Debt Crisis Economic End Game, Future Evolution of the Debt-to-GDP Ratio

Economics / Global Economy May 19, 2009 - 05:08 AM GMTBy: John_Mauldin

Nearly everyone I talk with has the sense that we are at some critical point in our economic and national paths, not just in the US but in the world. One path will lead us back to relative growth and another set of choices leads us down a path which will put a very real drag on economic growth and recovery. For most of us, there is very little we can do (besides vote and lobby) about the actual choices. What we can do is adjust our personal portfolios to be synchronized with the direction of the economy. The question is "What will that direction be?"

Nearly everyone I talk with has the sense that we are at some critical point in our economic and national paths, not just in the US but in the world. One path will lead us back to relative growth and another set of choices leads us down a path which will put a very real drag on economic growth and recovery. For most of us, there is very little we can do (besides vote and lobby) about the actual choices. What we can do is adjust our personal portfolios to be synchronized with the direction of the economy. The question is "What will that direction be?"

Today we are going to look at what I think is a very clear roadmap given to us by Dr. Woody Brock, the head of Strategic Economic Decisions and one of the smartest analysts I have come in contact with over the years. This week's Outside the Box is his recent essay, "The End Games Draws Nigh." For those who have the contacts in government, I urge you to put this piece into the correct hands so that Woody's very distinct message gets out. I think this is one of the most important Outside the Box letters I have sent out.

Woody normally does not allow his work to go beyond the circles of his clients, but I suggested to him that this piece was quite macro in cope and important for both individuals and policy makers everywhere to understand. In my own simple terms, trees cannot grow in some unlimited manner to the sky. Families cannot grow debt without limit beyond the growth of their incomes. And countries have the same constraints. While growth of debt in the short term is viable, growth of debt faster than the growth of GDP is not viable over the long run. This is not debatable. It is a simple fact. Therefore, as Woody says, it is important that you get the growth side of the equation right as you increase the debt side. Without the proper balance, you are heading for disaster.

From his intro:

"We weave these three concepts together so as to make possible an extension and generalization of "macroeconomic policy" as normally understood. Central to this extension is the need for policies that drive down the nation's Debt-to-GDP Ratio over time. Accordingly, we identify 15 policies that jointly reduce the growth of federal debt and increase the growth of GDP over time. Doing so not only points to a new set of policies for exiting today's quagmire, but also permits an appraisal of the Obama administration's current policy proposals. Regrettably these proposals do not fare well with respect to growth. Furthermore, the extension of macroeconomics we propose applies not only to the US economy, but to most all others as well. It should thus be of interest to readers everywhere."

This is longer than the usual Outside the Box, and will require you to put on your thinking cap. But you need to digest this, and especially the conclusions. But it is very important that you understand the principles and concepts Woody discusses. We are at a very critical juncture, and the paths we choose will have profound impacts on our lives and fortunes. I cannot overemphasize the point. If we choose a path of growing debt faster than we can grow GDP, the negative implications for many traditional asset classes are enormous.

Let me again thank Woody for allowing me to send this on to you. And for those who post this letter on various sites, just be sure to include a link to Woody's website, www.sedinc.com. For those interested in his subscription service you can contact Woody at woody@sedinc.com or visit his website.

Thanks, John Mauldin, Editor Outside the Box

The End Game Draws Nigh - The Future Evolution of the Debt-to-GDP Ratio

By Horace "Woody" Brock, Ph.D.

Preface: In this new report, we link together three quite different concepts that have been discussed in these publications during recent years. First, the problems posed for classical fiscal and monetary policy when extremely large deficits must be financed; second, the critical importance of the rate of economic growth as primus inter pares of all economic variables; and third, the all-important concept of "incentive-structure-compatibility" introduced by Leonid Hurwicz in the 1960s, and recognized in the award to him in 2007 of the Nobel Memorial Prize.

We weave these three concepts together so as to make possible an extension and generalization of "macroeconomic policy" as normally understood. Central to this extension is the need for policies that drive down the nation's Debt-to-GDP Ratio over time. Accordingly, we identify 15 policies that jointly reduce the growth of federal debt and increase the growth of GDP over time.

Doing so not only points to a new set of policies for exiting today's quagmire, but also permits an appraisal of the Obama administration's current policy proposals. Regrettably these proposals do not fare well. Furthermore, the extension of macroeconomics we propose applies not only to the US economy, but to most all others as well. It should thus be of interest to readers everywhere.

A. Introduction and Overview

In our 2008 research programme, we focused on three issues. First, what exactly caused the worst credit crunch the nation has arguably experienced since the depression of the 1930s? Second, how did the downturn in the US morph into a collapse in Planet Earth's GDP rate from nearly 5% in June 2008 to -0.5% in winter 2009? Third, can traditional macroeconomic policy suffice to turn around the economy? More specifically, will a killer application of classical fiscal and monetary policy truly restore the economy to a stable growth trajectory? Or is there an internal contradiction within macroeconomic policy that could prevent it from succeeding this time around?

To explain the "perfect storm" in the credit market, we drew extensively on the new Stanford theory of endogenous risk to demonstrate that there are three jointly necessary and sufficient conditions to predict and explain the perfect storm we have experienced: (i) A mistaken market forecast of some exogenous event that impacts security prices (in this case, a vastly higher than expected default rate on mortgages); (ii) A high level of Pricing Model Uncertainty bedeviling bank assets (the true cause of the "toxicity" of those complex securities that have clogged the

arteries of the banking sector); and (iii) An unprecedentedly high degree of leverage in the financial sector (money center banks had off-and-on balance sheet leverage of about 40:1 in contrast to the socially optimal leverage of 10:1). The reader can tack "greed" and "incompetence" onto this triad, although doing so diverts attention from the real causes of today's crisis.

To explain the collapse of economic growth worldwide in an astonishingly short period, we utilized a game theory model that explained how the cessation of inter-bank lending amongst the principal money center banks of the world precipitated the first known case of global credit market emphysema: The availability of credit dried up almost everywhere in the course of six months, from Auckland to Iceland. We stressed that this credit contraction had little to do with "globalization" as properly understood, and had no counter-part in history.

To explain the potential failure of fiscal and monetary policy in restoring growth, we demonstrated how the financing of exceptionally large government deficits usually causes a sharp rise in longer-term real interest rates -- a rise that bites back and offsets the GDP impact of the fiscal stimulus being applied. The logic leading to this conclusion is reviewed just below in the context of Figure 2.

B. The Good News -- A World of Greatly Reduced Uncertainty

A year ago, even six months ago, the great debate centered on whether the credit market crisis would precipitate either a US or global recession. A majority predicted a manageable recession in the US, but nowhere else with the possible exception of the UK. Uncertainty was great, and kept increasing until recently -- but no longer. The good news today is that this uncertainty has disappeared. For we now know with probability ¹ that everything sucks everywhere. Welcome to a risk free world!

To wit, the G-7 economies are all in recession, and more astonishingly the economy of the planet earth is growing at about -1% or even less. Earnings are crumbling, global trade has decreased by nearly 10%, rising global unemployment foretokens social unrest in many quarters, industrial production has dropped more than ever before, and excess capacity is rising in almost all manufacturing sectors globally. Stephen Roach of Morgan Stanley believes that the "world output gap" could reach a mind boggling 8%-10% by year end. All in all, we have witnessed problems that originated within the US give rise to global scenarios that were virtually unthinkable as recently as the summer of 2008, and do so with blinding speed.

Within the US, there are two parallel problems. First, the nation faces a hitherto unprecedented growth of Federal debt, over both the short and long run. Second, there is the severity of the recession itself. Figure 1 offers a simple way of understanding what killed growth in the US economy. The variables shown remind us of the old adage that "History rhymes, but does not repeat."

History Rhymes: More specifically, the contents of the figure will disturb those seeking to identify today's US recession with earlier ones in 2001 or 1991 or 1981 or 1973 or even 1931. No such identification is possible since the three developments highlighted in the chart and their improbable synergies are different from anything we have seen before. This sui generic nature of today's crisis explains why traditional theories of recessions and "debt super-cycles" possess little explanatory and predictive power.

For example, according to standard business cycle theory, "pent-up demand" on the part of consumers is a principal driver of recovery -- but it will not be this time around. The shift towards less consumption and more savings due to the implosion of household balance sheets and to demographics is most probably permanent. If so, this bodes poorly for hopes of a pent-updemand-driven recovery.

History Repeats: While the context of today's crisis differs from those in the past, history repeats itself in that the common denominator of this and all other debt crises has been excess leverage -- our mantra in these pages for three years. Our greatest fear was that the all-important role of leverage would be sidestepped in the rush to assign blame and reform the financial system. In this regard, it is dismaying that, whereas we have now vented our anger at bankers and capped bonuses, we have not capped leverage. To be sure, there are calls for "improved bank capitalization" and related reforms, but the crucial role of excess leverage in bringing down the global financial system has not been properly recognized. Instead, excess "greed" has been the principal focus.

Then again, from a game theoretic viewpoint, it may not be surprising that the role of leverage has been underplayed. For leverage is precisely what is required for financiers to reap those huge incomes needed to fund both political parties in Washington, not to mention those "blockbuster" exhibitions we all love so much at the Metropolitan Museum of Art in New York. Stay tuned for Loophole Analysis 101.

C. The Bad News -- Two New Uncertainties

Two new uncertainties are now rising to the fore. First, will traditional fiscal and monetary policy suffice to restore economic growth -- and in the process restore the viability of the financial sector? Without the latter, there is little hope of revived growth. Our concerns about the inadequacy of traditional macroeconomic policy were discussed at length in our February 2009 PROFILE, and are summarized in Figure 2 taken from that analysis. The flattening out of the stimulus curve in the figure reflects that, when fiscal stimulus exceeds a certain level (e.g., 7% on the horizontal axis), the financing of deficits is likely to cause a sharp increase in real longer-term interest rates. Importantly, this holds true regardless of whether the huge deficits are monetized for reasons we carefully articulated. Higher real yields in turn neutralize the original fiscal stimulus, thus causing the curve to flatten out.1

We concluded that the risks of policy failure in today's context are disturbing. Moreover, even if traditional policies do prove successful in the shorter run, there is a genuine risk that the huge amount of debt that accrues and must be serviced in the future could transform the US into a "banana republic" in the much longer run. This risk is heightened by the need to fund soaring Social Security and Medicare "entitlements," as record numbers of baby-boomers retire during the next two decades. Moreover, as time goes on, it is precisely these longer-term risks that will matter most to the market, and will increasingly be discounted. Investors of every stripe will be impacted.

The second new uncertainty focuses on whether new and different fiscal and monetary policies can help salvage matters, and guarantee a happier ending.

If the effectiveness of traditional macroeconomic remedies is in doubt, can its arsenal of policies be expanded so as to restore strong longer-term equilibrium growth? The answer is yes, and it is the purpose of this new essay to sketch such an extension of classical macroeconomics.

D. The Critical Dynamics of the Debt-to-GDP Ratio

There is nothing new about a nation running into trouble and running up large amounts of debt in bailing itself out. There is also nothing new about attempting to monetize (via "quantitative easing") the resulting accumulation of debt. The good news for the US is that its total federal debt of some $10T at the outset of the crisis in 2008 was a manageable 70% of current GDP of $14T.² Suppose debt rises $3T by the end of 2011 as the Congressional Budget Office now predicts, and then rises $7T more by 2020. The result will have been a doubling of federal debt between 2008 and 2020, rising from $10T to $20T.³ While this increase is shocking, some forecasts are much worse.

Suppose, moreover, that GDP rises conservatively to $17 trillion in 2020 from today's $14T as a result of a modest 2% GDP growth recovery between 2011 and 2020. Then the federal Debt-to-GDP ratio would rise from today's 0.7 to 1.18. Interestingly, this does not represent the disaster many observers assume. To begin with, there are nations where a disturbingly high Debt-to-GDP ratio proceeded to fall way back down over time. Thus, the US Debt-to-GDP ratio was 1.25 at the end of World War II, yet it fell to 0.25 by 1980. Britain's Debt ratio upon defeating Napoleon in 1815 was over 2.7, and it fell back to 0.2 by the end of the 19th century.

In other cases, the Debt-to-GDP ratio has stayed persistently high, neither increasing nor decreasing dramatically over time. Thus Japan has had a very high ratio of 1.5 to 1.8 for the past decade. Italy and Belgium, too, have sustained high ratios in the range of 1 to 1.25. Finally, there are the countries where the Debt ratio continues to rise after some initial shock with either hyperinflation or outright default being the end result. Such has been the fate of myriad banana republics including some large players such as Brazil, Argentina and Russia. What exactly determines which nations dig their way out, or else go under? This will be our primary focus in the pages ahead.

Rebounders versus "Banana Republics": To begin with, note that what matters is not a onetime rise in the Debt-to-GDP ratio due to a particular shock (e.g., today's US housing and credit crises), but rather the dynamic trajectory of the ratio in the years subsequent to the initial rise. It is the direction of this trajectory that is all-important. If the Debt ratio continues to rise, then it tends to accelerate due to the ever-rising cost of servicing this ever-rising "primary" deficit. Not only does the increasing debt-load itself cause ever-higher servicing costs, but the rising real rates that typically result from ever-greater debt make the spiral ever worse. The result can be economic and social collapse.

If, on the other hand, the Debt-to-GDP ratio stagnates, it tends to be associated with very low real growth, political paralysis, and a degree of social disenchantment. If the ratio falls, it is usually because of a combination of two developments: higher real growth and vigorous fiscal discipline. Rising living standards, dreams of a better future, and a sustained belief in democracy are associated with this happiest of trajectories.

Three Sets of Scenarios: Figures 3.A - 3.C illustrate the stunning range of outcomes that can result from sustained differences in the growth rates of debt versus of GDP. We have adapted the analysis here to the case of the US. We assume an initial federal debt burden of $12T for 2011, and an initial GDP value of $14T. We then grow these forward at the stipulated growth rates.

At the one extreme of very low economic growth and very high debt growth, the Debt ratio rises to an arresting 18 -- a half-way house to Zimbabwe. At the opposite extreme, the ratio falls to a paltry 0.4, half of today's level. These two extreme outcomes are circled in the table.

The data in the tables represent real growth rates of both debt and GDP.

E. The Case for Driving Down the Debt-to-GDP Ratio - "It's the Growth Rate, Stupid!"

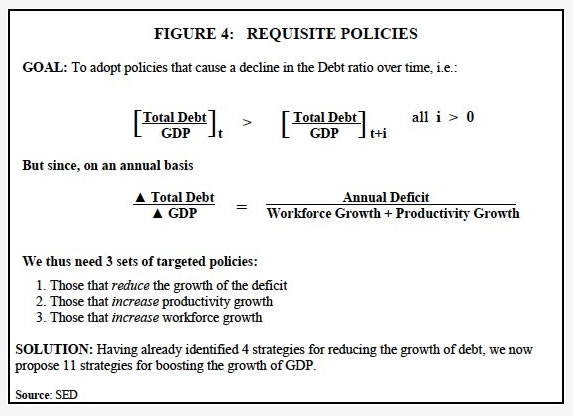

We can deduce from the foregoing analysis that sustainable long run economic recovery from a debt overload requires two sets of policies: One set must be dedicated to curtailing the growth of government spending and hence, the growth of the deficit. The other set must be dedicated to maximizing real economic growth. In this way, both the numerator and the denominator of the killer Debt-to-GDP ratio will be managed so as to maximize future social welfare.

Policies aimed at augmenting real growth are arguably the more important here. This is because more rapid growth not only reduces the Debt ratio, but also causes swelling tax revenues which can help to reduce the deficit each year. That is, stronger growth drives both the numerator and the denominator in the right directions.

This reality underscores why "It's the real growth rate" must become the mantra of recoveries not only in the US, but almost everywhere else as well. Note that this "strong growth" mantra is a far cry from the Obama administration's counsel to the world at the recent G-7 conference: "Stimulate everywhere by running higher deficits!"

The True Payoffs from Strong Growth: Looking at matters from a game theoretical "Who wins?" standpoint, strong economic growth is the rising tide that lifts all ships. Within a given nation, it alone offers win-win strategies whereby most all interest groups can come out ahead. Externally across nations, strong growth generates expanding trade. Happily, the game of trade between nations is that all-important positive-sum game that encourages peace and discourages war. It creates "the ties that bind." For example, the recent globalization of the supply chain is a principal reason why the business community has been so strangely silent in demanding protectionist policies during the present crisis. When a significant portion of your own manufacturing inputs come from "abroad," do you really want trade barriers?

Finally, and perhaps most importantly, productivity-driven strong growth alone increases living standards that boost the hopes and dreams of people everywhere for a better tomorrow for their children. When citizens have realistic hopes of a better tomorrow, social unrest is minimized. Conversely, when prospects for the long run are grim, voters are easily swayed by demagogues to vote for the Hitler of their day.

Three Important Books: Are these points obvious? They should be, but they frankly are not. Moreover, they are never sufficiently emphasized, and virtually no orientation towards rapid future growth is evident in the policies and "reforms" proposed by the Obama administration, as we see in Section G below. The arguments set forth in three books support the view we are taking as regards the critical role of growth.

First, a widespread lack of understanding and appreciation of growth led Professor Ben Friedman of Harvard University to write his superb book, The Moral Consequences of Economic Growth (A. Knopf, 2005). This is the best work we know of that makes the case for growth and (more implicitly) for globalization at an appropriate economic and moral level of analysis.

Second, and at a more practical level, Alan Beattie's brand new book False Economy: A Surprising Economic History of the World (Riverhead Press, 2009) provides myriad case studies of how nations chose between success or survival or ruin by the specific policies they adopt. His case studies make very clear indeed how policies that depress the Debt-to-GDP ratio of Figure 3 correlate strongly with success, whereas policies that inflate the ratio correlate with ruin.

Third, at an even deeper and more theoretical level, there is the late Mancur Olson's magisterial The Rise and Decline of Nations: Economic Growth, Stagflation, and Social Rigidities (Yale University Press, 1982). Olson explains from first principles how special interest groups become entrenched and, in defending their turf, usually cause nations to go bust. [Our "entitlements lobby" anybody?]

Olson's logic is game theoretical: He shows that special interest groups become the principal players in a generalized Prisoner's Dilemma game whereby individually group-rational strategies lead to the collectively irrational outcomes of declining growth, diminishing dreams, increasing social unrest, and ultimately ruin.

This book should be required reading by anyone serving in government. It is one of the best books the present author has ever read in the field of political economy.

F. Four Debt-Minimizing Strategies

Before turning to those all-important strategies for maximizing the growth in the denominator of the Debt-to-GDP ratio, consider several different strategies for minimizing the growth of the numerator.

First, counter-cyclical policies should consist of temporary increases in spending -- spending that automatically expires with no Congressional vote when good times return. The Obama administration policies largely amount to permanent spending increases, and have been widely criticized as such.

Second, a new set of government accounts must be introduced that clearly distinguish government investment expenditures from non-investment expenditures. The former should not be included as part of "the deficit." Only an appropriately amortized portion should be included. Moreover, for reasons stressed below, infrastructure investments should take priority when discretionary government spending decisions are made. The current administration has not proposed the required accounting changes. This is, of course, consistent with its failure to propose serious investment spending in the first place (see below).

Third, true leadership -not to be confused with fine rhetoric- is needed to alert citizens to the true disaster we face if the growth of long-term federal debt is not curtailed. This is particularly true given the demographic realities that now lie around the corner. Nobody has made this point better than Stephen Roach in a recent commentary in Morgan Stanley's "Debating the Future of Capitalism" series, March 26, 2009:

I believe that Congress and the White House should collectively declare a formal "fiscal emergency" and empower a bi-partisan task force to develop new guidelines for federal budgetary control.

Washington did this once before in an effort to contain the runaway budget deficits of the Reagan era -- deficits that now look like child's play when compared with what lies ahead. The automatic spending caps and sequestration mechanisms prescribed by the GrammRudman-Hollings Balanced Budget and Emergency Deficit Control Acts of 1985 succeeded in taking some of the optionality out of the fiscal debate.

This problem is too big -- and the long-term stakes are too high -- for fiscal sustainability to be entrusted to the oft-politicized whims of the year-by-year discretionary budgeting process.

Slam Dunk! Given the reality that today's deficit crisis far exceeds that of the Reagan era, it is all the more irresponsible that the President has not already proposed the "fiscal emergency task force" that Roach correctly calls for. Paul Volcker: Where are you when we need you the most? The reforms that such a task force would propose are all pretty obvious, including "sunset provisions" for all manner of government mandates, entitlement reforms, an end of ear-marking, etc.

Fourth, as noted in Section E above, policies must be adopted that maximize economic growth since faster growth is the best way to generate those higher revenues needed to reduce a given deficit. We identify specific growth policies just below.

Lingering Doubts: Even longstanding Democratic Party liberals are now expressing shock at the staggering growth of long-term government debt the US now confronts. Nonetheless, the President's cheerful rhetoric suggests little concern with the growth of the numerator. To be sure, his administration's OMB budget projections blithely assume that very high growth rates will magically return after the next three years, and nothing solves fiscal problems as well as rapid growth. Yet everyone acknowledges that these projections are smoke-and-mirrors, constituting a leadership default of the first magnitude.

Yet could all of this be deliberate? Could the administration's choice to tax and spend ad infinitum have been politically strategic in nature? After all, haven't both President Obama and his chief of staff Rahm Emanuel openly admitted that "the new budget is a means to altering the very architecture of American life, with government playing a much larger role than before"? The likelihood that their new architecture would drive the growth of numerator of the Debt-to-GDP ratio ever-higher and the growth of the denominator lower was never mentioned.

Do financial commentators even understand this risk? While the press has expressed appropriate "concern" about the sea of red ink to come, there is little sense of the true End Game at stake: Which of our Figure 3 scenarios will occur, and what will it imply?

The answer may well determine whether we face a future of peace and prosperity, or of war and privation. As a personal aside, this author has never been more concerned than he is now about the economic state of the nation.

G. Growth-Maximizing Strategies

We now identify a plethora of growth-maximizing policies. Before doing so, however, we must recall the true origins of economic growth itself. Only by understanding these origins can we identify meaningful pro-growth policies.

G. 1. The Two Principal Sources of Real Economic Growth

At the most basic level, trend growth is the sum of workforce growth plus productivity growth. Intuitively, this rate of growth equals the rate of growth of the number of workers producing the pie, plus the rate of increase of pie production per person hour. In the latter case, we distinguish between productivity increases that result solely from "working smarter" versus increases that result from increased investment per worker, or "factor stuffing" in economics jargon. The former is called pure labor productivity growth (e.g., take a weekend off and invent the differential calculus), whereas the latter is referred to as total factor productivity growth.

The very rapid growth of emerging economies is usually due to a very high rate of increase in total factor productivity growth as workers gain access to roads, computers, medicines, and other productivity-improving (but not free!) endowments for the first time. Developed economies cannot replicate this strategy, so their growth rate is much lower than the "catch-up" rates in newer economies.

Thus, policies that augment growth must operate through two channels: Increasing productivity growth (via enhanced skills and investment), and/or increasing workforce growth.

Incentive-Structure-Compatibility: In proposing pro-growth policies of both kinds, we shall keep in mind the requirement that such policies be "incentive-structure-compatible" with growth, a concept first articulated by the economist and philosopher Leonid Hurwicz in the late 1950s. Everyone acknowledges the importance of incentives in a given situation, e.g., the appropriate carrots and sticks needed to raise children, to motivate workers, etc.

What Hurwicz first articulated was the way in which the totality of incentives throughout society -- its "incentive structure" -- could be conducive to achieving a particular societal goal, such as maximal growth. The great importance of Hurwicz's concept is that it provides the correct analytical bridge between the micro and macro domains of social life. This was a stunning achievement, and earned him the 2007 Nobel Memorial Prize.4

Most "policies" and "goals" promulgated by politicians turn out not to be incentivestructure-compatible with growth, or with any other defensible objective. That is to say, most policy proposals are hot air.

Figure 3 summarizes the structure of our argument up to this point.

G.2. Productivity-Enhancing Growth Strategies

During the past three decades, a great deal of research has been done to understand the true sources of productivity growth. In particular, Paul Romer of Stanford University developed his theory of "endogenous growth" in which the rate of productivity growth is determined within the economic system, as opposed to being modeled as an external "residual" as it previously had been. In what follows, we draw on this and related research in an informal manner.

1. Infrastructure-Orientated Fiscal Stimulus: Economists increasingly believe that consumption will fall by 7% from its 72% share of US GDP in 2007 to around 65% over the next three years. Moreover, they believe it will remain at a significantly lower level. Pessimists conclude that "without a recovery of household spending to previous levels, the economy will suffer for a long time." Yet this is not the case.

Should investment spending (both in the corporate sector and in government infrastructure spending) rise by an offsetting 7% of GDP, the growth rate of GDP will not only match, but in fact exceed its old rate of growth. This is due to the role of classical macroeconomic "accelerator/multiplier" theory: A dollar invested will generate much greater future output than a dollar of transfer payments or consumption-stimulating tax cuts.

As regards today's humongous fiscal deficits, this reality implies that, the more the deficit is dedicated to infrastructure investment each year, then (i) the greater productivity will be (recall that investment raises productivity), and (ii) the greater both job growth and output will be over time via the Keynesian multiplier theory. Since virtually everyone recognizes that US infrastructure spending has been woefully inadequate for decades, and that consumption has been excessive, the current recession has, in fact, presented the government with a golden opportunity to "rebalance" the composition of GDP in a highly desirable manner.

Yet there are two additional reasons why the increased deficit should be infrastructure-investment-orientated. First, government expenditure on productivity-raising investment is not, in fact, "an expenditure" that raises the deficit and frightens bond market vigilantes. For as explained above, government investment spending of this ilk should be amortized over time. Thus, the larger the investment share of a given stimulus package, the smaller the resulting deficit. Second, to the extent that today's deficit explosion burdens the young with much more debt to be serviced, then it is our moral obligation to dedicate the extra spending to investments that raise the productivity growth and thus the size the future GDP. Doing so clearly reduces the real burden on future tax payers of servicing the debt being accumulated today.

Given this rare opportunity -- and moral obligation -- to tilt the economy towards long overdue investment spending, how can the Obama stimulus package have fallen so short of the mark? It is frankly embarrassing to witness Chinese policy advisors like Professor Yu Qiao of Tsinghua University scolding the US about something as basic as this:

Most of Mr. Obama's stimulus spending is devoted to social programmes rather than growth promotion, which may exacerbate America's over-consumption problem and delay sustainable recovery.

Financial Times, Editorial page, April 1, 2009

Qiao's point parallels a principal point we are making in this essay. Why are we not reading this from Christina Romer or Larry Summers in Washington? Have the Best and the Brightest once again lost their moral integrity as they did during the Vietnam War era? Can they seriously believe that more transfer payments to Democratic Party special interest groups is what the nation needs in this hour of its distress? The author considers the composition of the proposed $3 trillion of discretionary stimulus over the next five years a moral travesty.

Case Study of Energy: As a case study in how poor the administration's policies are in this regard, consider its energy policies. Is anyone in the new administration reading about the disastrous 9% annual decrease in the output of "old" oil (yes, "peak oil" turned out to be true), in conjunction with a collapse of previously scheduled investments in exploration and development, and in refining capacity? Are they blind to the supply-crisis that is unfolding, one that calls not only for "renewable energy," but also for a major expansion of traditional oil and gas production?

By now, has it not become crystal clear that the increased production of traditional fuels should come from within the US, given the devolution of both the political leadership and the infrastructure of those thugocracies upon whom the US increasingly depends for 40% of its consumption? Is no thought being given to the rising probability of $500 oil prices -- or perhaps outright rationing -- when global energy demand recovers? [Recall how jointly price-inelastic demand and supply curves cause huge changes in price both upward and downward, as we demonstrated mathematically five years ago.]

Elementary arithmetic is all that is needed to ascertain that the administration's BTU gains from increased renewable energy production and conservation from increased "weather-stripping" will not yield even 10% of the BTU shortfall that the nation will confront. The reality, therefore, is that the country needs a vast expenditure of funds on novel and traditional sources of energy, as well as on our deteriorating energy infrastructure. Expenditures of this kind would create several million jobs of precisely the kind that are needed during the next decade. And they would leave the next generation with an improved infrastructure, in addition to lessening our extraordinary dependence on imports from rogue states.

But what do we get from the Obama team? A present value tax hike of up to $400 billion on "big oil" in one form or another, along with weather-stripping tax credits and expenditures on renewable energy alone. And who is the newly appointed spokesman for national energy policy? A highly credentialed academic who strikes virtually everyone as indecisive and ineffectual. Does even one reader of this essay know his name? [Steven Chu] Of course, his Nobel Prize supposedly substitutes for his lack of political skills. By extension, are we about to witness the "quant" financial theorist Myron Scholes appointed as Treasury Secretary after Tim Geithner steps down? After all, Scholes too, is a Nobel laureate, even if his notorious "pricing models" helped to bring down Long Term Capital Management and then the world economy a decade later. The Lord save us from "The best and the brightest!"

2. Stimulation of Innovation and Venture Capital: While increased infrastructure investment is one channel to higher productivity growth (and hence higher GDP growth), innovation is another. As someone who lived in Menlo Park, California for two decades between 1980 and 2000, the author was privileged to witness first hand the stunning comeback of the US from its "rust bowl" status of the 1970s.

The comeback was almost entirely due to a broad array of venture capital sponsored innovations, starting with the micro-processor. In a Memo he wrote for Mssrs. Clinton and Rubin in 1996, the author demonstrated that the US had an "Innovation Quotient" 17 times higher than that of our next competitor. [Finland. Think Nokia!] As a result, US productivity growth doubled from its depressed level of 1.4% in the 1970s to 3% by the late 1990s and early 2000s. No other nation came close to this achievement.

Yet now, when we need renewed innovation and enhanced productivity growth as much as we did in the 1970s, we read that the Obama Treasury Secretary Geithner has proposed to regulate the venture capital industry. Specifically, he has called for mandatory SEC registration of large firms, lest the sector become a "systemic risk" like hedge funds and proprietary trading desks. As Jack Biddle of the VC firm Novak Biddle Venture Partners has pointed out in a Wall Street Journal interview (April 9, 2009):

I cannot imagine any venture capital firm being of a size to pose 'systemic risk,' so they (the administration) either do not understand the nature of the business, or...What Washington needs to understand is that bank-style regulation could destroy the culture that created the micro-processor.

3. Education and Elitism: In contemplating the sources of productivity growth, we would all do well to recall Isaac Newton's celebrated confession that, in developing his theory of mechanics and the differential calculus, "I stood on the shoulders of giants." Politically incorrect as it is to admit, we need policies that identify and reward elite young people and entrepreneurs from a very early age, and do so regardless of where they come from. Indeed, we should be seeking young scientific talent worldwide and paying for immigrants to come to the US and study.

Instead, the stimulus package dedicates significant funds to lowest common denominator educational expenditures. In particular, virtually nothing is being proposed to end the monopoly of teachers' unions that discourages qualified teachers from attempting to teach. The consequences for productivity growth of the longstanding decline of our public schools is by now well known, and has been articulated by public figures ranging from Bill Clinton to Bill Gates and Steve Jobs.

4. Taxation that Rewards Innovation and Success: Both the president and his chief of staff Rahm Emanuel have been completely candid about their redistributionist agenda -- an agenda that has even alarmed European liberals. Were they at all concerned with innovation, productivity, and growth, the administration would not publicly espouse taxation policies that punish success and reward failure. In particular, they would not have declared war on small business, since small businesses typically generate the bulk of new jobs and innovations that determine the rate of economic growth.

To be sure, disparities in the current tax code do permit Warren Buffet to incur a much lower tax rate than his receptionist, as he quipped. Such inequities must be remedied. But the fact remains that the top decile and quartile of income earners in the US pay a larger share of government tax revenues than in any other G-7 nation. If so, why does the president assume it is "fair" to hike the tax rates on top income earners, and only on this group? From an employment standpoint, the new tax rates may well send talented young Americans to live elsewhere. Starting in 2011, a New York City wage earner will pay a marginal tax rate (federal, state, and local) of over 60% on "high" incomes of $200,000. This rate is higher than comparable rates in Germany and France where taxes paid secure decent schooling and medical care, which they do not in the US. Yet even so, France has witnessed a veritable diaspora of young talent to London, the US, and Switzerland during the past two decades.

5. Incentives for Investment in the Private Sector: Productivity growth comes not only from government-sponsored infrastructure of the kind discussed above, but also from investment by private businesses of all sizes in new capital stock. It is not clear what the new tax policy will be towards investment tax credits, but such credits have not yet been identified as important. They are important, especially at a time when the search for higher productivity and hence higher economic growth must become the nation's number one priority.

6. Less Regulation, Not More: "Re-regulation" is back in vogue. But increased regulation where it's not needed chokes off innovation and growth. While the financial sector clearly needs re-regulation, it is not clear that other sectors do. Should the new administration become growth-oriented, then it must be very careful not to choke off the all-important forces of "creative destruction."

Even in the financial sector, overkill is likely. In our own view, two general forms of regulation are needed. First, incentives must be properly aligned (e.g., banks issuing securitized products must hold a certain proportion of such products in-house.) Second, leverage must be radically curtailed, a point we have stressed for three years. As for "excess pay," the limitation of leverage and proper alignment of incentives will automatically remedy most excesses of recent years. In brief, the less regulation the better.

G.3. Workforce-Enhancing Growth Strategies

1. Strong GDP Growth: The six growth-maximizing strategies above will do more to boost workforce growth than anything else. The strong correlation of workforce growth and GDP growth is well understood at both an empirical and theoretical level. Most important, perhaps, is the need to stimulate innovation so that new industries can rise and replace old industries via the unfettered forces of creative destruction. Indeed, new industries have contributed over 75% of job growth in the US during recent decades. Numerous studies have shown how policies preventing creative destruction within most of Europe depressed private sector job creation during recent decades. Most job creation occurred in the public sector. Regrettably, none of these employment realities have been discussed by the new administration.

2. Deficit Composition: Utilization of today's huge deficits for boosting investment expenditures triggers those accelerator/multiplier effects cited above that boost employment far more than transfer payments or tax cuts do. Yet the administration's stimulus package is very infrastructure-lite, as was discussed above.

3. Deregulation of the Labor Market: Labor unions have long wanted to return to the practices of card-check balloting (or majority sign-up) without secret balloting. Yet such practices are definitionally anticompetitive, and retard employment growth. The administration initially supported card-check legislation or the so-called Employee Free Choice Act, but does not have enough votes to impose it. As to the tricky issue of immigration, the Obama team is doing a good job to date supporting rights for undocumented workers who have played such an important role in the nation's economic history, and must continue to do so in the future.

4. Managing Demographic Change within the Labor Market: There will be new and important tensions within the US labor market, given the likely influx of millions of post-65 year old boomers. It is becoming clear that the retirement planning of this generation was woeful, with up to half of boomers expecting they could afford a retirement financed by the ever-rising values of stocks and houses. Such expectations have been shattered, and many boomers will have to work until age 75 to afford the lives they expect.

In many ways, this is a good development. However, it presupposes that the requisite jobs exist. Yet they will not exist unless labor markets are deregulated, not re-regulated. In particular, minimum wages and guaranteed hours of work must go by the boards. Maximum flexibility will be needed to equate supply and demand in the labor market, thereby reducing tensions between older and younger job-seekers. Such tensions have already begun to appear in today's scramble for jobs.

A welcome dividend of elderly workers joining the workforce will be the reduction of the Social Security Trust Fund deficit. If the average retirement age de facto (not de jure) rises from 64 to 70, trillions of dollars of unfunded liabilities will evaporate as people draw upon their Social Security entitlements later, and contribute longer. The present value of the resulting fiscal savings is truly huge, making it all the more important that the US labor market become as flexible and efficient as possible. The administration has never touched upon this issue.

5. Tax Policy: Any student of public finance will recall that the best kind of tax is the tax that least distorts the efficiency of the economy. The Value Added Tax (VAT) is well known to be optimal in this regard. Conversely, taxes on labor (e.g., income taxes) distort workforce growth and thus, economic efficiency the most. But the administration is wedded to higher taxes on labor, and has never proposed a VAT.

This concludes our identification of over a dozen policies that can drive the Debt-to GDP ratio down. Please note that each of the pro-growth strategies is incentive-structure-compatible with growth, as desired and as promised up front.

H. Conclusion: When Being "Smart" Is Not Enough

This essay began with a demonstration of the all-important role of the evolution of a nation's Debt-to-GDP ratio. The direction of this evolution is a good proxy for the future success or failure of the nation. We argued that a one-time shock (like today's US recession) that drives the initial Debt ratio way up does not pose the problem most people assume. Long run recovery is possible, but only if policies are adopted that drive the growth rate of the numerator down, that of the denominator up, and thus that of the ratio down.

We then identified over a dozen policies that can achieve the goal of driving down the Debt-to-GDP ratio in the longer term. The End Game that is now being played is whether policies of this kind are adopted, or whether they are not. In our view, the Obama administration has adopted both a philosophical perspective and a set of policies that will drive the ratio up. If this is indeed the price of a "new American social architecture," then it is a price that is too high.

We also proposed that these "ratio management policies" should be viewed as a refinement, and indeed an extension of classical monetary and fiscal policy. They add a new dimension to the concept of "macroeconomic policy," and to its objectives.

Why do so few administration spokesmen or economic commentators seem to share our views? Is "politics" the problem? We do not think so, at least to the extent that growth-maximizing policies are win-win policies that any good politician should be able to sell. No, the problem is rather one of the mind-set of a generation that has never before needed to confront the problems lying ahead, and that is tone deaf to philosophical issues, as opposed to "policy wonk" issues.

Today's True Challenge -- Governance: In this vein, we proposed at the end of our February 2009 PROFILE that the root problems of today are not macroeconomic as much as they are political philosophical: How can democracy save itself from itself? How can people be made to realize that a reform of governance is what is now most needed -- more so even than a reform of Wall Street? And even in the financial sector, it is increasingly clear that regulatory lapses in Washington were more responsible than "greed" for what has happened. Messrs. Rubin, Summers, and Greenspan actively encouraged the most pernicious of the deregulatory policies that brought down the system.

By now, it is clear that we need bold new constitutional amendments that mandate (i) sterilization of excess money creation during cyclical recoveries, (ii) fiscal surpluses during recoveries to pay down past fiscal deficits, and (iii) deficits during recessions tilted towards growth-enhancing infrastructure spending, not towards goodies for special interest groups.

In this regard, economists Martin Wolf and Stephen Roach have both correctly identified financial market "credibility" as the key to future growth, inflation, and interest rates. Can today's administration end up with any credibility when it blithely ignores the very existence of the End Game we have identified, much less those policies needed to solve it correctly? Will there be any credibility if the three proposed amendments just cited are not adopted?

In his magisterial The Rise and Decline of Nations, Mancur Olson understands that these are the topics that matter -- not greed management 101. Yet barely a word is being said about these issues by the Best and the Brightest now staffing the Obama White House. Why? The explanation partly lies in a crisis of intellectual competence. Scholars trained in "macroeconomics" are as poor in discussing Olson's dilemmas of collective action as oncologists are in discussing dentistry. The fact that the macroeconomists in question are "brilliant" is irrelevant. Being smart is not enough.

The abject moral failure of the new team to identify much less to propose a solution to the End Game is extremely disturbing to the present author. Despite his initial support of President Obama, he increasingly wonders whether we have the right team in place. And he is alarmed that time to rebuild credibility is running out.

© 2009 Strategic Economic Decisions, Inc.

Footnotes:

1 We stressed that this hike in real rates does not occur in the case of normal-sized fiscal deficits caused by normal G-7 recessions. It only occurs when the deficits are exceptionally large, as they are turning out to be this time around. Accordingly, our analysis cannot be supported by the data of G-7 recessions during the past half century for the simple reason that we have rarely before experienced deficits of the magnitude confronting the US today. Nonetheless, our analysis can be supported by the experience of many emerging market economies that became overly indebted.

2 US federal debt is often stated to be $5.5T. This is because some $4.5T of debt is held by the Social Security Administration trust funds and other entities. But what matters for the purposes of our analysis is the total debt of some $10T.

3 This forecast growth of debt excludes the growth of liabilities of the balance sheet of the Federal Reserve Bank, as well as some off-balance sheet operations by the Treasury. But much of the costs of bailing out the financial system should properly be viewed as asset exchanges, and not as increases in the fiscal deficit per se. The story is highly complicated, and mistaken interpretations are commonplace.

4 In one of the grandest achievements in the history of social thought, Hurwicz demonstrated mathematically that the incentive structure of "true capitalism" alone is compatible with the societal goals of efficiency, privacy, freedom, equity, and stability. In our view, this result gave a more compelling and concrete interpretation of Aristotle's concept of "The Good Life" than any theory before or since has done.

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.