UK Housing Market Crash of 2007 - 2008 and Steps to Protect Your Wealth

Housing-Market / UK Housing Aug 22, 2007 - 01:59 AM GMTBy: Nadeem_Walayat

The Credit Crunch has been hitting the UK Mortgage Sector hard as many easy credit mortgage deals have been removed from the high street shelves in recent weeks. Despite central bank actions to ease financing terms and increase liquidity, this does not address the real issues of illiquid mortgage related bonds and expectations that the UK Housing Market will slump on the back of a surge in foreclosures.

The Credit Crunch has been hitting the UK Mortgage Sector hard as many easy credit mortgage deals have been removed from the high street shelves in recent weeks. Despite central bank actions to ease financing terms and increase liquidity, this does not address the real issues of illiquid mortgage related bonds and expectations that the UK Housing Market will slump on the back of a surge in foreclosures.

UK Mortgage Banking Sector - Northern Rock Example

For an example of the credit crunches impact on the UK mortgage banking sector , we need look no further than at Northern Rock. The mortgage banks stock price has fallen from recent highs of £12.58 to recent lows of just £6.20, a drop of more than 50%. Trading on a PE of just 7.5 and a yield of 4% may now make the stock seem enticing, but the mark down is in anticipation of the much higher risk of mortgage defaults and repossessions in the UK as the housing market starts to nose dive. These repossessions (foreclosures) are already hitting the likes of northern rock with expectations of a tripling in the rate over the next 6 months as compared with the same period last year. This surge in repossessions will impact the earnings of the UK Mortgage banks as they make every larger bad debt provisions and issue profit warnings.

This is in addition to any toxic US Sub prime related exposure. Therefore in Northern Rock's case a PE of 7.5 could jump many fold in a worse case scenario.

UK Adjustable Rate Mortgages (Arms) & Liquidity

If the Adjustable Rate Mortgage Resets are termed as Arm-ageddon in the US, then here in the UK they should be termed as Doomsday, as the more than 90% of ALL mortgages are adjustable rate or floating rate mortgages in the UK. The short-term fixed deals taken out over recent years are now resetting with a vengeance. With UK interest rates at 5.75%, and a chance (albeit diminishing one) of a further rise to 6% in October 2007 (UK Inflation CPI Falls But Interest Rates Set to Rise to 6% By October 2007 18th July 07). The UK Arm resets will have a significant impact on the UK consumer and send the UK Housing market into a downward spiral. To make matters worse the credit crunch ensures that lending criteria will be much stricter with much higher interest rates charged than the base rate would imply, i.e. a greater spread between the Bank of England's rate and the mortgage interest rates.

Already the latest figures for new mortgage approvals for July show a 27% fall over the same period a year ago as liquidity continues to tighten with borrowers facing much tougher refinancing conditions.

The third impact of the credit crunch on the UK Housing market is the loss of 'city bonuses'. If as expected the financial markets remain depressed for at least the next quarter then the year end bonuses may virtually dry up. In the City of London many of the house purchases are reliant on bonuses to pay off capital as mortgages tend to be many, many times salaries. If the bonuses fail to materialize then that will depress London House prices which will send another negative ripple through the whole UK housing market.

Uk Repossessions (Foreclosures)

UK home repossessions continue to soar this year and are forecast to total as much as 34,000 by year end, which is double the number of 2006 of 17,000. Going into 2008 we could be seeing repossession not seen since the last housing bust of the early 1990's. The mortgage banks such as Northern Rock are being hit hard, which reported a doubling in the rate of repossessions. The impact of this will mean even tighter borrowing requirements and a similar squeeze on house prices led by sub primers as has occurred in the US. Where expectations are extremely tight credit for those with poor credit histories.

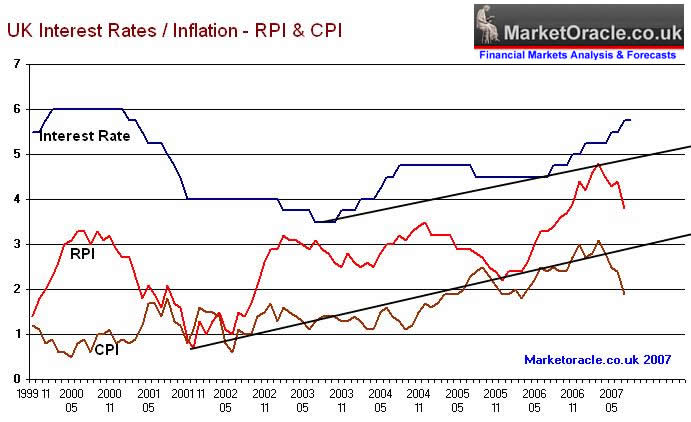

Uk Inflation RPI / CPI / Interest Rates

The Rate rises from 4.5% to 5.75% in a year are having the effect of dissipating the bullish sentiment that has carried UK house prices to such extremes.

The latest Inflation figures fell strongly in July, with the CPI dropping from 2.4% to 1.9% and the RPI falling to 3.8% to 4.4%. However given the extent of the rise in the money supply, further declines are likely to be more muted. The chart trend suggests RPI could decline towards support at 3%.

This is enough to keep UK interest rates on hold for the time being, which increases the probability that interest rates may now peaked, as by the time the UK Housing market nose dives and the economy slows to borderline recession, a further rise in interest rates will no longer be on the cards and infact the expectations will be for cuts in UK interest rates.

Interest Rate Conclusion - The Market Oracle expectations are for UK interest rates to target 5% during the second half of 2008.

Buy to Let Sector

The Buy to let sector continues to expand strongly with a record number of buy to let mortgages taken out during the first 6 months of the year despite the rising interest rates and falling rental yields. The result is an increasing number of buy to let investors unable to cover their mortgage repayments from rents and therefore are relying on capital gains to provide profits. Should, as expected house prices take a tumble then a mad rush by weak buy to let investors to cut losses could hasten the decline in UK house prices during 2008.

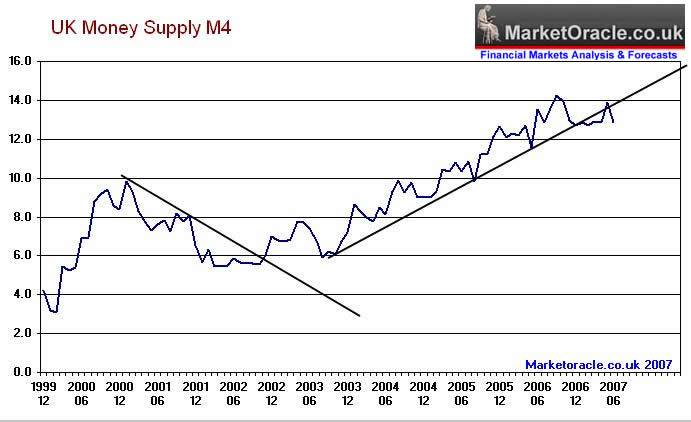

UK M4 Money supply

UK Money supply growth shows signs of having peaked at 14%, however, whilst the money supply remains at the elevated rate of 12.9%, this still suggests higher inflation in the future. And would require a much more significant reduction to below 10% before inflationary pressures are expected to ease.

The Market Oracle UK House Price Ratio

The above chart clearly shows that despite the strong rise in house prices from 1996 to 2006, house prices remained affordable in terms of earnings and historically low interest rates which enabled house buyers to meet mortgage repayments.

However this year the ratio clearly broke above the upper range and has led to an increase in relative costs of servicing mortgages to an extent not seen since 1992. This will become more evident as the impact of mortgage fixes taken out when interest rates were at or below 4.5% expire as the increased risks in the mortgage sector result in ever higher floating rate mortgages, especially for those deemed to be if higher risk with poor credit histories, who may see their mortgage interest rates double i.e. from say 4% to more than 8% !

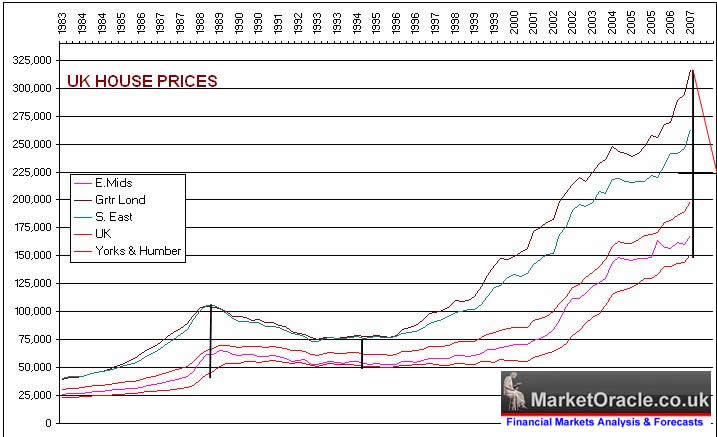

UK House Prices

London and the South East led the way during the 1980's Boom, rising much further than the rest of the country, with the rest of the country continuing to rise as London peaked.

Similarly today, the South of England has risen to a much greater extent than the rest of the country, and thus is expected to fall especially hard given the credit crunch in the city of london.

The resulting bear market will undoubtly seek to contract the spread between London and the rest of the country by at least 50%. Which implies a decline of 30% in the Greater London Area, and an overall UK decline of some 14%. however the decline in real terms when inflation is taken into account will be much greater.

UK Housing Market Conclusion:

The UK Housing market is expected to decline by at least 15% during the next 2 years. Despite the 2012 Olympics, London is expected to fall as much as 25%. UK Interest rates are either at or very near a peak, as there is an increasingly diminishing chance of a further rise in October 2007. After which UK interest rates should be cut as the UK housing market declines targeting a rate of 5% during the second half of 2008. The implications for this are that the UK economy is heading for sharply lower growth for 2008.

What to Do ?

1. Home Owners - If you are thinking of selling your home then the time to act is now ! Waiting whilst the credit crunch continues to tighten is a big mistake, especially given the fact that further sharp falls are in the financial markets are just around the corner.

2. Cash - Invest in Fixed Interest Bonds issued by large strong banks , avoid issues from mortgage banks such as Northern Rock. Keep in mind that In the UK savers have protection at 90% of holdings of the first 35k of investments in fixed bonds and savings accounts so bare that limit in mind. Also ensure you have used up your Tax Free ISA allowances.

3. Government Bonds - Invest in Government Bonds, be prepared to hold to maturity so as to reduce risk of market volatility.

4. Government Certificates - Invest in national Savings Certificates such as the and Index Linked Tax Free Certificates, which are an excellent vehicle for higher rate tax payers.

5. A Stock Market Crash or Slump Would be A Buying Opportunity. The stock market is expected to be volatile since we are moving into a new risk climate. Despite a high probability of further sharp falls, and even a crash, there are plenty of long-term plays out there especially in the big cap oil sector. I would also look at bargain hunting metals and mining on further sharp falls or a crash. Similarly for the utilities sectors such as Water. The best plays are probably via investment trusts, of which there are many. I favor investment trusts over unit trusts as they are traded on the stock exchanges exactly as any stock is. Whereas, as I recall in previous financial crisis you may find the phone off the hook on the other end of the line when you try to call to buy or sell unit trust positions.

6. Emerging Markets - I would avoid china, the market is not pricing in risk and is primed for a crash. India and Russia look enticing especially on any sharp falls in sympathy to global market sell offs.

Whatever you do, remember that today's Idyllic pleasant picture in the UK is very shortly in for a rude awakening, much as the US home owners are experiencing in increasing numbers. The bull market in housing is over for now, better to realize this now whilst you have the opportunity to do something about it rather than be forced into a decision later on.

Related Articles

- Hedge Fund Sub prime Credit Crunch to Impact Interest Rates - 31st July07

- UK Housing Market Heading for a Property Crash - 1st May 07

- UK House Prices continue to Rise whilst the US Housing Market Slumps - 25th Feb 07

- UK Housing market forecast for 2007 - 31st Dec 06

- Why UK House prices continue to rise ! - 14th Oct 06

By Nadeem Walayat

(c) Marketoracle.co.uk 2005-07. All rights reserved.

The Market Oracle is a FREE Daily Financial Markets Forecasting & Analysis online publication. We present in-depth analysis from over 100 experienced analysts on a range of views of the probable direction of the financial markets. Thus enabling our readers to arrive at an informed opinion on future market direction. http://www.marketoracle.co.uk

This article maybe reproduced if reprinted in its entirety with links to http://www.marketoracle.co.uk

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any trading activities.

Nadeem Walayat Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

Ron Kennor

22 Aug 07, 17:15 |

UK House Prices

The USA is currently facing a slump in house prices caused by poorer home buyers defaulting on their ‘sub prime’ mortgages. These are home loans, normally at a higher than usual rate of interest, given to purchasers with a bad credit record. As prices slip down and personal equity in the property drops then the temptation for these borrowers to walk away from the debt and hand in the keys becomes a logical decision – especially for those who already have a bad credit rating which cannot be wrecked by repossession. With interest rates rising and the sources of easy mortgages drying up, or in some cases going bust, whilst their may be a huge pool of prospective buyers in America, if no one wants to lend them money they cannot buy and the market slips further. Add to this the easy availability of building land and the rapid American construction techniques and you have an oversupply with insufficient demand - a complete reverse of our present situation here. All this nervousness has spilt over into our stock markets but not,at least the time of writing, into our property market which remains ever robust and increasingly expensive despite promises of ‘affordable’ homes to come. But we too have our Sub Prime mortgage market which has enlarged enormously over the last 10 years and has forced many of the high street lenders to ease their formally strict lending criteria. The once rare ‘self cert’ mortgage has become a common way for lenders to turn a blind eye to whether a borrower can really afford the payments. Both lender and borrower are shielded by a rising market as the value of the house normally covers the loan and any arrears if the house has to be sold, but when prices are falling it’s a different story.

In the UK market we now have many buy to let investors and if negative equity occurs these will be the first to accept repossession as a business decision as, unlike the locked in owner occupier ,they wont need this particular roof over their head. But this is a worst possible scenario which is unlikely to occur, there will be no crash here as our offices, despite the holiday period, are still reporting huge numbers of buyers chasing too few houses for sale and our mortgage providers still have plenty of money to lend to the right customers. Ron Kennor is General Manager of Robinson Jackson Estate Agencies 020 8316 6200 |

|

JOHN R

22 Aug 07, 18:27 |

UK Housing Crash

Nadeem, Re your fascinating article on a UK Housing Crash 2007/08. Hypothetically, if you currently held cash (NOT bonds) with Northern Rock in a high interest rate savings account would you be inclined to transfer your cash with them to a savings account with another bank? As a matter of interest which banks do you currently regard as "large strong banks"? We will not,of course, know for some time to come which UK banks---large or otherwise--- have been particularly badly hit by their exposure to CDOs. Out of the frying pan into the fire? John R |

|

Nadeem_Walayat

22 Aug 07, 18:39 |

UK Crash and Banks

When the stock price of a bank falls by 50% in a few weeks, that is telling you something. And you should take note. In the UK the first 35k of your savings are protected upto 90%. Infact the first £2k is protected at 100%. So even in a worse case scenerio, unless you have more than £35k invested you would not go broke. I would avoid banks with big mortgage books such as United Trust Bank, Bradford and Bingley and Northern Rock etc. Even though its been a longtime since a UK bank went bust, there is a better than 50/50 chance that some UK mortgage banks will go bust during the next housing bust. The big Banks I am talking about are Barclays, Nat West, HSBC etc. And you could include HBOS, even though they have a significant mortgage book, though probably in much better shape than Northern Rocks. But which ever banks you choose, always follow the rule of not putting total savings of more than £35k with any bank. Eventhough we are some way away from any UK bank going bust, but as we saw with the hedge earlier funds collapse, by the time the public are aware, its usually too late to draw your savings out !!! |

|

Malcolm C

23 Aug 07, 05:11 |

Migration - impact on housing market

Great assessment. One factor I see often ignored is the migration factor. We hear that the number of immigrants entering the UK has contributed to house price inflation. If the economy turns sour, is it not possible that this tide may reverse, as immigrants take their money back home to their relatively booming emerging economies? Would this not exacerbate the fall in the housing market also? What are your thoughts? |

|

DrBubb

27 Aug 07, 03:03 |

Are the Builders signaling a 2008 UK Property Crash?

Shows the amazing power of a widely-believed dream - A bubble-forming mania. But when they burst, they tend to fade rather fast, as the US is showing. Here's a link to a Video, showing the predictive power of the UK builder share prices: "Are the Builders signaling a 2008 UK Property Crash?": http://www.youtube.com/watch?v=iNeCetQeLLU |

|

Alexander

27 Aug 07, 12:52 |

UK Housing market

The housing market, surprise-surprise, will not crash and the downfall will be short even if painful. Don't rush to sell, however, as by the time you would like to enter it again you would find the prise rose! Some people sold their London home for £1m some 6 years ago and then later had to fork out £2m for the same house. Read |

|

Jim

29 Aug 07, 15:03 |

US housing affects UK housing and world

In order for home sales to rise in the USA, salaries must be rising equally fast, from now on. Since inflation of 13% and higher will eat away at the US economy, due to unlimited war spending, salaries will stay the same, and unemployment will rise (stagflation). Corporate profits from war are now being held for future earnings. What happens to the US housing market affects the entire world economy. |

|

Tony Mosantee

19 Nov 07, 19:02 |

housing crash

Fasten your seat belts because we are going head on for a housing crash. |

|

jennifer A.

17 Dec 07, 20:20 |

House Prices crash!

Spot on Nadeem ! house prices in London crashed accoridng to rightmove dow nearly 7% in one month to mid december. Things are really starting to look very bad and fast! So you think the UK will be able to avoid a recession during 2008 ? |

|

Emete Wanogho

02 Oct 08, 09:26 |

Lack of Mortgage Supply

The fact that the level of mortgage available to both first time buyers and existing home owners is now very difficult to get means that the impact of the down turn in the housing sector will continue to bite far longer than originally predicted. Not to mention the gloomy state of the economy- rises in food price, rises in petrol, and the fact that more people are forecasted to lose their jobs, especially in the finanacial sector, makes for a very gloomy future prospect indeed. The housing market cannot be helped, nor will house prices stop falling if there are no suitable mortgage products available to attract the first time buyers to kick-start the housing market. How can this be if first time buyers, are expected to put down in excess of twenty percent deposit, and in some instances, they demand even more and as well as expecting the would-be mortgagee to possess impeccable credit history. In these days where the slightless thing is used against borrowers, I hate to say that the housing market will take at least five years to recover. |

|

Nadeem_Walayat

24 Sep 09, 21:48 |

UK House Prices and Unemployment - Update Aug 09

This is the first in a series of analysis as part of an in depth up-date to the UK house price forecast of August 2007 that correctly called a peak in UK house prices and forecast a 2 year bear market that would see UK house prices fall by 15% to 25%. This analysis seeks to compare UK house prices against unemployment data. To ensure that you receive the full final analysis and conclusion / forecast for the UK housing market covering the trend for the next 2-3 years subscribe to my always free newsletter. UK Unemployment Data I have long questioned the accuracy and validity of the official unemployment data which over several decades and much manipulation by successive governments has been tweaked many hundreds of time to under report true unemployment for political purposes. Current official unemployment stands at 2.435 million for May data release against which the total are recorded as economically inactive of working age stands at 7.955 million which in my opinion is reflective of the true rate of unemployment as the below graphs illustrate.

Another poignant reminder of the lack of accuracy in the unemployment data is observed in the announcement today that now 1 in 6 house holds have no wage earner, i.e. all adults are unemployed in a total 3.3 million households, which clearly suggests a number of unemployed significantly above the 2.435 million official data of those unemployed. UK Unemployment Data Forecast The original forecast of October 2008 (July 08 data) as illustrated by the below graph, forecast UK unemployment to hit 2.6 million by April 2010. The actual data to date of 2.43 million to May 2009 clearly continues to suggest a much higher peak which remains on track to hit 3 million, as unemployment tends to lag economic recoveries by anywhere from between 6 to 12 months. UK House Prices Against Unemployment Trend Analysis

The above chart indicates that there does exist a strong relationship between house price trends and the unemployment benefit claimant count, more so than the unemployment data. The possible reason for this is that those made unemployed that do not claim benefits are not in as financially distressed state than those that have no choice but to claim benefits, therefore house prices can and have risen in the past whilst the official rate of unemployment rose, if at the same time the claimant count did not rise. The recent bounce in house prices is tracking quite closely with the stabilisation of the unemployment claimant count numbers, which therefore suggests that as long as those claiming unemployment benefits continues to stabilise at the current level of 1.6 million then the outlook remains positive for UK house prices to continue drifting higher, this is despite official unemployment data that looks set to continue to rise towards 3 million from 2.43 million. Existing UK House Prices Analysis and Forecast As mentioned earlier the original forecast of August 2007 concluded with a forecast drop in UK house prices of between 15% and 25% by August 2009, which has materialised. August 2007 Forecast Conclusion - The UK Housing market is expected to decline by at least 15% during the next 2 years. Despite the 2012 Olympics, London is expected to fall as much as 25%. UK Interest rates are either at or very near a peak, as there is an increasingly diminishing chance of a further rise in October 2007. After which UK interest rates should be cut as the UK housing market declines targeting a rate of 5% during the second half of 2008. The implications for this are that the UK economy is heading for sharply lower growth for 2008. This has been supported by over a hundred pieces of analysis on the UK housing market with several warnings not to pay any attention to the vested interest as they continued to remain in denial right upto the summer of 2008 with announcements such as that of a soft landing or that house prices would not fall, as Sept 07's article illustrated - UK Housing Market on Brink of Price Crash - Media Lessons from 1989! UK Housing Market 2008 Crash Trigger - Following the peak in UK house prices, the initial trend was inline with the original forecast, however it was recognised following Northern Rocks bust that the pace of deterioration of credit markets as well as the capital gains tax changes as implying that the UK housing market's rate of decent would start to accelerate from April 2008 and could be termed as a housing market crash - November 2007 - Crash in UK House Prices Forecast for April 2008 As Buy to Let Investors Sell. - The timing for the sharp drop is likely to coincide with Labour's change on capital gains tax which effectively cuts the tax payable on gains accumulated over the last few years to 18% from 40%. This tax change comes into force on 1st of April 2008 and thus the expectation is for an avalanche of selling amongst buy to let investors to lock in profits. This also means that the market will to some degree be artificially supported going into April 08, but still will not be enough to prevent a wider decline in UK house prices but rather could register a drop of as much as 5% in the quarter April 08 to June 08 , which would represent a crash in UK house prices. July 2008 - UK House Price Crash In Progress! - The summer months subsequently witnessed the crash in UK house prices come to pass as house prices look set to full fill the original forecast for a 15% fall well ahead of the original time line with the risks that despite soaring inflation data, the housing bear market threatened imminent deflation, which has now increasingly become the mainstream story which was originally highlighted in the analysis of March 2008. January 2009 - UK Housing Market Depression Forecast - In depth analysis of 4th January 2009, forecast a continuing crash that would morph into a prolonged depression for several years that despite containing bounces, that house prices were unlikely to see a final bottom until late 2011 / early 2012 as the below graph illustrates. March 2009 - House Price Bounce Warning Signs- The mainstream press as epitomised by the Telegraph ran with a ridiculous story that Uk house prices could fall by another 55%, which prompted analysis that concluded that the forecast for a possible another 55% fall in UK house prices EXTREMELY unlikely. If anything the extreme measures of zero interest rates and quantitative easing implied a far shallower trend that suggested a stagnating market rather than anything like another 55% drop.

Summer Bounce 2009 - The unfolding bounce or blip in UK house prices prices is inline with my May analysis that concluded that UK house prices will experience a bounce during the summer months from extremely oversold levels as a consequence of liquid buyers returning to the market and the debt fuelled economic recovery which 'should' be reflected in rising house prices during the summer months that is increasingly being taken by the mainstream press and vested interests to announce that the house prices have bottomed. My next analysis will compare UK house prices to the GDP growth rate. To ensure that you receive the full final analysis and conclusion / forecast for the UK housing market covering the trend for the next 2-3 years subscribe to my always free newsletter. By Nadeem Walayat http://www.marketoracle.co.ukCopyright © 2005-09 Marketoracle.co.uk (Market Oracle Ltd). All rights reserved. Nadeem Walayat has over 20 years experience of trading derivatives, portfolio management and analysing the financial markets, including one of few who both anticipated and Beat the 1987 Crash. Nadeem's forward looking analysis specialises on the housing market and interest rates. Nadeem is the Editor of The Market Oracle, a FREE Daily Financial Markets Analysis & Forecasting online publication. We present in-depth analysis from over 300 experienced analysts on a range of views of the probable direction of the financial markets. Thus enabling our readers to arrive at an informed opinion on future market direction. http://www.marketoracle.co.uk Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any trading activities. |

|

Frank.Fagan

28 Sep 11, 14:40 |

Oil Prices

Nadeem Followed your articles for a while and you know a lot more than me and have called a lot of things correct. Got myself in a bit of a hole with some AIM shares instead of taking your dividend paying shares advice. Just hanging in here and hoping Oil can recover and lead my portfolio forward.What are your opinions on future oil prices. If in your knowledgable position you come across any risky but rewarding shares please let me know. Thanks |