Great Economic Paradox of Stimulus and Bailout Packages

Economics / Credit Crisis Bailouts Jan 07, 2009 - 09:52 AM GMTBy: John_Mauldin

There is an ongoing debate on the current nature of the economic environment and what should the response be by government. Today's Outside the Box by Paul McCulley takes up one view, arguing that we need a federal response and stimulus package to protect the overall economy and save capitalism from itself. Tomorrow, I am going to send yet another view arguing that by doing so we are hurting the prudent investor and businesses that did not over-leverage and behaved responsibly. Both are important to understand. And as I will argue on Friday in my 2009 Forecast Issue, both are right. And that is one of the great economic paradoxes that we are faced with today. Navigating through this period is particularly challenging, but I think it is critical that you understand what Paul says today and what Bennet Sedacca will say tomorrow. Understanding what is going to happen, whether or not we agree with the philosophy behind it should be our goal, as it will make us better able to respond with our own portfolio and business decisions.

There is an ongoing debate on the current nature of the economic environment and what should the response be by government. Today's Outside the Box by Paul McCulley takes up one view, arguing that we need a federal response and stimulus package to protect the overall economy and save capitalism from itself. Tomorrow, I am going to send yet another view arguing that by doing so we are hurting the prudent investor and businesses that did not over-leverage and behaved responsibly. Both are important to understand. And as I will argue on Friday in my 2009 Forecast Issue, both are right. And that is one of the great economic paradoxes that we are faced with today. Navigating through this period is particularly challenging, but I think it is critical that you understand what Paul says today and what Bennet Sedacca will say tomorrow. Understanding what is going to happen, whether or not we agree with the philosophy behind it should be our goal, as it will make us better able to respond with our own portfolio and business decisions.

By the way, Paul McCulley, the Managing Director of Pimco, always features a "conversation" he has with his pet rabbit at the end of each year. Not only is it instructive, but it can also be downright funny. I think you will enjoy this letter a lot. And sorry about the Outside the Box coming later this week. We lost power for the day yesterday due to a mild ice storm here in Dallas.

John Mauldin, Editor

Outside the Box

All In - Global Central Bank Focus

Paul McCulley | December 2008/January 2009

(A conversation with Bun Bun, the author's Netherlands Dwarf pet bunny

and early-morning debating partner.)

PMc: Good morning, Bun Bun. Ready for our end of year chin wag?

BB: Again? And the question is not whether I'm ready, but whether you're ready. You're looking haggard, man, like a horse rode hard and put up wet. I never see you anymore, where you been?

PMc: First off, I ain't a horse. But I do catch your drift. As to where I've been, I've told you before: either at work or at my little rental cottage down on the water. I rented it for a weekend getaway, and found the water so soothing to my soul that I essentially live there now. So you got this big house all to yourself, Precious.

Except when my son, Jonnie is home from college, of course. He likes this space more than down on the water, not the least because I'm rarely here, I suspect. But that's only a suspicion. You know anything about that?

BB: Don't act dumb, Mac. He's 19 years old and has more girlfriends than the Fed has special liquidity facilities. Enough said, except that I think he ought to be taxed one fresh head of romaine lettuce for me every time he shows me off to a date. Remember, I just get to live here in your study, while he has roam of the whole house.

PMc: Okay, Okay. I'll work on that for you. Meanwhile, how do you know about all the Fed's liquidity facilities?

BB: Simple. Jonnie explained them to me, telling me the Bank of Ben is now doing for the capital markets what the Bank of Dad does for him: liberal liquidity provisions against all sorts of collateral, including the mere promise to behave in a more socially acceptable and responsible way in the future.

PMc: That's not exactly right, Bun Bun. Well maybe it is with respect to the Bank of Dad, but it is not the case with the Bank of Ben. As a general rule, also called the law of the land, the Federal Reserve is not in the business of lending on a wing and a prayer, but rather good collateral.

BB: You mean like you giving money to Jonnie but taking his iPod and putting it in the desk drawer until he pays you back?

PMc: Sorta like that, but in the case of the Fed, they wouldn't give Jonnie the purchase price of his iPod, but some lesser amount against the re-sale value of his iPod, minus a haircut.

BB: You mean that Ben would make him get a haircut, maybe even a shave, before taking in his iPod as collateral against a loan?

PMc: No, even though that's not a bad idea. In the collateralized lending business, in which the Federal Reserve traffics, a haircut is the margin of safety the lender demands for a loan against the re-sale value of the collateral. In your example, if an iPod cost $200 new and has a secondary market value of $100, the Fed would not even lend $100 against it, but rather some haircutted amount, say $75.

BB: So Ben would take Jon's iPod and put it the drawer, give him 75 bucks, and if he didn't pay off the loan, Ben would sell it for anything greater than 75 bucks, even if it's quoted at 100 bucks today?

PMc: Yep, that's more or less the mechanics of the matter, though to the best of my knowledge, the Federal Reserve has never taken in iPods at its various lending facilities. Very much unlike the Bank of Dad, who is not really in the banking business but the welfare business.

BB: But Jonnie told me that the Fed really can be like you, Mac, lending to anybody against anything with no-recourse, if the Board of Governors declares an emergency. He said something about a section 33. Was Jonnie wrong? You are paying way too much tuition for that fancy college he goes to if they are teaching him stuff that is wrong.

PMc: Jon's answer is not so much wrong as incomplete, similar to his efforts to clean up his room. And it's not section 33; it's section 13(3) of the Federal Reserve Act of 1934 which allows the Fed to lend to anybody, but not against anything.

The Fed can do so only if (1) a super majority of the Board of Governors - not the Federal Open Market Committee, known as the FOMC - declares the need for such lending to be the consequence of "unusual and exigent" circumstances, and (2) such lending is done against collateral that is "indorsed or otherwise secured to the satisfaction" of the Fed's lending officers.

BB: Technical details, I say, Mac. Jonnie was essentially right: if the Fed declares that the stuff is hitting the oscillator, the law allows for the Fed to unplug the oscillator, just so long as it dutifully declares that said oscillator is indeed an oscillator that needs to be unplugged. Jonnie said that's what the Fed has been doing ever since some stern dude named Bear needed a loan against a bunch of iPods with the batteries stripped out of them. Is that true?

PMc: I think perhaps I need to have a conversation with Jon's economics professor, who needs to remember that you are supposed to teach students textbook economics before teaching them real-world economics. But yes, back in March, the Fed invoked Section 13(3), for the first time since it was passed into law in 1934, to make a big loan that it otherwise wouldn't have been permitted legally to make.

But it wasn't to a stern dude named Bear, but rather to a special purpose vehicle, known as an SPV and named Maiden Lane LLC, which was set up to lend against dodgy mortgages previously held by the investment bank named Bear Stearns. The Fed made this loan to facilitate the merger of Bear into a bank named JP Morgan, so that Bear Stearns didn't go bankrupt, blowing the financial system sky high.

BB: All technical details, no? Your boss Mr. Gross is right, you are far too wonkish sometimes. Jonnie had the essence of the transaction down, no? In that case, the Fed's lending principles were similar to those of the Bank of Dad, no?

PMc: What's with all the no's, Bun Bun? You are starting to sound like a lawyer, leading the witness. Jonnie hasn't started dating girls in law school has he?

BB: Not that I know of; he's only a sophomore in college, for goodness sake. Just yanking your chain, Mac. But the way Jonnie explained it to me, the Fed really did do something very novel when it dealt with that Bear oscillator. It put some $30 billion of Bear's dodgy assets into that Maiden Lane thingamabob, telling JP Morgan that it had to stand up for the first $1 billion of losses and that the Fed would stand up for the remaining $29 billion, no recourse to JP Morgan. Is that right?

PMc: Yes, that's right, it was indeed an unusual Fed loan, and the Fed declared that it was, so as to legally be able to make it.

BB: But didn't you say that the Fed must be "secured"? How could making JP Morgan stand up only for the first $1 billion of losses against a $30 billion portfolio of iPods without batteries be deemed a secure loan?

PMc: Enough, Bun Bun, enough. I like your inquisitiveness, but sometimes some things are just best accepted as the way the world works, not how some textbook says it is supposed to work.

You're triggering a memory that goes back some twenty-five years ago, when Paul Volcker was chairman of the Federal Reserve. That was before CNBC, so guys who do what I do, called Fedwatchers back then, had to literally travel to Washington, DC to hear Mr. Volcker deliver the Fed's semi-annual report to Congress.

Some Congressman, whose name I've long since forgotten, was really getting after Mr. Volcker, demanding that he detail something that Mr. Volcker didn't want to detail. So Mr. Volcker took a long draw on his cigar and blew a big fog of smoke and said: "Congressman, we did what we did and we didn't do what we didn't do." And that was that, no more explanation needed.

BB: Hold on here. This Volcker dude was smoking a cigar while testifying before Congress? Was the session held outside?

PMc: No, Princess, it was held in a stately Congressional hearing room. And I was sitting right behind him. Back then, it was not against the law to smoke a cigar indoors, though most considered it impolite.

Even I did, and I rarely begrudge a man a good smoke, because Mr. Volcker's cigars were so cheap that they smelled like burning car seats when he puffed them. But he didn't care. At least not back then. A few years later, he gave up cigars.

But that wasn't my point. While Congress is the legal boss of the Federal Reserve, Congress is a boss with 535 heads, and sometimes the Fed boss simply has to do what he has to do, blowing smoke, literally or metaphysically, after the fact.

BB: So is this what the Fed did in making that funky loan against Bear Stearns' funky assets?

PMc: No, Bun Bun. Well maybe, as the Fed didn't and hasn't disclosed all the details of just how funky the funky stuff was. But the Fed, and especially Chairman Ben Bernanke, made clear to everybody that would - or wouldn't - listen that the Fed was not happy about making that loan, and didn't want to have to ever make such a loan again.

Not that the Maiden Lane loan didn't need to be made at the time, to save the capitalist financial system from its debt-deflationary pathologies. But the loan should have been made by the fiscal authority, not the monetary authority, with express blessing from Congress, who have express blessing from the electorate to do such things. For you see, Bun Bun, if there is the equivalent of the Bank of Dad in Washington, DC, it is supposed to be the Treasury, not the central bank.

BB: All very interesting, very interesting. Is this why the Fed refused to make a loan to that Lee Man chap when he was teetering on the edge of bankruptcy, feeling remorse for having made a loan against that Bear dude's stinky stuff?

PMc: It's Lehman, not Lee Man. And I don't know about any remorse for the Bear loan, Princess. All I know is that the Fed was not happy about it. Thus, when it came time to decide whether to lend against Lehman's stinky stuff, the question became just how stinky it was versus the Bear dude's stuff. Ben and the NY Fed Chief Tim Geithner decided it was just too stinky and took a pass. Or, as Mr. Volcker might have said, they didn't do what they didn't do.

BB: In which case, why didn't the Treasury step up and make the loan? After all, you said the fiscal authority can legally do what the monetary authority can't. Why didn't the Treasury unplug the oscillator, rather than let Lehman go down, effectively turning the oscillator on high?

PMc: Again, we'll never know precisely, Bun. But most fundamentally, the Treasury didn't have the express authority from Congress to do so. At least that is what Treasury Secretary Paulson says, while pounding the table with his shoe, Khrushchev style.

Could he have found some way, say using the Foreign Exchange Stabilization Fund? It's a fund of near $50 billion that the Treasury has Congressional approval to spend, if such spending is deemed necessary to keep the dollar from going wonky. Mr. Paulson later used it to establish a guarantee program for Money Market Mutual Funds. So conceptually, he could have used it to keep Lehman out of bankruptcy. I wasn't there, so I don't know. I certainly would have, but that assertion ain't worth a cup of coffee unless you have 4 bucks to go with it.

BB: So Lehman went down, and as was feared when the decision was made to prevent Bear from going down, the financial system blew sky high?

PMc: I might have been using a bit of hyperbole earlier when I said that, Bun Bun. But your Ockham's Razor conclusion is essentially correct.

BB: Never heard of such a razor, Mac. I think Jonnie uses something called a Gillette when he shaves that scruffy beard off every six weeks. What's an Ockham's Razor and what does it have to do with you becoming a much older man in the 100 days or so since Lehman was consumed by the oscillator?

PMc: Ockham's Razor is not a device for removing whiskers, but rather a mode of logic from the 14th century, defined loosely as cutting away all non-essential arguments when trying to answer a question or solve a problem. Which you just did, wonderfully, Bun Bun, when you asserted that what happened after Lehman went down was exactly what policy makers feared when they prevented bankruptcy for Bear: a systemic lock up of the global financial system.

BB: And out of that lacuna was born the TARP (Troubled Assets Relief Program), which explicitly gives the Treasury the authority and the money to unplug oscillators that need to be unplugged, when the Fed lacks the power to do so?

PMc: Yea verily, I say unto thee, Princess. You are a rather smart rabbit. Lacuna, that's a nice word. I don't recall saying it in front of you before. Where did you learn it?

BB: Looked it up on the web myself, and it precisely defines living in this place, while you live in the cottage. Take a hint, dude.

PMc: Taken. Now back to the matter at hand. The TARP, which Congress fought intensely about, and is still fighting about, given how the Treasury has used it to date, does indeed fill a gap in the federal safety net against systemic risk. It allows the Treasury to go where the Fed can't, literally lending to anybody against anything, or simply injecting equity into anybody against nothing, if necessary to maintain the capitalist financial system as a going concern.

BB: So is it 21st century socialism or welfare? Or is that a difference without a distinction?

PM: Bun, how am I to answer your machine gun questions if you keep answering them yourself? But yes, you've called it what it is. For my taste, I prefer the word socialism, but it does have a kernel of welfare in it, too. Whatever you call it, the TARP is a huge new tool for the visible fist of Treasury to support the invisible hand of capitalism.

BB: A fist, you say? How about calling it the taxpayers providing a hand out?

PMc: Ain't going there, Bun. Wouldn't be prudent, as the current President's father used to say. It is what it is, as everybody seems to say these days, in defense of what is unpalatable, but also necessary.

BB: So, if there was a positive externality of Lehman's demise, it is that policymakers finally found their socialist mojo, putting in place the necessary laws for the government to lever up and risk up its balance sheet more than proportionate to the private sector's new-found proclivity to do just the opposite?

PMc: Nice way to put it, Bun, with the operative phrase being "more than proportionate". That is indeed what is needed to save capitalism from its inherent debt-deflation pathologies. The paradox of deleveraging and the paradox of thrift are beasts of burden that capitalism simply can't bear alone. Only the Minsky Solution can lift that load.

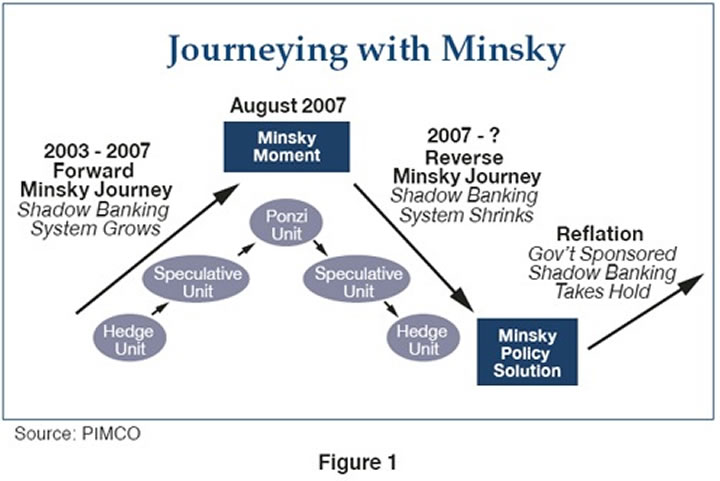

BB: Ah, Minsky. I knew you would get ‘round to him, it was only a question of how long you could restrain yourself. You and I recently talked a lot about Professor Minsky, complete with his Forward Journey, followed by his famous or infamous Moment, followed by his Reverse Journey. But I don't recall talking about his Solution. I know I'm going to regret this, but could you refresh my memory?

PMc: Thank you, Princess, for asking. I'm quite sure a number of those listening in on this conversation similarly share your reservation about letting me loose to pontificate on Minsky. So out of respect for both you and them, I'm going to act on the old cliché that a picture is worth a thousand words, maybe more. Here's a stylized graph, created by my colleague and friend Ramin Toloui, that captures all you need to know about Minsky right now.

BB: You are a kind man, Mac, spoiling me relentlessly. Looking at the graph, which I see starts in 2003, you have the Forward Minsky Journey unfolding, complete with the ever-risky steps from Hedge to Speculative to Ponzi Finance. The Shadow Banking System expands explosively. And then, you have the Minsky Moment in August 2007.

And then you have the Reverse Minsky Journey, as Ponzi Units evaporate, Speculative Units morph after the fact into Ponzi Units, and even Hedge Units take a beating, as the Shadow Banking System contracts implosively. And then the pain stops with this new thing called the Minsky Solution, followed by something called Reflation.

But I don't see a precise date on the graph for when this happens. Are we there yet? Is the pain going to stop? Like, now?

PMc: Nice framing and clearing of the graphic, Bun Bun. Have you been taking an on-line course from Communispond while I haven't been looking?

BB: Nope, I just look up cool words on the computer. You never take me out on the speaking circuit, so I don't need to learn how to dance the Communispond dance steps.

Stop dodging the question, Mac. I presume this Minsky Solution thing is that "more than proportionate" socialist response that we were talking about just a moment ago?

PMc: Precisely - if you weren't a bunny, Bun, I'd call you grasshopper! That is precisely the Minsky Solution: the government not only steps up to the risk-taking and spending that the private sector is shirking, but goes further, stepping up with even more vigor, providing a meaningful reflationary thrust to both private sector risk assets and aggregate demand for goods and services.

BB: Okay, I got it even though I hate the notion of being called a grasshopper. So answer my question, master: Are we there yet? And if so, doesn't that mean that it's now time for all good peoples, and bunnies, to sell their T-bills and canned green peas into cheap corporate bonds and stocks?

PMc: I didn't put a date on that box, Bun, precisely to avoid answering the question as to precise timing. All I can say is that the timing is ripening, with the Fed now committed to an all-in reflationary campaign. This includes not just expanding its lending facilities, but doing so in joint ventures with the Treasury, now armed with TARP money, which can serve as the equity in new SPVs that are essentially government-sponsored Shadow Banks.

The recently announced Term Asset-Backed Securities Loan Facility, known as the TALF, and scheduled to come on in February, is a perfect example of just such a joint venture, with the Treasury putting up $20 billion of equity and the Fed putting up $180 billion of loans senior to the Treasury.

The TALF will effectively step around the risk-adverse commercial banking system and provide warehouse financing directly for securitization of new consumer and business loans to Main Street. It's a really cool innovation, which is likely to be expanded or replicated. And most important, it is likely to get reflationary traction.

The Fed also stands ready to print $600 billion of money to buy directly $500 billion of Agency MBS (Mortgage-backed Securities) and $100 billion of Agency debentures, so as to pull down and hold down long-term mortgage rates. The buying of the debentures is already under way, and the buying of MBS is likely to start in a matter of weeks.

And if necessary, the Fed is openly willing to print money to buy longer dated Treasuries, providing a further downward gravitational force for long-term interest rates. As my friend Colin Negrych argues, and indeed forecast when the rest of the world thought he was nuts, there is nothing like a 2% handle on longer-term Treasuries yields - the credit risk-free benchmark - to make private sector assets more valuable.

BB: But where are Ben's helicopters tossing out money?

PMc: Bun, you know that I don't like references to Helicopter Ben. It's a cheap shot, absolutely a cheap shot, fired by people who haven't bothered to actually read his famous November 2002 speech, when he discussed an anti-deflation technique conceived by the great Milton Friedman - a money-financed tax cut.

That said, it is indeed a fact, a glorious fact, in my view, that the Fed does presently stand ready to print as much money as necessary to accommodate the financing of an all-in reflationary fiscal policy thrust, as promised by President-elect Obama. Through holes in the floor of heaven, Hyman Minsky weeps tears of joy.

Call it good, very good: the monetary and fiscal authorities, separately yet together, going all in. And call me cautiously optimistic that Reflation will get traction.

BB: I hate that phrase, Mac, absolutely hate it. And you're the one that taught me to hate it. What is cautiously optimistic? Either you are or you aren't, no?

PMc: Touché, Bun, touché. With respect to the willingness of policy makers to do the right reflationary thing, we can drop the adverb cautiously. I'm flat out optimistic. But prudence demands that I at least acknowledge that even the best laid reflationary plans might go awry, at least in the short run.

BB: Well if that might happen, how can you call them the "right reflationary thing"? All in means all in, no?

PMc: Yes it does, Bun Bun. But it doesn't mean that all sectors and all companies have to flourish in response. The "right reflationary thing" is a macro concept, not necessarily a micro concept. It doesn't mean extending the soothing socialist hand to every square inch of the capitalist landscape.

The right reflationary thing to do is to systemically save capitalism from its inherent debt-deflationary pathologies, not to eliminate capitalism. Recall, capitalism at its micro core is a process called creative destruction, churning resources from yesterday's technologies and work methods to the more productive ones of tomorrow.

BB: Ok, that makes some sense. In my world, that's called the survival of the fittest. Wouldn't make sense for government to try to overrule that force of nature, I agree. But it would make sense for the government to put out a forest fire that threatened to consume all us creatures, right?

PMc: Nice way to put it, Princess. Very nice! It's a delicate balance.

BB: Thank you. In your world of investing, it seems the analog would be to go long the forest, because the government is going to keep the flames of deflation from burning it down, while taking a selective approach to going long particular creatures. Is that about right?

PMc: Yea verily, I say unto thee again. But with just a slightly finer point on the matter: In order to save the capitalist economic forest, there are certain creatures that the government must necessarily also save. The right investment strategy is to go long both the forest and those creatures.

BB: Fair enough. Now name them!

PMc: We have been publicly naming them for months here at PIMCO, Bun Bun. Well maybe not always particular names, but rather the attributes of those names. The most important is explicit government support, which is most notably the case with the debt issued by banks that get to drink a triple-thick socialist shake: Equity injections from the Treasury, debt guarantees from the FDIC, and access to the munificent liquidity facilities of the Federal Reserve.

BB: But isn't it time to get a little more daring than that? What would be wrong with starting to average into some funds in the major stock and bond indexes, as a play on your thesis that the American capitalist economy is a going concern? Yes, I know that means you would be indirectly going long some individual names that will be on the fatal end of the creative destruction process, but isn't that always the case?

PMc: I can't argue with you, Princess. Your suggested strategy is consistent with the all-in reflationary policy responses. Yet caution is still warranted. I'd tilt it toward corporate bonds over corporate stocks, however, as seemingly little known in the popular press, high grade corporate bonds have, on a risk- and volatility-adjusted basis, been beaten up even more than blue chips stocks this year.

BB: I'm glad you are finally seeing it my way, Mac. Sometimes, you can be so thick, letting the pursuit of the perfect become the enemy of grasping the good. Do some of my trade for the Morgan Le Fay Dreams Foundation portfolio, okay?

PMc: As you wish, Bun. And thank you for honoring her memory and wanting her portfolio to do well. Because by doing well, she can continue to do good, lots of good. With that lovely thought, let's end this chin wag with Morgan's favorite prayer of the season. You have the honors.

BB: Thank you, Paul.

May God bless you and keep you,

May God's face shine upon you

and be gracious to you,

May God lift up his countenance

upon you,

And give you peace.

Paul A. McCulley

Managing Director

December 23, 2008

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.