Australian Housing Bubble About to Burst, Market About to Crash

Housing-Market / Austrailia Feb 03, 2010 - 12:47 AM GMTBy: Mike_Shedlock

Today the Reserve Bank of Australia (RBA) unexpectedly held interest rates at 3.75%. No doubt this was in fear of the Australia's enormous housing bubble that exceeds the height of the bubble that long ago burst in the US. 20 economists predicted the RBA would hike. Not a single one predicted anything else.

Today the Reserve Bank of Australia (RBA) unexpectedly held interest rates at 3.75%. No doubt this was in fear of the Australia's enormous housing bubble that exceeds the height of the bubble that long ago burst in the US. 20 economists predicted the RBA would hike. Not a single one predicted anything else.

Fear in the board of governors over the pending crash is palpable. Prime Minister Kevin Rudd did not learn a single thing from the US and the disastrous policies of Greenspan. He gave one last goose to the housing market with $14,000 tax credits in a foolish attempt to stem the tide of the global recession that started two years ago.

Prime Minister Rudd brags about Australia's ability to duck the recession. It did not work. All Rudd did was delay the inevitable, fueling an even bigger housing bubble. The bigger the bubble, the bigger the crash, and rest assured Australia is headed for a housing crash.

Here are a few snips from the Bloomberg article Australia Unexpectedly Keeps Interest Rate at 3.75%.

The Reserve Bank of Australia kept the overnight cash rate target at 3.75 percent after three increases, it said in Sydney today. The decision confounded the forecast of all 20 economists in a Bloomberg News survey for a quarter-point move, and futures contracts that signaled a 74 percent chance of an increase.

Australia’s dollar tumbled to a six-week low and Asian stocks pared gains after the announcement sparked concern at the economy’s ability to withstand higher borrowing costs. Business confidence fell to a six-month low, a report showed today, and Woolworths Ltd., the country’s biggest retailer, warned last week that rate increases would hurt consumers.

Business confidence fell in December to the lowest level in six months, a report by National Australia Bank Ltd. showed today. The bank’s sentiment index dropped 11 points to 8. Lending to companies “has continued to fall as companies have sought to reduce leverage, and lenders have imposed tighter lending standards,” Stevens said today. “Credit conditions remain difficult for many smaller businesses,” he said.Here is a statement from the article that particularly caught my eye: Prasad Patkar, who helps manage about $1.5 billion at Platypus Asset Management in Sydney said "Today’s decision reduces the serious risk of a policy blunder.”

Serious Policy Blunder

Sorry Prasad, a serious policy error was made long ago, and there is not a damn thing the RBA or anyone else can do to stop the impending housing crash in Australia.

What follows is a post I actually wrote yesterday. I intended to post this before the rate decisions, but it never happened. I too, thought one more hike was coming. That it did not come is a sign of panic at the RBA.

First Time Buyers In Severe Stress

Just as happened in the United states with subprime borrowers, Australia's first-home buyers struggle as interest rates rise.

Almost half of first-home buyers lured into the market by the Rudd Government's $14,000 grant are struggling to meet their mortgage repayments and many are already in arrears on their loans.

Thousands of young home buyers are using credit cards or other loans to meet obligations, while those in "severe stress" are missing payments.

Just weeks after the grant was withdrawn, a survey of more than 26,000 borrowers conducted by Fujitsu Consulting has found 45 per cent of first-home owners who entered the market during the past 18 months are experiencing "mortgage stress" or "severe mortgage stress".

"The dream of home ownership has turned sour for many thousands of first-home buyers now that the reality of rising interest rates is kicking in," said Fujitsu Consulting managing director Martin North.

"Rising utility costs and school fees are also cited as reasons for hardship, and many first-home owners are living without proper furniture or carpets as they divert all their cash to their monthly repayments."

During the past 18 months, more than 135,000 first-home buyers have entered the market, encouraged by the generous grants and stamp-duty relief.

As a result, more than 50 per cent of first-home owners are forecast to be in the "mortgage stress" category by the end of this year.

"This was a disaster waiting to happen," Steve Keen, professor of economics at the University of NSW, said yesterday.

"The grant panicked first-home buyers to rush into the market, which pushed prices up by far more than the grant itself. Now we have buyers falling behind with their repayments as rates increase and thousands of owners exposed to the danger of bankruptcy as the situation deteriorates."

No Lessons Learned

"LD", a reader from Australia who sent me the link asked and answered his own question: "What have Australians learned from Americans over the last 2 years? Nothing!"

Credit Squeeze Coming Up

Craig, another reader from Australia writes ...

Mish

I've been waiting a long time to buy a house in Australia. Looks like I may not have to wait too much longer for the Aussie bubble to burst. As always, love your blog. Cheers, Craig

Craig is referring to Tighter credit rules to halve home loans.

Last week Westpac cut its loan-to-value ratio (LVR) for new customers to just 87 per cent of the property's value - a new low for a big bank. Although it may appear relatively small, such a cut has a disproportionate effect on how much people can borrow and can halve the value of the property they can afford to buy.

"If you have a $50,000 deposit and you can get a 95 per cent loan, you are able to bid on a property worth $1 million," said Steve Keen, associate professor of economics at the University of Western Sydney. "But if the LVR is cut to 90 per cent, your $50,000 deposit is only equivalent to 10 per cent deposit on a $500,000 property, so the amount you can spend is halved."

Westpac's reduction from a maximum LVR of 92 per cent means that buyers with a $50,000 deposit will see the maximum that they can afford to pay for a property slashed from $625,000 to $384,615. Somebody with a $20,000 deposit would see the amount that they could spend reduced from $250,000 to $153,846, says Professor Keen.

Experts are worried that, if other banks follow suit, credit to the property market will be choked off and property prices could collapse. According to research by broker Mortgage Choice, fewer than half of all new home buyers have a deposit of more than 10 per cent of the property's value.

"Westpac's move could affect many thousands of buyers and they will be forced to go to new lenders," a spokesman said. "It's a very worrying development because if others follow suit, we could see the majority of first-home buyers priced out of the market."

Further restrictions now appear to be inevitable. "And banks can't go on lending forever."

Lenders have gradually been cutting back the size of loans that they are prepared to offer home buyers. Just over a year ago, 100 per cent - or even 105 per cent - loans were relatively common. But over the past 12 months, the LVR has fallen steadily to 95 per cent, then to 90 per cent, and now to 87 for new borrowers approaching Westpac.

It was this same tightening of credit that led to the collapse of property prices in the UK in 2008, even though the country was still suffering from a massive shortgage of homes at the time.

Deposit Math

Note the above paragraph in red by Steve Keen, one of few economists in the world who actually has a clue. His blog is Steve Keen’s Debtwatch.

Also note the worries of the so-called housing experts in the above article: Experts are worried that, if other banks follow suit, credit to the property market will be choked off and property prices could collapse.

If those "experts" had an ounce of common sense they would be worried the housing bubble would get bigger.

Indeed, housing prices are so stretched in Australia that the bubble will bust soon enough regardless of whether lenders tighten standards or not.

The US housing bubble burst with credit standards still getting looser a year or more later.

When Do Bubbles Burst?

Bubbles burst when the pool of greater fools runs out, and not before.

That is exactly why Economist Steve Keen lost housing bet against Rory Robertson.

AN ECONOMIST known as the "Merchant of Gloom" will have to walk from Canberra to the top of Australia's highest mountain after losing a bet about the resiliency of Australian house prices.

Last November, University of Western Sydney associate professor of economics and finance Steve Keen made a high-profile bet with Macquarie Group interest rate strategist Rory Robertson.

The two parts of the bet were that house prices would tank by the end of 2009 and that house prices would fall 40 per cent from their all-time high within 15 years.

The loser of the bet would have to make the more than 200km trek from Canberra to the top of Mount Kosciuszko wearing a T-shirt that says "I was hopelessly wrong on house prices! Ask me how."

Keen's mistake (miscalculation is a better word as I am positive he will ultimately be proven correct), was that he misjudged actions the Rudd administration might take to keep the bubble going.

Bear in mind that once the trend changes, it changes for good, but until the trend does change, efforts to keep bubbles alive frequently produce blowoff tops.

In Australia's case I finally sense a blowoff top in fools. The US suffered the same fate in 2005 when the cover of Time Magazine went "gaga over real estate" and people were camping out overnight and entering lotteries for the right to buy Florida condos.

Inquiring minds might be interested in the following flashbacks, the first showing the funniest Time Magazine cover in history, the second shows approximately where we are today although I do have to move the arrow one notch closer to the bottom.

April 10, 2006: US vs. Japan Land Prices Pictorial Update

July 13, 2009: Housing Update - How Far To The Bottom?

How did Bernanke and other experts fair?

Let's answer that with a few more flashbacks.

The initial data point on my chart came in the post It's a Totally New Paradigm on March 26, 2005. Here are some excerpts from that post.

- Ron Shuffield, president of Esslinger-Wooten-Maxwell Realtors says that "South Florida is working off of a totally new economic model than any of us have ever experienced in the past." He predicts that a limited supply of land coupled with demand from baby boomers and foreigners will prolong the boom indefinitely.

- "I just don't think we have what it takes to prick the bubble," said Diane C. Swonk, chief economist at Mesirow Financial in Chicago, who was an optimist during the 90's. "I don't think prices are going to fall, and I don't think they're even going to be flat."

- Gregory J. Heym, the chief economist at Brown Harris Stevens, is not sold on the inevitability of a downturn. He bases his confidence in the market on things like continuing low mortgage rates, high Wall Street bonuses and the tax benefits of home ownership. "It is a new paradigm" he said.

Flashback October 27, 2005

Inquiring minds may wish to review Bernanke: There's No Housing Bubble to Go Bust.

Ben S. Bernanke does not think the national housing boom is a bubble that is about to burst, he indicated to Congress last week, just a few days before President Bush nominated him to become the next chairman of the Federal Reserve.

U.S. house prices have risen by nearly 25 percent over the past two years, noted Bernanke, currently chairman of the president's Council of Economic Advisers, in testimony to Congress's Joint Economic Committee. But these increases, he said, "largely reflect strong economic fundamentals," such as strong growth in jobs, incomes and the number of new households.

Flashback February 12, 2008

Bernanke Expects Housing Recovery by Year End

Federal Reserve Chairman Ben Bernanke told lawmakers Tuesday he expects the downtrodden U.S. housing sector to improve by the end of the year, a senator who participated in the closed-door meeting said.

"He let us believe that the housing situation should begin to ameliorate by the end of the year," said Sen. Pete Domenici, a New Mexico Republican, told reporters.

"He gave a very good, succinct, short overview of where he thought the economy was right now and how it might move forward," said Sen. Jon Kyl of Arizona.Bubbles and Humpty Dumpty

Bernanke has proven all the king's horses and all the king's men cannot put bubbles together again.

For further proof please see Bernanke's Deflation Preventing Scorecard.

After bubbles burst, nothing matters including loose lending standards in the US that lasted long after the housing peak in summer of 2005.

Supply of Fools Exhausted

I am willing to bet that at long last, Australia's pool of greater fools just ran out. Rudd's ridiculous $14,000 grant and stamp-duty relief programs were likely enough to exhaust that pool.

The ultimate irony of Keen's bet is that by the time he starts his hike in April he will likely be right.

Bear in mind however, that prices tend to fall slowly at first as inventory builds up. Then the losses accelerate quickly.

A Long Wait

By the way, Australia buyers might need to wait 5-7 years or more for reasonable valuations. Look how long it took for the US housing bubble to implode. We have not hit bottom yet after 5 years, and the Australia bubble has a bigger starting point.

Please see Housing Bubble Comparison: US, UK, Canada, Spain, Australia, Japan for a county by country comparison of housing bubbles from the Ecomomist.

Demographia International Housing Survey

Inquiring minds are reviewing the results of the 6th Annual Demographia International Housing Affordability Survey. Countries in the survey include Australia, Canada, Ireland, New Zealand, the United Kingdom, and the United States.

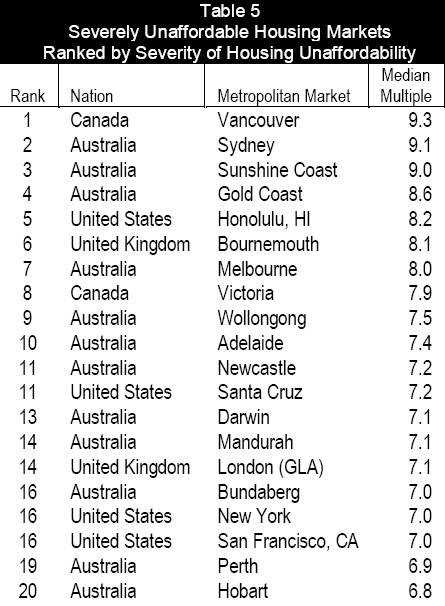

Least Affordable Cities

The article shows the top 58, I captured the top 20 above.

Congratulations To Canada And Australia

Congratulations go to Vancouver, Canada for being the least affordable city in the survey. Vancouver thus wins the gold medal in the individual competition.

Sydney Australia proudly wins the Silver medal and the Sunshine Coast Australia wins the bronze. It was close but no cigar for Australia's Gold Coast. Honolulu Hawaii came in a respectable fifth place.

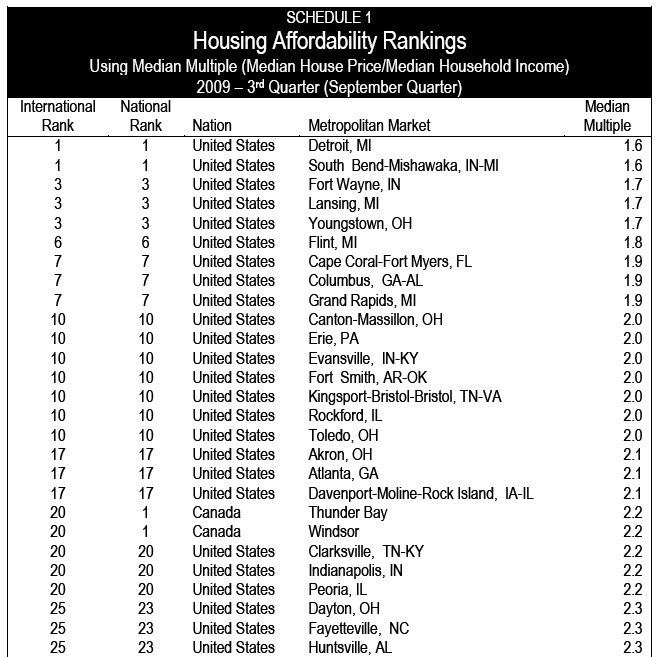

Most Affordable Cities

Detroit, South Bend, Youngstown, Flint, Toledo, Akron, Peoria, Cleveland, and many other "affordable" cities are not places where anyone would particularly want to live. Indeed many cities at the top of the affordability list are places that most would hope to escape from.

The high school graduation rate in Detroit is a mere 25%!

I am willing to bet that Detroit's graduation rate is far and away the worst of any city in the survey. See Michigan Forces Business Owners Into Public Sector Unions; Detroit's Aura of Hopelessness for more details.

Moreover, there are houses in Detroit, Cleveland, Flint, etc, that one could buy for $500 that have no takers. Unlivable houses no one wants at any price skew the results.

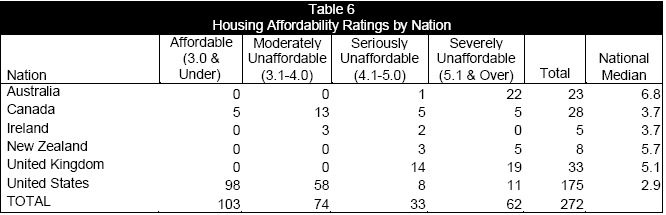

Demographia Summary by Nation

All of the affordable markets were located in Canada and the United States, while most markets in Australia, New Zealand and the United Kingdom were severely unaffordable.

Australia: House prices have continued to rise in Australia (Figure 2), which registered the worst housing affordability (the highest Median Multiple) in the history of the Survey. Overall, housing in Australia is severely unaffordable, with a Median Multiple of 6.8, more than double the 3.0 historic maximum norm. Housing had been affordable in Australia in the late 1980s, with a Median Multiple of under

3.0. The Median Multiple remained at or under 3.5 until the late 1990s.

All of Australia‟s major markets were severely unaffordable (Median Multiple above 5.0). Moreover, all markets, including smaller markets were severely unaffordable except Ballarat (Victoria), which was seriously unaffordable (Median Multiple between 4.1 and 5.0).

Canada: Housing is moderately unaffordable, as in previous Surveys. Canada‟s Median Multiple is 3.7. Housing had been affordable in Canada in the late 1990s, with a Median Multiple of 3.0. Canada had 5 affordable markets, 13 moderately unaffordable markets, 5 seriously unaffordable markets and 5 severely unaffordable markets.

Vancouver remained the least affordable market of any size in the surveyed nations, at 9.3, worsening from 8.4 last year. Toronto joined Vancouver as severely unaffordable, with a Median Multiple of 5.2. However, Barrie, within the Toronto region was moderately unaffordable, at 3.4. Victoria, Abbotsford and Kelowna (all in British Columbia) were also severely unaffordable.

Ireland: Housing in Ireland has become moderately unaffordable with a Median Multiple of 3.7, showing a trend toward historic norm of 3.0.20 Housing had been affordable as late as the middle 1990s, with a Median Multiple below 3.0. The extent of Ireland‟s recent housing affordability improvement is illustrated by the EBS/DKB Affordability Index, which indicates that mortgage payments have been halved in Ireland since the peak of the bubble in relation to first home buyer incomes.

New Zealand: Housing in New Zealand was severely unaffordable, with a Median Multiple of 5.7, nearly double the historic maximum norm of 3.0. Housing had been affordable in the early 1990s, with a Median Multiple of under 3.0. Auckland is the least affordable larger market, with a Median Multiple of 6.7, while Christchurch (6.1) and Wellington (5.7) were also severely unaffordable.

Tauranga-Bay of Plenty was again the least affordable market, with a Median Multiple of 6.8. Five of the 8 New Zealand markets were severely unaffordable, while Palmerston North, Napier-Hastings and Hamilton were seriously unaffordable New Zealand had no affordable markets and no moderately unaffordable markets

United Kingdom: Housing in the United Kingdom remains severely unaffordable, with a Median Multiple of 5.1, well above the historic maximum norm of 3.0. Housing had been affordable in the late 1990s, with a Median Multiple of under 3.0. Less than one-half of the United Kingdom markets were severely unaffordable (14 of 33), while the other 19 markets were seriously unaffordable. The United Kingdom had no affordable markets and no moderately unaffordable markets.

United States: Housing in the United States is rated as affordable, with the Median Multiple of 2.9.The recent house price declines have restored U.S. housing affordability to the below 3.0 historic norm (last achieved in the early 2000s), as the price bubble burst in many plan-driven markets. The United States had 98 affordable markets, 58 moderately unaffordable markets, 8 seriously unaffordable markets and 11 severely unaffordable markets.

The most affordable major market (population over 1,000,000) was Detroit. Other affordable major markets were Atlanta, Buffalo, Cincinnati, Cleveland, Columbus (Ohio), Dallas-Fort Worth, Houston, Indianapolis, Kansas City, Las Vegas, Louisville, Memphis, Minneapolis-St. Paul, Oklahoma City, Phoenix, Riverside-San Bernardino, Rochester, Sacramento, St. Louis and Tampa-St. Petersburg.Gold, Silver, Bronze Medals

In terms of national unaffordability (the team competition) Australia wins the gold medal, New Zealand, the silver medal, and the UK wins the bronze medal.

Because of a preponderance of "affordable" cities in the US and the way the national rankings are made, I question the results of the national survey although it likely did not affect the top three medal-winning rankings.

Email Exchange With Survey Developer

I had this exchange with Hugh Pavletich of Performance Urban Planning who helped develop the survey.

Mish: When you come up with "national affordability" are all the cities given equal weight? Does Detroit count as much as San Francisco?

Hugh: Yes.

Mish: In my opinion, a weighted average is what matters most (at least for the purpose of figuring out how big the bubble still is).

Hugh: We are NOT attempting to explain how big the bubble is on a country wide basis. We are simply illustrating what the Median Multiple is at the 3rd Qtr of each of the urban markets listed.

Other researchers are most welcome of course to take the next step and do a population weighting, if they wish to do so.

Our goal is simply to illustrate the degrees of housing stress of the urban markets listed.Bear in mind my goal is quite different than Hugh Pavletich's. He wants to show the role local planning rules have in affordability. Hugh makes a case that local zoning rules play a huge factor on a city by city affordability basis while I am concerned with "How Big Is The Bubble?"

From my perspective, the US and Canadian bubble problems are very understated, and the national affordability rankings of the US and Canada are thus overstated. To be certain, one would have to take a weighted average of populations and rankings. One would also need to take into consideration unlivable houses offered at $500 that no one would take. If one did that, we would see the bubbles are where the most people live.

There is much more in the survey. Please give it a look.

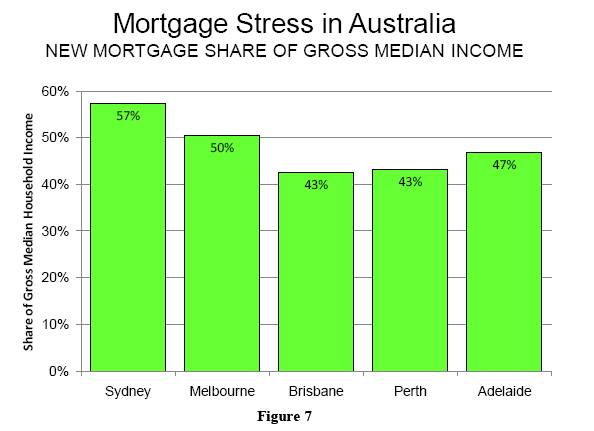

Mortgage Stress in Australia

If this chart does not scream "nationwide bubble", nothing ever will.

Australian Interest Rate Hikes

On December 2, the Reserve Bank of Australia hiked rates to 3.75%.

At its meeting today, the Board decided to raise the cash rate by 25 basis points to 3.75 per cent, effective 2 December 2009.

With the risk of serious economic contraction in Australia having passed, the Board has moved at recent meetings to lessen gradually the degree of monetary stimulus that was put in place when the outlook appeared to be much weaker. These material adjustments to the stance of monetary policy will, in the Board’s view, work to increase the sustainability of growth in economic activity and keep inflation consistent with the target over the years ahead.Let's come back to that last paragraph a year from now. Two years from now it is likely to look downright silly.

One more hike is in the cards, too, on February 2. Some will lay the blame on what is about to happen on these last couple hikes. The reality is the blame for the coming bust lay in the ridiculous expansion of credit that preceded it.

Australia's problems have not yet started. Remember too, that commercial real estate follows residential with a lag. Australia can look forward to a bust in commercial real estate down the road as well.

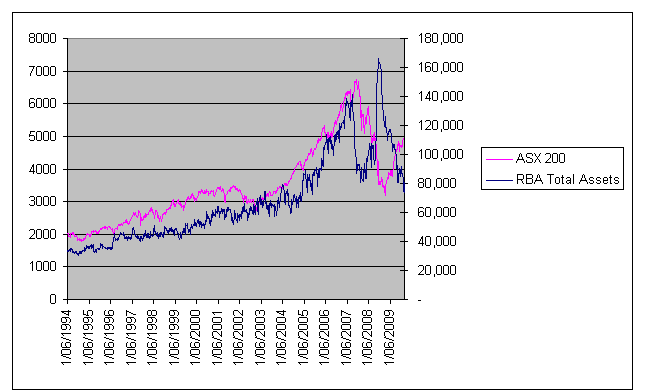

Email From "Down Under"

Here is another email from Australia that readers may appreciate.

"Down Under" Writes ...

Mish,

I actively watch this chart and a colleague of mine updated it today. RBA balance sheet collapsed in early part of 08 ahead of the debacle.

Add this to the recent report of Sydney being second most expensive city in the world. And add in likely tightening of bank prudential standards by our regulator APRA (extend liquidity requirements out to 21 days) and not looking so pretty. Deja vu all over again.

You can get the data straight from the RBA on the web: RBA Liabilities and Assets - Weekly

Kind regards,

"Down Under"

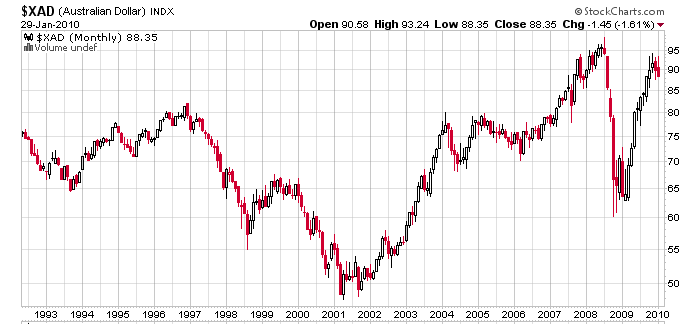

Australian Dollar Outlook

Two of the biggest factors affecting currency fluctuations are interest rate differentials between countries along with trends in interest rate differentials. The latter is more important. The Fed clearly is not going to cut rates (at zero bound it can't).

The Australian dollar has strengthened vs. the US dollar on the back of rate hikes. If the RBA hikes once more and the Australian dollar sinks anyway, the top is likely in.

$XAD Australian Dollar vs. US Dollar Monthly

Déjà vu all over again?

At some point the RBA will stop hiking and start cutting. In turn, speculators in Australian dollars will start taking profits. At a bare minimum, at least a fair sized pullback in the Australian dollar vs. the US dollar is likely.

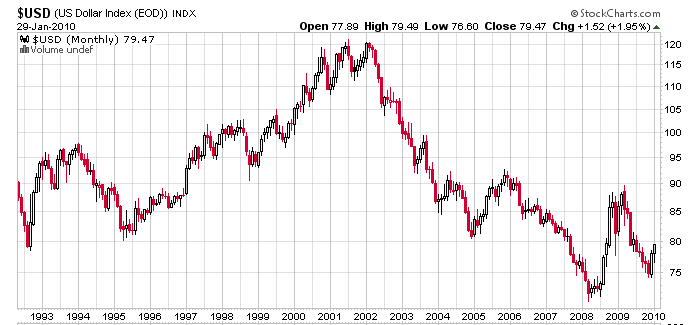

$USD - US Dollar Index Monthly Chart

Most underestimate how far the US dollar can strengthen. Another run at 90 is certainly not out of the question.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.comClick Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2010 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.