U.S. Dollar Crash Count Down Madness

Currencies / US Dollar Aug 31, 2009 - 08:41 AM GMTBy: Mike_Shedlock

It never ceases to amaze me what hype people will believe. The latest is a series of posts by Jim Sinclair who on August 14, started a countdown to dollar oblivion.

It never ceases to amaze me what hype people will believe. The latest is a series of posts by Jim Sinclair who on August 14, started a countdown to dollar oblivion.

Aug 14 2009: The Motivation Behind The Countdown

85 days to go!

The primary reason for this “out on the limb statement” is that the recent China/US financial Summit meeting in Washington which was requested by China, was not significantly pre-planned.

As I understand it there are two things wanted and one thing disapproved of.

The US financial leadership wants, but more so needs, Chinese buying of US Treasury offerings to remain at these levels but more so to increase to offset the wholly unavoidable increase in offering of US Federal Debt.

The Chinese wish to see the USA support the creation of a Super Sovereign Currency as an offset to dependence on the dollar for international settlements and national reserves.

The Chinese rightly feel that the greatest risk to their present dollar position’s valuation is quantitative easing. or simply put, the monetization of one’s own debt by the electronic creation of money for funding yourself.

I am informed that Chinese interests want to see both in 2009.

Tools of timing, some I have not shared with you, indicate a major potential turning point that could easily see a break below .7600 or .7200 coming in the final quarter of this year.

Add this all together and you get a November bull’s eye for a loss of confidence in the US dollar internally as well as externally. That will end the misguided belief that MOPE, via its tool SPIN, defeats economic law.An 85 day countdown to a break on the US dollar below .76 from .78 hardly seems worthy of a countdown.

And it would be nice if Sinclair told us a bit more than "I am informed that Chinese interests want to see both in 2009."

Informed by who? A top ranking official? Minnie Mouse? Uncle Joe? At least give us a hint.

OK the US and China met in an unplanned meeting. This is grounds for a "November bull’s eye" collapse on the dollar? All the way to a shocking .76?

If you are going to hype about dollar implosions, please hype with dignity. Give us our hype's worth.

Aug 19 2009: The Countdown To The Implosion Of The Dollar

My Dear Friends,

You can take your waves, percentages, algorithms, quants and quarks and throw them directly into the basket. The time for lines and squiggles are behind us. The common shares of the US dollar are and have been in a long term downtrend. That downtrend is 81 days from implosion. The selling of the US dollar and US dollar instruments is increasing in international markets, making it ever more difficult to manipulate the popular US dollar index, the USDX.

COT has cooked its own goose.

China holds in its hands the future of the category, “Foreign Purchasers of US bonds.”

China wishes the annihilation of the Fed policy of “Quantitative Easing.”

The Fed wishes to accommodate China.

The US Treasury is absolutely opposed to any such consideration as it would cement the present Administration into a one term wonder.

The US Treasury must win this battle because the boss of this opposition has the power to appoint the new Chairman of the Fed, either Summers or Geithner.

China as spokesman for the BRICs has publicly stated their desire for the institutions of a Super Sovereign Currency. This is not an intended as an immediate substitute for the dollar as a reserve currency but rather an alternative in new commitments.

It is my understanding that the BRIC countries, not China alone, have given the US until early November to deliver.

As a result of the above I see 81 days left for the US dollar.

The gold price has but one criteria and that is the US dollar. Armstrong and Alf are correct on the levels awaiting the gold price.

I know $1224 and $1650 are certain.Once again inquiring minds must ask the obvious "understanding from who?"

The odds that the BRIC countries (Brazil, Russia, India, China) got together and gave the US an ultimatum on anything for November are none and none.

By the way, can I have a timeframe on that $1650 please? Is that also November?

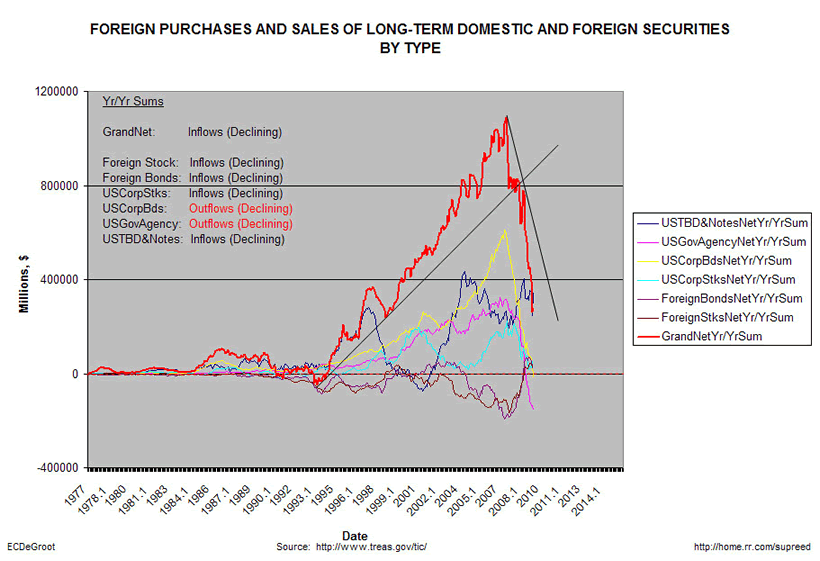

Foreign Purchases and Sales of Long-Term Domestic and Foreign Securities by Type

Sinclair posted the following chart with this comment:

"I Find this simple chart so ominous I had to send it. Decelerating year-over-year inflows and outflows across the board. Stick your head in the sand if you like, but string this trend out a little longer and you’re going to have flight from the dollar."

Basic Math

That chart may look ominous but in fact it is returning to normalcy.

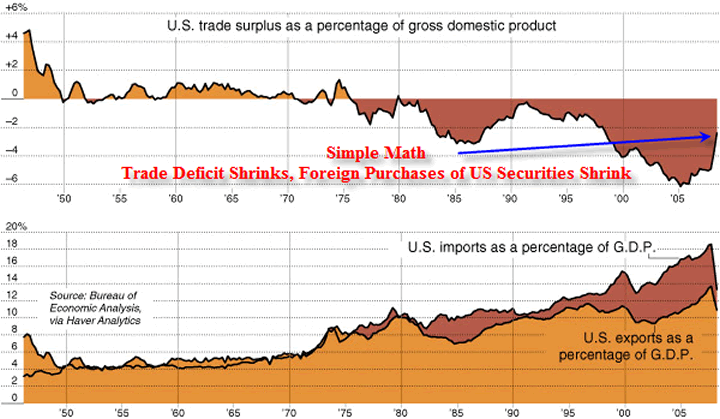

The amount of US securities foreign countries buy is directly related to the trade deficit as shown in the following chart.

US Trade Surplus vs. GDP

The above chart from New York Times, A Shrinking Trade Deficit, at Least for Now, May 1, 2009.

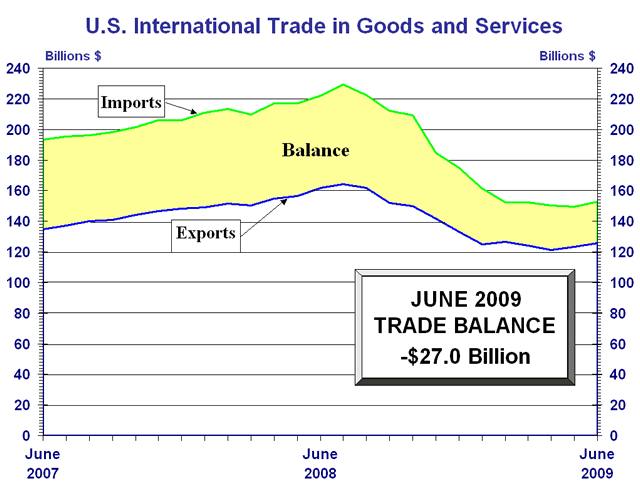

The trade balance has shrunk again and is now sitting at -27 billion as the following chart of U.S. International Trade in Goods and Services shows.

A year or so ago the US trade deficit was a whopping $77 billion. It has since shrunk to $27 billion. The chart shows exports have shrunk, but imports shrunk faster as the US consumer threw in the towel.

If the price of oil drops again, as I expect it will, the trade deficit is likely to shrink more, which would be US$ friendly.

Households Start to Rival the Chinese in Treasury Market

Inquiring minds are reading the Wall Street Journal Article Households Start to Rival the Chinese in Treasury Market.

China is center stage when it comes to fears that buyers will one day spurn U.S. Treasurys. The bond market has been the source of much political theater between the U.S. and China in recent months, with Chinese officials passing up few chances to lecture the U.S. on its profligacy.

But that has obscured an important change: The market for Treasury bonds is now more reliant on U.S. buyers -- including the Federal Reserve after its recent buying spree -- than the Chinese.

China held $801.5 billion in Treasury debt at the end of May. The Fed at that time held about $598 billion, although that has now risen to $704 billion. The latest figures for U.S. households, from the first quarter, showed holdings of $643.9 billion -- more than double the $266.6 billion in the fourth quarter of 2008.

The rising budget deficit, which has led to record issuance in recent months, doesn't necessarily mean the government is becoming more indebted to foreigners. While the U.S. government is borrowing furiously, the current account deficit has actually halved from an annualized $829 billion in mid-2005 to an annualized $409.5 billion in the first quarter of 2009. That shows the U.S. is now less dependent on external financing, because it is saving more domestically. The U.S. government may be in hock, but it is increasingly to its own citizens.US doesn’t need foreigners to finance the US fiscal deficit

For those interested in China, I have a recommendation: The best financial blog on China, bar none, is Michael Pettis' China Financial Markets.

It has been banned in China. So has my blog.

Pettis posts infrequently but his latest happens to be on this subject. Please consider The USG doesn’t need foreigners to finance the US fiscal deficit? Who knew?

In referring to the Wall Street Journal article above Pettis says...

This shouldn’t be a surprise. The reason for the growing US fiscal deficit is to slow the economic impact of a rise in US household and corporate savings. This means that the period in which very high Asian savings were matched by very low US household savings is changing to one in which the pressures to save in Asia remain while US households are increasing their savings (or reducing their borrowing, which amounts to almost the same thing). The pool from which the US Treasury can borrow is increasing, not decreasing.

In addition, as the US current account deficit drops, foreign net purchases of dollar assets must also drop. The rising US fiscal deficit will increasingly be financed by Americans and less and less by foreigners, and the much-decried impact on US interest rates of the massive US borrowing turns out to be very small.

Although there are plenty of good reasons for China to worry about the value of its dollar holdings, and I hope many people, not just the Chinese, are looking warily at growing US fiscal deficits and making disapproving noises, the fact is that there is little China can do about its dollar holdings without either causing a damaging rise in trade tensions with Europe (or any other country whose currency is an alternative to the dollar) or causing a collapse in its export industry. As long as China’s trade surplus directly or indirectly is connected to the US trade deficit, China will have to recycle the surplus into the dollar pool that ultimately funds the US fiscal deficit, and it is in the best interest of the US that the US trade deficit decline smoothly, which means that it is also in the best interest of the US that foreigners, including the Chinese, buy fewer US dollar assets.

What is confusing is the conflict between China’s natural position and its stated position. Rather than demand reassurance that the US will control its fiscal spending, China should be secretly hoping that the US fiscal deficit will mushroom. It is after all largely the size of the US fiscal deficit that will determine the speed with which US imports and the US trade deficit contract, and it is in China’s best interest that these contract very slowly.Pent Up Demand For Treasuries

In regards to the savings rate and US Treasuries, I have been saying the same things as Pettis for quite some time.

Flashback January 20, 2008: Time To Short Treasuries?

Kass: Central banks are diversifying away from U.S. government bonds. With the creation and proliferation of sovereign wealth funds, a growing portion of central bank reserves are being invested in non-bond assets. So, over time, central banks (especially of an Asian kind) could be lowering their U.S. bond purchases.

Mish: China is diversifying away from U.S. government bonds right now. It did not stop treasuries from rallying. Furthermore, the pent up demand for treasuries in the US is enormous. They are despised by nearly everyone here. This internal pent up demand can easily pick up any slack from reduced purchases by foreigners. 2.5% yields may looks measly, but not vs. 15% declines in the stock market. 30%? 50%? Most are severely underestimating the potential for enormous stock market declines here.

Virtually no one, including Bernanke thinks deflation can happen in the US. My position is that Things That "Can't" Happen are about to. The result will be Deflation American Style.Predictably Wrong

Maybe something happens in November, maybe not, but this dollar implosion countdown based on unnamed sources regarding impossible to believe demands and a trade chart interpreted assbackwards is more than just a bit silly. Yet, every day someone asks me about it, thus this reply.

The thing about these kind of predictions is how predictably wrong they have all been.

Based on interpretations of the Commitment of Traders Reports (COT) we have see a couple countdowns to running out of gold and or silver on COMEX by various people. Those never happened. We have seen "gold to the moon" hyperinflation calls based on backwardation. Those never happened, either.

There is also a bunch of hype going around right now about bank holidays and a devaluation of the dollar vs. all major currencies coming up this Autumn. The across the board dollar devaluation idea is potty because the US dollar floats. There is nothing to devalue it to. And even if there was, Europe and Japan do not want stronger currencies and would not go along. For that matter the US would not want to do it either fearing a market crash. Yet, the theories persist.

If something does happen in November, it will not be because some blogger knows something. It will be happenstance.

But for those counting, it's about 70 days. I can hardly wait.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2009 Mike Shedlock, All Rights Reserved

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.