Real Story Behind Last Week’s Stock Market Panic

Stock-Markets / Stock Markets 2010 May 10, 2010 - 05:51 AM GMTBy: Money_Morning

Thursday's U.S. stock market trading session qualified as a genuine stock-market "panic." They're rare, fortunately, so they're memorable.

Thursday's U.S. stock market trading session qualified as a genuine stock-market "panic." They're rare, fortunately, so they're memorable.

You can say you were there.

According to the volume analysts at Lowry Research Corp., this stock market panic was on par with the mini crash of October 1989, when the Dow Jones Industrial Average plunged 6.9% in a single day. But it wasn't on par with the famed session of October 1987, when the Dow plunged 22.6% in a day.

Last week's stock market panic wasn't merely intense - it was also heavy, with 10.5 billion shares trading changed hands - 53% greater than the average.

But Thursday's trading session was part of a tough week, overall.

Stocks fell like dominoes over the past week as forced selling by big hedge funds responding to margin calls, panicky selling by people who watch too much TV during the day, and a gremlin in the algorithmic trading systems overwhelmed the exchanges and common sense. The result - highlighted by a truly horrid high-frequency-trading session on Thursday - was five sessions dominated by headless chickens and bottomless anxiety.

The major U.S. indexes fell 6.3%, the Nasdaq 100 Index fell 7.7% and overseas large-caps fell 9.2% during the week, while certain high-beta emerging markets like Indonesia and Turkey fell 12% to 14%.

Breadth was heavily negative as 90% of trading was in falling stocks on four separate days in the past two weeks. Losers outpaced advancers by a ratio of 6-to-1. The least-worst sector was healthcare, down 5.5% for the week, while the worst was basic materials, down 9.2%. Everything else was on a spectrum from coyote ugly to shield-the-children's-eyes.

There was a lot of chatter about a "fat finger" incident - or something worse - that caused the Dow Jones Industrial Average to fall nearly 1,000 points on Thursday. Conspiracy theorists had a field day with rumors about a trader at a major brokerage accidentally selling a "billion" S&P e-mini futures instead of a "million," and about the possibility of cyber-terrorism - all right up there with UFOs and Elvis sightings.

Maybe those things happened, or maybe they didn't. But it really doesn't matter. Mistakes are a part of life. The fact remains that a market correction was due after a scorching run higher. As we've been saying for weeks, stocks were like a can of gasoline just waiting for a careless match to be flicked in.

The investigations are still under way, but so far it looks like computer trading systems just choked on a lot of "sell" orders arriving at the same time and blew a fuse, allowing some big stocks to free-fall, which kicked off a lot of stops, which kicked off more sales. There will be Congressional hearings and Securities and Exchange Commission (SEC) soul-searching, but I don't think they'll find a single smoking gun. It was sort of like the Toyota Motor Corp.'s (NYSE ADR: TM) with runaway accelerators: One part human error, one part system failure, one part mystery.

Call it "Revenge of the Robots."

And that brings us back to Thursday.

A high-volume, high-intensity plunge normally results in a "capitulation," or a session in which selling becomes exhausted, leaving a vacuum into which buyers rush. That selling was more than likely not completed on Thursday because of confusion over what exactly happened continued to reign.

More forced sales from margin calls kicked in on Friday, and it would not surprise me at all to learn that some big hedge funds might have been forced to liquidate. If you have several funds with $2 billion in real money that is leveraged at a ratio of 5-to-1, and they get margin calls, they might have to sell $10 billion in securities all at once in an illiquid market. That creates more havoc.

These things cannot be resolved quickly. The last time this happened, it took from October 2008 to February 2009 before all these issues were resolved.

Stocks are now very oversold and overdue for some bargain hunting among individuals and buybacks among corporations. Companies like International Business Machines Corp. (NYSE: IBM) that regularly buy back shares are usually heavy purchasers in the wake of a wipeout like Thursday, as are corporate insiders.

It doesn't take much of a spark of buying to persuade others to come in behind them, so they act like the first wave of infantry. A 90% upside day would set a firm bottom. A weak rebound or further weakness would set the stage for a return for a close at least at the Thursday low and at worst the February lows.

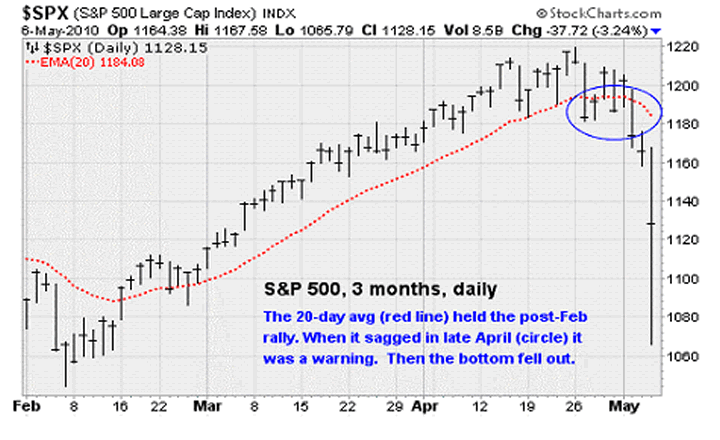

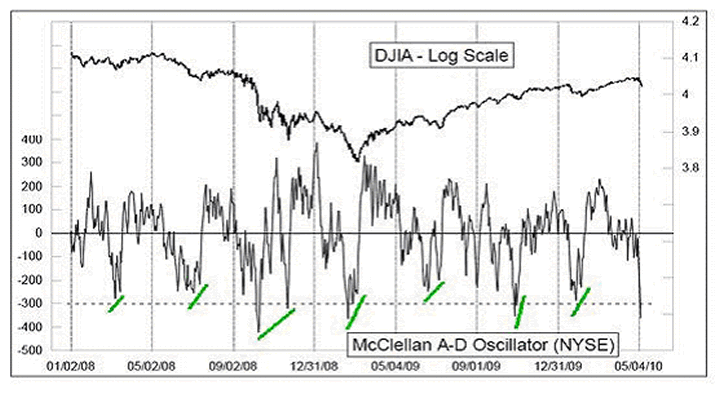

One way to measure an oversold condition is to look at the McClellan Oscillator, shown above. Tom McClellan, whose parents created the famed oscillator for just this purpose, reported Thursday that the New York Stock Exchange (NYSE) saw 2,849 net declining issues at the close, which pushed the oscillator to (-358.6, which is very low. Any reading below -300, he says, is "exceedingly extended," and it doesn't matter if it's -320 or -360.

"It's like the difference between falling off a 19-story or a 21-story building," McClellan said to me. "Architecturally, there is a difference, but it does not matter much when you hit the sidewalk.''

Minus-300 rarely occurs alone, and it's the second one that occurs at a slightly higher low, creating a divergence, that marks the final bottom. That's what the green lines in the chart above are highlighting. He does a lot of great cycle work, and is looking for a final low next week, May 11-14.

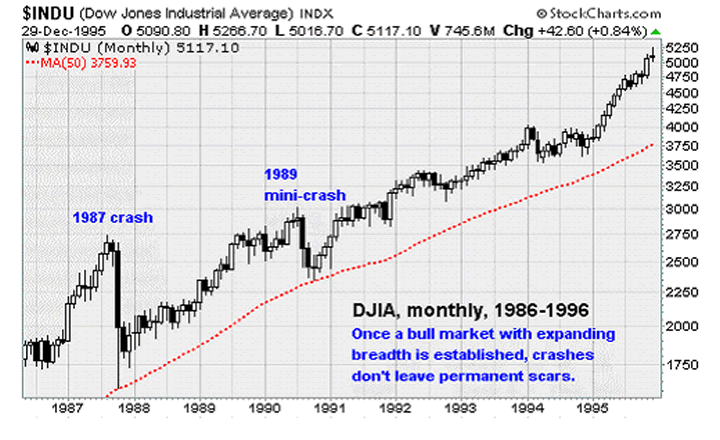

Either way, since breadth was strong and making new highs going into this unpleasantness, the odds are high that ultimately this will look like a serious but insignificant bump on the way toward new highs. Back in 1987, it took two years to get back to the old high. In 1989, after a worse sell-off than Thursday, it only took three months to get back to a new high, as you can see above.

In a new bull cycle, these declines are all about resetting the deck on valuation and blowing the froth off the top. I don't mean to sound like Pollyanna, because there are plenty of very serious problems in the world that can derail investors, spook them into bonds for a long time and basically kill the bull cycle that started in March 2009. But the titanic wave of fiscal and monetary liquidity supplied to the global financial system over the past year is unprecedented in scope and will have long-lasting consequences. All that money has to go somewhere, and it usually goes into productivity-creating risk assets.

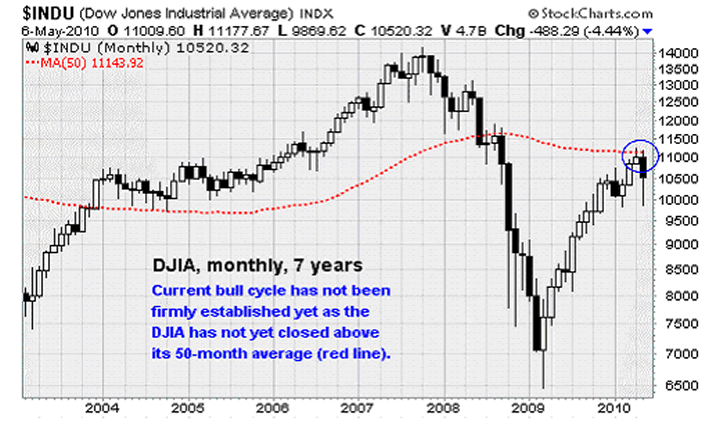

When the two big setbacks occurred in the late 1980s, the bull cycle was already five years old, having started in 1982. The current cycle is just barely a year old, and has not yet become fully established with a close over its 50-month or 200-week average. It's being tested right now in a big way. If it gets over this hump in the next couple of months, closing over the 11,145 area at the end of month, we'll know more about the cycle's potential longevity.

The Tuesday Spark

Now let me tell you what I am hearing hedge-fund managers, prop-trading-desk managers and other public fleecers that I am in contact with. Thursday has caught everyone's attention, but crashiness began on Tuesday. Here's why:

•The U.S. session only began to accelerate downhill on Tuesday when a wire story emerged out of Berlin that the Bundestag is working on legislation that would bar Germany from contributing to a financial bailout of any other European Union country besides Greece. That news helped credit bears to launch a renewed assault on Spanish, Portuguese and Greek bonds.

That mattered because a couple of major hedge funds are said to have borrowed heavily to load up on high-yield Greek debt over the weekend in anticipation of the EU deal. The attack on that debt on Tuesday was so successful that the unfortunate hedge funds received margin calls, which forced them to raise cash quickly. They had to sell both their new debt positions at big losses and to dump a wide variety of other holdings, such as oil, gold and stocks. This explains why oil crashed $4, seemingly out of the blue, at a time when supplies were actually constricted due to the Gulf of Mexico drilling rig disaster.

-- This is how contagions get rolling. I've said this before but I'll say it again: It's not the sovereign debt sellers (i.e. Greece) that cause the problem. Trouble arises when overleveraged debt holders (i.e. fund managers) must puke out their most liquid positions in other markets to make margin calls.

-- One prop desk manager laid the blame for Tuesday's losses on these issues: a) Doubts that the $110 billion EU aid package for Greece will be sufficient; b) doubts that EU member parliaments will pony up for any large Greek bailout; c) fears that a bailout package for Spain would amount to $350 billion later this year; d) fears that European banks that hold Greek debt will suffer massive losses even if the bailout occurs, which is why their credit default swaps widened to 209 basis points from 109 bps in the past few days; e) surprise that Hong Kong and German purchasing managers' indexes missed expectations badly; f) surprise that a record amount of commercial mortgage backed securities were reported in delinquency by Realpoint; g) fears that German elections to be held Sunday will rile markets as populists rage against contributing to the Greek bailout.

What's the next flash point? Well, global margin calls take awhile to play out, and are not pretty. They feed on themselves, growing worse as they circle the globe. Fund Manager A who is forced to sell Greek debt, oil and gold can cause an otherwise innocent Fund Manager B to discover his own leveraged position in gold and oil compromised, and so he is compelled to sell stocks; the sale of those stocks may force leveraged stock Fund Manager C to sell his most liquid positions. Rinse and repeat. As this circle intensifies, banks may pull credit lines to make sure that their own reserve ratios remain within legal limits.

Now here's where it gets really tricky. Private citizens and companies with lots of euros in European banks that have a lot of exposure to Greece, Spain and Portugal may decide to move their money to more stable banks in Germany and the United Kingdom. That causes the most worrisome banks to get out of synch with their reserve ratios (balance of deposits to loans), which can force them to call in loans, borrow more heavily from central banks, and generally create a nuisance. This is why the European Central Bank (ECB) last week announced it would take almost anything as collateral.

Not to dredge up bad memories, but it's all very reminiscent of what happened in the days surrounding the Bear Stearns collapse. A run on the bank is very emotional and panic-driven, and can spark unfortunate and unexpected consequences. It's nothing to be taken lightly.

Closing Thoughts

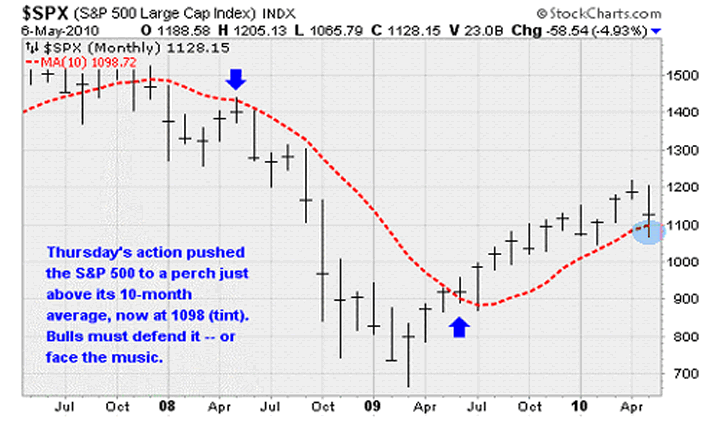

As you can see in the chart below, the Thursday action pushed the monthly bar of the Standard & Poor's 500 Index below the 10-month average, which is now 1,098. That's the line in the sand that bulls must defend, and I think they will - much as they did in similar circumstances in 2004. If they don't, more than likely the advance out of the March 2009 low will be invalidated, we'll be back in the land of the bears, and you'll want to be out of all equities.

The best-case scenario now would be some more churning around current levels - a bit higher, a bit lower, possibly a test of the Thursday low and a test of the Wednesday high - that ultimately ends with the S&P 500 moving back above its 20-day average. Then we'll recommend getting fully long again for a move at least back to the April high. The worst-case scenario, well, that's pretty obvious.

If you want to get long something in the event of a rally, then go for high-beta stocks and funds that were down the most in the past week, such as materials and steel. Also the energy master limited partnerships that pay big income yields, such as Plains All American Pipeline (NYSE: PAA) and Kinder Morgan Energy LP (NYSE: KMP) are probably good buys on their recent declines. They pay 7% annual dividends.

If you want to short the market in anticipation of a return to the bearishness of 2008, or at least until all the sales of last week are sorted out, then the best looking and most liquid ones at this time are our old friend from 2008, ProShares UltraShort Financials (NYSE: SKF), ProShares UltraShort Europe (NYSE: EPV) and ProShares UltraShort China (NYSE: FXP).

The Week in Review

Monday: The ISM Manufacturing Index continued to accelerate in April, coming in at 60.4 versus the 59.6 reading in March. Still, this was slightly below Wall Street expectations. The new orders remained very strong, coming in at 65.7. Production is rising along with new orders, jumping seven points to 66.9 for its best reading in six years. Separately, consumer spending continued to increase in March.

Tuesday: Pending home sales zoomed higher in March as the April expiration of the homebuyer tax credit loomed. It'll be interesting to see what happens to the sales numbers now that the credit has expired.

Wednesday: The ISM Non-Manufacturing Index was flat month-to-month but remains in expansionary territory at 55.4.

Thursday: Initial weekly jobless claims came in just under expectations at 444k. Initial claims have been stuck in a range between 440k and 500k since last October. We need to see some progress on this front soon. The good news is that there are other signs of strength in the labor market: Nonfarm productivity jumped 3.6% in the first quarter, down from the 6.3% surge in Q409. Unit labor costs also fell at a slower pace. Reduced productivity and stabilization in labor costs all suggest employers will need to start hiring soon -- and they'll need to pay more to get talent. This is good news for consumer spending and the economy at large.

Friday: The April payroll report showed an increase of 290k for the best one-month result since early 2006. The unemployment rate increased slightly as discouraged laborers returned to the workforce.

The Week Ahead

Monday: No major economic releases.

Tuesday: Two reports on weekly chain store sales will be released.

Wednesday: The Mortgage Bankers Association will release their purchase applications index. Also, we'll get an update on the foreign trade balance.

Thursday: Federal Reserve chairman Ben Bernanke will participate in a Q&A session at the Philadelphia Federal Reserve Bank.

Friday: Updates on retail sales, industrial production, consumer sentiment, and business inventories.

[Editor's Note: As this market analysis demonstrates, Money Morning Contributing Writer Jon D. Markman has a unique view of both the world economy and the global financial markets. With uncertainty the watchword and volatility the norm in today's markets, low-risk/high-profit investments will be tougher than ever to find.

It will take a seasoned guide to uncover those opportunities.

Markman is that guide.

In the face of what's been the toughest market for investors since the Great Depression, it's time to sweep away the uncertainty and eradicate the worry. That's why investors subscribe to Markman's Strategic Advantage newsletter every week: He can see opportunity when other investors are blinded by worry.

Subscribe to Strategic Advantage and hire Markman to be your guide. For more information, please click here.]

Source :http://moneymorning.com/2010/05/10/stock-market-panic/

Money Morning/The Money Map Report

©2010 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or 72 hours after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.