The Fed's Role in the Bear Stearns Meltdown

Housing-Market / Subprime Mortgage Risks Jul 02, 2007 - 01:25 AM GMTBy: Mike_Whitney

The Bank for International Settlements issued a warning this week that the Federal Reserve's monetary policies have created an enormous equity bubble which could lead to another “Great Depression”. The UK Telegraph says that, “ The BIS--the ultimate bank of central bankers--pointed to a confluence a worrying signs, citing mass issuance of new-fangled credit instruments, soaring levels of household debt, extreme appetite for risk shown by investors, and entrenched imbalances in the world currency system.

The IMF and the UN have issued similar warnings, but they've all been shrugged off by the Bush administration. Neither Bush nor the Federal Reserve is interested in “course correction”. They plan to stick with the same harebrained policies until the end.

The “easy credit” which created the subprime crisis in mortgage lending has now spread to the hedge fund industry. The troubles at Bear Stearns prove that Secretary of the Treasury Henry Paulson's assurance that the problem is “contained” is pure baloney. The contagion is swiftly moving through the entire system taking down home owners, mortgage lenders, banks, rating agencies, and hedge funds. We are just at the beginning of a system-wide breakdown.

The problem originated at the Federal Reserve when Fed-chief Alan Greenspan lowered the Feds Fund Rate to 1% in June 2003 and kept rates perilously low for more than 2 years. Trillions of dollars flowed into the economy through low interest loans creating a massive equity bubble in real estate which drove up housing prices and triggered a speculative frenzy.

The Feds' “easy money” policy has disrupted the “debt-to-GDP” balance which maintains the integrity of the currency. By expanding circulation debt via low interest rates; Greenspan put the country on the path to hyperinflation and, very likely, the collapse of the monetary system.

The problems at Bear Stearns are the logical upshot of Greenspan's policies. The over-leveraged hedge funds are a good example of what happens during a “credit boom”. Liquidity flows into the markets and raises the nominal value of all asset classes but, at the same time, GDP continues to shrink. That's because the wages of working class people have stagnated and not kept pace with productivity. When workers have less discretionary income, consumer spending—which accounts for 70% of GDP—begins to decline. That's why this quarters earnings reports have fallen short of expectations. The American consumer is "tapped out".

The current rise in stock prices does not indicate a healthy economy. It simply proves that the market is awash in cheap credit resulting from the Fed's increases in the money supply. Consumer spending is a better indicator of the real state of the economy than stocks. When consumer spending drops off; it is a sign of overcapacity, which is deflationary. That means that growth will continue to shrivel because maxed-out workers can no longer purchase the things they are making.

The underlying problem is not simply the Fed's reckless increases to the money supply, but the growing “wealth gap” which is undermining solid economic growth. If wages don't keep pace with productivity; the middle class loses its ability to buy consumer items and the economy slows.

The reason that hasn't happened yet in the US is because of the extraordinary opportunities to expand personal debt. The Fed's low interest rates have created a culture of borrowing which has convinced many people that debt equals wealth. It's not; and the collapse in the housing market will prove how lethal that theory really is.

To large extent, the housing bubble has concealed the systematic destruction of America's industrial and manufacturing base. Low interest rates have lulled the public to sleep while millions of high-paying jobs have been outsourced. The rise in housing prices has created the illusion of prosperity but, in truth, we are only selling houses to each other and are not making anything that the rest of the world wants. The $11 trillion dollars that was pumped into the real estate market is probably the greatest waste of capital investment in the nations' history. It hasn't produced a single asset that will add to our collective wealth or industrial competitiveness. It's been a total bust.

The Federal Reserve produces all the facts and figures related to the housing industry. They knew that trillions of dollars were being diverted into a speculative bubble, but they did nothing to stop it. Instead, they kept interest rates low and endorsed the lax lending standards which paved the way for millions of defaults. Now the effects of their "cheap money" policies have spread to the hedge fund industry where hundreds of billions of dollars in pensions and savings are in jeopardy.

Alan Greenspan played a major role in the housing boondoggle. On February 26, 2004, he said, “American consumers might benefit if lenders provide greater mortgage product alternatives to the traditional fixed rate mortgage. To the degree that households are driven by fears of payment shocks but willing to manage their own interest-rate risks, the traditional fixed-rate mortgage may be an expensive method of financing a home.”

Greenspan tacitly approved the whacky financing which produced all manner of untested loans—including ARMs, piggyback loans, “no doc” loans, “interest only” loans etc. These loans are a break from traditional financing and have contributed to the increase in bankruptcies.

Millions of people who were hoodwinked into buying homes with “interest-only”, “no down” loans will now either lose their homes or be shackled to an asset of decreasing value for the next 30 years. They've been tricked into a life of indentured servitude.

A recent article in the Wall Street Journal revealed the extent of Greenspan's involvement in the housing fiasco. Here's an excerpt from the article:

“Edward Gramlich, who was Fed governor from 1997 to 2005, said he proposed to Mr. Greenspan in or around 2000, when predatory lending was a growing concern, that the Fed use its discretionary authority to send examiners into the offices of consumer-finance lenders that were units of Fed-regulated bank holding companies.

"I would have liked the Fed to be a leader" in cracking down on predatory lending, Mr. Gramlich, now a scholar at the Urban Institute, said in an interview this past week. Knowing it would be controversial with Mr. Greenspan, whose deregulatory philosophy is well known, Mr. Gramlich broached it to him personally rather than take it to the full board.

"He was opposed to it, so I didn't really pursue it," says Mr.

Still, Mr. Greenspan's views did color the regulatory environment, facilitating growing concentration in banking and a hands-off approach to derivatives and hedge funds. That approach, broadly shared by both the Clinton and Bush administrations, is coming under increased scrutiny”. (Wall Street Journal)

So, Greenspan had the chance to “crack down on predatory lending” and he refused. Now millions of low income people are saddled with payments they have no reasonable prospect of paying off. How much of the present carnage could have been avoided if he had Greenspan done the right thing?

The “Not So Great” Depression

An article appeared this week in the UK Telegraph by Ambrose Evans-Pritchard which supports the theory that Greenspan's “ loose monetary policy” fueled a huge credit bubble, which is pushing the global economy towards a “1930s-style slump.”

The article quotes from a statement made by The Bank for International Settlements:

"Virtually nobody foresaw the Great Depression of the 1930s, or the crises which affected Japan and Southeast Asia in the early and late 1990s. In fact, each downturn was preceded by a period of non-inflationary growth exuberant enough to lead many commentators to suggest that a 'new era' had arrived".

But today we face “worrying signs” of another economic meltdown.

The BIS said that they were “starting to doubt the wisdom of letting asset bubbles build up on the assumption that they could safely be ‘cleaned up' afterwards”. (Greenspan's method) and that, “while cutting interest rates in such a crisis may help, it has the effect of transferring wealth from creditors to debtors and sowing the seeds for more serious problems further ahead.'"

“The bank said it was far from clear whether the US would be able to ignore the consequences of its latest imbalances, ($800 billion per year) citing a current account deficit running at 6.5% of GDP, a rise in US external liabilities by over $4 trillion from 2001 to 2005, and an unprecedented drop in the savings rate. ‘The dollar clearly remains vulnerable to a sudden loss of private sector confidence.”'

The BIS referred to the toxic effect of the “$470 billion in collateralized debt obligations (CDO), and a further $524 billion in "synthetic" CDOs which have spread through hedge funds industry. These CDOs are the loans (many sub primes) which were bundled off to Wall Street and turned into securities which are highly leveraged in hedge funds for maximum profitability. As Bear Stearns is discovering, these CDOs are like roadside bombs; exploding without notice whenever the stock market suddenly dips.

The BIS also cautioned about the excess of “leveraged buy-outs (mergers) which touched $753bn, with an average debt/cash flow ratio hitting a record 5.4…. ‘Sooner or later the credit cycle will turn and default rates will begin to rise.'”

The central banks around the world are increasingly worried that the Bush administration's profligate spending and irrational monetary policies will trigger a global depression. The recent volatility in the stock market suggests that the credit boom is just about over. Once the liquidity dries up---stocks will fall sharply.

The Housing Slump

Yesterday's housing data, shows that sales are still weak while inventory continues to grow. Existing home sales dropped 3% while prices dropped another 2.1%. Falling prices mean that cash-strapped home owners will not be able to tap into their home's equity for other expenses. Last year, mortgage equity withdrawals (MEWs) accounted for $600 billion of consumer spending. This year, the amount will be negligible at best.

The media and the Fed continue to mislead the public about the magnitude of the housing bubble. Fed chief Bernanke assures us that the sub prime calamity hasn't “spread to other parts of the economy” (tell that to Bear Stearns) and the media keeps cheerily reiterating that a “turnaround” or “soft landing” is just ahead.

These claims are ridiculous. Apart from the 80 or more sub-prime lenders that have gone “belly-up” in the last few months, the rickety collateralized debt obligations (CDOs) and mortgage backed securities (MBSs) are steamrolling their way through the stock market bowling down everything their path. Bear Stearns is just the first on the casualties list. There'll be many more before the storm is over.

Fed-chairman Bernanke knows what's going on. He was given a full rundown by “ John Burns Real Estate Consulting that the national sales information for both new and existing homes, is “misleading and covering up a deep plunge of the housing sector.” The housing market is freefalling. Existing-home sales are down 22% in May and mortgage applications have fallen a whopping 18%....In Florida home sales are down 34%, not 28% as NAR reported; Arizona sales are down 38%, not 28%; and California's down 37%, not 24% as NAR reports.”

Down 37% in California!?!

Gadzooks! It's a landslide.

As the defaults continue to pile up; the hedge funds will take a bigger and bigger pounding. It can't be avoided. That's what happens when bankers abandon traditional lending standards and lend trillions of thousands of dollars to people who have bad credit and lie on their loan applications.

Thousands of these same shaky sub primes loans have been wrapped up like the Crown Jewels and sold off to Wall Street as CDOs. Now they are ripping through the hedge fund industry like a tornado in a trailer park. The media has tried to downplay the damage, but its not hard to see what is really going on. According to Reuters:

"Banks doubled the amount of CDOs outstanding in the past two years to $2.6 trillion, including a record $769 billion sold last year, according to J.P. Morgan. These figures include funded and unfunded issuance. Pimco's Bill Gross said there are hundreds of billions of dollars of subprime residential mortgage-backed securities (RMBS), derivatives on subprime RMBS and collateralized debt obligations (CDOs) that buy subprime RMBS and/or the derivatives on the RMBS -- all of which he considers "toxic waste.”'

"$2.6 trillion"! That's enough to bring down the whole economy. And, as Bear Stearns proves, the whole mess is beginning to unwind pretty quickly.

“Foreign investors have been the dominant buyers of these exotic debt instruments in recent years, owing to their insatiable demand for yield. ‘If investors start dumping them, oh boy, watch out for some massive credit widening," said Dan Fuss, Vice Chairman at Loomis Sayles. (Reuters)

If the hedge fund industry follows the downward slide of the housing bubble, foreign investors will run for the exits. In fact, this may already being happening.

China sold $5.8 billion in US Treasuries in May; the first time they have dumped USTs on the market. This may be the first sign of “capital flight”---foreign investment fleeing the US for more promising markets in Asia and Europe. The greenback's survival now depends on the generosity of foreign bankers. If they refuse to recycle our $800 billion current account deficit by purchasing US bonds and securities, then the dollar will sink like a stone and lose its place as the world's reserve currency.

More Housing Blowdown

Last Friday, the stock market took a 185-point nosedive on the news that Bear Stearns was trying to raise $3.2 billion to rescue its battered hedge fund. According to the New York Times, however, Bear was only able to came up with "$1.6 billion in secured loans to bail out one of the 2 hedge funds".

The funds are the latest victim of the sub-prime meltdown which Bernanke and Paulson assured us was “largely contained”. In fact, Paulson even said, "We have had a major housing correction in this country," and "I do believe we are at or near the bottom."

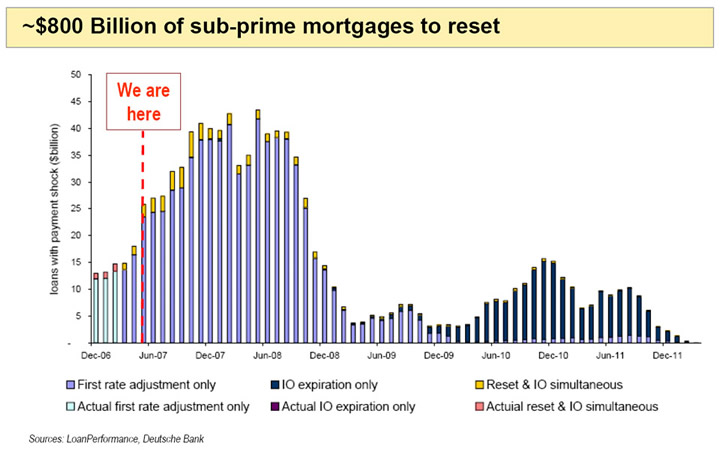

Anyone who believes Paulson should take a look the chart linked below:

It illustrates that how loan “resets” will continue to pound the housing market for at least another year and a half getting steadily worse as inventory grows.

The disaster is so bad that even the realtors are beginning to tell the truth. As one agent noted, “It's a bloodbath.”

But the debacle in housing is only the first part of a much larger problem—a global liquidity crisis. Banks and mortgage lenders have already begun to tighten up their lending practices and many have abandoned sub prime loans altogether. (20% of the housing market in 2006 was sub prime) Now the focus has shifted to the stock market, where banks are beginning to see that “risk” has not been properly calculated. That means that if more hedge funds collapse, the banks may not be able to cover the losses.

The Bear Stearns fiasco has had a chilling affect on lending. In fact, the New York Times reported on 6-26-07 that “After years of supersize private equity deals…the buyout boom may be about to hit a bump…Rising interest rates and tougher terms from investors may signal that private equity players will soon be struggling to continue reaping the outsize returns that have made the buyout business so lucrative.” (Private Equity Investors Hint at Cool Down” NY Times)

Liquidity is drying up in the private equity business. The troubles at Bear Stearns has changed the credit-landscape overnight. Bankers are nervous, money is getting tighter, and liquidity is vanishing.

"We know that these holdings are not unique to Bear Stearns," said Professor Joseph R. Mason, co-author of a recent study warning of dangers in securities backed by home loans to high-risk borrowers. "It would be hard to find a Wall Street firm that hasn't created similar funds."

That's right; the industry is waist-deep in these sub-prime time-bombs. Shaky loans and rising foreclosures threaten to knock the foundation blocks out from under the stock market and set off a wave of panic selling.

Could it have been avoided?

Perhaps, if there were better regulations on rating bonds and restricting leverage.

Consider this: one of Bear Stearns hedge funds took a $600 million investment and leveraged it 10 times its value to $7 billion. Their portfolio was chock-full of dicey CDOs and “illiquid assets” such as timber holdings in foreign countries and toll roads. These assets are difficult to price and nearly impossible to quickly auction off if the market suddenly takes a downturn.

It looked like Merrill Lynch & Co., was going to auction off $850 million of Bear Stearns CDOs this week, but backed off at the last minute. (They were reportedly only offered 30 cents on the dollar!) Once the hedge funds start selling these CDOs, then everyone will know how little they're worth. That could trigger a wave of selling that could bring down the stock market. Even if that scenario doesn't play out, the Bear Stearns incident ensures that CDOs in other hedge funds will be face a substantial downgrading that could take a big chunk out of their bottom line.

And, there's a bigger fear on Wall Street than the fact that 2 hedge funds are headed into bankruptcy, that is, that a sudden tightening of credit will send the over-leveraged stock market into a downward spiral.

The market is particularly sensitive to any rise in interest rates or tougher lending standards. It's become addicted to cheap credit and any break in the chain will cause equities to plummet.

Economist Henry C K Liu sums it up like this:

“The liquidity boom has been delivering strong growth through asset inflation without adding commensurate substantive expansion of the real economy. …. Unlike real physical assets, virtual financial mirages that arise out of thin air can evaporate again into thin air without warning. As inflation picks up, the liquidity boom and asset inflation will draw to a close, leaving a hollowed economy devoid of substance. …A global financial crisis is inevitable”. (Henry C K Liu “Liquidity boom and looming crisis” Asia Times)

In other words, the “virtual” wealth of Wall Street is a chimera which was created by the Fed's inexorable expansion of debt. It can vanish in a flash if the sources of liquidity are cut off.

Puru Saxena draws the same conclusion in his article “A Gradual Transition”:

“Thanks to the Federal Reserve's expansionary monetary policies over the past 5 years, US asset-prices have risen considerably; also known as the “wealth effect”. At the end of last year, the market capitalization of the US stock market rose to a record-high of US$20.6 trillion, matching the value of household real-estate, which also rose to a record-high at the same time. On the surface, this may seem like brilliant news, however you must realize that this “wealth illusion” achieved by an ocean of money and record-high indebtedness is only a consequence of inflation."

Code Red: Subprime Chernobyl

We expect that the mounting losses in CDOs and the continuing defaults in the housing industry will precipitate a “severe credit crunch” which will end in a stock market crash. A report which appeared yesterday in the UK Telegraph appears to agree with this analysis. Lombard Street Research predicted that:

"Excess liquidity in the global system will be slashed. Banks Capital is about to be decimated, which will require calling in a swathe of loans. This is going to aggravate the US ‘hard landing”' (“Banks set to call in swathe of loans” UK Telegraph 6-26-07)

Three of the main hoses which provide liquidity for the market, have either been cut off or severely damaged. These are "securatized" subprime CDOs, corporate mega-mergers and hedge fund leveraging. Without these instruments for expanding debt; liquidity will dry up and stocks will fall. The period of "easy credit" will end in disaster.

We should now be able to see the straight line that connects the Fed's low interest rates to the impending stock market meltdown. The problems began at the central bank.

Presidential candidate Rep. Ron Paul (R-Texas) summed it up best when he said:

“From the Great Depression, to the stagflation of the seventies, to the burst of the dot.com bubble; every economic downturn suffered by the country over the last 80 years can be traced to Federal Reserve policy. The Fed has followed a consistent policy of flooding the economy with easy money, leading to a misallocation of resources and artificial “boom” followed by recession or depression when the Fed-created bubble bursts”.

By Mike Whitney

Email: fergiewhitney@msn.com

Mike is a well respected freelance writer living in Washington state, interested in politics and economics from a libertarian perspective.

Mike Whitney Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.