph below shows the movements of various commodities over the past week, indicating an improvement across the whole complex (with the exception of natural gas) as a weak US dollar pushed prices higher.

The International Energy Agency urged a “substantial” cut in Opec output when the oil cartel meets next week, as global oil demand this year is expected to contract for the first time in 25 years. The price of West Texas Intermediate crude surged by 20.4% in expectation of a cut of at least 1 million to 1.5 million barrels a day.

Gold bullion (+9.1%) remained in favor with investors as a result of a solid supply/demand situation, store-of-value considerations and a weaker US currency. The chart below illustrates the strong inverse relationship between gold (green line) and the dollar (red line). In addition, gold has broken above its 50-day moving average (blue line) and trades at about the same level it started off in January 2008 - quite a feat in these difficult markets. Platinum (+4.9%) and silver (+8.5%) improved in tandem with the yellow metal.

After the storm comes the calm. With only 12 more trading days remaining before we wish the tumultuous 2008 goodbye, let's hope the calm lies just ahead. And as Richard Russell reminds us: “Calm after a bearish trend is usually bullish.” Meanwhile, the news items and words from the investment wise below will hopefully assist in steering our portfolios on a profitable course.

YouTube: The twelve days of bailouts

A bailout song for the holidays.

Source: YouTube , December 6, 2008.

CNBC: Merrill Lynch - outlook for 2009

“An economic and investment outlook for 2009, with Merrill Lynch's Richard Bernstein and Davis Rosenberg.

Source: CNBC , December 11, 2008.

Financial Times: Obama to focus on stimulus not deficit

“Barack Obama on Sunday spelled out his plans for the biggest infrastructure investment in the US for half a century. The president-elect argued that with the economy reeling, his incoming administration could not afford to worry about a spiralling budget deficit.

“Mr Obama's proposals for government works on roads, bridges, internet broadband and school buildings, together with energy efficiency measures and health spending, are far more detailed than the normal announcements during a time of transition.

“At a time of deepening economic gloom - with half a million jobs lost last month alone - president George W. Bush has been largely absent from the recent economic debate. Mr Obama is highlighting his concern at the depth of the recession he will inherit, while fast-tracking his plans to counter it.

“‘Things are going to get worse before they get better,' Mr Obama said on Sunday on NBC's Meet The Press. He emphasised that his plans represented the largest US infrastructure programme since the federal highway system in the 1950s.

“‘The key is making sure we jump-start the economy in a way that doesn't just deal with the short term, doesn't just create jobs immediately, but also puts us on a glide path for long-term sustainable economic growth.'

“Noting the US budget deficit might surpass $1,000 billion before his spending plans are factored in, Mr Obama added: ‘We understand that we've got to provide a blood infusion to the patient right now to make sure that the patient is stabilised. And that means that we can't worry short term about the deficit. We've got to make sure that the economic stimulus plan is large enough to get the economy moving.'

“He wanted a strong set of financial regulations to make banks, credit ratings agencies, mortgage brokers and others ‘much more accountable and behave much more responsibly'.

“‘I am absolutely confident that if we take the right steps over the coming months that not only can we get the economy back on track but we can emerge leaner, meaner and ultimately more competitive and more prosperous,' Mr Obama said at a subsequent press conference.”

Source: Daniel Dombey, Financial Times , December 7, 2008.

Bill King (The King Report): Obama Plan one of the better plans

“The Obama Plan to spend massive amounts of money on infrastructure in the US is one of the better plans being proffered to keep the US out of a depression. But it has its drawbacks.

“Other stimulus plans put money or entitlements in US consumers' pockets. Most of the money ends up in China, Japan or OPEC. Most infrastructure spending will remain in the US. And instead of just passing out checks or larger entitlements, jobs, mostly temps, will be created and permanent assets will result.

“The resultant infrastructure and physical assets will be far better than endowing busted banks, insurance companies and other financial entities with US taxpayers' cash, which effectively goes down a black hole.

“Obama's Plan will boost blue collar employment, provided a limited number of illegals are hired. This will produce an income shift to blue collar and lower middle class households. But fired employees of financial, high tech and other high-end jobs are unlikely to participate. So the multiplier effect of increased income will be less on the economy in general.

“The negatives of the plan, besides the massive debt and likely corruption, is that it does not remedy structural problems in the US economy and financial system. There will be few new industries spawned and therefore few permanent well-paying jobs. Nothing addresses the savings and investment problems.

“There is too much capacity in the world. There are hundreds of empty or abandoned factories in China alone. Until excess capacity is scuttled and new industries appear, stable employment is a fantasy.

“The real problem, the one that solons will not address, is the US welfare state is busted. The Keynesian and monetary stimuli that were abused over many decades to paper over welfare state spending are now being escalated to an unsustainable degree in a last grand attempt to salvage the welfare state system.

“Like all state attempts to stave off a debt deflation by running the printing press and nationalization, it will likely result in a massive inflation that destroys the nation's fabric and the financial assets of the upper middle class and elites. The middle and lesser classes have few financial assets.”

Source: Bill King, The King Report , December 9, 2008.

Financial Times: Treasury signals rescue for carmakers

“The US administration was on Friday scrambling to save Detroit's troubled car industry, as General Motors said it was closing most of its North American manufacturing plants for the month of January in the wake of the Senate's failure to agree a $14 billion loan for GM and Chrysler.

“The US Treasury signaled it was ready to step in with funds intended to prop up the financial system to prevent the biggest industrial failure in US history.

“‘Because Congress failed to act, we will stand ready to prevent an imminent failure until Congress reconvenes and acts to address the long-term viability of the industry,' the Treasury said.

“GM's bonds fell to a new low of 9-10 cents on the dollar on fears of a bankruptcy by America's largest domestic carmaker, before recovering to 15 cents on the news that the Bush administration was looking for alternative financing.

“For weeks George W Bush, the US president, has resisted using the $700 billion troubled asset relief program to provide aid to the carmakers, arguing that such an interventionist step would be a misuse of funds.

“However, facing the prospect of the collapse of one or more of the Detroit companies, the White House indicated it had few other options. ‘A precipitous collapse of this industry would have a severe impact on our economy and it would be irresponsible to further weaken and destabilize our economy at this time,' said Dana Perino, White House spokeswoman, specifically noting the possibility of using Tarp funds.

“A Chapter 11 bankruptcy filing by GM, the world's biggest carmaker, would mark the biggest industrial failure in US history.”

Source: Daniel Dombey, John Reed and Bernard Simon, Financial Times , December 12, 2008.

Reuters: Fed mulls issuing own debt

“The US Federal Reserve is considering issuing its own debt for the first time, the Wall Street Journal said, citing people familiar with the matter.

“Fed officials have approached Congress about the move, which could include issuing bills or some other form of debt and would provide the central bank with more flexibility to tackle the financial crisis, the Journal said.

“The Fed can already print as much money as it wants, but issuing debt is largely the province of the Treasury Department.

“The Fed stepped in with emergency credit for investment bank Bear Stearns in March and insurer AIG in September, and threw open its direct loan window to Wall Street firms this year in a bid to stabilize financial markets amid a credit freeze.

“But with the credit crisis showing no signs of abating, and the narrow scope for further interest rate cuts from the present levels of 1%, economists expect the Fed to look at new ways to boost the supply and circulation of money to avoid a deflationary slump.”

Source: Reuters , December 10, 2008.

Paul Kasriel (Northern Trust): The credit rating on a benevolent counterfeiter's debt - infinity A?

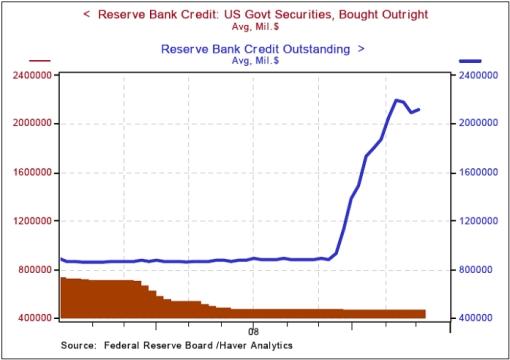

“Why would the Fed be contemplating issuing its own debt? To soak up in the future some of the massive credit the Fed has created in the past year or so. Why would the Fed not just sell US Treasury securities from its portfolio in order to soak up this excess Fed credit? Because, as shown in the chart below, the Fed's outright holdings of US Treasury securities has dropped from a shade under $800 billion to about $475 billion as Fed credit outstanding has risen from a little over $800 billion to about $2.1 trillion. In percentage terms, the Fed's outright holdings of US Treasury securities has gone from a bit over 90% of reserve bank credit outstanding to about 22-1/2%. The Fed is afraid it might run out of US Treasury securities to sell!

“I can see nothing sinister about all this. It is not a conspiracy to print money. Just the opposite. It is a way to destroy some of the paper the Fed already has ‘printed'.”

Source: Paul Kasriel, Northern Trust - Daily Global Commentary , December 10, 2008.

Bloomberg: Fed refuses to disclose recipients of $2 trillion

“The Federal Reserve refused a request by Bloomberg News to disclose the recipients of more than $2 trillion of emergency loans from US taxpayers and the assets the central bank is accepting as collateral.

“Bloomberg filed suit November 7 under the US Freedom of Information Act requesting details about the terms of 11 Fed lending programs, most created during the deepest financial crisis since the Great Depression.

“The Fed responded December 8, saying it's allowed to withhold internal memos as well as information about trade secrets and commercial information. The institution confirmed that a records search found 231 pages of documents pertaining to some of the requests.

“If they told us what they held, we would know the potential losses that the government may take and that's what they don't want us to know,” said Carlos Mendez, a senior managing director at New York-based ICP Capital, which oversees $22 billion in assets.

“The Fed stepped into a rescue role that was the original purpose of the Treasury's $700 billion Troubled Asset Relief Program. The central bank loans don't have the oversight safeguards that Congress imposed upon the TARP.

“Congress is demanding more transparency from the Fed and Treasury on bailout, most recently during December 10 hearings by the House Financial Services committee when Representative David Scott, a Georgia Democrat, said Americans had ‘been bamboozled'.

Source: Mark Pittman, Bloomberg , December 12, 2008.

The Wall Street Journal: Mayors get in line for US funds

“Big-city mayors will arrive on Capitol Hill Monday to lobby for more federal spending to be funneled to urban areas that they say drive the country's economic engine.

“The push comes after a strong Democratic turnout in metropolitan areas helped President-elect Barack Obama - who is set to become America's first urban president in almost half a century - win by such a decisive margin in November.

“A delegation of mayors, including Michael Bloomberg of New York and Antonio Villaraigosa of Los Angeles, plans to ask the federal government to distribute funds directly to cities instead of going through state governments. The group is set to present a list of more than 4,600 infrastructure projects that they say are ‘ready to go'.

“Tom Cochran, executive director of the US Conference of Mayors, which is organizing Monday's event, said the next administration has signaled that it will coordinate financing for projects for an entire metropolitan area instead of dealing with cities and suburbs separately.

“‘I am of the opinion, based on our conversations with President-elect Obama, that he gets it,' said Mr. Cochran. ‘You can't just have a transportation system that stops at the city line.'

“Mr. Obama's transition office is drawing up plans to create a White House office on urban policy, which would report directly to the president, to coordinate funding for cities from different federal agencies. Mr. Obama has pledged to provide new funding for job training, education and grants for local governments and organizations.”

Source: T.W. Farnam, The Wall Street Journal , December 8, 2008.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.