Bankrupt Banking System Bailouts & Stimulus , You Can't Borrow Your Way Out of Debt

Economics / Credit Crisis Bailouts Jun 24, 2009 - 10:28 AM GMTBy: James_Quinn

“Rather than love, than money, than fame, give me truth.” - Henry David Thoreau

“Rather than love, than money, than fame, give me truth.” - Henry David Thoreau

Time is running out. The public relations campaign being conducted by the Obama administration, Federal Reserve and nation’s largest banks is beginning to fail. The lies, half-truths, and cover-up regarding the solvency of the largest banks in the U.S. will be revealed as reality interrupts their master plan. The politicians and government bureaucrats know that 80% of the population don’t understand or care about economic issues. The plan is insidious, systematic and deceptively simple:

Part 1 of the plan was for the Federal Reserve to print billions of dollars and lend this money to the insolvent banks in return for worthless toxic assets as collateral. They have not revealed which banks received the money or the “assets” that have been hidden on the Federal Reserve balance sheet.

Part 2 of the plan was to reduce short term interest to 0% so that the insolvent banks could borrow money from the Fed for free and then lend it out at 6% or higher to consumers and businesses. Therefore, risk averse senior citizens like my mother are receiving 0.5% on their money market funds, while the horribly run insolvent banks are being propped up and enriched by the Fed. With billions in TARP funds, the FASB no longer requiring mark to market accounting, and free money from the Fed, the large banks reported fake profits in the 1st Quarter of 2009.

Part 3 of the plan was the fake stress test conducted by Tim Geithner, his Treasury Department, and the Federal Reserve. The entire stress test was a publicity stunt conducted to provide a false sense of confidence in the largest banks so they could fool investors into pouring billions of new capital into their bankrupt banks. The assumptions used in the stress test were stress free. Unemployment is already higher than the worst case scenario. The stress test time frame ended in 2010. The next wave of mortgage resets and foreclosures will hit in 2011 and 2012. William Black, former bank regulator and author of the book The Best Way to Rob a Bank Is to Own One, concluded:

“There were no real examinations. Banks continue to overstate asset quality. The bankers pressured Congress, which extorted the Financial Accounting Standards Board, which gutted the accounting rules on loss recognition. Because there were no real examinations, there were no real stress tests.”

Even the Congressionally-appointed panel overseeing the Troubled Asset Relief Program concluded: “unanswered questions about the details of the tests, make it impossible to replicate the tests to determine how robust they are or to vary the assumptions to see whether different projections might yield very different results."

Part 4 of the plan had billions in TARP funds going to the likes of GMAC, Capital One and American Express so they would lend it out to over-indebted consumers and jump start the economy. The $787 billion porkulus plan has dumped wads of dollar bills into the laps of government bureaucrats and unions throughout the country with hopes that something productive might happen. Senator Coburn of Oklahoma issued a report last week regarding stimulus spending. Millions of dollars are going toward bicycle lockers, bike paths, walking trails and skate parks. One town in North Carolina is using stimulus funds to hire an administrator whose job will be to procure more stimulus funds. You judge whether these projects will jump start our moribund economy:

- Optima Lake is in line to receive $1.15 million in federal stimulus money to construct a new guardrail for a lake that does not exist. The guardrail is needed for “public safety,” says the Army Corps of Engineers, but there is not much of the public around to protect. Because the lake has never filled with water it is all but useless to potential visitors.

- The repair of 37 rural bridges in Wisconsin that average little more than 500 vehicles apiece each day - with one carrying no more than 10 cars a day. The projects jumped over larger, urban repairs because they were "shovel ready." $840,000 to repair a bridge in Portage County, Wis., that carries 260 vehicles a day largely to a backwater saloon and a country club.

- $3.4 million Florida Department of Transportation project for an "eco-passage" - an underground wildlife road crossing for turtles and other wildlife in Lake Jackson, Fla., along U.S. 27.

- A Bureau of Land Management project to study the impact wind farms have on the sage grouse population in Oregon. The proposal calls for hiring people to tag sage grouse in areas where wind farms may be built, to help determine where turbines could be located.

- $1.5 million in stimulus money for a $5 million new wastewater treatment plant in Perkins, Okla. The stimulus money came with strings that will increase the costs. With a new total cost of $7.2 million, the city will be forced to borrow money and, as a result, utility taxes have increased by 60 percent this year.

- Grants and loans totaling $1.3 million to Solon Township in Leelanau County, Mich., to help pay for construction of a wastewater treatment plant. Local opposition killed the project. The money will now be used for a future treatment plant, for which there is no plan and questionable local support.

- Road signs costing $300 each, being placed at construction sites to alert motorists that the project is being paid for by the stimulus money. Transportation Department spokesman Jill Zuckman said each state decides whether to use stimulus money for signs, and the cost would vary in each state.

- A $3 million project to repair taxiways at Hanscom Field, Mass., which Coburn said is for corporate jets. Richard Walsh, a spokesman for the independent state agency that runs the airport, Massport, said only 18 percent of the traffic at the airport is for corporate jets. Most of the use, 70 percent cent, is for flight students, he said.

- Montana's state-run liquor warehouse, to receive $2.2 million in stimulus cash to install skylights. The project is part of the $27.7 million the state has been awarded for energy programs.

If Only the Dead Could be Stimulated

James Hagner: It shocked me and I laughed all at the same time and though how in the world could they do this.

TV Commentator: 83 year old James Hagner says he isn’t too big on surprises, but he got quite a big one when he visited his mailbox last Thursday.

James Hagner: I got a check for my mother. She has been dead 43 years, and I got a check for my mother. The $250 stimulus check in the mail.

TV Commentator: As part of President Obama’s American Recovery and Reinstatement act, the Social Security Administration somehow mailed a $250 stimulus check to his mother Rose, who passed away Memorial Day 1967.

James Hagner: I didn’t even expect to get one for myself, but to get one for my mother from 43 years ago…

Interviewer: kind of strange, right?

James Hagner: Yes sir.

TV Commentator: We contacted Social Security representatives over the phone and they told us there is a good explanation here. First of all, Social Security has mailed or is mailing out 52 million checks, and of those 8,000 to 10,000 have been sent to people who are deceased. Social Security blames the error on the strict mid-June deadline for mailing out all the checks which didn’t leave officials much time to clean up all their records. So that means there are 8 to 10 thousand James Hagners all over the country getting the same surprise in the mail box. The thing is what do you do with the check? Social Security kindly asks that you return it. As far as Hagner is concerned, he would like to frame it and hang it on a wall.

James Hagner: I just want to keep it as a souvenir. That’s all. I will never cash it.

This is just another quaint funny story about our incompetent government working to improve our lives. They sent $2.5 million to dead people. Social Security’s records haven’t been “cleaned up” for people who died before we put a man on the moon? Picture the scene when a government bureaucrat explains to your family that taking out your liver instead of your appendix was due to some computer system glitch. Once the government puts its efficiency expertise gained from running the IRS, Social Security, the Postal Service, and Amtrak to work on your healthcare, the fun will really begin. It will make dealing with Verizon’s “customer service” seem like a treat.

This is only the tip of the iceberg. A report by Deloitte Touche last week said that about $500 billion of the $787 billion in stimulus will be spent through the "traditional (government) procurement network." Using past performance as a gauge, Deloitte Touche predicted as much as $50 billion will end up being fraudulently spent — or 10% of the total. The entire United States government outlays in 1952 totaled less than $50 billion. Now, $50 billion is an acceptable fraud write-off.

Reality Bites

“Society in every state is a blessing, but government, even in its best stage, is but a necessary evil; in its worst state an intolerable one." - Thomas Paine

I’ve laid out the master plan of our “leaders”. The only problem is the are about to get in the way of a good yarn. Below is a chart that tells a disturbing truth for the largest banks in the U.S. The government supported banks have only written off $1.3 trillion thus far. Based on the realistic estimates from Nouriel Roubini and T2 Partners, there is only $2.3 trillion more write-offs to go for our glorious banking behemoths. The 19 stress tested banks were able to convince foolish investors to drop another $75 billion of capital onto their balance sheets after the stress test fraud publicity campaign. This $75 billion only comes up 30 times short of covering $2.3 trillion in future losses. As Mr. Roubini recently reported we need a little of Joseph Schumpter’s creative destruction.

“Once again, the question will be how the near-insolvent banks can be kept afloat, to avoid systemic risk. But the question we really should be asking is: why keep insolvent banks afloat? We believe there is no convincing answer; we should instead find ways to manage the systemic risk of bank failures. Why did creditors not prevent the banks taking excessive risks before the crisis hit? For the very same reason creditors are getting a free pass now: they expected to be bailed out. For capitalism to move forward, it is time for a little orderly creative destruction.”

The Obama administration has chosen to go with a plan centered around creative accounting, creative financing, and a creative public relations campaign versus the system correcting creative destruction. This is a plan of imminent destruction of our economic system.

![[mm19.png]](/images/2009/June/debt-24_image003.jpg)

The country has lost jobs in every month since December 2007. The number of unemployed has doubled over this time to approaching 15 million people. While 7 million people have lost their jobs in the private sector, government has increased their hiring by 600,000, from 21 million to 21.6 million. We can all be thankful there are 600,000 more bureaucrats increasing the efficiency of our government. Despite happy talk by CNBC pundits, investment managers, and government officials another 2 million people will lose their jobs this year. The unemployment rate will approach 11% by the end of 2009. Last week the “business correspondents” at CNBC proclaimed that the reduction in continuing unemployment claims was another green shoot. If they had just scratched the surface like Barry Ritholtz, they would have found the truth.

“The ‘exhaustion rate’ for jobless benefits reveals that people are not leaving the pool of continuing unemployment claims because they are getting new jobs; Rather, they are leaving because they have exhausted their benefits. They are now unemployed AND broke.”

![[WeeklyClaimsJune18.jpg]](/images/2009/June/debt-24_image002.jpg)

The continuing deterioration in employment, the tsunami of Alt-A mortgage resets coming in 2010 and 2011, home prices declining another 10% to 15%, doubling in oil prices since January, billions in credit card write-offs in the pipeline and the progressing collapse of the commercial real estate market will throw cold water on the Obama master plan to save the banks and the economy. The sooner this occurs, the better. Their solution of trying to borrow and spend our way out of debt was flawed and asinine from the start. If Americans are ready to accept the inevitable pain of deleveraging today, we can take back the country from the banking crime syndicate and the politicians that are in their back pocket.

Money is Power

“Money is power, and in that government which pays all the public officers of the states will all political power be substantially concentrated.”Andrew Jackson

The chart below shows that after 182 years as a country we had accumulated a National Debt of $389 billion. Then in 1971, President Nixon closed the gold window. The Federal Reserve was free to print dollars with no constraints. And print they did. Politicians used the printed dollars to spend on any costly initiative that would help them get re-elected. From 1970 to 1980, the National Debt went up by 2.4 times. From 1980 until 1990, the National Debt went up by 3.5 times. From 1990 until 2000, the National Debt went up by 1.8 times. From 2000 until today, the National Debt has gone up 2.0 times. Based on the spending implemented and proposed over the next few years, it will go up 1.5 times during Obama’s 1st term. It will have gone from 33.3% of GDP in 1980 to 100% of GDP by the end of Obama’s 1st term. At that point we will have entered the Argentina – Weimer Republic zone.

| End of Fiscal Year |

US Gross Debt USD billions |

US Gross Debt as % of GDP |

| 1910 | 2.6 | |

| 1920 | 25.9 | |

| 1930 | 16.2 | |

| 1940 | 43.0 | 52.4 |

| 1950 | 257.4 | 94.1 |

| 1960 | 290.2 | 56.1 |

| 1970 | 389.2 | 37.6 |

| 1980 | 930.2 | 33.3 |

| 1990 | 3,233 | 55.9 |

| 2000 | 5,674 | 58 |

| 2005 | 7,933 | 64.6 |

| 2007 | 9,008 | 65.5 |

| 2008 | 10,699 | 74.6 |

| 3rd Quarter of 2009 | 11,383 | 82.5 |

“Debt is the fatal disease of republics, the first thing and the mightiest to undermine governments and corrupt the people.” Wendell Phillips

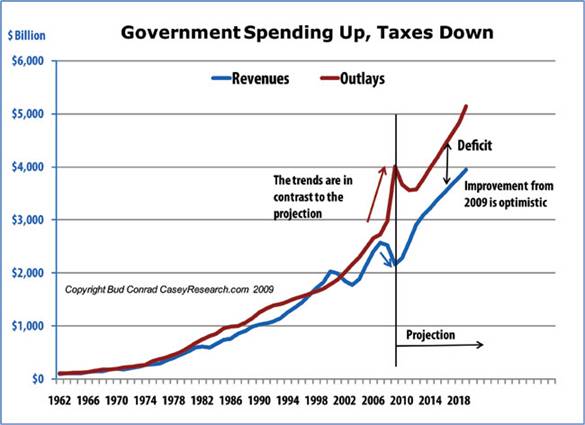

When looking at a graph of government revenues and outlays since 1962 a few things stand out. The government was able to keep revenues in line with outlays until about 1982. Even while fighting the Vietnam War, the budget deficit was kept relatively under control. Since then we have had cooperation between the Republican and Democratic parties for the majority of the last 27 years. The Democrats allowed the Republicans to reduce taxes and increase military spending, therefore decreasing revenues. The Republicans allowed the Democrats to increase spending on social welfare programs. The only time revenues exceeded expenditures was when gridlock reigned during the Clinton administration. New spending slowed down and capital gains taxes from the Dot.com era provided a one-time boost to revenues. The CBO projects a $1.8 trillion budget deficit in 2009. This equals our entire National Debt in 1985.

“Blessed are the young for they shall inherit the national debt.” - Herbert Hoover

As can be expected when politicians make projections, the likelihood of them being within $10 trillion is nil. It is fascinating that individual income tax revenue will jump by 32% and corporate income taxes by 30% in 2011 from 2009 levels. The inconvenient fact that you need a job to pay taxes and corporations need to have profits to pay taxes is brushed aside. I presume they also are counting on a windfall when the Bush tax cuts expire. The largest tax increase in history will surely lead to 4.7% GDP growth in 2011 and 6.0% GDP growth in 2012. Maybe the Cap & Trade tax and the additional $1 or $2 trillion for government takeover of the healthcare system will lead to a boom in our economy. These projections are at best pure fantasy and at worst a bold faced lie. The scary part is that even with the pie in the sky numbers, they still project the National Debt to grow by $4 trillion between 2009 and 2014. The likely number will be $8 trillion.

“In general, the art of government consists of taking as much money as possible from one class of citizens to give to another.” - Voltaire

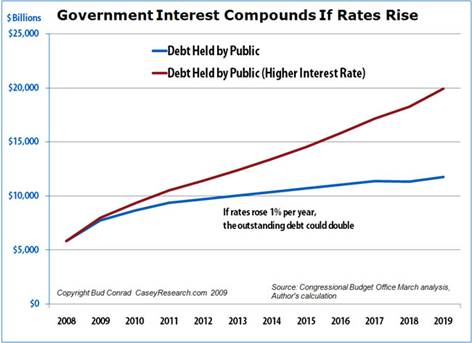

The single biggest risk to the Obama rosy scenarios is interest rates. The CBO assumes interest rates will stay below 5% through 2019. This is a ridiculous assumption. The Federal Reserve is printing trillions of dollars, we are fighting two wars, we have just committed $787 billion in pork spending, we’ve committed billions to our banks and auto companies, and now we are about to commit at least a trillion dollars to national healthcare. The countries lending us this money will absolutely require higher interest rates to account for their risk. If interest rates don’t approach double digits in the next five years, all economic reason will be out the window. As Bud Conrad from Casey Research points out, just a 1% increase per year over the assumption in the budget will double the debt. The government has pushed this country to the limit of debt induced growth and we are no longer in control.

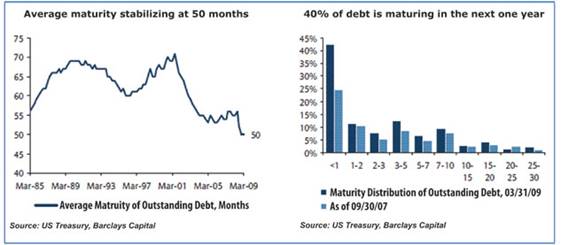

Any good corporate Treasurer worth their salt would have been taking advantage of the lowest long term Treasury rates in decades by locking in their debt for 20 to 30 years. Not our brilliant chieftains of finance at the Treasury Department. 40% of all U.S. debt rolls over in less than one year. Less than 5% of all U.S. debt is locked in for 20 years or more. The average maturity is 50 months, a three decade low. The extremely short duration of this debt leaves the country susceptible to a spike in interest rates. A spike in interest rates could drive annual interest expense from $250 billion to $500 billion virtually overnight. The worst part is that a large portion of this interest expense is flowing out of the country to foreigners.

Foreigner Invasion

Warren Buffet described the problem the U.S. was getting itself into a few years ago:

“In effect, our country has been behaving like an extraordinarily rich family that possesses an immense farm. In order to consume 4 percent more than we produce—that’s the trade deficit—we have, day by day, been both selling pieces of the farm and increasing the mortgage on what we still own.”

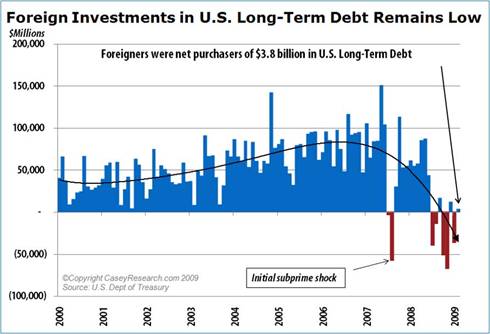

Warren was right. We’ve now sold off more than half the farm and the mortgage owed to foreigners threatens to force us into foreclosure. Foreigners currently hold 30% of all U.S. debt and have been buyers of more than 50% of new issuance in recent years. The U.S. will need to issue $2 trillion of new debt in the next year. Who is going to buy this debt? What pension manager or foreign treasury official would buy long term U.S. Treasury bonds paying 4.3%. The chart below shows that foreigners were purchasing hundreds of billions in U.S. debt between 2004 and 2007. Even a Treasury bureaucrat can look at the chart and realize they have a problem. Foreigners are now selling U.S. long term debt. They will not be the buyers of the $2 trillion coming to the market unless rates rise to 6% or higher. The Fed will not allow that to happen, so the buyer of the $2 trillion will be the Fed. They will monetize the debt and push the country closer to default. The coming crash in the dollar will ruin Ben Bernanke’s academic textbook plan.

Starve the Beast

“The budget should be balanced, the treasury should be refilled, the public debt should be reduced and the arrogance of public officials should be controlled.” - Ross Perot

As a country we face an extremely difficult challenge. The deceptive scheme instituted by the government bureaucrats, dishonest bankers, corrupt politicians and the Federal Reserve has convinced millions to believe their deceit. The foundations of their scheme are built upon a blizzard of lies. The only way to confront lies is with the truth. They are counting on some givens. Doug Casey describes a large portion of the U.S. population as Boobus Americanus. These are the functionally illiterate who have been pushed through our government run public school system. They don’t know the name of our Vice President. They can’t add, subtract or write a sentence. They will believe anything they are told by Obama. There are also the ultra-liberals who will believe anything their Messiah utters. Lastly, the large banks, Treasury, and Federal Reserve will do anything to maintain their wealth and power. This coalition of greed, sloth, and avarice presents a daunting challenge.

The cards have been stacked against Americans who don’t borrow too much, save for a rainy day, drive 10 year old cars, and didn’t spend all the equity in their houses. But, all is not lost. The large portion of middle class Americans who have lived their lives prudently have more control than they might think. I recently refinanced my mortgage. I’ve had a mortgage with Citadel Federal Credit Union since 1995 and have refinanced to a lower rate three times. Even though I have been banking with them for 25 years, they required an appraisal and shockingly, proof of income before allowing me to refinance. What a concept. While speaking with the mortgage specialist at the Credit Union, I asked how the financial crisis had impacted them. She said their insurance had gone up dramatically to pay for a few big credit unions that had collapsed due to bad lending practices. I asked how many mortgage loans they had to write off. The answer was NONE. Amazingly, if you get a legitimate appraisal, proof of income, and proof of assets, and keep the loans on your books, you can make loans that will be repaid. It is called prudent banking. My question is why are we saving the worst run banks in the history of the world when we have thousands of prudent banks willing and able to step up to the plate?

“Disobedience is the true foundation of liberty. The obedient must be slaves.” - Henry David Thoreau

My plan to reinstitute prudence and common sense into our economic system has two parts. The first part is to heap ridicule and scorn upon Congress, the Federal Reserve, the Treasury, and the banking cartel trying to maintain their stranglehold upon the American people. This part is quite easy. Since their entire plan is based upon lies, just telling the truth will weaken the foundations of their plan. The results of their past policy decisions, lack of transparency, proof of insider dealings, covering up of secret deals, and examples of incompetence and fraud makes it easy to undermine the solutions put forth by these people.

Part two of my plan is more difficult, but with a concerted effort by millions of sensible Americans, we can bring the country back from the brink of disaster. The plan is to put the banks responsible for the collapse of our financial system out of business. The Federal Reserve and the Obama administration do not want creative destruction to revive our economy, so we will have to force creative destruction upon them.

The 20 biggest banks in the country control $3.5 trillion of the $7.1 trillion deposits in the country. There are 8,400 banks in the country and 20 banks control 50% of the deposits. The list below reads like a who’s who list of the worst run banks in history that took the greatest risks and lost the most money.

| State Headquartered |

No. of Offices |

Total Deposits June 30, 2008 |

|

|---|---|---|---|

| BANK OF AMERICA CORPORATION | North Carolina | 6,146 | 701,485,101 |

| JPMORGAN CHASE & CO. | New York | 3,195 | 497,215,362 |

| WACHOVIA CORPORATION | North Carolina | 3,363 | 422,002,374 |

| WELLS FARGO & COMPANY | California | 3,378 | 293,406,008 |

| CITIGROUP INC. | New York | 1,079 | 271,290,597 |

| U.S. BANCORP | Minnesota | 2,597 | 127,849,616 |

| SUNTRUST BANKS, INC. | Georgia | 1,759 | 115,603,668 |

| NATIONAL CITY CORPORATION | Ohio | 1,568 | 97,764,933 |

| ROYAL BANK OF SCOTLAND GROUP PLC, THE | Foreign * | 1,654 | 95,255,161 |

| TORONTO-DOMINION BANK, THE | Foreign * | 1,090 | 89,756,985 |

| CAPITAL ONE FINANCIAL CORPORATION | Virginia | 740 | 88,916,281 |

| REGIONS FINANCIAL CORPORATION | Alabama | 1,924 | 86,225,760 |

| BB&T CORPORATION | North Carolina | 1,492 | 85,930,565 |

| HSBC HOLDINGS PLC | Foreign * | 477 | 83,045,865 |

| PNC FINANCIAL SERVICES GROUP, INC., THE | Pennsylvania | 1,200 | 82,424,564 |

| FIFTH THIRD BANCORP | Ohio | 1,356 | 74,656,971 |

| KEYCORP | Ohio | 997 | 61,023,875 |

| BANK OF NEW YORK MELLON CORPORATION, THE | New York | 49 | 55,028,475 |

| BANCO SANTANDER, S.A. | Foreign * | 806 | 53,824,517 |

| BNP PARIBAS | Foreign * | 739 | 43,887,185 |

The total credit card debt outstanding in the U.S. at the end of 2008 was $960 billion. The top 15 credit card issuers hold $793 billion of this credit card debt, or 83% of all the debt. They also hold a major portion of auto loans, home equity loans and personal loans. Do any of these banks ring a bell?

Top 15 issuers of general purpose credit cards for 2008 based on outstandings

1. Chase - $183.32 billion

2. Bank of America - $166.32 billion

3. Citicorp - $106.74 billion

4. American Express - $88.02 billion

5. Capital One - $60.08 billion

6. Discover - $49.69 billion

7. Wells Fargo - $36.36 billion

8. HSBC - $29.97 billion

9. US Bank - $18.53 billion

10. USAA - $17.48 billion

11. Barclays - $11 billion

12. Target - $8.65 billion

13. GE Money - $7.51 billion

14. Advanta - $5.02 billion

15. First National - $4.93 billion

(Source: Nilson Report, March 2009)

There are currently $15 trillion of mortgage loans outstanding in the U.S. You may be surprised to learn that the biggest banks in the U.S. hold the majority of the mortgages in the country. These banks issued the subprime and Alt-A toxic mortgages that brought the financial system to the brink of collapse. There is no doubt after examining these figures that the mega-banks control the country’s financial system. Ben Bernanke, Hank Paulson, and Tim Geithner have decided that these banks need to be saved at the expense of senior citizens and the American taxpayer.

Top 10 originators of mortgage loans in 2008

1.Wells Fargo

2.Bank of America

3.JPMorgan Chase

4.Citigroup Inc.

5.SunTrust Bank Inc.

6.U.S. Bank Home Mortgage

7.Residential Capital LLC

8.MetLife

9.Flagstar Bank

10.PHH Mortgage

Fiscal Sanity Movement

“How does it become a man to behave towards the American government today? I answer, that he cannot without disgrace be associated with it.” - Henry David Thoreau

The largest banks in the United States have balance sheets populated by trillions in toxic worthless assets. The lifeblood of any bank is deposits. If a bank is denied its deposits, it will collapse. There are 8,000 other banks and 8,000 credit unions in the country. Thousands of these institutions never made a bad loan. If you have money on deposit with one of these mega-banks withdraw the money and deposit it into a small local bank or credit union. You will have the same FDIC insurance and won’t sacrifice any income, since these mega-banks are paying less than 0.5% on your deposits, while charging you 8% for car loans and 20% on credit card balances.

These banks continue to write-off billions in bad credit card and mortgage debt, quarter after quarter. These banks make billions in late fees and interest income by charging 20% to people who pay their debts over time. If the good credits take their business elsewhere, the mega-banks will be left with only bad credits. Most people have 5 to 10 credit cards. Stop using your mega-bank credit card and use a credit card issued by a local bank or credit union. With mortgage rates near generational lows many people have an opportunity to refinance. If this opportunity arises, choose a local bank or credit union. If you decide to buy a car, don’t buy a General Motors or Chrysler vehicle. The government controls these entities. Don’t finance your car through GMAC. By denying the government beast its revenue stream, it will slowly die.

The average individual tax refund for 2008 was $2,700. This was effectively a $200 billion interest free loan to the U.S. government. If every working American walked into their place of employment on Monday morning and increased their W-4 exemptions by 2, we would deny the politicians in Washington of billions for a year. This is a legal way of starving the beast. The corrupt political machinery in Washington DC is dependent upon Americans to spend money. Our spending accounts for 70% of the U.S. economy. Surprisingly, American citizens have more control over the situation than we know. The mega-banks and our government are rotting from the inside like a diseased Oak tree. A gale force wind provided by the prudent Americans can topple the diseased tree.

“If you would convince a man that he does wrong, do right. Men will believe what they see.” - Henry David Thoreau

The current fiscal course of the country is unsustainable. We can choose to let the country drift toward a corporate fascist run government which will collapse under the weight of debt, corruption and mismanagement or we can make a stand today with our own money. If enough Americans choose to put the horribly run mega-banks out of business it can be done. There would be absolutely nothing that Obama or Bernanke could do stop it from happening. It is time to do the right thing. Do you know what’s worth fighting for?

“All endeavor calls for the ability to tramp the last mile, shape the last plan, endure the last hours toil. The fight to the finish spirit is the one... characteristic we must posses if we are to face the future as finishers.” -Henry David Thoreau

To join the discussion of how to take back our country from the banking cartel and government central planners, go to www.TheBurningPlatform.com.

By James Quinn

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer, and are not sponsored or endorsed by his employer.

© 2009 Copyright James Quinn - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

James Quinn Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.