Fed Planning Inflationary Dollar Destroying 15-Fold Increase In US Monetary Base

Economics / HyperInflation Mar 22, 2009 - 05:02 PM GMTBy: Eric_deCarbonnel

The fed is planning moves that would more than double its balance-sheet assets by September to $4.5 trillion from $1.9 trillion. Whether expressing approval or concern over the fed's intentions, most commentators fail to understand the real magnitude of the projected expansion of the US monetary base because they don't take into account the amount of dollars circulating abroad.

The fed is planning moves that would more than double its balance-sheet assets by September to $4.5 trillion from $1.9 trillion. Whether expressing approval or concern over the fed's intentions, most commentators fail to understand the real magnitude of the projected expansion of the US monetary base because they don't take into account the amount of dollars circulating abroad.

At least 70 percent of all US currency is held outside the country , and this means the US monetary base is considerably smaller than the fed's overall balance sheet. Take, for example, the true US domestic money supply at the beginning of September 2008, before the fed started its quantitative easing. From the Federal Reserve's website , we know that currency in circulation was 833 Billion. This translates as 583 Billion dollars circulating abroad (70 percent), and 250 Billion dollars circulating domestically (30 percent). Since the bank reserve balances held with Federal Reserve Banks were 12 billion, that gives us a 262 Billion domestic monetary base as of September 2008. Now compare that to the projected US domestic monetary base for September 2009 which is 3,818 billion (4,500 billion – 583 billion (dollars circulating abroad) – 99 billion (other fed liabilities not part of the money supply)). The fed's planned balance sheet expansion results in a 15-fold increase in the base money supply.

262 Billion = US monetary base as of September 2008 (minus dollars held abroad)

3,818 Billion = projected US monetary base in September 2009 (minus dollars held abroad)

3,818 Billion / 262 Billion = 15-Fold Increase in US monetary base

This is a staggering devaluation of the US currency! It means that for every dollar in America in September 2008, the fed is going to create fourteen more of them! Below is a rough sketch of what this Increase in US monetary base would look like:

This 15-Fold Increase will be impossible to reverse

Next September, when the fed realizes it has gone too far and tries to reverse its balance sheet expansion, it will be unable to do so. The realities which will hinder the fed's control of the money supply are:

1) The toxic assets filling its balance sheet

Expanding the money supply is easy. All the fed has to do is print dollars and then use them to buy assets. There is no effective limit to how much the fed can print and spend.

Shrinking the money is much trickier. To shrink the base money supply, the fed sell assets and takes the dollars it receives for them out of circulation. The amount the fed can shrink the money supply is therefore effectively limited by the market value of assets on its balance sheets. Since the fed is in the process of loading up on toxic securities while trying to restore health to the financial sector, it is now sitting billions of unrealized losses. These unrealized losses means the fed has little ammunition available to bring the money supply under control.

Once September rolls around, If the fed wants to reverse the expansion of its balance sheet and shrink the monetary base back down from 3,818 billion to 262 billion, then it will need to sell 3,556 billion worth of assets. However, the market value of its assets will only be worth a fraction of that.

2) Political constrains on fed's actions

Even if the fed does try to shrink the money, it is likely to run into political constrains on its actions:

A) Selling toxic assets at a loss could become a crippling source of major embarrassment for the fed, undermining its authority. For example, last year when the fed took 29 billion toxic assets to help JPMorgan's takeover of Bear Stearns, it assured Americans that by holding those securities till maturity, the cost to taxpayers would be minimal. If the fed sells those toxic Bearn Stearns assets at a catastrophic loss, it would cause fury and outrage from voters and lawmakers.

B) Selling assets at below book value will quickly cause the fed's equity to turn negative. The Federal Reserve would then need to be recapitalized by new debt from the treasury, which would increase the national debt.

3) The benefits from of its balance sheet expansion would be lost if the fed starts selling assets

The fed is accumulating toxic mortgage backed securities, long term treasuries, and other assets to unfreeze the credit markets and spur economic growth. Turning around and selling those assets would result in the collapse of the credit markets and the financial system, which the fed has been desperately trying to prevent.

Upwards pressure on interest rates

On top of all the issues above, the fed's woes are going to be compounded by upwards pressure on the yields of treasuries and other US debt. This upwards pressure will likely force the fed to monetize far more treasuries than the planned $300 billion purchases it has already announced, and will greatly complicate any efforts by the fed to control the money supply.

Below are the nine factors which will cause yields to move higher.

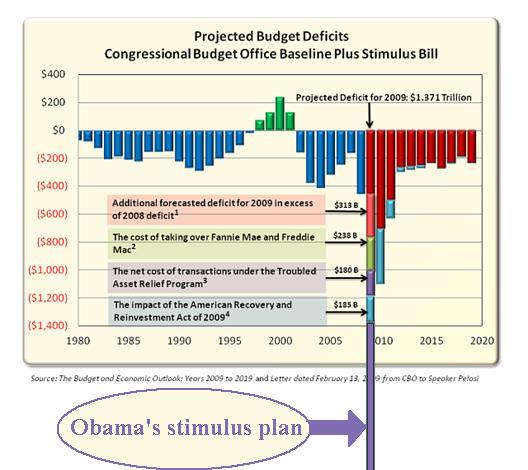

1) Massive supply of treasuries in the pipeline

The biggest force pressuring treasury yield upward is without a doubt the trillions of debt the treasury has to sell to finance the enormous 2009 budget deficit. There is nowhere near enough buyers to absorb this supply. The graph below demonstrates the challenge facing the treasury in funding this year's budget.

2) As a reserve asset, treasury bonds will face enormous selling pressure in 2009

There is the mistaken belief that the role of treasuries as a safe haven is bullish for treasury bonds. It is not. This logic ignores the reality that reserve assets, such as treasuries, are accumulate in good times and sold in bad times:

Federal and state agencies will be selling treasury reserves. For example, the Deposit Insurance Fund (a.k.a. FDIC) will be selling treasuries to pay back depositors of failed banks, and the Unemployment Trust Fund will be selling treasuries to make payments to the unemployed.

State and local governments will be selling treasury reserves. As an example, states have already begun drawing down reserves as their budget troubles worsen . The bulk of those reserve remain, and they will be sold over the course of this year.

Banks and insurers will be selling off their treasury loan-loss reserves. Financial institutions have been building their treasury loan-loss reserve for the last year in anticipation of growing defaults. In 2009, this process will reverse as loans go bad and insurers make good on claims.

Foreign central banks will be selling off their treasury foreign reserves. Saudi Arabia, for example, is projecting a 2009 Budget Deficit , which it intends to finance by selling off its US holdings. Russia, meanwhile, has already sold over 20% of its $598.1 billion reserves , and India's central bank has been forced to sell off its US holdings to curb its currency's decline, and its total reserves have decreased by $62.2 billion. Japan, which is now running a record current account deficit, can also be expected to sell treasuries.

Even China could become a seller of treasuries as it mobilizes its dollar reserves . The Chinese government has sent clear signals that it is shifting from passive to active management of its reserve and is exploring more efficient ways to use its reserves to boost its domestic economy.

3) Retirement inflows into treasuries are over

The steady accumulation of treasuries by government retirement funds has helped absorb the supply of treasury bonds for over three decades. This accumulation of government debt to secure the retirement of baby boomers helped drive down treasury yields and fund deficit spending. As of September 2008, the four biggest of these funds held 3.3 trillion treasuries:

2150 billion (Federal old-age and survivors insurance trust fund)

615 billion (Federal employees retirement fund)

318 billion (federal hospital insurance trust fund)

217 billion (federal disability insurance trust fund) (for more on these four funds, see where social security tax amounts are deposited )

3300 billion total

Today, the accumulation of treasuries by government retirement funds is over. Baby boomers are beginning to retire, increasing outflows, and unemployment is rising, cutting inflows. More importantly, the 3.3 trillion already accumulated in these funds provides an enormous political incentive to prevent treasury prices from collapsing. Faced with a run on treasuries, politicians, rather than explaining to baby boomers that their retirement savings are gone, will instruct the fed to monetize treasury bonds. This alone will prevent the fed from reversing its current balance sheet expansion.

4) Deleveraging in credit-default swap market will drive up risk premiums

If you have been following the credit crisis in any detail, you might have heard that the 53 trillion credit-default swap market threatening the solvency of the financial system. What you might not have heard is the other dire threat posed by the CDS market: drastically higher risk premiums on all forms of debt.

These higher risk premiums are the result of reversing the process by which credit-default swaps were leveraged up and packaged into investment vehicles . Some examples of these horrors are:

Synthetic CDOs

As opposed to regular CDOs (which contain actual bonds), synthetic CDOs provide income to investors by selling credit-default swaps on hundreds bonds from companies and governments.

To juice returns, these synthetic CDOs disproportionally insured the riskiest AAA rated debt, such as Lehman's bonds. Synthetic CDOs are estimated to have sold insurance on between $1.25 trillion to $6 trillion worth of bonds.

Constant-Proportion Debt Obligations

CPDOs are specialized funds which work exactly like synthetic CDOs but with one major difference: they used leverage to boost returns. These CPDO funds typically borrowed about $15 for every dollar invested with them. They also contain safety triggers that force the liquidation of their investments if losses reach a predetermined level, and most CPDO funds have begun to hit these triggers. For example, Three CPDO funds launched in 2006 by Dutch bank ABN Amro Holding NV have already been forced to liquidate as credit insurance costs spiked and their credit ratings were downgraded.

Credit Derivative Product Companies

CDPPs are another group of specialized funds which work exactly like synthetic CDOs and CPDO funds, except for one key difference: they used an insane amount of leverage, as much as $80 for every dollar invested. CDPP funds together with subprime CDOs squared are finalists for the title of “most idiotic financial instrument ever created” .

Since these leveraged investment vehicles sold an enormous amount of insurance, the premiums for CDS insurance dropped sharply, making corporate debt seem safer and lowering interest rates. In effect, the process of building up the 53 trillion CDS market created an era of artificially low risk premiums on all forms of debt. Unfortunately, the pendulum is now swinging in the other direction, and the pain has just begun.

As investors attempt to get out of synthetic CDOs and CPDO/CDPP funds try to deleverage, they push up the cost of default insurance. In turn, that raises the risk premium on all forms of debt since most investors use the cost of default insurance as a guide when deciding at what interest rate they will buy bonds. Many banks are also tying corporate loan rates to credit-default swaps, raising borrowing costs and exposing companies to an overleveraged derivative market which is largely responsible for crippling the financial system.

The graph below shows how the cost of insuring the debt of EU nations is being driven up.

The rising cost of insuring debt is impacting treasuries too. The cost to hedge against losses on $10 million of Treasuries is now about $100,000 annually for 10 years, up from $1,000 in the first half of 2007. These rising insurance costs have helped push up treasury yields in the last few months. Worse still, the rising costs of insuring against government defaults will undermine faith in dollar. After all, the CDS market is telling us that 10-year treasury notes have become 100 times riskier in the last two years.

5) Unwinding the Gold carry trade

The massive expansion in the US money supply will undoubtedly drive gold prices several times higher and force the unwinding of the gold carry trade. To see the threat which unwinding the gold carry trade poses, it is necessary to understand how US and UK financial institutions got themselves stuck in an enormous short position in gold from which they have no hope of ever escaping. For that purpose, I have outlined below the five steps Wall Street seems to repeat endlessly on its path to ruin.

Step 1: Wall Street embraces a false paradigm

“Housing prices never fall”

-----

“gold is a relic” or “gold is in a permanent downtrend”

Step 2: Wall Street makes billions embracing this false paradigm…

US/UK Financial institutions made billion in fees from making mortgage loans and securitizing them.

-----

US/UK Financial institutions made billions via gold carry trade. Here is an ultra quick explanation how it works from zealllc.com

So, if you can find a cheap enough cost of capital, a safe enough destination, and you have the credit to borrow large amounts of money, you too could make enormous profits in carry trades. The notorious gold carry trade is based on the exact same idea. Elite money-center bullion banks were given sweetheart opportunities to borrow central bank physical gold at 1%, sell it in the open market, and immediately invest the proceeds in higher yielding “safe” investments and reap vast profits.

As Moneyweek further explains :

It seemed like a no-brainer. The central banks got to squeeze a yield from their gold. The borrowers got to sell the gold on, and use the proceeds to fund more exciting investments like 10-year US Treasuries yielding 4% per year or so. Yes, these 'carry trade' returns were tiny. But the cost of borrowing gold was tinier still.

Step 3: …and creates a catastrophic mess in the process

Enormous housing bubble

Subprime CDOs squared

Off balance sheet SIVs

Etc…

-----

Commercial banks and speculators are left inescapably short gold. These ridiculous short positions are best captured by John Hathaway in his 1999 article, The Golden Pyramid .

The recipe for a shortage has been carefully followed. A few finishing touches may be required before a market epiphany. There is no known reconciliation between paper and physical positions, and none will be attempted until after the squeeze. The weakness of credit analysis and supervisory oversight, as well as the many ambiguities in the linkage between paper gold and physical can flourish only if there is supreme confidence in gold's permanent downtrend. The trust and confidence essential to balance the gold derivatives pyramid depends on three critical errors: that mine reserves = physical gold; that gold receivables = gold on hand; and that financial markets will enjoy smooth sailing indefinitely. Trust is nothing more than a state of mind. When this levitation is finally exposed and its illusions shattered, it is ludicrous to think the imbalances can be corrected by a small rise in the price and within a comfortable time frame. Expect the resolution to be swift, furious, and uncomfortable for those caught short.

Step 4: Something goes horribly wrong

Subprime borrowers start defaulting

Housing prices plummet

-----

Gold prices shoot up after the 1999 Washington Agreement on Gold (EU central banks agreed to limits on gold sales/leasing).

This gold bear trap is best described by Reginald H. Howe in his report about central banks at the abyss .

The first Washington Agreement on Gold , announced in September 1999 at the close of the annual meetings of the International Monetary Fund and World Bank in Washington, D.C., placed limits for the next five years on the official gold sales of the signatories as well as on their gold lending and use of futures and options. Put together at the instigation of major Euro Area central banks in response to the decline in gold prices caused by the series of U.K. gold auctions announced in May of the same year, WAG I caused gold prices to shoot sharply higher.

Within days, as gold shorts rushed to cover, the price jumped from around $265 to almost $330/oz. and gold lease rates spiked to over 9%. The rally caught the major bullion banks completely wrong-footed, resulting in the panic later described by Edward A.J. George , then Governor of the Bank of England (Complaint, 55):

We looked into the abyss if the gold price rose further. A further rise would have taken down one or several trading houses, which might have taken down all the rest in their wake. Therefore at any price, at any cost, the central banks had to quell the gold price, manage it. It was very difficult to get the gold price under control but we have now succeeded. The U.S. Fed was very active in getting the gold price down. So was the U.K.

Despite managing to “get the gold price under control”, US/UK bullion banks (JPMorgan, HSBC, etc…) have been stuck on the short side of gold ever since.

Step 5: The US fed and UK do everything in their power to “save the financial system”

Royal Bank of Scotland bailout

Bear Stearns bailout

Freddie/Fannie bailout

AIG bailout

US/UK Quantitative easing

Etc…

-----

Leasing out all US/UK gold to bullion banks

Gold swaps with foreign central banks (then leasing out the gold)

Convincing allies to sell gold

Writing naked call options on gold

Britain's 1999 gold sales

Pre-emptive gold sales

Allowing JPMorgan's and HSBC's manipulation of COMEX futures

Etc …

Make no mistake, gold prices have suppressed, but calling this process a “conspiracy” would be inaccurate. Gold suppression by the US and UK is better characterized as a desperate cover-up. Furthermore, while a side affect of the gold carry trade and gold suppression was to drive down interest rates, that was never their intended effect. A desire to hold interest rates would not have been enough to push the fed or the Bank of England to manipulate gold prices. It was only the threat of the total collapse of US/UK financial system which prompted the suppression of gold. The unwinding of the gold carry trade would have (and will) dragged down the some of the biggest US/UK banks under (JPMorgan, HSBC, etc…) and that was what had to be prevented at any cost.

Stay away from any form of paper gold: GLD (HSBC is custodian), gold pools and unallocated gold accounts , gold futures , etc… Paper gold investments are guaranteed to default before this crisis ends.

Besides leaving the financial system inescapably short gold, the gold carry trade also drove down yields on treasuries and other US debt, as commercial banks invested the proceeds from the sale of borrowed central bank gold and other naked short positions. Unwinding the gold carry trade involves the purchase of physical gold, but also the sale of the investments linked to the gold short positions. As the fed begins 15-fold expansion of the monetary base (which logically should eventually send gold prices up at least ten times where they are now), the unwinding and fallout of the gold carry trade seems imminent.

6) The return of the 580 billion dollars circulating abroad

Over the last thirty years, the steady outflow of 580 billion dollars has helped drive down interest rates. For example, If 10 billion dollars leaked out of the US and began circulating abroad, the fed would print 10 billion and buy treasuries in order to replenish the domestic money supply. So the 580 billion dollars held abroad resulted in the purchase of roughly 580 billion treasury bonds by the fed, thereby increasing demand for US debt.

While the accumulation of oversea dollars has been beneficial in the past, today the large pools of dollars circulating in foreign hands pose a threat. With many dollar alternatives becoming available, US oversea currency looks increasingly likely to start flowing back home. The main currencies with the potential to displace dollars are:

A) The Chinese yuan which is becoming an international currency

B) The Khaleeji, a new currency being launched by Gulf states which will be possibly backed by gold.

C) The Euro with its partial gold backing

D) Gold

Furthermore, now that the fed has begun creating money at an accelerating rate, the extensive foreign holdings of US currency might exacerbate the effects of inflation fears. As foreign dollar holders' confidence in the dollar is eroded, they will trade their dollars for alternate stores of value (yuan, euro, gold, etc…), potentially sending a flood of currency back to the US. If the Fed failed to reduce the supply of currency to counteract dollars being unloaded from abroad, the inflationary consequences would be made worse as the mass reversal of currency flows from foreigners to the US becomes overwhelming.

7) Interest rate derivates nightmare

The threat posed by interest rate derivates is perhaps the greatest out of all the ones outlined so far. It is also the one hardest to understand. The first thing to note about interest rate swaps is the size of the market, as explained by the Wikipedia :

The Bank for International Settlements reports that interest rate swaps are the largest component of the global OTC derivative market. The notional amount outstanding as of December 2006 in OTC interest rate swaps was $229.8 trillion , up $60.7 trillion (35.9%) from December 2005. These contracts account for 55.4% of the entire $415 trillion OTC derivative market. As of Dec 2007 the number rose to 309,6 trillion according to the same source.

The growth in interest rate swaps creates demand for bonds because many of these interest derivatives require the purchase of bonds as a hedge. Rob Kirby on 321gold.com explains this in his article, the real ponzi scheme - "unreal interest rates" .

Interest Rate Swaps create demand for bonds because bond trades are implicitly embedded in these transactions. Without end user demand for the product - trading for "trading sake" creates ARTIFICIAL demand for bonds. This manipulates rates lower than they otherwise would be.

…

Interest rate swaps were originally developed to [1] allow parties to exchange streams of interest payments for another party's stream of cash flows; [2] manage fixed or floating assets and liabilities and [3] to speculate - replicating unfunded bond exposures to profit from changes in interest rates. Growth in the first two of these activities are dependent on their being increased end-user-demand for these products - graph 1 above indicated that this is not the case:

In the case of J.P. Morgan in particular [forgetting about the lesser obscenities at Citi and B of A]; their interest rate swap book is so big that there are not enough U.S. Government bonds being issued or in existence for them to adequately hedge their positions.

This means that the obscene, explosive growth in interest rate derivatives was all about overwhelming the long end of the interest rate complex to ensure that every and any U.S. Government bond ever issued had a buyer on attractive terms for the issuer. Concurrent with the neutering of usury, the price of gold was also "capped" largely through Fed appointed banks "shorting gold futures" as well as brokering gold leases [sales in drag] sourcing vaulted Sovereign Central Bank gold bullion. The gold price had to be rigged concurrently because historically, according to observations outlined in Gibson's Paradox - lowering interest rates leads to a higher gold price. Gold price strength is historically synonymous with U.S. Dollar weakness which leads to higher financing costs or the possibility of capital flight.

Same as with the gold carry trade, while the explosive growth in interest rate derivatives did reduce interest rates by creating demand for bonds, I am not sure about the conspiracy element. From everything I have seen and read during the credit crisis, the wizards of Wall Street (ie: the creators of the subprime CDO squared and other horrors) and the Federal Reserve seem more like children playing with dynamite rather than masterminds capable of pulling off vast conspiracies.

The greater threat posed by interest rate swaps

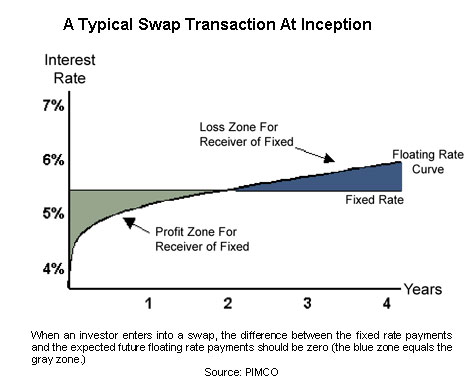

Besides creating artificial demand for bonds, the interest rate swap market poses a systematic risk exceeding that of the credit-default swap market because of its enormous size and the fact that each interest rate swap contract offers the potential for unlimited losses. The graph below should help show this danger.

In a currency collapse (which is where we are headed with Bernanke's 15-fold increase in the money supply), interest rates follow inflation to astronomical heights. Loans for 24 hour periods and interest rates in the five or six digits are common in hyperinflation, and, should they occur here in the States, anyone “short the swap” (the floating-rate payers in interest rate swaps) will be crushed into oblivion. At least with credit default swaps, there is a limit to how much investors can lose.

8) The liquidation of the 8 Trillion dollar holdings of overleveraged European banks

European banks increased their dollar assets sharply in the last decade which helped drive down US interest rates and absorbed a large portion of America's growing debt. Their combined long dollar positions grew to more than $800 billion by mid-2007. This $800 billion was then leveraged into $8 trillion in US assets. The low capital ratios of these dollar positions were acceptable to regulators because European banks are allowed to apply a lot more leverage as long as they are buying exclusively AAA rated securities.

Unfortunately, as we have learned over the past 18 months, AAA is not always AAA. While much of the AAA rated securities bought by European banks were treasuries and agencies, some of these AAA rated securities were senior securitized loans that are still marked close to par on the balance sheet of European banks despite the fact they trade around 70 cents on the dollar in the markets. The enormous unrealized losses on their US holdings are only one of the problems facing European banks.

The other is the loss of their dollar funding. The enormous leverage employed by European banks to purchase toxic AAA rated assets was funded in great part by loans from US money market funds. After Lehman's default led to massive withdrawals from those money market funds, European banks lost access to billions in dollar funding.

If European banks are forced to sell their 8 trillion US assets , it will crash the credit markets, and they will have to recognize enormous losses. Since the fed is desperate to prevent the collapse of the US financial system, it lent those European banks 600 billion dollars so that they wouldn't be forced to sell. Meanwhile, European banks accepted this 600 billion because they don't want to recognize losses on their toxic US securities.

What is going to happen next with these overleveraged European banks?

Well, if history is any guide, the outlook isn't good for the US financial system :

“When the American economy fell into depression, US banks recalled their loans, causing the German banking system to collapse”

The same thing will happen in 2009, except the roles will be reversed. It will be European banks that will recall their loans and sell off dollar assets, causing the US banking system to collapse.

What could convince European banks sell off their US assets at firesale prices?

The answer is simple: fear of a dollar collapse. With the fed increasing the monetary base 15-fold, the strategy of waiting for impaired assets to recover becomes meaningless: with the dollar likely to lose nine tenths of its value in the next year, waiting for assets trading 70 cents on the dollar to recover is a senseless venture.

9) Inflation expectations

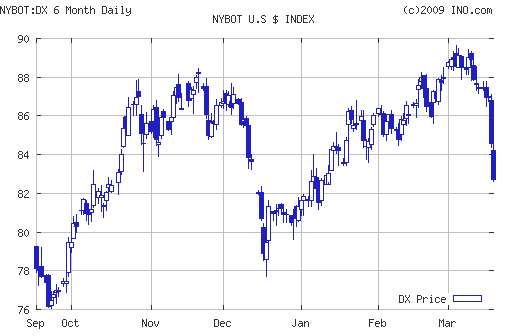

The US's experience during the Great Depression has left America dominated by Keynesian thinking and prone to deflation fears . As a result, inflation expectations are about nonexistent right now despite the current financial crisis. However, the fed's latest plan to expand the monetary base 15-fold should give pause to even the most hardened deflationist. Indeed someone must be worried, because the fed's Wednesday announcement has caused a dramatic collapse of the dollar:

The sheer size the fed's monetary expansion and the dollar's fall will soon increase both inflation and inflation expectations. This in turn will put upwards pressure on treasury yields.

Conclusion

During the last three decades, long-term interests rates have fallen steadily in US, as demonstrated by the chart below

Logically speaking, the chart above makes no sense. The fundamentals underlying the US economy have grown steadily worse over the last thirty years. For example, in 2006, the US's current account deficit nearly hit 9 percent of our gdp, and economists usually consider 4 percent to be unsustainable. There are also the US's chronic budget deficits and the massive projected social security shortfalls. Even more incomprehensible, over the last six months the yield on long-term treasuries has fallen in the face of a disintegrating economy and massive expansion in the supply of treasuries. This is NOT how the world works: as the financial health of borrowers decrease, their interest rates are supposed to go up. The only rational explanation is that some combination of forces has been unnaturally driving rates lower. These forces, (outlined above) which have been driving interest rates down, are today threats and issues which need to be resolved before the financial crisis can end:

The US budget deficit

The crisis in entitlement spending

The trade deficit and large holdings of treasury reserves

The credit-default swap market

The gold carry trade

The 580 billion dollar circulating overseas

The 8 trillion dollar assets accumulated by European banks

The interest rate swaps market

The Keynesian thinking dominating US economic and fiscal policy

By Eric deCarbonnel

http://www.marketskeptics.com

Eric is the Editor of Market Skeptics

© 2009 Copyright Eric deCarbonnel - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Eric deCarbonnel Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.