United States Economy At Zero Hour To Service Debt Mountain

Economics / US Economy Nov 17, 2009 - 01:55 AM GMTBy: John_Mauldin

Today's Outside the Box comes to us from England. My European partner Niels Jensen from time to time sends me some of the best letters he reads from the hedge fund world. He is an excellent filter for me, and this week's Outside the Box offering is no exception. Below is the November commentary from Eclectica fund manager Hugh Hendry. He challenges the current preoccupation with the falling dollar and China, and posits what would happen if that thinking is wrong? It offers some very thought-provoking ideas. You can contact them for more information at info@eclectica-am.com or visit their website: http://www.eclectica-am.com

Today's Outside the Box comes to us from England. My European partner Niels Jensen from time to time sends me some of the best letters he reads from the hedge fund world. He is an excellent filter for me, and this week's Outside the Box offering is no exception. Below is the November commentary from Eclectica fund manager Hugh Hendry. He challenges the current preoccupation with the falling dollar and China, and posits what would happen if that thinking is wrong? It offers some very thought-provoking ideas. You can contact them for more information at info@eclectica-am.com or visit their website: http://www.eclectica-am.com

Your wondering if we are all turning Japanese analyst,

John Mauldin, Editor Outside the Box

Eclectica November Fund Commentary

by Hugh Hendry

Eclectica Fund Manager

"The power to become habituated to his surroundings is a marked characteristic of mankind." John Maynard Keynes The Economic Consequences of the Peace, 1921

This month I will attempt to answer the entrance examination for the Chinese civil service. That is to say, I will attempt to tell you everything that I know. In doing so, I will argue that this year's rally in inflationary assets, from emerging stock markets to industrial commodities to the fall in the US dollar, could be a FAKE. Let me explain why.

But first, I am indebted to Scott Sumner, professor of economics at the University of Bentley, and his essay on the economic lessons that can be drawn from timelessness in art (see http://blogsandwikis.bentley.edu/themoneyillusion/?p=2542). It is a theme that I will constantly revisit in my arguments below.

Sumner is able to take us from the Flemish forger, Van Meegeren, and his horrendous reproductions of the Dutch painter, Vermeer, to the notion that every recession seems unique and special to its protagonists. So just how did Van Meegeren fool the Nazis with paintings that today look so awful, so un-Vermeer? Jonathan Lopez, the noted art historian, argues that a FAKE succeeds owing to its power to sway the contemporary mind. Or in other words, the best forgeries tend to pay homage to the tastes and prejudices of their time. The present is so seductive.

Sumner is able to take us from the Flemish forger, Van Meegeren, and his horrendous reproductions of the Dutch painter, Vermeer, to the notion that every recession seems unique and special to its protagonists. So just how did Van Meegeren fool the Nazis with paintings that today look so awful, so un-Vermeer? Jonathan Lopez, the noted art historian, argues that a FAKE succeeds owing to its power to sway the contemporary mind. Or in other words, the best forgeries tend to pay homage to the tastes and prejudices of their time. The present is so seductive.

However, forget the art world. Controlling the psyche of this generation of investor is the indelible mark of the falling dollar and the associated fear of inflation. Monetary inflation has been the distinguishing feature of the last ten years, and it is now firmly embedded in the contemporary mind. I am sure I need not remind you that gold, along with just about every other commodity, has at least quadrupled in price since 1999. You already know my explanation for why this has happened.

The spectacular rise in the Chinese trade surplus, predominantly with America, to $320bn per annum at its peak in 2007, and the mercantilist desire to prevent currency appreciation drove the Asians and the sheiks to buy Treasuries and print their own currencies. The ability of fractional reserve banking to leverage this liquidity many times over provided the monetary mo-jo to instigate ever higher commodity prices. In other words, quantitative easing, masquerading as a cheap but fixed currency regime, has succeeded where Japan's orthodox version has failed. The QE succeeded because, amongst other features, it raised the velocity of monetary circulation.

However, it was not always like this. As an example, ten years ago it was unthinkable that the dollar would prove so fragile. Recall that back then, when the euro was first launched in 1999, it promptly lost 31% of its value against the greenback. The subsequent reconstruction of modern China, though, intervened. In order to finance the emergence of a new economic superpower, an abundance of dollars was needed. Have no doubt that had we not had the dollar as a reserve currency, the rise of China would not have been as swift nor as decisive.

The Yellow Brick Road

Consider another economy needing to be rebuilt: that of the United States in 1865, the post Civil War era. The rebirth of the American economy was funded from the monetary rectitude of the gold standard, not from the generosity of a foreign and infinitely expandable paper currency. However, all of this occurred before the discovery of cyanide for heap-leaching and the opening up of the huge South African gold fields. In other words, hard money was in tight supply and the recovery was neither swift nor decisive. Indeed, 30 years later, during the presidential election campaign of 1896, Williams Jennings Bryan was still hotly contesting its merits. He railed against the persistent price deflation and argued that the economy was burdened by a "cross of gold" (see The Eclectica Fund Report, December 2005).

Perhaps I Should Stick to the Twenty-First Century?

My previous investment letter attempted to explain the subtleties of the Triffen dilemma and the dollar's pre-eminent role in regenerating modern day economies. Let me repeat once more: lots of dollars were required, and duly delivered, to build modern China. They did not have to wait on the vagaries of a gold discovery to promote and sustain their economic engine. Instead, they required the willingness of their trade partners to run trade deficits. The US delivered and, partly as a consequence, the Fed's broader trade weighted dollar index has now fallen 20% since its peak in 2002 (the narrower DXY index compiled by the Intercontinental Exchange has fallen more, but excludes the renminbi and overstates the role of the euro). In return, the world has a new $4trn trading partner: China.

Heady stuff, but not without precedent: recall the Marshall Plan, a watershed American aid program that assisted the reconstruction of the Western European economy during the 1950s and 60s. This was further augmented by America's willingness to run trade deficits, the modern day equivalent to a gold discovery, which became necessary to sustain the emergence of the new economic trading bloc. This resulted in the dollar's huge devaluation versus gold in the 1970s. However, back then, the broad trade weighted index kept rising. This time it has fallen sharply.

What an Ungrateful Lot We Are?

The dollar's role as the world's sole reserve currency has both assisted and accelerated the development of world trade. America's trading partners have come to rely upon the bounty of dollars necessary to recycle their trade surpluses and thus finance their growing prosperity. This was done even at the expense of domestic American job losses. Replace the dollar with IMF special drawing rights; I hear your retort. Sure, but have you ever bought a cup of coffee with an accounting identity? And, fundamentally that argument still suffers from the dearth of any other major economy showing any willingness to sacrifice its short term economic standing for the longer-term mutual benefit of having enriched trading partners.

Do not forget that the Chinese could replicate equivalent currency baskets to SDRs at any moment. Instead, they continue to recycle almost three quarters of their trade surplus back into dollars. This is not coercion but simple commercial pragmatism. They know full well that neither Europe nor Japan nor Britain nor Switzerland nor the rest of Asia are willing to sacrifice the implicit loss of manufacturing jobs. They understand that it is only the US that is willing to embrace the benefits of comparative advantage that arise from international trade. Have you ever asked yourself why car prices in America are so low compared with those in Europe? This is my point.

I keep hearing that a dollar devaluation would help matters. I agree; it has. Let me say it again; we have already had the devaluation. That is what the last five years were all about. Now with China rebuilt, and the trade deficit in full retreat (note the -47% contribution from net exports to China's GDP growth in the first 9 months of this year), there are less dollar bills being exported overseas to ungrateful recipients. Is it not time we drop our fascination with the present and consider the future? Is it really inconceivable that the dollar could now strengthen?

Women in Love, Investors in Love. What's the Difference?

Of course this is a minority view. Investors have reacted to last year's deflationary traumas by insisting that it is business as usual. They behave like D.H. Lawrence's coal miner Gerald from the novel Women in Love, who, just days after his father's funeral, steals into his former lover's bedroom and, "...into her he poured all his pent-up darkness and corrosive heat, and he was whole again." Or was he? The trouble is that we are so anchored to the recent past. Investors are fearful of what now seems so familiar and recognisable; at what they perceive as the reckless behaviour of our monetary authorities. "Inflation is a monetary phenomenon" is their Friedmanite dogma. Their salvation can only be found in the safe sanctuary of gold and the embrace of risky assets, but are they truly safe?

This is my home. Don't be so sure about anything, Big Horace. Not about anything in this world. The Orphan's Home Cycle Horton Foote

And so, just as the Church of England commissioners became convinced by the cult of equity way back in the whimsical days of 1999 and went 100% long the stock market, investors today recant a new mantra of, "anything but the dollar (A-B-D)". Inflation bets are all the rage. Some would insist that it is their fiduciary duty to protect their clients' capital; I say tell that to the Church of England pension fund, whose assets today are just £461m against liabilities of £813m. Austerity beckons for the clergymen; heaven will have to pay their stipend.

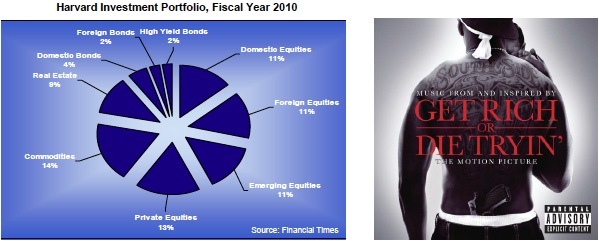

But the spell cast by a contemporary cult is hard to resist. Take another august body, the Harvard Endowment Fund. Not typically renowned as a hotbed of reactionary fervour, the fund is nevertheless radical in its construction and has come to typify the A-B-D stance.

Harvard's position could well be construed as a one-way bet. Almost half of the fund is invested in emerging market equities, commodities, real-estate, private equity and junk bonds. It is as though the rap artist 50 Cent has taken over the advisory board. The fund is going to, "get rich or die tryin'".

We, on the other hand, approach risk by considering the worst possible outcome. For a current pension scheme the greatest torment would be a repeat of last year's final quarter when 30 year Treasuries yielded just 2.5%. This would require a CAGR of 20% or more from the fund's riskier assets at precisely the time that their future returns would seem most questionable; insolvency would beckon. And yet, they blithely run the risk of ruination.

Of course, they are not alone. Another popular argument is that the emerging economies have to urgently diversify their immense dollar reserves. And so the Chinese are colonising the African continent in the pursuit of commodities and the Indian government has just agreed to buy 200 tons of the IMF's gold hoard.

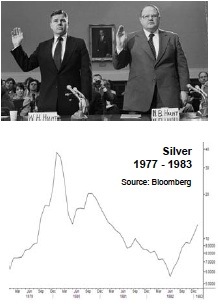

Is this not a reincarnation of the 1980 trade of the brothers Hunt? It is hardly an exaggeration to suggest that China, for all intents and purposes, is already the commodity market. For despite providing less than 8% of global GDP, China accounts for more than half of the world's steel production and more than half of global seaborne iron ore freight. Indeed, this peculiarity is circular in nature. Consider that a modern aluminium plant requires 25% of the project's cost to be spent on buying aluminium in the first place. And remember that investments in fixed capital formation (think new aluminium plants et al.) have made up 95% of Chinese GDP growth this year. China Inc. is Commodities Inc.

Is this not a reincarnation of the 1980 trade of the brothers Hunt? It is hardly an exaggeration to suggest that China, for all intents and purposes, is already the commodity market. For despite providing less than 8% of global GDP, China accounts for more than half of the world's steel production and more than half of global seaborne iron ore freight. Indeed, this peculiarity is circular in nature. Consider that a modern aluminium plant requires 25% of the project's cost to be spent on buying aluminium in the first place. And remember that investments in fixed capital formation (think new aluminium plants et al.) have made up 95% of Chinese GDP growth this year. China Inc. is Commodities Inc.

Accordingly, China shares the same risk as the world's largest pension schemes. An over- leveraged American consumer does not return to his/her manic buying of old. As William White, former chief economist of the BIS, has argued:

Many countries that relied heavily on exports as a growth strategy are now geared up to provide goods and services to heavily indebted countries that no longer have the will or the means to buy them.

Surely, the Chinese stash of Treasuries is a prudent elimination of the fat tail risk that private sector deleveraging in the west ends up killing the golden goose of the trade surplus. But instead, in exercising good ol' Texan tradition, they have opted, like the Hunt brothers did, to double up. It is the old dice game, Mort Subite, played by the employees of the National Bank of Belgium in the busy lunch time cafes of Brussels in 1910. If the players didn't have time to complete their business, they played a final round with a sudden ending where the loser would be pronounced dead.

Much is made of the comparison between today's balance sheet recession and Japan's demise back in 1989. Despite their bubble never coming close to matching China's prominence in industrial commodities, the loss of Japanese economic growth in the 1990s was nevertheless a major factor in the waterfall crash in commodities. This plunge ultimately saw oil trade for as little as $10 per barrel in the next decade. Just consider how much more devastating the experience would have been had they gone very long the commodity market in 1989 rather than golf courses and Rockefeller Centre. At least the Harvard endowment scheme did not share their enthusiasm for golf. But, this time around, I fear a Mort Subite beckons for the losers in Asia and the pension market.

Last Orders: Inflation or Deflation?

If a poet knows more about a horse than he does about heaven, he might better stick to the horse... the horse might carry him to heaven. Charles Ives

I am now going to return to the torturous and binary debate concerning inflation. As you know, I am in the deflation camp for now, and we own a modest amount of government bonds and a series of asymmetric bets which would receive a boost from a return to some form of risk aversion. You could say that I am sticking to my horse.

My intellectual foes, on the other hand, are adamant that long duration government bonds are a short. I even hear that some Wall Street legends are so convinced of the argument made by the likes of Niall Ferguson that they personally own Treasury put options and are actively counselling others to do the same. The argument can be condensed into just two fears.

First, they will suggest that 4.5% is not an adequate return for lending your money to the profligate United States for 30 years. I agree wholeheartedly. Again, I fear it is my accent, but let me stress once more that I do not propose that anyone adopt a buy-and-hold policy for the next thirty years in bonds. However, a nominal rate of 4.5% might prove very profitable over the coming year should breakeven inflation expectations head south again.

Second, the bears contend, a lower Chinese trade surplus will eliminate a very large source of Treasury buyers at a time of burgeoning supply. Again, we find ourselves agreeing vigorously. However, it is our contention that US savings are heading north over the months and years to come. And an America that saves is an America that does not run a current account deficit. It is an American that can finance its own spending domestically. The US produced a small surplus back in the 1990-91 recession, so why not again?

As a consequence the Chinese surplus is set to fall further and, with fewer dollars needing to be recycled to maintain the currency peg, their demand for Treasuries will continue to shrink. Now this is potentially a huge headache owing to the massive projected American budget deficits for this year and next, and the Treasury's desire to extend the maturity of the existing stock of government bonds which is becoming perilously short dated. Some estimate new issuance of around $2.5trn for the upcoming year. Perhaps, it is better that we buy those Treasury put options after all?

American Gothic

American Gothic

Or is it? I have quoted Don Coxe's definition of a bull market before and I intend to do so again. "The most exciting returns are to be had from an asset class where those who know it best, love it least." On this point, America has fallen out of love with its own currency and bond market. Foreigners own over half of the outstanding Treasury stock. But, like I said, I think events could reignite some of the natives' old amour.

It is almost like declaring an enthusiasm for Say's Law. Think of it this way, a greater supply of Treasuries would be a very obvious by-product of weaker than anticipated economic growth. And in this environment risk aversion stimulates the investment desire for risk free assets. So, in a round about way, there are circumstances when supply and demand can match in the bond market. But weaker economic growth? Surely the governments' interventions this year have remedied the economy?

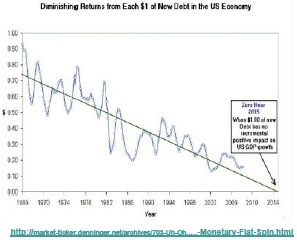

The surprise might concern the role that rising leverage has played in boosting GDP and in anchoring investors' expectations to an unrealistic level of nominal GDP. Over the last decade, each marginal dollar of debt has generated less and less marginal income. We knew that there would be a "zero-hour" for the economy when the creation of new debt would not contribute to GDP growth. The government's reaction to last year's demand shock has been to increase its own leverage. But, with the economy operating at its zero-hour, we believe this incremental leverage will actually have a negative impact. That is to say, the public sector will fail in its attempt to bring the economy back to its previous level of nominal GDP. In this scenario, the outcome will disappoint the market's expectations, which are rampantly bullish as evidenced by this year's dramatic re-pricing of risk assets.

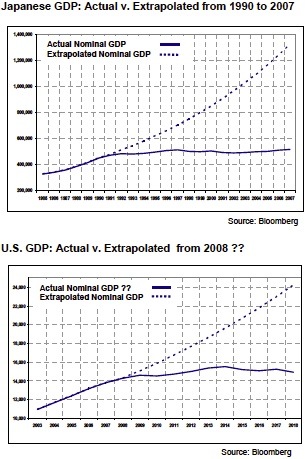

This zero-hour for America has perhaps arrived sooner than many had anticipated. It was heralded by the Japanese experience. Japan is the bogeyman that confronts all academic thinkers, regardless of creed, from Krugman to Ferguson, as well as all who would choose to intervene in the workings of the economy. In a debate I had with Mr. Ferguson in London last month, he claimed that Japan was an extreme outlier and could be ignored. Really?

This zero-hour for America has perhaps arrived sooner than many had anticipated. It was heralded by the Japanese experience. Japan is the bogeyman that confronts all academic thinkers, regardless of creed, from Krugman to Ferguson, as well as all who would choose to intervene in the workings of the economy. In a debate I had with Mr. Ferguson in London last month, he claimed that Japan was an extreme outlier and could be ignored. Really?

No sex, no drugs, no wine, no woman, no fun, no sin, no wonder it's dark Everyone around me is a total stranger. Everyone avoids me like a psyched loan-ranger That's why I'm turning Japanese, I think I'm turning Japanese, I really think so The Vapors, 1980

Japan has championed both Friedman and Keynes. They have built bridges to nowhere and dropped Yen notes from helicopters for twenty years and still they have nothing to show for it. Clearly the additional return from Yen debt in Japan is close to zero and it exposes the nightmare of interventionists everywhere: it may just be that there are no policy remedies for a debt deflation. So to elaborate further, our chances of financial success are greatest under conditions where investors believe government spending will succeed but in reality it fails.

However, where will the demand for all of this additional government debt come from? Let us review the Fed's Z1 numbers. The US has household wealth of some $67trn. Of that, $20trn is accounted for by real estate and is perhaps out of bounds for our purposes. But $8trn is held in the form of private pensions and insurance funds. And yet, remarkably, these institutions presently allocate just $630bn to Treasuries et al. Households have a further $22trn in time deposits and other financial assets. But again they own just $500bn of Treasuries, and commercial banks own a tiny $130bn or, 1% of their total asset base of $12trn.

Consider that in 1952, at the very end of the supernova bond bull market formed from the ashes of the Great Depression and the Liberty Bonds that financed the Second World War, US banks held 40% of their gross assets in Treasuries. That is a potential $5trn of demand from this one source alone, albeit spread out over a number of years. And again, the Japan experience lends support. Japanese financial institutions have quadrupled the percentage of their assets held in JGBs. Furthermore, their households have lifted their government bond weightings five-fold over the last ten years. Should the same pattern repeat itself stateside, American households would need to buy another $2.5trn, but again, over ten years.

And let us not forget that a trend of rising prices allied to the most basic human emotion of avarice encouraged commercial banks and other financial institutions to buy $3.2trn of questionable mortgage backed securities in 2004, $1.9trn in 2005, $2.2trn in 2006 and $2.1trn in 2007. So it is not inconceivable, at least in my mind, that financial institutions, and notable amongst them the nation's pension and endowment schemes, could be motivated by another basic human emotion, namely fear for their own survival, to snap up all these new government bonds. Perhaps in the end supply will create its own demand.

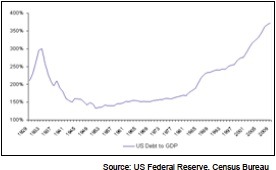

Again, it all really comes down to your take on the ratio of total debt-to-GDP. If you believe, like I do, that it peaked in 2007 then the repercussions are enormous. The leverage does not necessarily have to come down (after peaking in 1932 at 300% it troughed 20 years later at 150%). Rather, it may well be that low interest rates allow the mountain of debt to continue to be serviced. This has been the Japanese experience to date. However, everything in our economic life exists at the margin, and the consequences of just maintaining the leverage constant would be a very low delta in nominal GDP growth. Consider that the Japanese, under these very circumstances, have managed to grow nominal GDP at just 1% compound since 1990.

Again, it all really comes down to your take on the ratio of total debt-to-GDP. If you believe, like I do, that it peaked in 2007 then the repercussions are enormous. The leverage does not necessarily have to come down (after peaking in 1932 at 300% it troughed 20 years later at 150%). Rather, it may well be that low interest rates allow the mountain of debt to continue to be serviced. This has been the Japanese experience to date. However, everything in our economic life exists at the margin, and the consequences of just maintaining the leverage constant would be a very low delta in nominal GDP growth. Consider that the Japanese, under these very circumstances, have managed to grow nominal GDP at just 1% compound since 1990.

In Bernie We Trust?

This is why China's mad dash for commodities and its investment splurge this year is so worrying. In my marketing presentations I show a picture of Madoff superimposed on a dollar bill and ask, "...in Bernie we trust?" My point is that if the hedge fund fraudster had been given the responsibility for US GDP accounting, he would surely have overstated the figure. And in a similar way, the rise in leverage has probably misrepresented the truly recurring nature of nominal GDP. Now, if we repeat the Japanese experience then it is possible that nominal US GDP will rise from $14trn today to perhaps just $16trn in ten years time. Along similar lines, the German government does not anticipate its economy exceeding its previous GDP high until 2014. And yet it is as though the other surplus countries are behaving like Bernie's former investors who, believing in the stated NAV and its promise of more of the same (i.e., predictable and attractive compound growth rates), were happy to spend lavishly. The Chinese are building capacity to meet a world where US nominal GDP is $25trn in ten years time. I fear they could be in for a nasty shock.

This is why China's mad dash for commodities and its investment splurge this year is so worrying. In my marketing presentations I show a picture of Madoff superimposed on a dollar bill and ask, "...in Bernie we trust?" My point is that if the hedge fund fraudster had been given the responsibility for US GDP accounting, he would surely have overstated the figure. And in a similar way, the rise in leverage has probably misrepresented the truly recurring nature of nominal GDP. Now, if we repeat the Japanese experience then it is possible that nominal US GDP will rise from $14trn today to perhaps just $16trn in ten years time. Along similar lines, the German government does not anticipate its economy exceeding its previous GDP high until 2014. And yet it is as though the other surplus countries are behaving like Bernie's former investors who, believing in the stated NAV and its promise of more of the same (i.e., predictable and attractive compound growth rates), were happy to spend lavishly. The Chinese are building capacity to meet a world where US nominal GDP is $25trn in ten years time. I fear they could be in for a nasty shock.

What Do I Mean?

Consider the steel market. The homogeneous nature of steel, as well as other factors such as its price-to-density, allows for the export of the finished good across trade boundaries. Now with China having been on such an expansionary tear, it may not surprise you to hear that finished Chinese steel prices today trade below their production cost. Furthermore, import license applications to sell steel in the US, the world's largest export market, rose 24% last month. Now, mostly this comes from Mexican and Korean producers, but clearly there is the implicit threat that their Chinese competitors might also be tempted.

But the Economy is Growing?

Clearly it would be inappropriate to annualise the production of the US steel industry in the fourth quarter of last year when capacity utilisation plummeted to just 32%. So consider, instead, the annual run rate this year from January to August. This was a period of stabilisation in tandem with the cash-for-clunkers program, which boosted the industry's largest customer, the car sector. It is quite chilling to note that steel production in America is on a par with output back in 1938, when GDP was a mere 7% of its current size. The industry's run rate dropped to a paltry 13% during the Great Depression. However, output only troughed at its 1908 level; a twenty year retracement that is a far cry from our 70 year retracement. So the physical developments in the western steel markets should raise some concern. However, with an active steel futures market in China turning over $15bn a day (consult the Bloomberg page <RBTA CMDY CT>), speculative fears concerning the dollar have overcome the paucity of industrial demand in the west.

Of course, it is not just steel. Consider the aluminium market. We recently had a very bearish meeting with the Norwegian company Norsk Hydro. Admittedly, their strong petro-currency does not help and you have to discount the solace I seek in finding people even more miserable than myself. Even so, the aluminium situation mimics that of steel, but with an even mightier inventory overhang. Four and a half million tons reside at the London Metal Exchange, perhaps 20% of world ex-China annual capacity. It is probable that 75% of this surplus stock is accounted for by financial players exploiting a contango.

Does Life Imitate Art?

The advocates of Prechter's socio-economics would not be surprised to hear that the Romanian writer Herta Mueller has been awarded this year's Nobel Prize for literature for her work depicting "the landscape of the dispossessed". In a Los Angeles Times review of her book, The Appointment, they noted,

"...it is sometimes difficult to tell whether we are reading about people driven mad by a mad regime or people who may not have had all their marbles in the first place."

My partner, Mr. Lee, reflected on this as he sat in the chilly offices of Norsk Hydro last week watching the snow fall outside. The Norwegians continued with their tale of woe: a couple of million tonnes of inventory remains unaccounted for on the world stage and are believed to be hidden in cheaper warehouses in Russia. The rationale behind this is the same as the rationale used by LME speculators. Furthermore, the big Russian players like Rusal are under intense pressure from Putin not to cut capacity (check out 'Putin ***** slaps Deripaska' on http://www.youtube.com/watch?v=PprlM5R3Hbg), and are rumoured to be surviving only by not paying their electricity bills.

To make matters even worse, the Chinese have stopped importing and are eager to ramp up domestic aluminium production. They havethe capacity to produce another 13mt annually, which is equivalent to 52% of global production. Lastly, there is the fact that Rio Tinto bought Alcan right at the very top of the cycle, though they dare not admit it is a terrible business.

Poor Old Norsk Hydro?

Who would want to share a stage with so many mad villains? The Norwegians noted that construction demand had just taken another leg down as buildings started pre-crisis are now finished whilst no further pipeline exists outside of China. Even Ryanair are talking about suspending their aggressive growth plans and may delay the purchase of more planes. The Norwegians suffer the most pain at present, but if the dollar were to strengthen Alcoa could conceivably go bust. Their dollar cost is the company's only competitive advantage. Let us not forget Alcoa has the most exposure to aircraft construction and still has $10bn of gross debt lording over an almost equivalent market cap. Imagine that we have not even considered their pension liabilities. Yet the Alcoa CDS trades at 200 basis points, down from its high of 1200 earlier this year. Why?!

"May sorrow break these chains of my sufferings, for pity's sake" Lascia ch'io pianga Handel

Now remember I have been describing a positive macro scenario: a world in which low interest rates make the debt load manageable and that we muddle through with lower growth rates in nominal GDP. But clearly the consequences for corporate profitability are very poor. The alarming thing is that my opponents (see Ferguson et al.) believe that government bond yields are going much higher. Effectively, the world's bond vigilantes are going to punish the Fed and tighten monetary policy. It is almost as if the world's greatest speculators are agitating for their own demise. It is my contention that the leverage of the economy is only tenable if interest rates stay low and yet, whilst I believe some of them agree, they still fervently expect a rise.

Je consens, ou plutôt j'aspire à ma ruine. Pierre Corneille Polyeucte, 1642

Do not forget that the US does not share the distinction of the British or Australian housing markets. According to FSA data, 55% of UK mortgages are fixed rate and 45% are floating. The latter have, of course, collapsed and have proven a boon for disposable income. We must remember, however, that British fixed rates are determined by two and three year swap rates; so effectively the entire stock of UK mortgages are determined by the central bank and could be thought of as floating. In the US, however, things are very different. Total single-family mortgages outstanding are $11trn but $9trn is fixed to the prevailing 30 year Treasury yield. Banks just do not offer variable rate or teaser mortgages anymore. You might say that the American housing market hangs by the tender threads of the bond market's generosity. Lose it, and let us say that the markets demand 6% yields on 30 year durations and mortgage rates would then shoot back up to 7%. And, I would argue, the economy would come to a crashing halt. Do speculators really want this to happen?

Perhaps I am describing a pressure cooker. The private sector's debt may be sustained by maintaining low nominal interest rates.But the pressure from so much issuance at a time of great reluctance from financial institutions to purchase bonds could break the stalemate. And with it the ominous precedent of 1931, outlined in our February report, when a back up in ten year Treasury yields from 3.1% to 4.4% undoubtedly accelerated the rate of deflation in the US economy.

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.