Small Investors Rush Into Junk Bonds, Where is the Fiduciary Responsibility?

Interest-Rates / International Bond Market May 19, 2010 - 04:40 AM GMTBy: Mike_Shedlock

Burnt by the stock market too many times to count, small investors have been herding into junk bonds instead. Indeed, the mad rush into junk continues even as debt covenants weaken and fund managers are skeptical.

Burnt by the stock market too many times to count, small investors have been herding into junk bonds instead. Indeed, the mad rush into junk continues even as debt covenants weaken and fund managers are skeptical.

My rant is coming up. First consider Junk Bonds Sell With Weakest Creditor Protection Since 2007.

Two years after suffering $213.2 billion of losses when debt markets froze, investors in junk bonds are accepting what Moody’s Investors Service calls the weakest creditor protections since 2007.

Even with housing starts hovering at their lowest levels on record, Beazer Homes USA Inc. managed to sell bonds this month on terms that allow it to add more debt. The Atlanta-based builder couldn’t even do that when it issued debentures at the height of the housing bubble in 2006 and its credit rating was seven levels higher. In a report last week Moody’s singled out CF Industries Inc., Standard Pacific Corp., AK Steel Corp. as borrowers offering debt on terms historically available only to higher-rated companies.

“We got ourselves in trouble with that in the past and here it is again,” James Kochan, the chief fixed-income strategist at Wells Fargo Fund Management in Menomonee Falls, Wisconsin, said of the trend toward looser debt covenants. “It’s not that surprising, but it is disturbing,” said Kochan, who helps oversee $179 billion.

Money managers say they have little choice but to go along. They need to find a home for the record $29.4 billion that has flowed into high-yield bond mutual funds the past 16 months from retail investors seeking to join in a rally that has produced an average 69 percent return since the market bottom in March 2009.

“This trend represents more than an episode of ‘back to the future,’” Moody’s analysts including Alex Dill, the firm’s senior covenant officer, wrote in their report. “It reflects a weakening in covenant protections even below those existing at the peak of the market, in 2006 and 2007.”

Cash is flowing into mutual funds that specialize in high-yield debt at an accelerating pace. EPFR Global, a research firm in Cambridge, Massachusetts, estimates that before last week, investors put $8.57 billion into the funds, up from $7.33 billion in the same period of 2009.

“In 2008, all the companies that we said would screw the bondholders did it,” said Cohen of Covenant Review. “Now, it feels like 2007 to me. We’re telling them they’re going to get screwed and they’re not paying attention.”Pool of Greater Fools About to Run Dry

There's lots more in the article to read, including a look at homebuilder Beazer Homes.

With junk bonds, the greater fool of investing is still alive and well, but I doubt it lasts much longer.

Credit defaults swaps in Europe gave one warning signal already, declining yields in the US Treasury market is another warning, a strengthening US dollar is a third, and for good measure China's Shanghai Index $SSEC is a fourth warning signal.

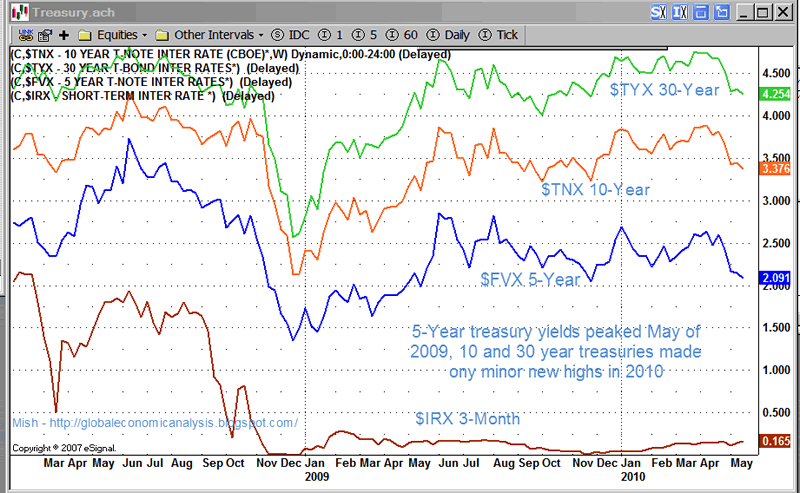

If the US was in the midst of a recovery, 10-year treasury yields would not be at 3.39 and falling. Note that the yield on 5 year treasuries peaked in May of 2009, while the yield on 10-year and 30 year treasuries only made marginal new highs in 2010.

The chart below shows weekly closing highs. There were higher spikes mid-week.

Yield Curve 2010-05-18

It was just a few weeks ago everyone seemed to think 10-year yields of 6% or more was on the way. To me, 3% or even 2.5% seems more likely.

Where is the fiduciary responsibility?

OK. Time for the rant.

James Kochan, the chief fixed-income strategist at Wells Fargo Fund Management who helps oversee $179 billion said of the trend toward looser debt covenants “We got ourselves in trouble with that in the past and here it is again. It’s not that surprising, but it is disturbing.”

The article goes on to say, "Money managers say they have little choice but to go along. They need to find a home for the record $29.4 billion that has flowed into high-yield bond mutual funds ..."

That last statement was not attributed to anyone specifically. However, it is clearly part of the problem. Where is the fiduciary responsibility? Where?

Yes, Virginia, There is a Choice!

Of course there is a choice. If a fund manager does not think he can wisely invest fund flows, then he should not take them.

The correct choice is to say, "We think this market is fully priced, we do not like the risk-reward setup, and we advise treasuries, or sitting in cash, or whatever."

I heard many horror stories from people whose managers said they were willing to go to cash. In 2008 none of them did.

Wells Fargo, Fidelity, Vanguard, etc., all offer a whole range of products, none of them giving any discretion to the fund manager. The money comes in, the managers put 100% of it to work collecting a fee for his services, even if the manager thinks the market is primed for a huge drop.

A friend told me his experience at a large brokerage firm that had 500 managed account programs consisting of the usual gamut of garbage: big cap, small cap, mid cap, emerging markets, blends, various grades of bonds, foreign equities, a dozen blends, energy, bio, semiconductors, tech, ad nauseum.

All 500 strategies had one thing in common: They were all 100% long 100% of the time. There was not one alternative strategy that allowed shorting or hedging or simply taking half the chips off the table if the risk reward setup was unfavorable.

Why is this?

Fee Structure Offers Managers Huge Incentive To Do Wrong Thing

Part of the problem is the fee structure system itself. Typically clients only pay fees when the money is invested. Thus, there is a huge incentive to "invest" whether it makes any sense or not, even in cases the manager is pretty sure it is wrong.

The second problem is, if the manager does not take the money, it will go somewhere else.

To that I say, so what?

Ultimately the only choice is to always act in the best interest of the client, even if that means sending them somewhere else, not accepting new funds, or sitting in cash waiting for better opportunities.

Putting money to work, even though a manager thinks “We got ourselves in trouble with that in the past and here it is again" is precisely one of the things blatantly wrong with Wall Street. Unfortunately, that attitude is all too commonplace. Don't expect it to change anytime soon.

This is my second rant on the subject. In case you missed it, please see Rant of the Day: No Ethics, No Fiduciary Responsibility, No Separation of Duty; Complete Ethics Overhaul Needed.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2010 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.